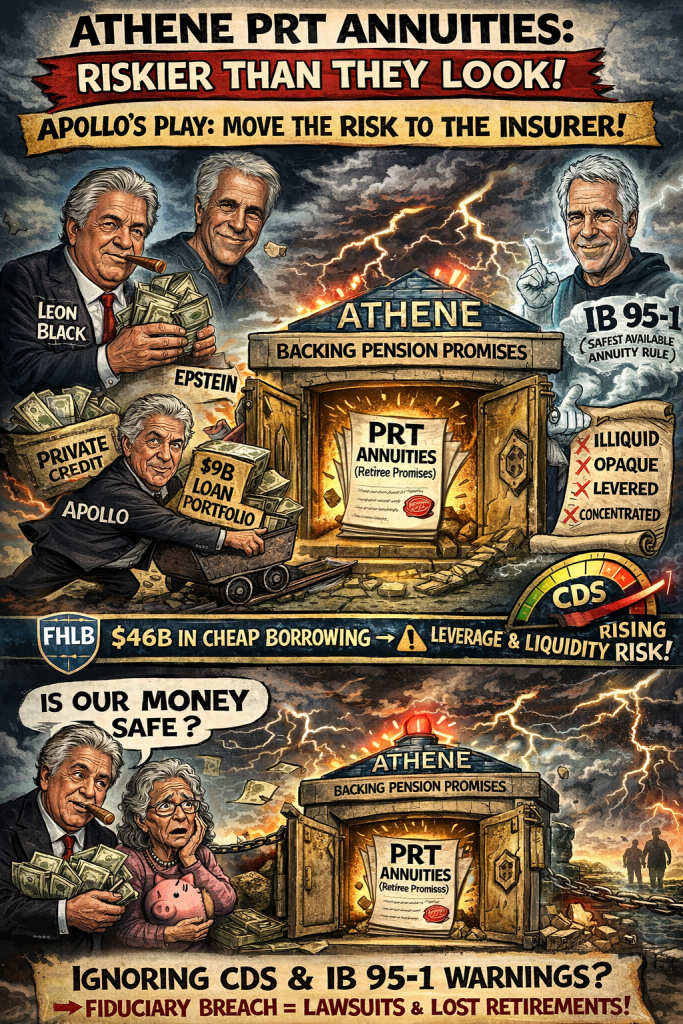

PRT annuities depend on one thing: The long-term financial strength of the insurer. But now that insurer Athene is: Increasing leverage via FHLB, Absorbing large real estate loan portfolios, Exposed to private credit stress, and Operating under prior regulatory violations

Athene paid a $45 million penalty for improper PRT activity in April 2020, after an investigation found its pension risk transfer (PRT) business had solicited and placed group annuity contracts with an unlicensed subsidiary. The Department of Financial Services cited violations of New York Insurance Law, noting the subsidiary had entered into 14 large-scale pension risk transfer transactions involving thousands of New York policyholders. https://www.dfs.ny.gov/reports_and_publications/press_releases/pr202004132

The American Federation of Teachers and the American Association of University Professors filed a complaint letter to the SEC on Apollo that specifically mentions Athene.

I believe your decision re only paying 20m has frankly, left me felling quite uneasy, colors my view about the Athene or Rothschild transaction. ……Athene,income, capital,foreign, exit, corporate, insurance regs, out and inbound issues, basis, appropriate discount rates. ? …….We can talk about Rowen request re Athene, complex 2 billion in taxes on transaction. ?

Rowen refers to Apollo CEO Marc Rowen who previously filed an SEC report in which he claimed no contact with Epstein or his involvement with Apollo issues like Athene.

Rising CDS spreads (market signaling higher credit risk) Renewed scrutiny from Epstein-related disclosures and Ongoing litigation risk at Apollo and the conclusion becomes unavoidable: The risk profile of Athene-backed annuities is increasing—not decreasing.

Apollo says Athene’s access to cheap government-backed FHLB funding makes annuities safer. In reality, it allows them to load more risk onto the balance sheet that retirees depend on. The $9 billion commercial real estate loan transfer isn’t a sign of strength. It’s a signal that the risks of private credit and real estate are being quietly shifted into the very entity that is supposed to guarantee pension benefits.

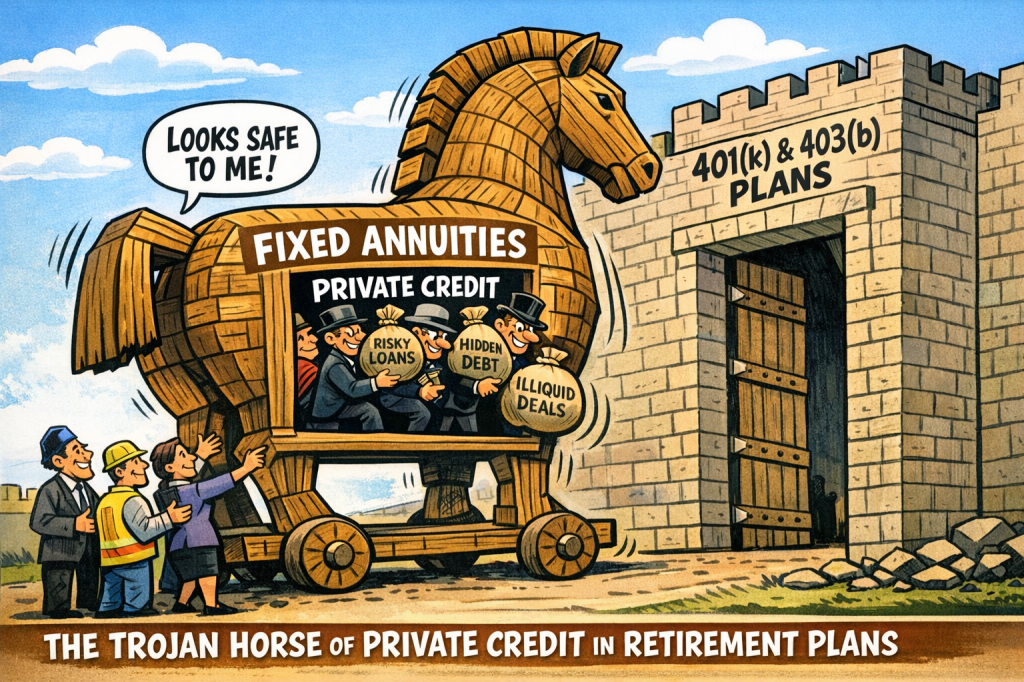

Wall Street keeps telling regulators, lawmakers, and plan sponsors that private credit in 401(k) plans is coming. That is the distraction. Private credit is not coming. It is already here. And not in the place anyone is debating.

Roughly 98% of all private credit exposure inside 401(k) and 403(b) plans already sits inside one product: fixed annuities—buried inside insurance company general accounts where participants cannot see it, price it, or escape it. Of the 9000 401(k) and 403(b) plans with over $100 million in assets, over 3500 hold fixed annuities. For the over 700 thousand plans, probably half hold fixed annuities https://commonsense401kproject.com/2026/01/23/fixed-annuities-are-the-dirty-secret-hiding-in-401k-and-403b-plans/

The real scandal is not future allocations to private markets. It is the massive, undisclosed private credit exposure already embedded in the system today.

The Misdirection: Target Date Funds with “Future” Private Credit, and Lifetime Annuities

The current policy debate focuses on whether private equity or private credit should be allowed inside target date funds. There is also a huge push for Lifetime Income Annuities

But today:

Actual direct private credit exposure inside target date funds is minimal to negligible

Lifetime income annuity adoption remains tiny with very low balances

Most participants have no direct allocation at all

This is not where the risk is. This is narrative management. Some bait and switch pushing lifetime annuities, knowing that any rules encouraging them will make it easier to retain fixed annuities.

Synthetic Funds like Fidelity MIPS and Vanguard RST, and products from T.Rowe Price, Galliard, Invesco, are transparent diversified and do not contain private credit.

Public pension trustees still think the Apollo problem is reputational. It isn’t.

It has now become regulatory, legal, and financial—at the same time.

And the window to act voluntarily is closing fast. Since the February 1st Financial Times of London story dropped was soon followed by a SEC complaint by AFT and AAUP unions on February 12, and stock drop cases filed the next week after Apollo stock tanked over 35%, losing nearly $20 billion in value.

Apollo Is No Longer “Headline Risk”—It Is a Systemic Risk

For years, pensions were sold a carefully constructed narrative:

Leon Black’s relationship with Jeffrey Epstein was “personal”

The Apollo facts have become harder and harder for fiduciaries to wave away. In the February 17, 2026 SEC complaint from AFT and AAUP, the unions asked the Commission to investigate whether Apollo’s prior disclosures about its and its executives’ ties to Jeffrey Epstein painted an “inaccurate and incomplete picture.” Their letter pointed to newly released Epstein documents referring to Marc Rowan, including meetings at Apollo’s offices, breakfasts involving Rowan, Leon Black, and Epstein, discussions of donor-advised funds, tax matters, a possible Apollo inversion, and other business-related contacts. The letter concluded that the 2021 disclosures may have offered “an inaccurate depiction of the extent of Apollo’s ties with Jeffrey Epstein” and said the SEC should investigate whether the statements were materially false or misleading.

That matters enormously for pension fiduciaries. In 2019 and again in 2021, many institutional investors were told, in substance, that the Epstein problem at Apollo was largely personal to Leon Black and was being cleaned up. The new AFT-AAUP complaint directly challenges that sanitized version, arguing that the public record now suggests a broader and deeper institutional relationship. Whether the SEC ultimately agrees is not the point. The point is that pensions are on notice that the old comfort story may no longer hold. Once fiduciaries have credible notice that a manager may have mischaracterized material relationships, continuing to invest without a serious re-underwriting of the manager becomes its own governance failure.

Apollo co-founder Joshua Harris admitted at a 2013 meeting of the Philadelphia Board of Pensions that the firm’s capital base was overwhelmingly dependent on public retirement systems. Asked directly whether Apollo had many public pension investors, Harris responded bluntly that “almost all” of Apollo’s capital came from public funds, estimating that roughly 75% to 80% of Apollo’s capital was supplied by public pension plans. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

The UN Human Rights Office is looking into Jeffrey Epstein’s files as a transnational “global criminal enterprise. Many US pensions have signed onto the UN Global Compact on Human Rights. Investment firms like Apollo have signed, which could lead to divestment. https://news.un.org/en/story/2026/02/1166980

This is no longer a contained issue. It is expanding across disclosure, governance, and labor fronts simultaneously.

Once fiduciaries are on notice that: disclosures may have been inaccurate, governance failures may be deeper than represented and Epstein-related ties may have been broader than disclosed the legal standard changes. Trustees no longer get to say: “We didn’t know.”

Congress has already shown its hand. They aimed it at ESG specially the Environmental. But the logic doesn’t care about politics. Apply it to Apollo around Governance. Holding Apollo could endanger the IRS tax status of the plan.

Apollo’s stock collapse is not a side issue. It is confirmation. Between January and early March 2026, Apollo’s stock fell sharply wiping out tens of billions in market value.

That decline did three things at once:

1. Converted Governance Risk into Financial Loss

This is no longer theoretical.

Public pensions now hold:

Apollo private equity and private credit (paying fees and likely hidden losses)

Apollo stock (APO taking huge losses 2026)

Apollo REIT (ARI -26% last 5 years)

They are simultaneously: clients and victims

2. Triggered Securities Litigation

This type of decline automatically triggers:

stock-drop lawsuits

securities fraud claims

institutional investor recovery actions

This creates a direct fiduciary obligation: Pensions must evaluate whether to pursue recovery.

3. Exposed an Irreconcilable Conflict

Pensions now face a contradiction they cannot explain:

suing Apollo (as shareholders)

while allocating billions to Apollo (as clients)

Or worse:

not suing at all—because of the conflicted relationship of Apollo secret no-bid contracts

That is the exact type of conflict regulators look for.

What They Cannot Do

They cannot:

stay invested

keep paying fees

ignore the stock collapse

ignore SEC complaints

ignore labor violations

and claim they are acting solely in beneficiaries’ interest. That position is no longer credible.

Apollo is no longer just a controversial manager. It is now a litigation event embedded inside every public pension portfolio.

Which leads to only one defensible conclusion: Divest now—while it is still a choice.

Because the next phase is not voluntary. It will be driven by courts,regulators or Congress

And by then, trustees will not be asked whether they acted. They will be asked: Why they didn’t.

List of Plans with Apollo Funds

Alaska Permanent Fund Apollo PE funds

Arizona PSPRS Apollo PE funds

California Public Employees’ Retirement System (CalPERS) Apollo Investment Fund VI and related vehicles

California State Teachers’ Retirement System (CalSTRS) Apollo Investment Funds VI, VII, IX, X; Hybrid Value II

Chicago Teachers Pension Fund 2024 performance confirms Apollo PE/PC as manager

Colorado PERA Apollo Investment Funds III,IV,V,VI, VII, Distresssed DIF

Colorado School Apollo Credit Opp III & DIF

Connecticut Retirement Plans & Trust Funds Apollo Investment Fund VIII

Florida State Board of Administration Apollo PE funds IV, V PC Accord V and VI

Georgia Teachers Retirement System

Idaho PERSI Apollo PE funds

Illinois Teachers Retirement System Apollo PE funds X

Illinois Municipal Apollo Credit Wilshire

Indiana Public Retirement System (INPRS) Apollo Origination Partnership

Iowa Public Employees Retirement System Apollo PE funds Wilshire

Kansas Public Employees Retirement System Apollo PE funds VIII,IX

Kentucky Teachers Apollo REIT & Apollo Stock

Los Angeles City Employees’ Retirement System (LACERS) Apollo PE funds VI

Los Angeles (CA) Water and Power has PE fund X

Louisiana Teachers’ Retirement System of Louisiana (TRSL), Apollo Credit, Natural Resources

Maryland State Retirement & Pension System ?PE funs

Massachusetts PRIM Apollo PE funds

Michigan RS Apollo Investment fund VIII, IX Hybrid Value Funds, Credit/ Opportunistic Credit

Minnesota State Board of Investment Apollo/Athene Dedicated Investment Program II

Mississippi PRS Apollo VIII IX Private Equity funds

Montana Board of Investments Stock holdings?

Nebraska Investment Council India Property Fund II LLC.

New Hampshire Retirement System Apollo PE funds

New Jersey Division of Investment: Stock holdings?

New Mexico State Investment Council Apollo PE VII, VIII PC

New York City Teachers’ Retirement System Apollo PE funds

New York City (NY) ERS PE $500mm 2013

New York City (NY) Police PE fund VI

New York State Apollo PE VIII

North Carolina Retirement Systems Apollo PE funds VI, VII

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Oregon PER recently comitted $300mm to Apollo distressed debt fund as well as earlier funds like Apollo PE IX

Pennsylvania PSERS Apollo PE funds IV $620mm

Pennsylvania SERS Apollo PE funds VI- VIII

Rhode Island Retirement System Apollo PE VIII, IX

San Diego City Employees Retirement System Apollo PE funds

San Francisco (SFERS) San Francisco Employees’ Retirement System Apollo PE funds Wilshire

South Carolina RS $750mm

South Dakota Retirement System Apollo PE funds

Texas County & District PE fund X

Texas ERS Apollo Credit Strategies

Texas Municipal Fund VIII

Texas TRS Teachers’ Retirement Apollo PE funds

Tennessee Consolidated Retirement System Stock holdings?

San Francisco Employees’ Retirement System Apollo PE funds

San Diego City Employees’ Retirement System Apollo PE funds

University of Calfiornia PE VII, VIII Principal Wilshire

Virginia Retirement System Apollo PE funds

Washington State Investment Board (WSIB) Apollo S3 Equity & Hybrid

Wisconsin (SWIB) Apollo Credit

Appendix: Senator Wyden’s Findings on Apollo Founder Leon Black

In a March 20, 2026 letter, Senator Ron Wyden details extraordinary financial dealings between Apollo co-founder Leon Black and Jeffrey Epstein, including $170 million in payments between 2012 and 2017—amounts far exceeding what Black paid elite law firms for similar estate planning work. Wyden notes that, according to a U.S. Virgin Islands settlement, Epstein used money paid by Black to help fund his sex trafficking operations, raising serious questions about whether these payments were truly for legitimate services . The letter highlights newly unsealed Department of Justice records suggesting the arrangement “went well beyond” traditional tax or estate planning and may have involved undisclosed or improper purposes. https://www.finance.senate.gov/imo/media/doc/senator_wyden_letter_to_leon_black_redacted.pdf

Wyden further raises concerns about potential financial misconduct, including evidence that payments to Epstein may have been channeled through a questionable 501(c)(3) structure to maximize tax deductions, and that Black’s estate planning arrangements involved $141 million in overpayments tied to Apollo-related partnership interests. Additional records cited in the letter suggest Epstein may have acted as an intermediary for payments to women and was involved in activities far removed from legitimate advisory services. Taken together, the Senate Finance Committee’s findings underscore that the Apollo–Epstein relationship is not merely historical—it presents unresolved questions about financial integrity, governance, and compliance that remain directly relevant to fiduciaries evaluating continued investment exposure. https://www.finance.senate.gov/continuing-epstein-investigation-wyden-questions-leon-black-over-new-revelations-in-epstein-files-appearance-of-hush-money-payments-and-surveillance-of-women

From an FTX-funded Super PAC to pro-crypto legislation, the money trail behind one Indiana congresswoman shows how the industry buys influence before it sells risk to retirees

It didn’t happen in a vacuum. It happened after the crypto industry quietly built political allies—one race at a time. And in southern Indiana, no figure better represents that strategy than Erin Houchin—a congresswoman whose rise to power was boosted by crypto-linked money and whose political positioning now aligns almost perfectly with the industry’s most aggressive expansion goals.

Call it what it is: the making of Indiana’s Queen of Crypto.

The Origin Story: FTX Money in a Southern Indiana Primary

Houchin’s path to Congress runs straight through one of the most notorious financial scandals of the modern era.

In her 2022 Republican primary, a little-known super PAC—American Dream Federal Action—suddenly flooded Indiana’s 9th District with ads supporting her candidacy. That spending was decisive. It helped propel Houchin past her rivals and into Congress.

But here’s what voters were not told at the time: That PAC was funded entirely by Ryan Salame, a senior executive at FTX. Not a diversified donor base. Not grassroots support. One man. One checkbook. One crypto insider.

And that story only got worse with time. Federal prosecutors later charged Salame with campaign finance violations tied to a broader scheme involving illegal political contributions connected to the FTX empire. He ultimately pleaded guilty and was sentenced to prison.

The political machine that helped elect a sitting member of Congress in Indiana was funded by a man who later admitted to breaking federal election laws tied to crypto money.

Her breakthrough victory was materially assisted by money from the inner circle of one of the largest financial frauds in history.

Round Two: The Crypto Money Doesn’t Stop

The story doesn’t end with FTX. After entering Congress, Houchin continued to show up in the same financial ecosystem. Campaign finance data shows contributions tied to Andreessen Horowitz, the Silicon Valley powerhouse heavily invested in crypto infrastructure, exchanges, and token platforms. Different players. Same industry.

And at the same time, Houchin’s political positioning became unmistakable. She aligned with the pro-crypto legislative push in Washington, including support for industry-backed frameworks like the CLARITY Act, and she has been publicly embraced by crypto advocacy groups such as Stand With Crypto, which labels her a “strongly supportive” candidate.

.

From Campaign Money to Retirement Policy

Indiana recently became the first state in the country to effectively mandate access to crypto investments inside retirement plans—a historic shift that exposes workers to one of the most volatile and least regulated asset classes ever created.

“It is fiscally irresponsible to allow state pension funds to be opened up to such risk simply because we want to send a message that the Indiana House of Representatives is supportive of the crypto industry,” said Rep. Ed DeLaney (D-Indianapolis) in a statement “If state funds are invested in cryptocurrency and that investment goes bad, the state still has an obligation to pay for those pensions https://indianapolisrecorder.com/house-bill-1042-crypto-investment/

This did not happen by accident. It happened in a political environment where:

Crypto money had already influenced elections

Pro-crypto lawmakers had already been elevated

The industry had already gained a foothold in policy conversations

And lawmakers like Erin Houchin were already in place.

The Real Risk: Turning 401(k)s Into Crypto Distribution Channels

The final step in this process is the most dangerous.

Once crypto enters retirement plans—whether through brokerage windows, target-date funds, or collective investment trusts—it stops being a speculative side bet and becomes a default exposure for ordinary workers.

The same industry that used political money to gain influence is now positioning itself to capture retirement assets at scale.

The Political Reality: Influence First, Accountability Later

There is no need to prove a direct quid pro quo to understand what is happening.

The sequence tells the story:

A crypto-funded PAC boosts a candidate

The donor later pleads guilty to campaign finance violations

The candidate enters Congress

The candidate aligns with crypto-friendly policy

The state moves to integrate crypto into retirement systems

That is not coincidence.

That is a pipeline of influence.

Conclusion: Indiana as the Test Case for a National Problem

Indiana is not just another state experimenting with financial innovation. It is the first clear example of how crypto moves: From campaign finance To political legitimacy To retirement plan integration

And at the center of that story sits Erin Houchin—the “Queen of Crypto”

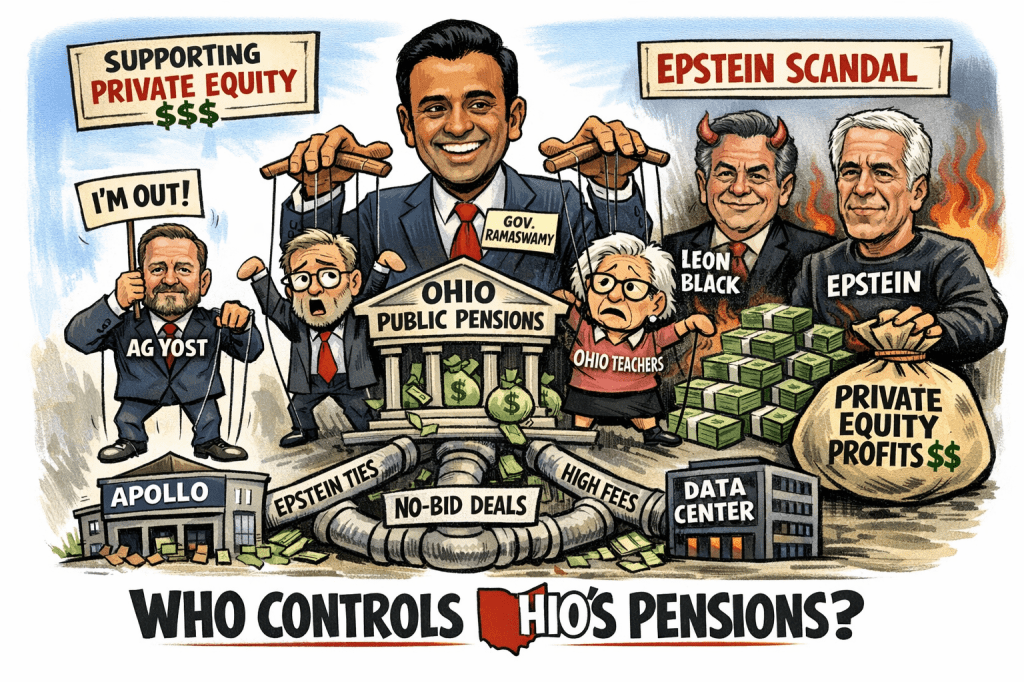

There is a growing effort across the country to scrutinize—and in some cases divest from—private equity firms entangled in conflicts, secrecy, and scandal. Nowhere is that pressure more justified than with Apollo Global Management, whose documented ties to Jeffrey Epstein and reliance on public pension capital have triggered renewed calls for accountability. https://commonsense401kproject.com/2026/03/10/jeffrey-epstein-funder-leon-blacks-apollo-bleeds-public-pensions-of-6-billion-a-year-through-secret-no-bid-contracts/ But in Ohio, that effort is likely to collide head-on with a potential governor whose financial roots and policy instincts are deeply aligned with the very system under scrutiny: Vivek Ramaswamy.

Ramaswamy is often marketed as a biotech entrepreneur, but the deeper story is one of private equity alignment. A significant portion of his wealth traces not to traditional operating businesses, but to data monetization platforms like Datavant, which was backed and scaled by New Mountain Capital. This is not incidental—it is emblematic. Datavant sits at the intersection of private equity, data extraction, and long-duration capital structures, the same ecosystem that increasingly dominates public pension portfolios.

That ecosystem depends heavily on state and local pension systems for capital. In Ohio, that includes both the Ohio Public Employees Retirement System and State Teachers Retirement System of Ohio—multi-billion-dollar funds that have allocated significant assets to private equity managers, including Apollo and its affiliated credit vehicles. As documented in prior analysis, these investments are often executed through opaque, no-bid contracts with layered fee structures that can exceed 500–600 basis points annually when fully loaded.

The political question is simple: would a Governor Ramaswamy support divestment from firms like Apollo in light of their Epstein ties, fee extraction, and governance concerns? The financial answer is far more revealing: it is highly unlikely.

Ramaswamy’s economic worldview is not merely tolerant of private equity—it is structurally dependent on it. His alignment extends beyond passive investment exposure into active policy advocacy. He has publicly supported the expansion of data center infrastructure—an asset class increasingly dominated by private equity and private credit vehicles, including those tied to Apollo. These data centers are not neutral infrastructure plays; they are fee-generating machines financed by the same pension capital that bears the downside risk.

This creates a reinforcing loop: public pensions allocate to private equity → private equity finances data centers and data platforms → political actors aligned with those interests promote further expansion → pension capital becomes even more dependent on the same opaque structures.

Ramaswamy’s involvement with Strive Asset Management adds yet another layer to this conflict. Strive positions itself as a challenger to ESG-driven investing, but in practice, it operates as a gatekeeper—advising and influencing pension allocations in Republican-controlled states such as Indiana. This is not a passive role. It places Strive—and by extension Ramaswamy—directly in the flow of pension capital decisions, including allocations to private equity managers.

In other words, the same individual who could oversee Ohio’s pension systems has already built a business model around influencing where those systems invest. That is not reform. That is vertical integration.

If Ohio’s pensions were to seriously consider divesting from Apollo or similar firms—whether due to Epstein-related governance concerns, hidden fee structures, or the growing risks in private credit—such a move would run directly counter to the financial architecture that underpins Ramaswamy’s own wealth and network. And that is before considering the broader systemic risk.

Private equity’s expansion into private credit, insurance balance sheets, and data infrastructure has created what can only be described as a shadow financial system—one that avoids mark-to-market discipline, obscures true fee levels, and concentrates risk in ways that are difficult for beneficiaries to see and even harder for fiduciaries to challenge. Ohio’s pensions are deeply embedded in this system.

A governor aligned with private equity is not going to unwind that exposure. He is far more likely to defend it. The result is a potential collision between fiduciary duty and political economy. Beneficiaries—teachers, public workers, retirees—have a right to demand transparency, competitive bidding, and independence from conflicted intermediaries. But those demands threaten a system that has become extraordinarily profitable for private equity firms and their political allies. The Apollo-Epstein controversy is not just a reputational issue. It is a stress test of whether public pension systems can act independently of the financial and political networks that influence them.

The Political Consolidation Behind Private Equity Power in Ohio

The political landscape in Ohio has already shifted in a way that reinforces—not challenges—the private equity status quo. When Dave Yost exited the 2026 gubernatorial race, it was not a neutral event. It effectively cleared the field for Vivek Ramaswamy, consolidating Republican political power behind a single candidate aligned with private equity interests. Yost’s withdrawal came immediately after the Ohio Republican Party endorsed Ramaswamy, turning what he described as a difficult path into a “vertical cliff” and eliminating meaningful intra-party opposition.

This matters for one reason: it removes one of the last potential institutional checks on how Ohio’s public pension capital is deployed. Because the stakes are not abstract. As documented in Epstein, Apollo, and Ohio Teachers’ Billions, https://commonsense401kproject.com/2026/02/23/epstein-apollo-and-ohio-teachers-billions/ Ohio’s largest pension systems—particularly State Teachers Retirement System of Ohio—have already committed billions to private equity structures tied to Apollo Global Management and its affiliates. These allocations are not passive index exposures. They are embedded in opaque, illiquid vehicles with limited transparency, no competitive bidding, and fee structures that can extract extraordinary value from beneficiaries over time.

The Epstein connection is not a historical footnote—it is a governance red flag. Apollo’s co-founder Leon Black was documented as having extensive financial ties to Jeffrey Epstein, raising serious questions about oversight, fiduciary judgment, and counterparty risk at the exact firms entrusted with public pension assets.

And yet, despite this, there has been no serious political push in Ohio to re-evaluate or unwind these relationships.

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Yost’s exit helps explain why. With the Republican field consolidated behind Ramaswamy—and with additional statewide officials and party infrastructure aligning in the same direction—the probability of a coordinated effort to investigate, much less divest from, Apollo or similar private equity firms drops dramatically.

Instead, what emerges is something far more concerning: political consolidation that mirrors financial concentration. Ohio’s pensions are already heavily allocated to private equity. Now the political leadership overseeing those pensions is converging around a candidate whose personal wealth, business ventures, and advisory networks are deeply intertwined with that same ecosystem. That is not a coincidence. It is alignment. And for beneficiaries—teachers, public employees, retirees—it raises a fundamental question: if both the capital and the political oversight are concentrated within the same private equity orbit, who exactly is left to challenge the system?

Ramaswamy will keep all the Apollo funds in Ohio

In Ohio, voters have a new option by voting for Amy Acton for Governor. Acton is more likely to support divestiture

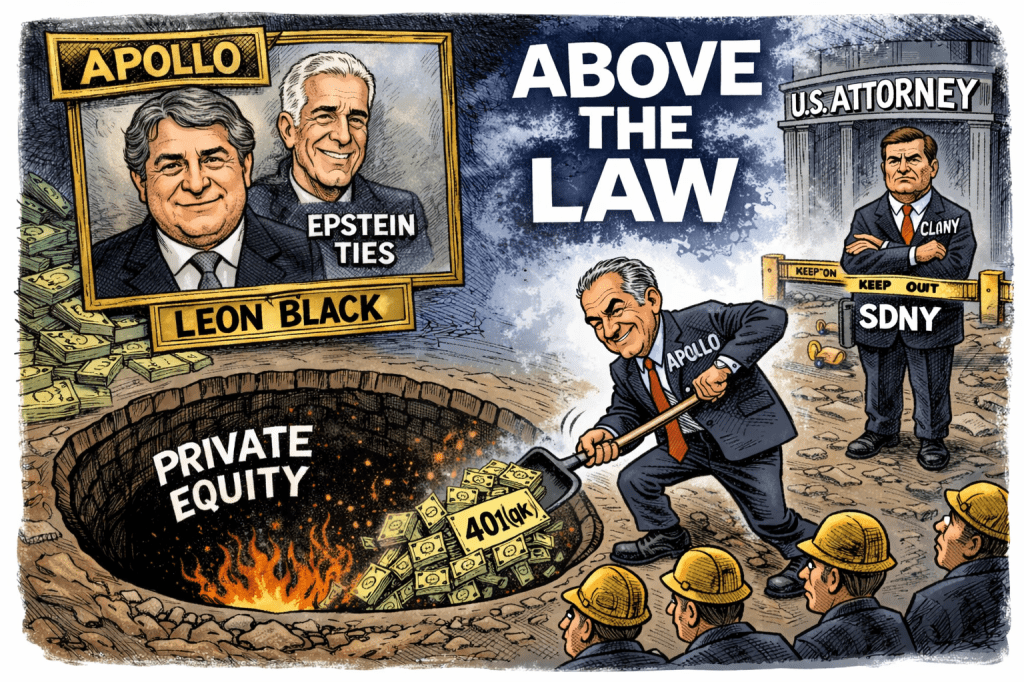

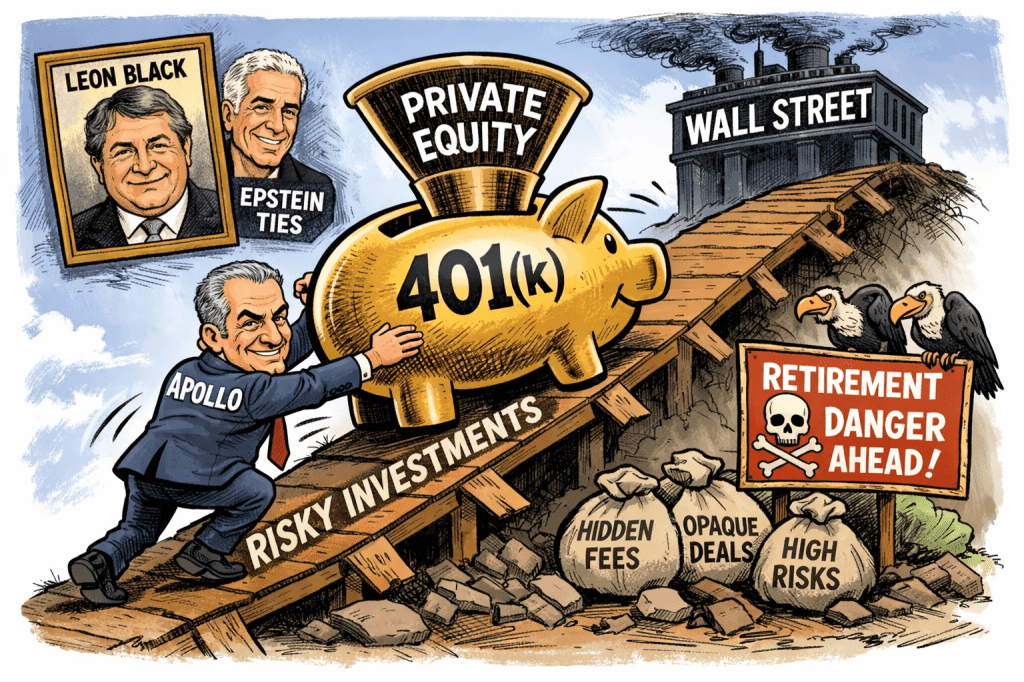

There are scandals on Wall Street. And then there is Apollo Global Management. Apollo was co-founded by Leon Black, the billionaire who paid convicted sex trafficker Jeffrey Epstein $158 million for mysterious “tax advice.” That relationship detonated into one of the ugliest scandals in modern finance and ultimately forced Black to step down as CEO. Yet despite that disgrace, Apollo remains deeply embedded in the American financial and political system. This is on top of a long history of scandals and violations with the SEC, EPA, and others.

Apollo CEO Marc Rowan is now leading the private-equity industry’s push to move trillions of dollars from 401(k) plans into opaque private assets. The sales pitch is dressed up in the language of “democratizing private markets.” But the reality is much simpler. Private equity needs fresh capital. Institutional investors are increasingly questioning fees, illiquidity, and performance. So Wall Street, led by Apollo, is now targeting the largest untouched pool of money in the country — American workers’ retirement savings.

And the political doors are wide open. Rowan has become one of the most influential financiers in Washington and was recently named to President Trump’s advisory structures related to Gaza reconstruction and governance. That alone should make people uncomfortable. But the deeper problem is the extraordinary web of influence surrounding Apollo and the agencies that are supposed to police it.

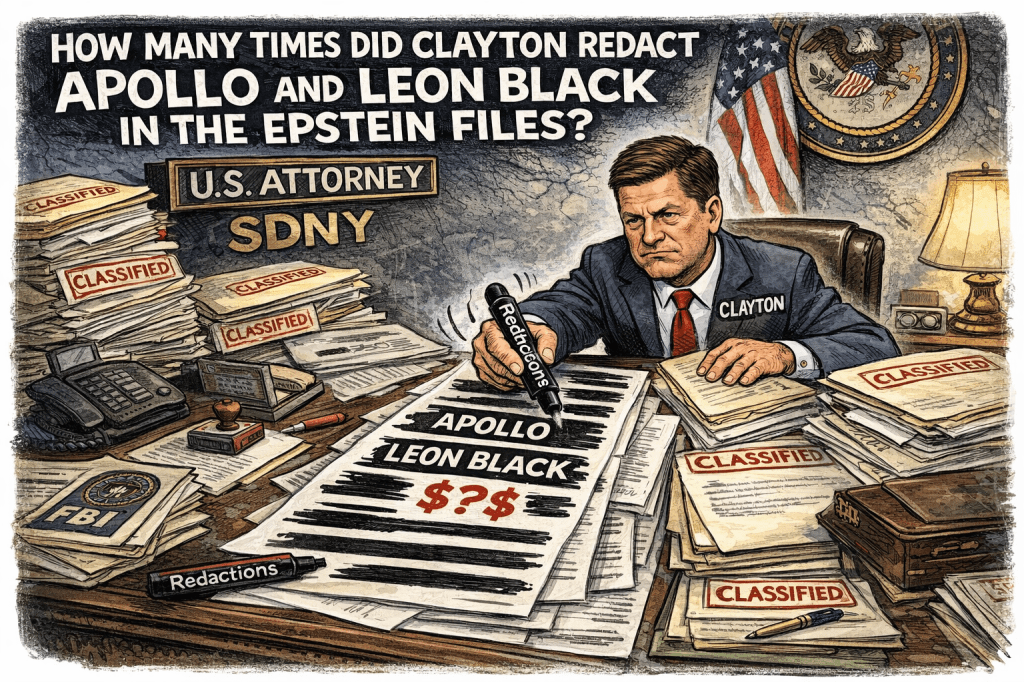

Consider the man now running the most powerful financial crime prosecutor’s office in the country. Jay Clayton, the U.S. Attorney for the Southern District of New York — the office that historically prosecutes Wall Street corruption — previously served as chairman of Apollo’s board. According to reporting by The Lever, Clayton still holds more than $1 million in Apollo investments.

What is worse, Attorney General Pam Bondi put Clayton in charge of the redactions of the Epstein files. My question is how many redactions did he make that involved Apollo and Leon Black? Pam Bondi has a long history with Apollo, hiring them to manage hundreds of millions for the Florida Retirement System when she was a trustee of that Pension.

Think about that for a moment. The top federal prosecutor in Manhattan has deep financial ties to a private-equity firm whose founder’s Epstein relationship remains the subject of lawsuits and investigations. The office that prosecuted Jeffrey Epstein now has a leader financially connected to the firm founded by Epstein’s most famous billionaire client. On top he was assigned by the US Attorney General to oversee redactions of millions of files, where he had numerous conflicts.

Meanwhile, the scandals keep coming. In February, Epstein file disclosure (maybe the one in a hundred Clayton missed) emails showing CEO Marc Rowan’s involvement with Epstein and that Epstein provided advice to Apollo, in contrast to SEC documents filed in 2021. In March 2026, Apollo, Leon Black, and Marc Rowan were sued by shareholders who alleged the firm had misled investors for years about its relationship with Epstein. The lawsuit claims Apollo’s filings falsely denied doing business with Epstein, even though he allegedly played a significant role in advising senior leadership.

Apollo has built a vast empire extracting fees from public pension funds through secretive, no-bid contracts, opaque valuation methods, and complex structures that hide the true cost of private equity and private credit. As much as 85% of their assets come from taxpayer funds. As documented in prior reporting, the firm’s fee machine likely drains billions of dollars annually from public retirement systems.

And now Apollo wants the next frontier. Your 401(k). The plan is straightforward. Private equity firms partner with asset managers to build collective investment trusts, target-date funds, and hybrid products that quietly insert private assets into retirement portfolios. Workers will be told they are receiving “diversification.” What they are actually receiving are illiquid assets priced by models, surrounded by multiple layers of fees, and wrapped in disclosures almost no participant can understand. It is a perfect system for Wall Street. Daily pricing in 401(k)s becomes fiction. Transparency disappears. Benchmarking becomes meaningless. And the fees — always the fees — continue flowing upward.

For decades, private equity thrived because public pensions provided patient capital with limited scrutiny. Now even those investors are asking questions about performance and fee extraction. So the industry is hunting for something better. Captive capital. A 401(k) participant cannot negotiate terms. They cannot demand transparency. They cannot fire the manager running the fund inside their target-date product.

If a firm was built by a billionaire who secretly paid Jeffrey Epstein $158 million… If that firm’s executives are currently being sued for allegedly concealing Epstein ties… If the nation’s top Wall Street prosecutor previously chaired that firm and still holds financial stakes in it…Why in the world would anyone allow that firm to manage workers’ retirement savings?

Public pensions should divest from Apollo. Regulators should scrutinize every contract the firm holds. And Congress should slam the door on the private-equity industry’s attempt to convert America’s 401(k) system into the next extraction machine.

Because if Apollo and the rest of the private-equity industry succeed, the Epstein scandal will end up being remembered not as the moment Wall Street cleaned house — but as the moment it realized it could get away with almost anything.

Wall Street never stops looking for a new pool of captive money. Now Apollo Global Management — the firm long shadowed by Jeffrey Epstein through co-founder Leon Black — is pushing to move deeper into America’s 401(k) system under CEO Marc Rowan. That push is no longer theoretical. Reuters reported in August 2025 that Rowan publicly welcomed an expected Trump administration move to channel more retirement assets into private markets, saying he believed the industry was “on the cusp” of serving the 401(k) and defined-contribution marketplace and that regulatory changes to make this easier were “common sense.”

The timing could hardly be more revealing. In February 2026, Apollo and Schroders announced a partnership that includes a collective investment trust for the U.S. defined-contribution market, targeted for launch in the second quarter of 2026. Schroders was recently purchased by TIAA division of Nuveen. Empower also set up deals with Apollo to put private assets into 401(k)s. Reuters and Apollo’s own announcement described the project as a retirement product blending public and private exposures for the defined-contribution channel. In other words, Apollo is not merely cheering from the sidelines. It is building the distribution pipe.

This is exactly the danger. Private equity has always depended on opacity, delayed pricing, layered fees, insider-friendly contracts, and benchmarks that can be manipulated or custom-built. Those features are a scandal in a public pension. In a retail 401(k), where workers are told they have daily liquidity and transparent account values, they become something worse: a structural mismatch between what participants are shown and what they actually own. Your March 6 piece makes that point directly — that private equity often survives in retirement plans only when buried inside more complex wrappers where participants cannot see the contracts, compensation, or valuation mechanics clearly.

That is why the political and regulatory backdrop matters so much. On August 7, 2025, the White House issued an executive order explicitly aimed at “democratizing access” to alternative assets in 401(k) plans and directed the Labor Department and SEC to facilitate that access. The Department of Labor then issued Advisory Opinion 2025-04A in September 2025, expanding the room for products housed in variable annuities, CITs, and pooled vehicles to qualify within QDIA-type structures. At the same time, SEC Commissioner Mark Uyeda gave a November 2025 speech urging broader access to private markets in defined-contribution plans. The direction of travel has been unmistakable: open the gates, soften the guardrails, and normalize illiquid, hard-to-price products in retirement plans built for ordinary workers.

But disclosure has not kept pace — not remotely. Your February 2026 comment letter to DOL laid out the core defect: participants often are not given full look-through holdings, underlying manager identities, layered fees, affiliate relationships, embedded insurance exposures, or even clarity about who regulates the product. As you wrote there, electronic delivery cannot solve a substantive transparency failure; it merely “accelerates opacity.” That criticism applies with even greater force to private-equity-laced CITs and hybrid retirement products.

The accounting problem is just as severe. In my “4 Sets of Books” piece, I noted that private assets inside 401(k)s are commonly valued using Level 3 inputs and often priced by managers or appraisers chosen by managers. That means the same firms collecting the richest fees are often closest to the marks participants are asked to trust. The more private assets migrate into 401(k) structures, the more retirement savers will be forced to rely on numbers that are neither market-clearing nor independently testable in real time.

And this is where Apollo’s own credibility problem becomes impossible to ignore. Just last week, Reuters reported that Apollo, Leon Black, and Marc Rowan were sued by shareholders who allege they concealed business ties to Jeffrey Epstein for years. Reuters also reported in February that Apollo publicly stated Rowan had no business or personal relationship with Epstein as scrutiny intensified. Whether Apollo ultimately prevails in that litigation is not the point here. The point is simpler and more devastating: one of the firms most aggressively seeking access to America’s retirement savings is simultaneously defending itself against allegations that it misled investors about its Epstein-related business ties. That is not a due diligence green flag. That is a fiduciary siren.

This is why Marc Rowan’s “common sense” line should be turned on its head. Common sense says that a private-equity giant born in secrecy, enriched by hidden fee structures, and still engulfed in Epstein-related fallout should not be handed a new franchise over workers’ nest eggs. Common sense says that 401(k)s are not venture-capital pools, not valuation laboratories, and not a bailout mechanism for an industry desperate for fresh retail capital as institutional investors push back on fees, illiquidity, and disappointing net returns. Common sense says that if a product cannot survive full fee transparency, clear legal accountability, independent valuation, and easy participant comprehension, it does not belong in a retirement plan.

Apollo’s campaign is not about democratizing finance. It is about democratizing extraction. The private-equity industry sees trillions sitting in 401(k)s and wants in. Marc Rowan is trying to lead that march. Fiduciaries, regulators, unions, and participants should say no — before workers discover too late that their retirement plan has become just another permanent-capital vehicle for Wall Street.

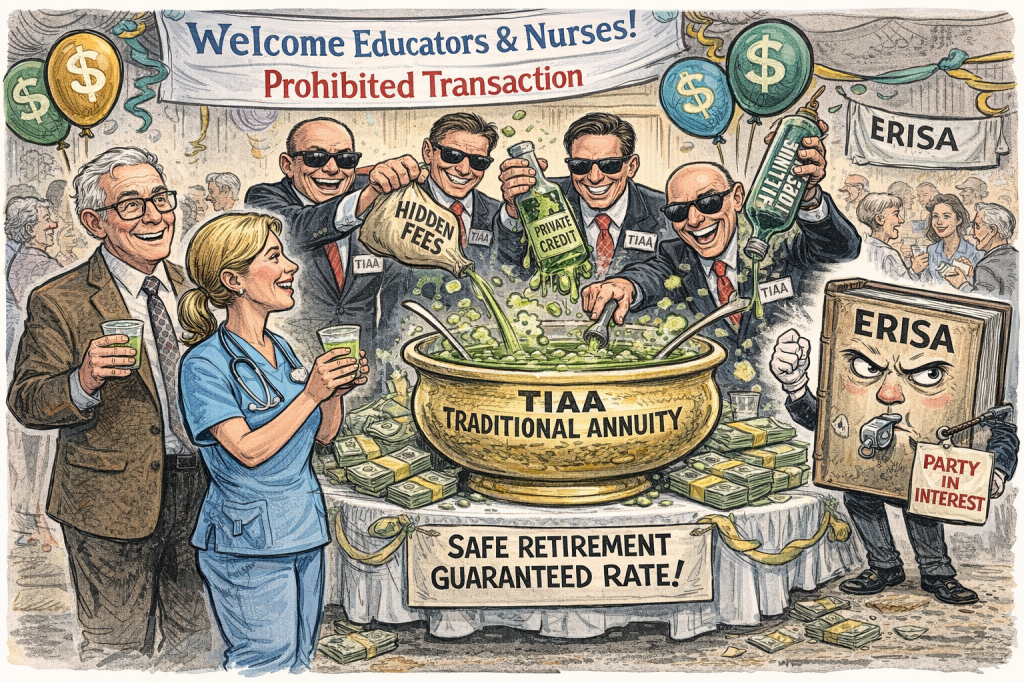

TIAA Traditional has long been marketed to professors, researchers, hospital workers, and nonprofit employees as the gold-standard “safe” retirement product. That sales pitch depends on one central illusion: that a general-account annuity can be treated like a conservative bond substitute when, in reality, it is a conflicted insurance product issued by the very financial institution profiting from the spread, controlling the crediting rate, and locking participants into liquidity restrictions they often do not understand until it is too late. TIAA’s own materials and even a favorable outside guide confirm the basic structure: TIAA Traditional is backed by TIAA’s General Account, not by a segregated portfolio owned by participants, and many contract forms restrict withdrawals to multi-year installment windows rather than true daily liquidity.

That matters far more after Cunningham v. Cornell. In April 2025, the Supreme Court held that ERISA plaintiffs alleging a prohibited transaction under §406(a) do not have to negate exemptions at the pleading stage; the Court specifically described TIAA and Fidelity as service providers and therefore parties in interest in the Cornell plans. In plain English, that means a fiduciary who causes plan assets to flow to TIAA through a conflicted annuity structure has stepped directly into prohibited-transaction territory unless TIAA or the fiduciaries can prove an exemption. The old defense playbook—forcing plaintiffs to plead around exemptions before discovery—has been badly weakened.

TIAA Traditional is exactly the sort of product that should trigger that scrutiny. The insurer sets the crediting rate. The insurer holds the assets on its own balance sheet. The insurer decides how much of the underlying yield to pass through and how much to retain. And the insurer has every incentive to preserve a hidden spread for itself. That is not arm’s-length pricing. That is not transparent compensation. It is the classic structure of a party in interest dealing with plan assets through a proprietary product whose economic terms are largely invisible to participants and, too often, to fiduciaries themselves. My September 2025 NB Cpiece put the hidden spread at roughly 120 to 150 basis points annually and noted that TIAA still would not disclose what it earns, calling the information “competitive and proprietary.” NBC’s 2024 investigation likewise reported whistleblower allegations that TIAA pushed higher-cost in-house products to shore up losses elsewhere, while the later Rhode Island reporting described participants trapped in opaque, illiquid TIAA products with undisclosed costs and little practical exit.

The conflict does not disappear because TIAA Traditional carries a guarantee. A guarantee from the same conflicted insurer is not a cure for conflicted dealing. It is part of the product being sold. And the positive review you pointed to, far from rebutting the prohibited-transaction case, actually reinforces it. The uploaded Scholar Financial guide explains that TIAA Traditional is backed by TIAA’s General Account; states that legacy RA and GRA contracts are “highly restricted”; and acknowledges that many withdrawals must be paid through a Transfer Payout Annuity in 10 annual installments, while Retirement Choice contracts may require 84 monthly installments. It also highlights that more liquid versions of the product usually offer lower crediting rates, which is simply another way of admitting that participants are being paid less or more depending on how much liquidity they surrender to TIAA. That is not a plain-vanilla fixed income investment. It is a proprietary insurance bargain in which TIAA prices the lockup, controls the spread, and captures the economics.

The balance-sheet risk is also far uglier than the marketing implies. TIAA says the General Account is invested mostly in public and private fixed income, high-grade commercial mortgage loans, Treasuries, high-yield fixed income, structured credit, and alternatives. Dr.Lambert and I published an article that compares the TIAA underlying portfolio to that of the Vanguard RST stable value fund. Vanguard holds 74% in high-quality (AA and above) rated securities, while TIAA only holds 12.5% in rated securities. While the Vanguard is nearly 96% liquid in public securities, the TIAA portfolio is only 48% liquid. Many of the AA fixed-income securities they tout are illiquid private credit and private mortgage contracts rated by 2nd-tier rating agencies. https://www.tandfonline.com/doi/full/10.1080/00213624.2026.2613361

It is a massive, opaque insurer portfolio with material exposure to precisely the sectors—private credit, structured credit, commercial real estate, and illiquid fixed income—where price discovery can break down, and smoothing can mask deterioration. Participants are told they own something steady. In truth, they are depending on TIAA’s internal accounting, asset-liability management, and discretionary crediting decisions.

That is why the “low risk” story around TIAA Traditional is so misleading. As your January 2026 critique of TIAA’s target-date research argued, the product looks less volatile than bonds mainly because it is not marked to market; the risk is hidden on the insurer’s balance sheet while returns are smoothed through discretionary crediting. TIAA’s own consultant-facing materials continue to market TIAA Traditional as something that can “complement bonds” and improve portfolio stability, but that framing sidesteps the central fiduciary question. A plan fiduciary is not allowed to call something safe merely because the danger is hard to see. If a product concentrates participants in the credit risk of one insurer, pays undisclosed spread compensation to that insurer, and relies on opaque internal valuation and crediting practices, it is not a clean bond alternative. It is a conflicted insurance product.

The stable-value comparison is devastating for TIAA. As you argued in your March 2026 and December 2025 pieces, diversified synthetic stable value is structurally different because it typically relies on diversified underlying fixed-income holdings and wrap contracts rather than a single insurer’s general account. Even the industry has been forced to acknowledge that synthetic funds can be safer in important respects. Once that point is conceded, the legal problem for TIAA Traditional becomes harder to avoid. If fiduciaries have access to less-conflicted, more transparent, more diversified capital-preservation options, why are they steering participants into a proprietary general-account annuity issued by a party in interest that retains an undisclosed spread and imposes heavy liquidity restraints? That is exactly the sort of question §406 exists to force into daylight.

The defenders of TIAA Traditional will say the product has paid competitive credited rates for decades, has strong insurer ratings, and has served educators well. But none of those points resolves the ERISA problem. A prohibited transaction does not become lawful because it produced decent historical returns. Hidden compensation does not make one loyal merely because the counterparty is prestigious. And liquidity restrictions do not become prudent because some participants failed to read the contract. The issue is structural conflict: TIAA is on both sides of the deal. It designs the product, manages the balance sheet, sets the crediting rate, withholds the spread, and then asks fiduciaries to place retirement assets into that structure without full price transparency. That is the very type of self-interested arrangement ERISA was written to police.

NBC’s reporting should have ended the complacency. The 2024 whistleblower story alleged TIAA pushed costly proprietary products to cover losses elsewhere. The latter Rhode Island story showed what these structures can look like on the ground: workers stuck in products they cannot freely access, with costs and restrictions far murkier than the sales pitch suggested. Put that together with the Court’s recognition in Cunningham that TIAA is a party in interest, and the legal theory becomes straightforward. When ERISA fiduciaries place plan assets into TIAA Traditional, they are not merely selecting a conservative retirement option. They are causing the plan to transact with a conflicted insurer through a proprietary annuity contract whose compensation is opaque, whose liquidity is restricted, and whose risks are hidden behind insurance accounting. That is why TIAA Traditional should be analyzed not as a benign “guaranteed” option, but as a prohibited transaction waiting to be litigated.

The real scandal is that TIAA’s aura of public-mindedness still disarms scrutiny. For generations, TIAA wrapped itself in the language of education, service, and retirement security. But ERISA does not have a nonprofit halo exception. It does not excuse undisclosed spread extraction because the logo looks trustworthy. It does not permit fiduciaries to ignore single-entity credit concentration because the insurer has a long history. And after Cunningham, it no longer makes sense to pretend that party-in-interest status is some technical sideshow. TIAA Traditional is a general-account annuity sold by a party in interest, with hidden spread economics, heavy liquidity limitations, and opaque balance-sheet risk. That is not merely imprudent. Under a faithful reading of ERISA, it is prohibited.

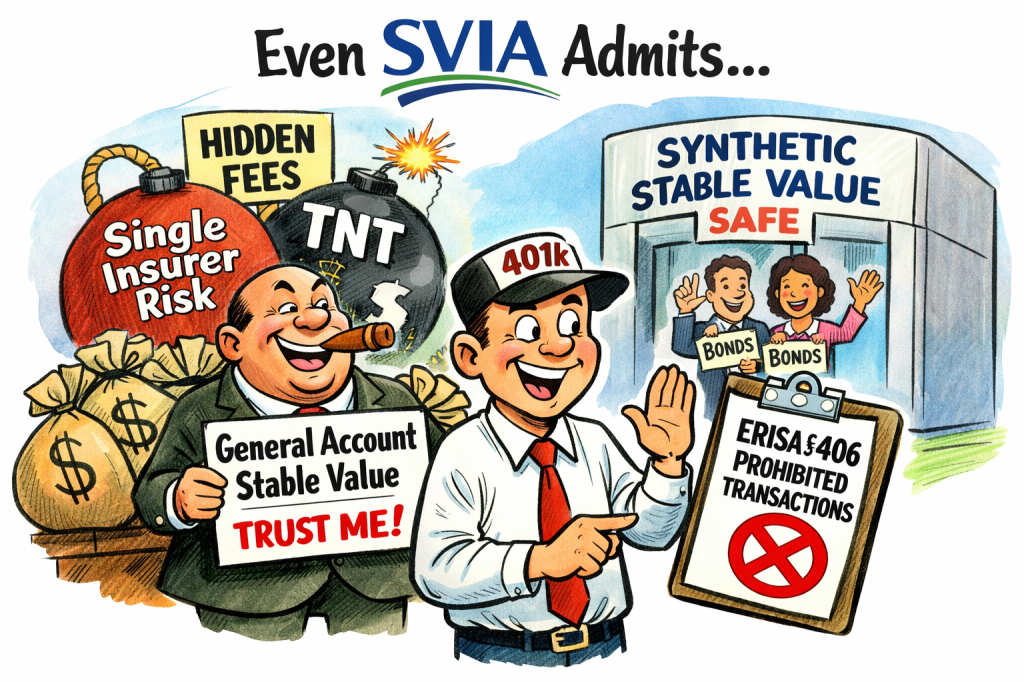

The stable value industry’s own trade association inadvertently exposes the structural problem with general-account fixed annuities in retirement plans. I agree that these lawsuits against low-risk diversified synthetic-based stable value are baseless and harmful.

In recent amicus briefs filed in federal ERISA litigation, the Stable Value Investment Association (SVIA) explains that stable value products fall into several very different categories. Synthetic stable value products—individually managed accounts and pooled funds—hold the underlying bond portfolios directly for the benefit of the retirement plan. Insurance company products, by contrast, are issued and guaranteed by a single insurance company and backed by that insurer’s general account. https://www.stablevalue.org/svia-and-u-s-chamber-of-commerce-file-amicus-brief/

That seemingly technical distinction is the entire ballgame. In a synthetic stable value structure, the retirement plan owns the underlying assets—typically diversified portfolios of high-quality bonds—and insurance “wrap” providers merely guarantee book-value liquidity. The plan therefore, retains ownership of the portfolio and diversifies credit risk across many issuers.

In a general-account annuity, the plan owns nothing. The assets are commingled with the insurance company’s liabilities and participants become general creditors of the insurer. Their retirement security therefore, depends on the solvency of a single financial institution.

This difference is not subtle. It is a fundamental transformation of a retirement plan asset into an insurance company liability. The SVIA briefs also acknowledge another crucial difference: compensation structures. Synthetic stable value funds typically charge explicit, disclosed fees, while insurance company products often compensate themselves through an undisclosed “spread” between the insurer’s investment earnings and the crediting rate paid to participants.

That spread structure creates a classic ERISA prohibited transaction. Under ERISA §406, a fiduciary may not cause the plan to engage in a transaction that allows a service provider to receive undisclosed or excessive compensation from plan assets. Yet the spread in a general-account annuity is not negotiated as a transparent fee. Instead, the insurer keeps whatever investment earnings exceed the declared crediting rate, a figure that participants and fiduciaries often cannot observe or benchmark.

In other words, the insurance company is simultaneously:

the issuer of the product,

the manager of the assets,

the counterparty to the contract, and

the party determines its own compensation.

No independent market mechanism exists to test whether that spread is reasonable. The SVIA briefs further note that general-account products are “offered and guaranteed by a single insurance company.” That means participants bear concentrated exposure to one insurer’s credit risk, while the insurer captures the upside from investing the assets.

Synthetic stable value does the opposite. Credit risk is diversified across many bonds and multiple wrap providers, fees are disclosed, and the plan retains ownership of the portfolio.

In short:

Structure

Asset Ownership

Credit Risk

Fees

Synthetic Stable Value

Plan trust owns bonds

Diversified

Explicit

General Account Annuity

Insurer owns assets

Single insurer

Hidden spread

The insurance industry likes to present general-account products as “guaranteed.” But the guarantee is only as strong as the issuing insurer. History provides many reminders—from Executive Life to more recent insurance failures—that these guarantees are far from risk-free.

From a fiduciary perspective, the problem is not simply that general-account annuities carry more credit risk. The problem is that they combine opaque compensation, single-entity credit exposure, and self-dealing by the product issuer.

Those characteristics are precisely the types of conflicts ERISA’s prohibited-transaction rules were designed to prevent.

Synthetic stable value products demonstrate that another structure is possible—one where the plan retains ownership of the assets, fees are transparent, and risks are diversified.

Which raises the obvious question fiduciaries should be asking:

If a transparent, diversified structure exists, why place retirement assets into opaque general-account contracts where the insurer controls the assets, determines its own compensation, and concentrates credit risk in a single institution?

Under ERISA’s strict prohibited-transaction framework, that question may eventually have a simple answer. Because they never should have been there in the first place.

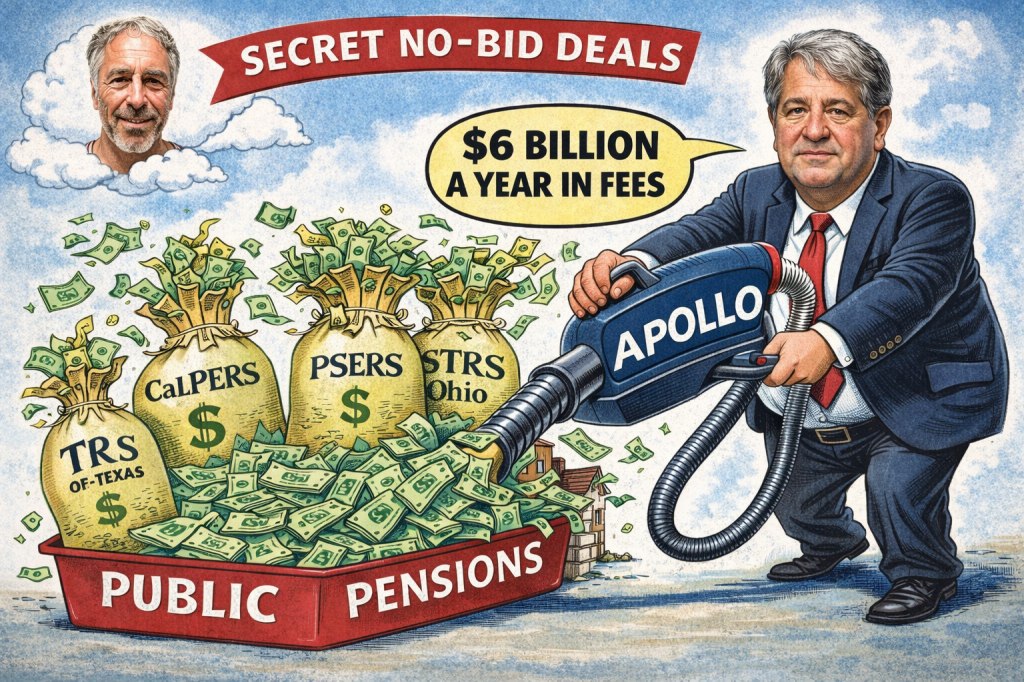

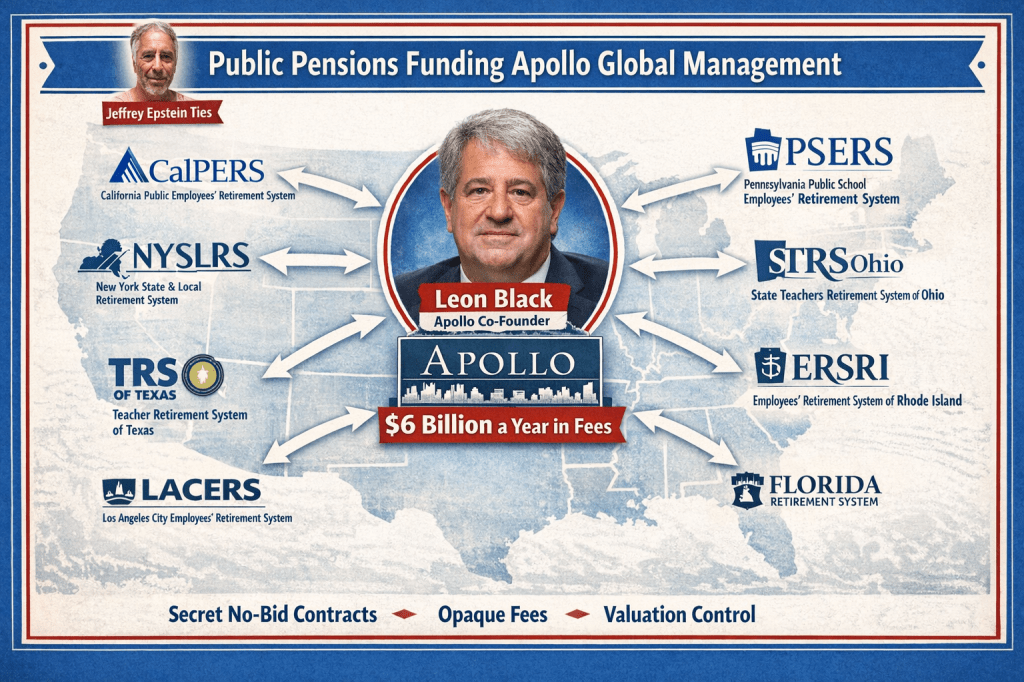

Public pensions across the United States may be paying as much as $6 billion a year to Apollo Global Management through a web of secret private equity and private credit contracts that most beneficiaries, taxpayers, and often even trustees themselves are never allowed to see. That estimate is not pulled out of thin air. It comes from combining two facts the industry would rather not discuss at the same time.

First, Apollo co-founder Joshua Harris admitted at a 2013 meeting of the Philadelphia Board of Pensions that the firm’s capital base was overwhelmingly dependent on public retirement systems. Asked directly whether Apollo had many public pension investors, Harris responded bluntly that “almost all” of Apollo’s capital came from public funds, estimating that roughly 75% to 80% of Apollo’s capital was supplied by public pension plans. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

Second, academic research by Oxford finance professor Ludovic Phalippou has repeatedly estimated that the true economic cost of private equity—including management fees, carried interest, transaction fees, monitoring fees, and portfolio-company charges—can reach 600 basis points annually, or roughly 6% of invested capital.

If public pension plans collectively have roughly $100 billion invested with Apollo, applying Phalippou’s cost estimate produces a staggering result: roughly $6 billion per year flowing from public retirement systems to one private equity firm. Even if the estimate is imprecise, the order of magnitude is the point. These are not marginal fees. They represent a massive transfer of retirement wealth from teachers, firefighters, public employees, and ultimately taxpayers to Wall Street managers operating under contracts that remain hidden from the public whose money is at stake.

And those contracts raise serious legal questions. During my time as a trustee of the Kentucky Retirement Systems, I repeatedly asked to see the private equity partnership agreements governing these investments. Like many trustees across the country, I was told they were confidential. Trustees responsible for billions of dollars of public pension assets were effectively asked to approve investments whose governing legal documents could not be publicly disclosed.

Only through a rare discovery process during a federal investigation was I able to obtain a number of these contracts. In 2014 I provided eleven of them to Naked Capitalism’s trove archive, and around the same time, the Pennsylvania pension system accidentally disclosed twelve private equity agreements, including the Apollo Investment Fund VIII Limited Partnership Agreement. https://trove.nakedcapitalism.com/LPAs/verified-as-LPAs/Apollo_Investment_Fund_VIII_LPA_S1.pdf The industry response was immediate: the documents were quickly pulled down after Apollo became aware of the disclosure. Fortunately, the files were captured during a brief window and preserved.

Those documents revealed what public pension beneficiaries are normally forbidden to see.The Apollo contract shows a structure that places enormous power in the hands of the general partner while sharply limiting oversight by investors. Valuation authority rests largely with the manager itself. Broad indemnification provisions protect the firm from liability except in cases of extreme misconduct. The agreement allows Apollo to operate parallel vehicles and affiliated funds while maintaining discretion over allocations across them. So called Advisory boards exist but are mostly boondoggles to wine and dine pension staff so they keep their secrets. https://www.bloomberg.com/authors/AR2mdR8I6A4/neil-weinberg

In other words, the manager holds the authority, the protections, and the conflicts—while the pension system holds the capital and the risk. I believe this would be found to be illegal in many states. This structure is not accidental. It is precisely why the contracts must remain secret. Public pension funds are not private investors deploying personal wealth. They are public trust funds, governed by state constitutions, fiduciary statutes, and procurement rules designed to protect taxpayer resources. Trustees of these systems have a duty to act solely in the interest of beneficiaries and to manage funds prudently and transparently.

Yet private equity allocations frequently bypass the procurement safeguards that apply to almost every other form of public spending. Instead of competitive bidding or documented market comparisons, staff and consultants typically recommend a specific private equity fund and negotiate privately with the manager. The board is then presented with a take-it-or-leave-it opportunity framed as a limited investment window.

In effect, multi-billion-dollar investment mandates are awarded through secret no-bid contracts.

In any other context involving public funds—construction projects, infrastructure contracts, or technology procurement—such arrangements would immediately trigger investigations into favoritism or corruption. But in the world of private equity, this process has become routine.

The secrecy itself may conflict with state open-records laws and fiduciary obligations. Pension assets are public trust funds, and fiduciaries generally cannot bind those assets under contracts that prohibit disclosure of the governing terms. Yet private equity partnership agreements routinely contain confidentiality provisions preventing the public from seeing fee structures, conflict provisions, valuation policies, and indemnification clauses.

When beneficiaries cannot see the contracts governing their retirement money, meaningful accountability disappears.

The valuation provisions in these contracts are particularly troubling. Private equity managers typically retain substantial control over how portfolio assets are valued. Those valuations determine reported performance, and performance determines both carried interest and the ability to raise new funds. When the same party that profits from strong valuations also controls the valuation process, the conflict of interest is obvious.

Under traditional fiduciary law, trustees are expected to maintain independent oversight over the valuation of trust assets. Delegating that authority to a counterparty whose compensation depends on the outcome would normally raise serious red flags. Yet in private equity, that structure has become standard practice.

Broad indemnification provisions compound the problem. Many LPAs shield the general partner from liability except in cases of extreme misconduct, limiting investors’ ability to pursue claims even if negligent decisions damage the fund. Public pension trustees generally cannot waive legal protections on behalf of beneficiaries in this way without careful justification.

Taken together, the secrecy, valuation control, indemnification protections, and absence of competitive procurement raise the possibility that many private equity contracts are inconsistent with the fiduciary duties imposed on public pension trustees under state law. But even if the legal issues were ignored, another problem looms.

Public pension funds appear increasingly reluctant to confront the true value of their private equity and private credit portfolios. As markets tighten and private credit defaults rise, there is growing evidence that many assets may be significantly overvalued. If these holdings were forced into the open market today, they might clear at 70 cents on the dollar or less, revealing billions in hidden losses.

The consequences of acknowledging those losses would be enormous. Funding ratios would decline. Consultants’ performance claims would collapse. And pension staff—many earning $300,000 or more annually with bonuses tied to reported investment performance—could see compensation sharply reduced or even face clawbacks. The incentives to delay recognition of those losses are therefore powerful.

Many pension trustees are appointed by political officials. Those officials operate in a post-Citizens United political environment where private financial firms, including Apollo and their executives, can legally contribute vast sums to political organizations and super PACs secretly. Whether or not such contributions influence pension investment decisions, the appearance of conflict is impossible to ignore.

Apollo, via its debt control of Gannett, controls the main state media in many of the markets, especially state capitols of the below-mentioned Public Pension Plans, like the Columbus Dispatch, Tallahassee Democrat, Springfield (IL) State Journal, Austin American-Statesman. Indianapolis Star, Des Moines Register, Topeka Capital-Journal, Lansing State Journal, Jackson Clarion-Ledger, The Providence Journal.

Apollo was founded by Leon Black, whose relationship with convicted sex trafficker Jeffrey Epstein ultimately forced Black to step down as CEO after it was revealed that he had paid Epstein more than $150 million for financial services. This caused serious divestiture talks in 2019 and 2020 that CEO Marc Rowan calmed by saying Epstein’s involvement was limited to Leon Black personally and that it was for tax advice. New Epstein files released in February 2026 document that Rowan was lying and that his and Apollos’ involvement with Epstein was extensive. The Teachers Unions AFT and AAUP have filed a complaint with the SEC and a civil class action has been filed against Apollo for lying about its Epstein involvement. www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf

Not because private equity is inherently illegitimate, and not because every Apollo investment has failed. But because fiduciaries cannot responsibly commit public retirement assets to opaque, no-bid contracts that place enormous power in the hands of private managers while denying transparency to the public whose money is at stake. Apollos recent issues around Epstein strain their credibility as a manager of public funds. https://commonsense401kproject.com/2026/02/05/the-apollo-epstein-files-why-public-pensions-should-reopen-the-2019-divestment-debate/

The longer pensions remain entangled in this system, the greater the risk that hidden losses, undisclosed conflicts, and legal challenges will eventually surface. When that day comes, retirees and taxpayers will ask a very simple question:

Why did no one act sooner?

A partial list of over 58 pensions that hold Apollo is below.

Alaska Permanent Fund Apollo PE funds

Arizona PSPRS Apollo PE funds

California Public Employees’ Retirement System (CalPERS) Apollo Investment Fund VI and related vehicles

California State Teachers’ Retirement System (CalSTRS) Apollo Investment Funds VI, VII, IX, X; Hybrid Value II

Chicago Teachers Pension Fund 2024 performance confirms Apollo PE/PC as manager

Colorado PERA Apollo Investment Funds III,IV,V,VI, VII, Distresssed DIF

Colorado School Apollo Credit Opp III & DIF

Connecticut Retirement Plans & Trust Funds Apollo Investment Fund VIII

Florida State Board of Administration Apollo PE funds IV, V PC Accord V and VI

Georgia Teachers Retirement System

Idaho PERSI Apollo PE funds

Illinois Teachers Retirement System Apollo PE funds X

Illinois Municipal Apollo Credit Wilshire

Indiana Public Retirement System (INPRS) Apollo Origination Partnership

Iowa Public Employees Retirement System Apollo PE funds Wilshire

Kansas Public Employees Retirement System Apollo PE funds VIII,IX

Kentucky Teachers Apollo REIT & Apollo Stock

Los Angeles City Employees’ Retirement System (LACERS) Apollo PE funds VI

Los Angeles (CA) Water and Power has PE fund X

Louisiana Teachers’ Retirement System of Louisiana (TRSL), Apollo Credit, Natural Resources

Maryland State Retirement & Pension System ?PE funs

Massachusetts PRIM Apollo PE funds

Michigan RS Apollo Investment fund VIII, IX Hybrid Value Funds, Credit/ Opportunistic Credit

Minnesota State Board of Investment Apollo/Athene Dedicated Investment Program II

Mississippi PRS Apollo VIII IX Private Equity funds

Montana Board of Investments Stock holdings?

Nebraska Investment Council India Property Fund II LLC.

New Hampshire Retirement System Apollo PE funds

New Jersey Division of Investment: Stock holdings?

New Mexico State Investment Council Apollo PE VII, VIII PC

New York City Teachers’ Retirement System Apollo PE funds

New York City (NY) ERS PE $500mm 2013

New York City (NY) Police PE fund VI

New York State Apollo PE VIII

North Carolina Retirement Systems Apollo PE funds VI, VII

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Oregon PER recently comitted $300mm to Apollo distressed debt fund as well as earlier funds like Apollo PE IX

Pennsylvania PSERS Apollo PE funds IV $620mm

Pennsylvania SERS Apollo PE funds VI- VIII

Rhode Island Retirement System Apollo PE VIII, IX

San Diego City Employees Retirement System Apollo PE funds

San Francisco (SFERS) San Francisco Employees’ Retirement System Apollo PE funds Wilshire

South Carolina RS $750mm

South Dakota Retirement System Apollo PE funds

Texas County & District PE fund X

Texas ERS Apollo Credit Strategies

Texas Municipal Fund VIII

Texas TRS Teachers’ Retirement Apollo PE funds

Tennessee Consolidated Retirement System Stock holdings?

San Francisco Employees’ Retirement System Apollo PE funds

San Diego City Employees’ Retirement System Apollo PE funds

University of Calfiornia PE VII, VIII Principal Wilshire

Virginia Retirement System Apollo PE funds

Washington State Investment Board (WSIB) Apollo S3 Equity & Hybrid