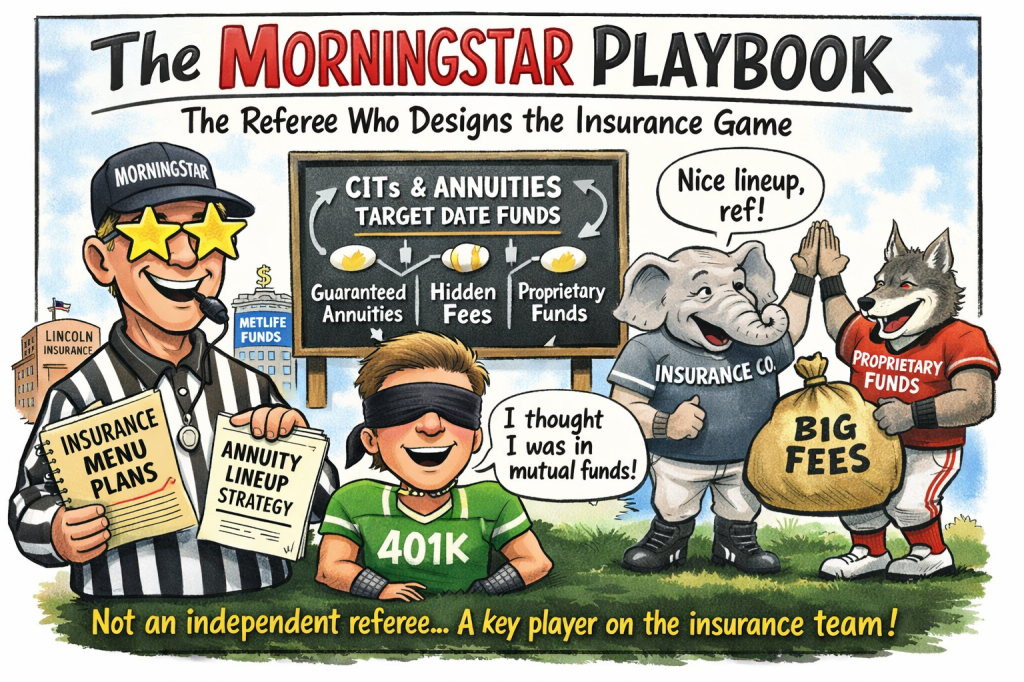

For years, Morningstar has positioned itself as the independent umpire of the mutual fund world.

The star ratings. The analyst reports. The fiduciary consulting.

If Morningstar approves it, fiduciaries feel safe.

But buried in Morningstar’s own SEC filings is something most plan sponsors, consultants, and courts do not realize:

Morningstar is deeply embedded in the business of helping insurance companies design retirement plan investment menus built around CITs, annuities, and proprietary insurance wrappers — the very structures now raising ERISA prohibited transaction concerns.

This isn’t speculation. It’s in their Form ADV.

Morningstar Retirement: Not What People Think

Morningstar Investment Management’s “Retirement” division does not simply analyze mutual funds.

They explicitly say they: “construct custom model portfolios for employer-sponsored retirement plans using the investment options available in a plan’s lineup.”

That sounds harmless — until you read the next sentence: “The universe of underlying holdings is generally defined by the Institutional Client and can include investment products that are affiliated with that Institutional Client.”

Translation: If Lincoln, MetLife, TIAA, Principal, Empower, or an insurance platform defines the menu, Morningstar builds portfolios using those proprietary insurance products.

They are not evaluating an open market of mutual funds. They are working inside insurer-defined universes.

The MetLife Smoking Gun

Morningstar has a dedicated ADV brochure for: “Advisory Services to MetLife ExpertSelect Program”

In this document, Morningstar openly states:

“We selected the menu of investment options available in the MetLife ExpertSelect Program from the universe of investments that MetLife is authorized to offer.”

They go further: “We do not review the annuity products in connection with the Program.”

Read that again. Morningstar — the supposed fiduciary expert — builds the menu but does not review the annuity products.

They also state: “The lineups we build are limited to a universe of mutual funds and other investment vehicles, such as CITs and guaranteed retirement income products such as annuities.”

So Morningstar’s job here is: Make insurance menus look like diversified retirement lineups.

The Target Date Angle Nobody Talks About

Morningstar also offers:

“Personal Target Date Fund Services” “Custom Model Portfolios” “3(21) and 3(38) fiduciary services”

But those services are constrained to: “the investment options available in the plan lineup.”

And those lineups, in insurance platforms, are:

CITs

Stable value

Separate accounts

Annuity sleeves

Proprietary trust wrappers

This is exactly the structure now showing up in TIAA, Lincoln, MetLife, and other insurance-based target date designs where:

The participant thinks they are in mutual funds, But they are inside insurance contracts.

Morningstar is often the firm paid to “monitor” and “approve” these lineups.

And Morningstar Gets Paid Very Well For This

Their fee schedules show:

2–15 basis points for institutional asset management

3–8 bps for fiduciary services

Minimums of $100,000 to $450,000

Special target-date and managed account fees

This is a huge revenue business tied directly to insurer retirement platforms.

They even disclose: “We receive direct or indirect cash payments from unaffiliated third parties for referring their services to other advisory firms or investors.”

And: “We provide compensation to Institutional Clients to provide marketing or educational support…”

This is not a passive ratings agency. This is an active participant in the insurance retirement ecosystem.

Why Their Articles Read the Way They Do

When Morningstar writes articles like:

“The hidden trend changing 401(k) plans”

“Target date fund trends”

They present the rise of CITs and insurance-based structures as innovation.

They never mention:

Prohibited transaction risk

Party-in-interest issues

Share class access problems

Insurance wrapper conflicts

Hidden spread compensation

Fiduciary benchmarking problems

Because this is the ecosystem they are paid to support.

There is a common thread running through what we are seeing in:

The media — where reporters struggle to explain why private equity results never quite match the story being told (see the NYT H-E-B piece you dissected),

The courts — where judges are beginning to realize that fake benchmarks and opaque reporting create fiduciary illusions (see your Intel analysis),

State governments — where pension reports in Kentucky, Chicago, North Carolina, Rhode Island and California show performance standards that would never be tolerated in public markets,

And now Vermont — where Tim McGlinn, CFA/CAIA, documents how the state is effectively misrepresenting private equity performance to the public.

This is not coincidence. It is not incompetence. It is a system.

A system in which private equity performance is engineered, narrated, benchmarked, and reported in ways that would be considered securities fraud if done in public markets.

And everyone involved gets paid to look the other way.

When performance is measured against something that cannot be owned, “outperformance” is meaningless. This does not hold up under careful application of ERISA fiduciary standards.

This is not just bad measurement. It is misleading disclosure.

Why This Is Systematic — Not Accidental

Look at who benefits:

Actor

Benefit from the deception

Private equity managers

Hide fees, control valuations, claim alpha

Pension consultants

Justify complexity, look sophisticated

Pension staff

Earn bonuses versus slow benchmarks

Politicians

Point to “outperformance” in reports

Media

Repeat the narrative without understanding mechanics

These structures survive because fiduciaries, consultants, and staff are compensated inside the system that benefits from the opacity. The deception is not loud. It is polite. Technical. Professional. Credentialed.

It is benchmark math, valuation timing, performance standards, and narrative framing.

Which makes it far more effective.

The Bottom Line

Tim McGlinn showed it in Vermont. The WSJ showed it when liquidity hit. Richard Ennis showed it nationally. CFA warned about it. Courts are starting to see it.

Private equity performance, as reported by pensions, is not a reflection of economic reality.

It is the product of:

Benchmark engineering,

Valuation lag,

Performance Standards (GIPS) avoidance,

Fee opacity,

Governance capture,

And incentives aligned to preserve the illusion.

This is not bad investing.

This is systematic performance deception.

And until pensions are forced to measure private equity against investable public benchmarks, full fee transparency, and GIPS-level standards, the numbers they report should be treated as marketing, not measurement.

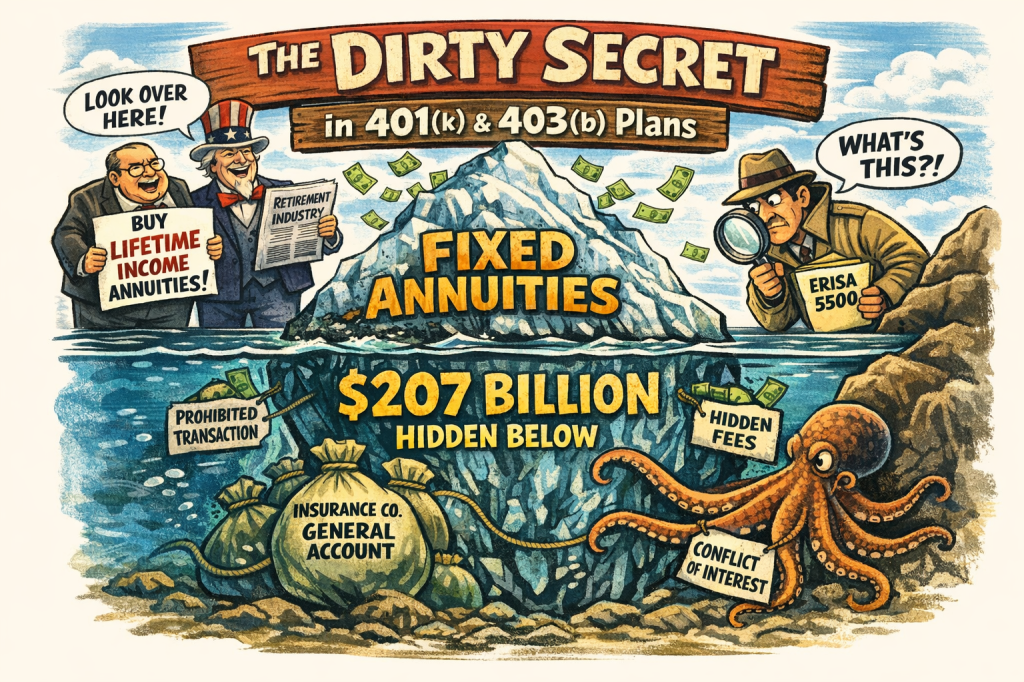

While the trade press, lobbyists, and Congress argue endlessly about putting lifetime income annuities into retirement plans, they are ignoring the much bigger, much quieter, and much more dangerous reality: Fixed annuities are already everywhere in 401(k) and 403(b) plans. Not income annuities. Not fancy new products. Plain vanilla, insurance company general account fixed annuities. And they have been sitting there for 20 years, largely unnoticed, unexamined, and almost never litigated. They are the dirty secret of defined contribution plans. By talking endlessly about Lifetime Income Annuities which barely register at under 1%, which sound good, they hope to hide these fixed annuities.

The scale no one talks about Using the RxTrima ERISA database: 774,172 ERISA plans 725,689 are defined contribution plans (mostly 401(k)s, some ERISA 403(b)s) The litigation universe (plans > $100 million): 9,010 plans Of roughly 9,000 plans over $100 million reviewed: 3,579 plans hold fixed annuities $207 BILLION in plan assets Let that sink in.

While journalists obsess over whether a handful of plans might add lifetime income, thousands of plans already hold hundreds of billions inside insurance company balance sheets.

Breakdown:

Plan Size# of Plans with Fixed Annuities

Over $1B 17

$500M–$1B 27

$300M–$500M 57

$100M–$300M 320

$50M–$100M 482

$30M–$50M 532

$10M–$20M 1,260

Under $10M 700 This is not a niche issue. This is systemic.

Who the major players are These are not fringe insurers.

Insurer# Plans $Assets

Empower 930 $51.8B

TIAA 392 $58.3B

Principal 612 $20.1B

MassMutual 253 $13.1B

NY Life 300 $11.8B

MetLife 196 $11.2B

Lincoln 194 $8.7B

Transamerica 215 $6.7B

Voya 157 $5.2B

VALIC 93 $3.8B

This is dangerous under ERISA These are primarily general account contracts. That means: Plan assets become liabilities of the insurer’s balance sheet. They are not mutual funds. They are not CITs. They are not segregated. They are loans to the insurance company.

And under ERISA §406: That is a transfer of plan assets to a party in interest.

Why Fixed Annuity Contracts are mostly Secret Because they hide under different names like: “Stable value” “Capital preservation” “Fixed account” “Guaranteed account” “General account GIC” “Group annuity contract” And they sit quietly for years paying 2–3% while the insurer earns 5–7% on the same money. That spread is never disclosed. Never benchmarked. And just starting to be litigated.

The industries where this is concentrated From your notes: Education (ERISA 403(b)s) —345 plans dominated by TIAA Medical / hospitals —780 plans heavy Lincoln and others Financial firms —206 plans led by Principal, Empower Unions/nonprofits — 274 plans led by Empower, MassMutual These are exactly the plans plaintiff firms usually ignore because they don’t look like fee cases. Many are 403(b)s But they are prohibited transaction cases, not fee cases.

The real irony While Congress pushes bills to allow annuities into plans… There are already 3,500+ plans with $207 billion sitting in annuities that likely never complied with ERISA in the first place. This is not a future problem. This is a 20-year-old problem hiding in plain sight.

The punchline The retirement industry wants you to debate whether lifetime income annuities should be allowed into 401(k)s. They do not want you to notice that Fixed Annuities are already there, and are a litigation bomb ready to go off.

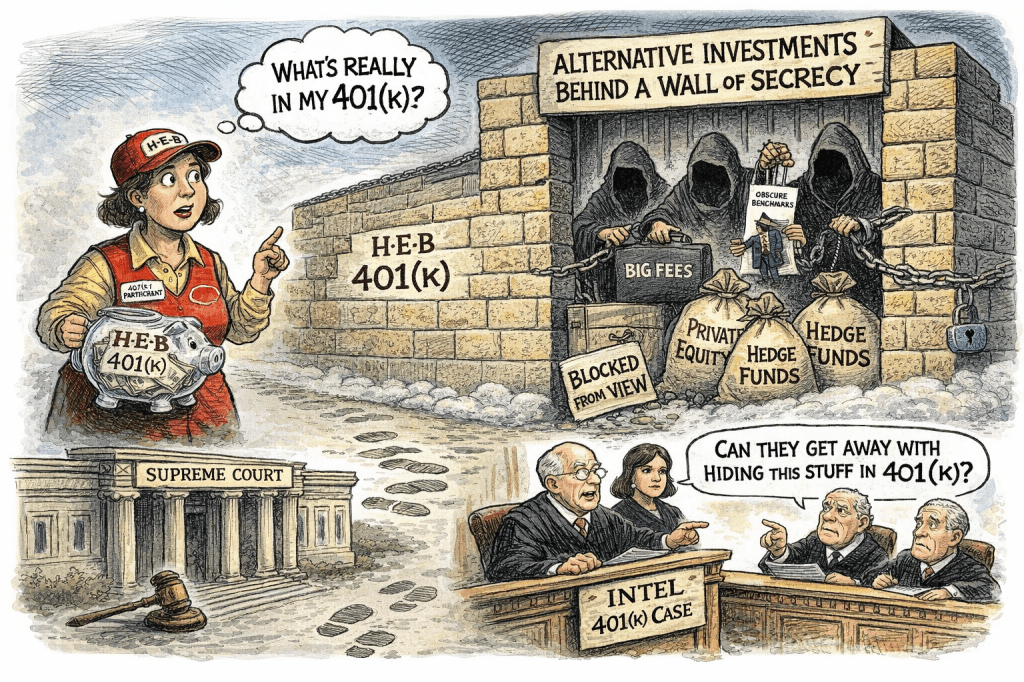

When a Plan’s Alternatives Echo the Same Secrecy and Conflicts Now Before the Supreme Court

The New York Times recently published a sympathetic profile about one H-E-B employee’s retirement savings, celebrating the virtues of long-term compounding and disciplined contributions. It’s a feel-good human narrative — but it carefully avoids the structural questions that truly matter to millions of participants.

Other alternate investments (hedge funds, private credit, opportunistic funds): $128,585,560

This is over $609 million in private and alternative assets — a striking allocation in what is supposed to be a daily-valued 401(k) designed for retail savers. Even holding a conservative interpretation of categories, the plan still lists well over $300 million in hard-to-value, illiquid positions.

HEB

That kind of exposure isn’t a minor footnote. It’s a strategic investment decision with big consequences.

Stale Valuations and “Daily Liquidity” — A Problem Wrapped in Language

H-E-B discloses in its 5500 that these alternative positions are:

Valued using “good faith estimates.”

Using manager valuations that may lag by 4–15 weeks

Used to price daily participant transactions

Participants assume the risk that true values may differ materially when actual trades settle later

HEB

Translated: the plan’s “daily valuation” window is an illusion. The values that participants see when they rebalance or change allocations, can be stale, and updated only after the fact — meaning participants make real decisions based on outdated information.

This too closely resembles the valuation and benchmark games at issue in the Intel Supreme Court case — where opaque pricing, bespoke benchmarks, and frozen valuations shield fiduciaries from accountability.

Private Equity in a 401(k)? Yes — But the Problem Is Bigger Than ‘Illiquidity’

Many PE vehicles embed fees and compensation that don’t become transparent until years later — carried interest that accrues in ways participants don’t see, placement agent fees shared with plan service providers, and revenue sharing that goes unseen. The plan’s total recordkeeping cost picture becomes distorted.

These hidden economic interests resemble the sort of related-party and soft-dollar conflicts that ERISA’s prohibited transaction rules were designed to prevent.

2) Manager-Controlled Valuation + Lack of Objective Benchmark

PE and other alternative asset managers often control monthly or quarterly NAV establishment. That’s fine for an endowment — not fine when:

A participant’s daily balance changes based on stale data

ERISA’s prudence and disclosure duties assume auditable, observable benchmarks and valuations — things private markets resist.

3) Liquidity Mismatch

Daily-tradable 401(k) interests priced on stale alternative valuations simply don’t behave like truly liquid vehicles. When participants rebalance, they get a price that may not reflect actual realized market value — transferring valuation risk to participants without their informed consent.

The Supreme Court Intel Case Isn’t About Pleading Rules — It’s About Secrecy

The conventional reporting treats the Intel case as a narrow statute-of-limitations fight. That’s the superficial framing.

What’s really at stake is:

Do fiduciaries have to disclose compensation, conflicts, and valuation mechanics transparently?

Or can they bury this information in opaque structures, stale assumptions, and “trust us” language?

Can participants ever compare plan performance to meaningful benchmarks — or does the “fiduciary illusion” shield fiduciary failures?

Why is a large plan diverting hundreds of millions into assets participants cannot evaluate?

Why are valuations lagged by weeks in a daily liquidity vehicle?

What benchmarks exist against which participants can measure performance?

What hidden compensation flows to advisers tied to these alternative allocations?

Is this consistent with ERISA’s core duties of loyalty, prudence, and disclosure?

These aren’t abstract academic questions. They go to the heart of whether retirement plans serve participants or structural economic interests tied to private markets and product fees.

The Convergence: H-E-B and Intel

If the Supreme Court allows fiduciaries to hide behind complexity and stale valuation benchmarks, then:

H-E-B’s allocation structure becomes a safer defensive line

More plans will emulate similar private market exposure without meaningful transparency

Participants will have no clear benchmark or valuation certainty for key portions of their retirement wealth

But if the Court affirms:

Meaningful disclosure duties

Real benchmarks (not proprietary or opaque targets)

A requirement that valuations reflect current participant realities

Then H-E-B’s structures — and those of countless other plans — are suddenly exposed to real fiduciary scrutiny.

The Bottom Line

Counting retirement balances is easy. Understanding what participants own, at what price, and with what conflicts is hard.

That is the structural issue the NY Times missed — and the Supreme Court must confront.

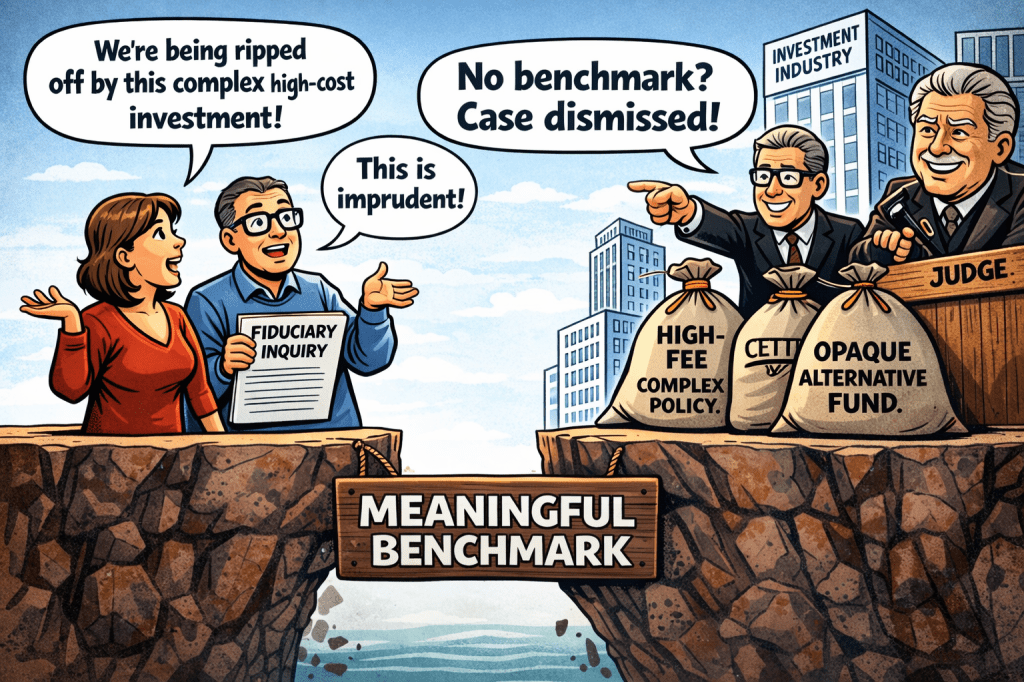

Over the last decade, a judicially fabricated standard has crept into ERISA litigation: the so-called “meaningful benchmark” requirement for claims alleging imprudence or excessive costs.

This appendix explains:

Where the concept came from

Why it is illegitimate as a substantive rule

How it masks high-fee, high-risk products that cannot be meaningfully benchmarked

1. Origins: A Procedural Pleading Universe, Not an Investment Principle

The idea of a “meaningful benchmark” did not originate in investment theory, economics, or statutes. It was born out of ERISA procedural case law, largely as a 12(b)(6) pleading standard for plaintiffs alleging fiduciary breaches based on investment performance or fees.

The early case law adopted by some circuits required that, to survive a motion to dismiss, a complaint alleging underperformance or excessive costs must include a comparator that is sufficiently similar — an “apples-to-apples” alternative that plausibly shows the fiduciary could have done better. Courts demanded such comparators because plaintiffs often had no discovery, and judges were (purportedly) reluctant to let cases proceed on uninformed guesses about what the fiduciary could have done differently.

But critically:

There is no statute that requires a “meaningful benchmark.”

ERISA’s prudence standard focuses on process, not performance relative to a counterfactual benchmark.

Benchmarks were a judicial convenience, not a substantive legal test.

2. It Is a Procedural Standard, Not a Substantive Investment Rule

The “meaningful benchmark” doctrine is a pleading rule — a device courts use to decide whether a complaint plausibly alleges imprudence before any discovery. It does not represent a real investment standard under ERISA or fiduciary law.

Indeed:

Some courts require it at the motion-to-dismiss stage.

Other circuits reject it as inappropriate fact-finding before discovery.

The Supreme Court now is considering this very issue in the Intel/Anderson cases — whether a meaningful benchmark is required at all at the pleading stage. The fact that this question has reached the Supreme Court underscores how unsettled and judge-crafted this standard really is.

In other words, meaningful benchmark is not a regulatory requirement; it is a judge’s attempt to police litigation before discovery by demanding early comparators. It is a procedural gatekeeper, not substantive law.

3. Why It Is Deceptive — Especially Against Insurance and Annuity Products

The meaningful benchmark standard sounds appealing — who wouldn’t want apples-to-apples comparisons? But in practice, it gives impermissibly broad cover to Wall Street, insurance companies, and institutional defenders because:

📌 a) Certain products cannot be benchmarked

· Fixed annuities · General account insurance contracts · Proprietary separate accounts · Private equity and hedge funds

These products have no market-priced peers — you cannot find another open-end mutual fund that does what a fixed annuity does under discretionary crediting and balance-sheet mechanics.

Nothing in finance theory or asset pricing mandates that annuities must be compared to Vanguard, BlackRock, or S&P 500 products. Benchmarks are easier for public market instruments precisely because they have prices. Annuities do not. Thus, the meaningful benchmark standard is illogical when it comes to products that cannot be benchmarked.

4. The Standard Is Being Used to Hide, Not Reveal, Risk

The meaningful benchmark doctrine effectively says:

“If you cannot show an obvious benchmark that demonstrates harm, you have no case.”

That standard flips fiduciary law on its head.

Under ERISA, the duty of prudence is about process and risk-adjusted judgment — not about whether some benchmark existed on which the fiduciary could have hypothetically outperformed. Instead, defendants have latched on to this judicial invention to argue that a lack of benchmark equals lack of harm — a position that serves Wall Street and insurance producers very well.

5. The Investment Industry Loves It — Because It Lets Them Sneak In Opaque, High-Fee Products

Investment intermediaries and insurers have a strategic advantage when the standard is “meaningful benchmark.”

Why?

Because the industry sells products that do not have logical benchmarks:

Annuities

Indexed insurance contracts

Private market funds

Multi-asset strategies with proprietary glidepaths

These products cannot be meaningfully compared to:

Public index funds

Mutual funds

Standard benchmarks

So the industry says:

“There is no market benchmark — therefore the allegation fails.”

This argument presumes the answer, rather than evaluating whether the fiduciary followed a prudent process or whether the product’s risks and costs were adequately disclosed and managed.

6. The Standard Was Never Explained in Investment Texts or Statutes

You won’t find “meaningful benchmark” defined in:

ERISA itself

DOL regulations

Investment management texts

SEC rules

It is purely a judicial procedural rule, created in cases like Ruilova, Barrick Gold, Oshkosh, and others that required comparators in pleadings. But there is no canonical source where the concept was explained and justified in investment academic literature. It is a creature of litigation economics, not fiduciary economics.

Now the Supreme Court is being asked to decide whether that procedural invention should even survive constitutional and statutory scrutiny.

7. The Standard Shields Wall Street at the Cost of Participants

Here’s the real impact:

👉 Judges who require a “meaningful benchmark” are effectively saying to plaintiffs:

“If you can’t find a near-identical investment strategy with public pricing, you have no case.”

This approach:

Promotes a hindsight performance regime

Undermines process-based prudence

Shields producers of opaque, illiquid, proprietary products

Raises barriers to scrutiny even where conflicts and undisclosed compensation are obvious

That is the opposite of ERISA’s purpose.

ERISA is supposed to protect participants from conflicts of interest, hidden costs, and imprudent choices, not protect Wall Street by enforcing a “benchmark inoculation” against scrutiny.

8. Because Judges Lack Investment Economics Training, They Default to Benchmarks

One reason the meaningful benchmark standard took hold is that many judges:

Lack finance or investment economics training

Are uncomfortable evaluating risk and compensation structures that do not fit classic mutual fund models

Are influenced by industry amici and defense briefings that frame benchmarks as the only way to demonstrate imprudence

The result:

A “benchmark requirement” becomes a judicial shortcut — not because it is technically correct, but because it makes litigation easier for courts that do not want to engage with real economics.

This dynamic benefits Wall Street, not participants.

9. As We Explained Earlier in Commonsense, Benchmarks Don’t Work for Complex Solutions

Our earlier discussion of target-date benchmarks — including why simple index comparisons are inadequate and how product design matters more than benchmarking — already exposed this fallacy. Benchmarks assume liquidity, transparency, and comparability — all of which are absent in the annuity, separate account, and private market contexts at issue in Intel, Cho, and other cases.

10. Bottom Line — “Meaningful Benchmark” Is a Procedural Illusion

The “meaningful benchmark” standard is not a substantive fiduciary rule; it is:

A judicial pleading device

A procedural barrier

A way for judges uncomfortable with investment economics to avoid deep analysis

A shield for the industry to hide products that cannot be bench-marked

And it should not be used to legitimize high-fee, high-risk contracts in ERISA plans — especially when:

The products are opaque;

Compensation is hidden;

Benchmarks don’t exist; and

Participants rely on fiduciaries, not benchmarks, for informed decisions.

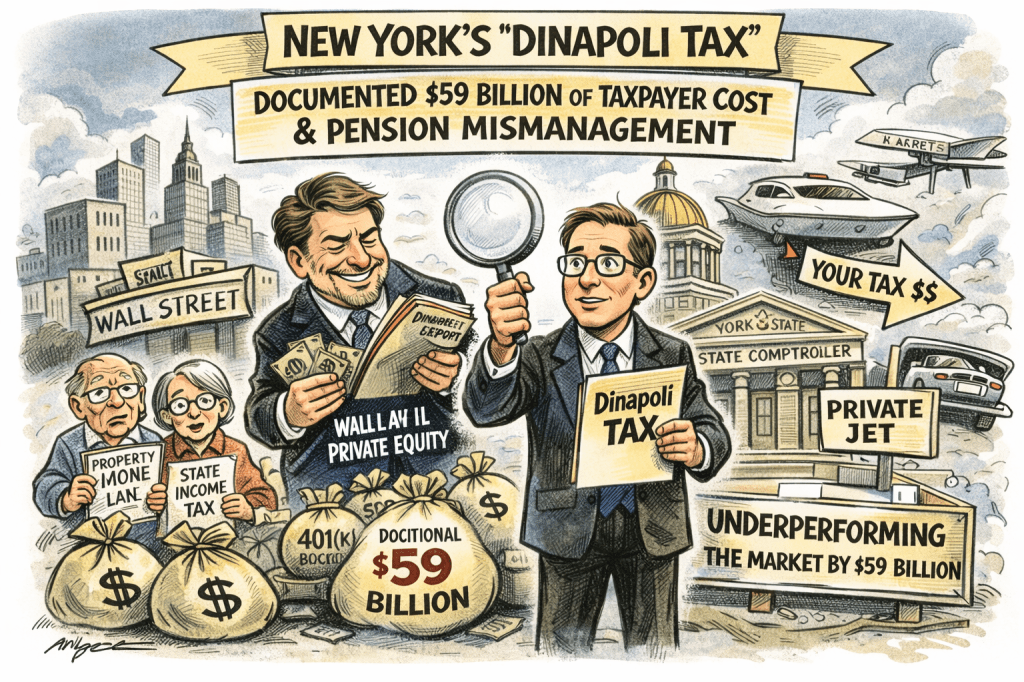

In New York, the Comptroller is the sole trustee of the pension. Candidate Drew Warshaw has published a study that the $59 billion in excess fees is borne by NY Taxpayers and is essentially a tax. https://www.drewwarshaw.com/ideas/dinapolitax

The Warshaw report “DiNapoli Tax” frames Fees as a Hidden Tax: How Underperformance Becomes a Public Burden. The DiNapoli Tax framework does something pension insiders rarely want done it treats investment fees and underperformance as a form of taxation.

Here’s the chain—simple but devastating: Private-market-heavy portfolios underperform investable benchmarks net of fees, which reduces asset growth. Reduced asset growth increases required employer contributions. Employers fund those contributions with tax revenue. Taxpayers unknowingly subsidize fee extraction and failed complexity

The report’s estimate—$59.1 billion since 2007—is not an abstract “missed opportunity.” It is the present value of additional checks written by the State of New York, counties, cities, and school districts and their taxpayers.

Fees are often the dominant driver of net underperformance. The opposition report shows that in FY 2025 alone, Roughly 13% of employer contributions went directly to investment management fees to external managers, many of whom underperformed public markets

In other words, taxpayers paid fees first, and only then funded benefits. The DiNapoli Tax report aggregates costs that are typically hidden across multiple layers: Management fees, Performance fees (carried interest), Transaction and monitoring fees, Partnership expenses and Fund-of-fund fees.

Controller DiNapoli covers up the $59 billion Loss. Last week, New York State Comptroller Thomas DiNapoli rushed out a press release proclaiming that an “independent review” had cleared the New York State Common Retirement Fund (CRF) of ethical, fiduciary, and conflict-of-interest concerns. According to the Comptroller, the report proves that New York’s pension fund “operates at the highest ethical and professional standards.”

These so-called independent reviews collapse under even modest scrutiny. It never grapples with the central economic finding of the opposition report: $59 billion in avoidable taxpayer costs.

The reports DiNapoli cites are not independent in any meaningful fiduciary sense. They are procedural compliance audits, not economic fiduciary reviews. They examine whether boxes were checked—not whether retirees and taxpayers were harmed. The most recent review, conducted by Weaver & Tidwell LLP, explicitly states that it does not analyze investment performance, valuation accuracy, or economic outcomes. Instead, it limits itself to whether transactions complied with internal policies and DFS regulations, which are written by the Comptroller’s own office.

The Comptroller’s “independent” reviews repeatedly emphasize compliance with disclosure rules while never quantifying the economic impact of fees. A fund can be perfectly compliant—and still impose tens of billions in avoidable tax burden. That is exactly what the DiNapoli Tax report alleges. And it is exactly what the Comptroller refuses to confront.

A Benchmark Shell Game is used to hide these problems. New York relies on custom, non-investable benchmarks that flatter reported results while obscuring real economic performance. The Weaver report praises the Fund’s asset-allocation process but never evaluates whether those benchmarks are structurally biased in favor of private markets.

Compliance with a bad benchmark is not prudence; it is misdirection.

Valuation Risk is also ignored. The DiNapoli press release leans heavily on claims of “high transparency.” Yet the Weaver review accepts conflicted manager-provided NAVs at face value and explicitly disclaims any responsibility for testing valuation accuracy or loss recognition timing.

Why the DiNapoli Tax Report Matters — and Why You Haven’t Heard About It

The DiNapoli Tax report — a clear, dollar-denominated indictment of how underperformance in New York’s public pensions translates into higher taxes — should be front-page news. Instead, it’s barely registered outside a few niche outlets. Why? Because powerful private-equity interests have an interest in burying the story..

New York officials s since Citizens United have had the ability to receive secret dark money contributions from Private Equity. Politically connected and current MSNBC media darling, Steven Rattner. co-founded private-equity firm Quadrangle. Quadrangle became entangled in New York’s notorious pension pay-to-play scandal involving placement agents and political consultants around the State Comptroller’s office. Rattner/Quadrangle retained Hank Morris (a political consultant tied to the Comptroller) in a way regulators viewed as improper, with enforcement and settlement outcomes reported by major outlets. New York’s Attorney General also filed pleadings describing alleged misconduct in connection with the New York State Common Retirement Fund.

DealBook Nation is a good description of NY media. “DealBook” is shorthand not just for a New York Times newsletter, but for an entire elite finance media ecosystem centered in New York: with editors, reporters, conference stages, think-tank panels, cable-news green rooms, and carefully curated “thought leaders.” Private equity is not merely covered by this ecosystem; it is embedded within it.

The Comptroller is not just defending past actions. He is running for re-election—and expanding allocations to the very asset classes these reviews refuse to scrutinize.

Until New York commissions a real independent review that: Uses investable public benchmarks, Performs PME and cash-flow analysis, Independently audits private-asset valuations, and Quantifies dollar underperformance …claims of being “cleared” should be treated for what they are: whitewash, not accountability.

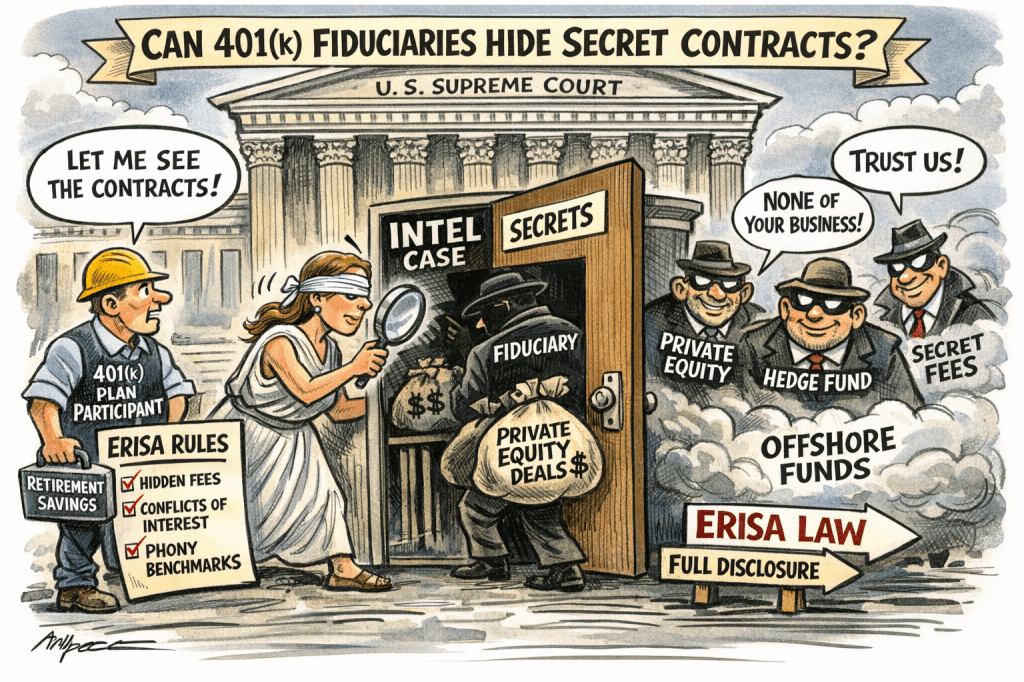

The retirement industry would like you to believe that the Supreme Court’s decision to hear Anderson v. Intel is a narrow, technical dispute about whether “alternative investments” belong in 401(k) plans.

That is industry spin.

The Intel case is not about whether private equity is “good” or “bad.” It is about whether ERISA fiduciaries can hide the governing investment contracts, invent benchmarks, and still claim compliance with the strictest fiduciary law in the country.

If Intel prevails, the consequences will not stop with private equity. They will extend directly to target-date funds, annuities, private credit, and any opaque product that depends on secrecy to survive scrutiny.

The Industry Narrative: “Nothing to See Here”

Industry groups such as NAPA frame Intel as reassurance:

Private equity is just another asset class

Fiduciaries followed a prudent process

Plaintiffs are asking courts to micromanage investments

Disclosure of contracts is unnecessary

This framing is designed to shift the focus away from the core problem:

Intel will not disclose the private-equity contracts—nor even the names of the funds—while asking courts to assume those contracts are prudent, fairly priced, and conflict-free.

That is not how ERISA works.

The Real Issue: You Cannot Prove Prudence While Hiding the Contract

ERISA is not a “trust us” statute.

Under ERISA §404 and §406:

Fiduciaries must demonstrate prudence and loyalty

Transactions with parties in interest are presumptively prohibited

Fiduciaries—not participants—bear the burden of proving an exemption

As the Supreme Court made clear in Cunningham v. Cornell, once a prohibited transaction is plausibly alleged, the burden shifts to the fiduciary.

That burden cannot be met if the fiduciary refuses to disclose:

The investment contract

The fee and carry structure

The valuation methodology

The indemnification provisions

The conflicts and affiliate transactions

Secrecy is not neutral. Secrecy defeats the exemption.

Private Equity in a 401(k) Is Not a “Fund” — It’s a Contract

This is where the industry misleads courts and fiduciaries.

Private equity is not a security with a market price. It is a bespoke service contract governed by a limited partnership agreement.

That contract determines:

Who controls valuation (the manager)

How performance is measured (IRR and GP-asserted NAV)

How fees are extracted (management fees, transaction fees, carry)

How conflicts are resolved (usually in favor of the GP)

Without seeing the contract, there is no way to benchmark, monitor, or audit the investment.

That is not a technical quibble. It is a fatal fiduciary defect.

The Intel Case Mirrors TIAA’s Target-Date “Risk Illusion”

If this sounds familiar, it should.

Intel’s strategy—hiding private-equity contracts while claiming prudence—is functionally identical to TIAA’s target-date fund strategy of hiding annuity contracts inside CITs and separate accounts.

In both cases:

The core economic engine is contractual, not market-based

The risks are masked by invented benchmarks

The valuation depends on manager discretion

The fiduciary claims “diversification” while avoiding disclosure

As I explained in TIAA’s Target Date Funds Are Built on a Risk Illusion, you cannot create real diversification—or real performance—by hiding contractual risk behind smoothed numbers.

Private equity in a 401(k) target-date fund is simply the next iteration of the same illusion.

Intel’s defenders repeatedly argue that the plan used “appropriate benchmarks.”

But non-investable benchmarks are not benchmarks.

Private equity relies on:

Lagged, GP-asserted NAVs

IRRs that ignore cash-flow timing risk

Peer universes built from the same flawed data

This is no different from annuity providers benchmarking opaque general-account products against invented indices that no participant could ever invest in.

ERISA does not permit fiduciaries to benchmark themselves to their own homework.

Why the Supreme Court Took the Case

The Supreme Court did not take Intel because it wants to bless private equity in 401(k)s.

It took the case because the lower courts have allowed fiduciaries to use opacity as a litigation shield, undermining ERISA’s enforcement framework.

The question before the Court is simple:

Can an ERISA fiduciary satisfy its duties while hiding the governing investment contracts from participants and courts?

If the answer is yes, ERISA’s prohibited-transaction rules collapse—not just for private equity, but for:

Annuities

Private credit

Insurance separate accounts

Crypto-linked products

Any future opaque “innovation”

Bottom Line for Fiduciaries

This case is a warning.

If your investment strategy depends on:

Secret contracts

Invented benchmarks

Smoothed valuations

“Trust us” disclosures

you do not have an innovation problem. You have a fiduciary problem.

The Supreme Court should—and likely will—make clear that ERISA does not permit secrecy as a substitute for prudence.

And when it does, the fallout will reach far beyond Intel.

Appendix 1 Why the “Meaningful Benchmark” Standard Is a Judicial Illusion Built for Wall Street

Over the last decade, a judicially fabricated standard has crept into ERISA litigation: the so-called “meaningful benchmark” requirement for claims alleging imprudence or excessive costs.

This appendix explains:

Where the concept came from

Why it is illegitimate as a substantive rule

How it masks high-fee, high-risk products that cannot be meaningfully benchmarked

1. Origins: A Procedural Pleading Universe, Not an Investment Principle

The idea of a “meaningful benchmark” did not originate in investment theory, economics, or statutes. It was born out of ERISA procedural case law, largely as a 12(b)(6) pleading standard for plaintiffs alleging fiduciary breaches based on investment performance or fees.

The early case law adopted by some circuits required that, to survive a motion to dismiss, a complaint alleging underperformance or excessive costs must include a comparator that is sufficiently similar — an “apples-to-apples” alternative that plausibly shows the fiduciary could have done better. Courts demanded such comparators because plaintiffs often had no discovery, and judges were (purportedly) reluctant to let cases proceed on uninformed guesses about what the fiduciary could have done differently.

But critically:

There is no statute that requires a “meaningful benchmark.”

ERISA’s prudence standard focuses on process, not performance relative to a counterfactual benchmark.

Benchmarks were a judicial convenience, not a substantive legal test.

2. It Is a Procedural Standard, Not a Substantive Investment Rule

The “meaningful benchmark” doctrine is a pleading rule — a device courts use to decide whether a complaint plausibly alleges imprudence before any discovery. It does not represent a real investment standard under ERISA or fiduciary law.

Indeed:

Some courts require it at the motion-to-dismiss stage.

Other circuits reject it as inappropriate fact-finding before discovery.

The Supreme Court now is considering this very issue in the Intel/Anderson cases — whether a meaningful benchmark is required at all at the pleading stage. The fact that this question has reached the Supreme Court underscores how unsettled and judge-crafted this standard really is.

In other words, meaningful benchmark is not a regulatory requirement; it is a judge’s attempt to police litigation before discovery by demanding early comparators. It is a procedural gatekeeper, not substantive law.

3. Why It Is Deceptive — Especially Against Insurance and Annuity Products

The meaningful benchmark standard sounds appealing — who wouldn’t want apples-to-apples comparisons? But in practice, it gives impermissibly broad cover to Wall Street, insurance companies, and institutional defenders because:

📌 a) Certain products cannot be benchmarked

· Fixed annuities · General account insurance contracts · Proprietary separate accounts · Private equity and hedge funds

These products have no market-priced peers — you cannot find another open-end mutual fund that does what a fixed annuity does under discretionary crediting and balance-sheet mechanics.

Nothing in finance theory or asset pricing mandates that annuities must be compared to Vanguard, BlackRock, or S&P 500 products. Benchmarks are easier for public market instruments precisely because they have prices. Annuities do not. Thus, the meaningful benchmark standard is illogical when it comes to products that cannot be benchmarked.

4. The Standard Is Being Used to Hide, Not Reveal, Risk

The meaningful benchmark doctrine effectively says:

“If you cannot show an obvious benchmark that demonstrates harm, you have no case.”

That standard flips fiduciary law on its head.

Under ERISA, the duty of prudence is about process and risk-adjusted judgment — not about whether some benchmark existed on which the fiduciary could have hypothetically outperformed. Instead, defendants have latched on to this judicial invention to argue that a lack of benchmark equals lack of harm — a position that serves Wall Street and insurance producers very well.

5. The Investment Industry Loves It — Because It Lets Them Sneak In Opaque, High-Fee Products

Investment intermediaries and insurers have a strategic advantage when the standard is “meaningful benchmark.”

Why?

Because the industry sells products that do not have logical benchmarks:

Annuities

Indexed insurance contracts

Private market funds

Multi-asset strategies with proprietary glidepaths

These products cannot be meaningfully compared to:

Public index funds

Mutual funds

Standard benchmarks

So the industry says:

“There is no market benchmark — therefore the allegation fails.”

This argument presumes the answer, rather than evaluating whether the fiduciary followed a prudent process or whether the product’s risks and costs were adequately disclosed and managed.

6. The Standard Was Never Explained in Investment Texts or Statutes

You won’t find “meaningful benchmark” defined in:

ERISA itself

DOL regulations

Investment management texts

SEC rules

It is purely a judicial procedural rule, created in cases like Ruilova, Barrick Gold, Oshkosh, and others that required comparators in pleadings. But there is no canonical source where the concept was explained and justified in investment academic literature. It is a creature of litigation economics, not fiduciary economics.

Now the Supreme Court is being asked to decide whether that procedural invention should even survive constitutional and statutory scrutiny.

7. The Standard Shields Wall Street at the Cost of Participants

Here’s the real impact:

👉 Judges who require a “meaningful benchmark” are effectively saying to plaintiffs:

“If you can’t find a near-identical investment strategy with public pricing, you have no case.”

This approach:

Promotes a hindsight performance regime

Undermines process-based prudence

Shields producers of opaque, illiquid, proprietary products

Raises barriers to scrutiny even where conflicts and undisclosed compensation are obvious

That is the opposite of ERISA’s purpose.

ERISA is supposed to protect participants from conflicts of interest, hidden costs, and imprudent choices, not protect Wall Street by enforcing a “benchmark inoculation” against scrutiny.

8. Because Judges Lack Investment Economics Training, They Default to Benchmarks

One reason the meaningful benchmark standard took hold is that many judges:

Lack finance or investment economics training

Are uncomfortable evaluating risk and compensation structures that do not fit classic mutual fund models

Are influenced by industry amici and defense briefings that frame benchmarks as the only way to demonstrate imprudence

The result:

A “benchmark requirement” becomes a judicial shortcut — not because it is technically correct, but because it makes litigation easier for courts that do not want to engage with real economics.

This dynamic benefits Wall Street, not participants.

9. As We Explained Earlier in Commonsense, Benchmarks Don’t Work for Complex Solutions

Our earlier discussion of target-date benchmarks — including why simple index comparisons are inadequate and how product design matters more than benchmarking — already exposed this fallacy. Benchmarks assume liquidity, transparency, and comparability — all of which are absent in the annuity, separate account, and private market contexts at issue in Intel, Cho, and other cases.

10. Bottom Line — “Meaningful Benchmark” Is a Procedural Illusion

The “meaningful benchmark” standard is not a substantive fiduciary rule; it is:

A judicial pleading device

A procedural barrier

A way for judges uncomfortable with investment economics to avoid deep analysis

A shield for the industry to hide products that cannot be bench-marked

And it should not be used to legitimize high-fee, high-risk contracts in ERISA plans — especially when:

The products are opaque;

Compensation is hidden;

Benchmarks don’t exist; and

Participants rely on fiduciaries, not benchmarks, for informed decisions.

Appendix 2 — Lessons from Pizarro v. Home Depot for the Intel Litigation

Recent commentary by James W. Watkins, III, JD, CFP® on the Pizarro v. Home Depot litigation — especially his critiques of the EBSA amicus briefs in that case — highlights fiduciary failures and regulatory capture dynamics that are deeply relevant to the Intel / Anderson litigation now before the Supreme Court.(fiduciaryinvestsense.com; fiduciaryinvestsense.com)

Watkins’s insights reveal systemic issues in how fiduciary standards are being interpreted and enforced — or, more accurately, how they are being diluted by regulators, industry amici, and courts. As Intel asks whether courts can demand “meaningful benchmarks” at the pleading stage, Watkins’s Home Depot critique shows why that question cannot be abstracted from larger issues of disclosure, economic substance, and fiduciary candor.

1. Disclosure and Secrecy: The Core of Fiduciary Duty

One of Watkins’s central points in Fair Dinkum: A Critique of the EBSA’s Amicus Brief in Pizarro v. Home Depot is that the Department of Labor (via EBSA) abandoned core fiduciary responsibilities by advocating positions that underplay the importance of disclosure and economic substance.

Specifically:

EBSA’s amicus brief emphasized process compliance over economic substance, effectively arguing that plan sponsors who followed certain procedural boxes were insulated from liability — even if they failed to disclose material economic facts about the investments at issue.

This mirrors the antinomian argument we see in Intel/Anderson: that plaintiffs must plead a “meaningful benchmark” before discovery — a procedural hurdle that distracts from whether the fiduciary failed to disclose material investment risks and economic realities in the first place.

Watkins’s critique of the EBSA amicus brief demonstrates a consistent pattern: regulators preferring formalism over substance, process over transparency.

In Intel, this manifests as judicial and amicus rhetoric that treats benchmarks as a proxy for prudence instead of focusing on whether fiduciaries provided investors with material information needed to evaluate risk and compensation.

2. Fiduciary Loyalty vs. Regulatory Theater

In The DOL’s Pizarro v. Home Depot Amicus Brief: Borzi and Gomez Don’t Live Here Anymore, Watkins documents how EBSA’s position effectively reframes fiduciary law to insulate conflict-laden decisions so long as process step boxes are checked.

The essential critique:

Fiduciary law historically requires both prudent process and loyalty to act solely in the interest of participants.

EBSA’s brief prioritized procedural immunities, not fiduciary loyalty — downplaying whether plan sponsors adequately disclosed economic conflicts.

This insight directly applies to Intel/Anderson. The push for a “meaningful benchmark” at the motion-to-dismiss stage:

Empowers defendants to argue that as long as there is no obvious comparator, there is no plausible claim — even if fiduciaries concealed material risk, compensation, or conflicts.

Shifts the focus from fiduciary loyalty and investor protection to procedural immunity.

Watkins’s work shows why this shift is perilous: it validates the very illusions that erode fiduciary protections — the same illusions central to the Intel and Cho litigation context.

3. Proprietary Economics and the Failure of Transparency

A common theme in Watkins’s writing on Home Depot is the danger of proprietary or undisclosed economics — where fiduciaries or issuers refuse to provide meaningful economic information.

In the Home Depot context, the EBSA amicus brief was criticized for diminishing the value of transparency:

The brief implied that plan sponsors can satisfy ERISA so long as they rely on procedural checklists and industry standards — even when economic substance and proprietary fee structures are opaque to participants and fiduciaries alike.

This has direct parallels to the Intel case’s context:

Many of the allegedly imprudent decisions at issue involved products (annuities, proprietary CITs, etc.) with undisclosed compensation via spread, discretionary pricing, and other opaque features.

A benchmark requirement effectively punishes plaintiffs for not discovering and pleading economic comparators that only discovery will reveal — a barrier rooted in secrecy, not sound fiduciary analysis.

Watkins’s critique highlights the inconsistency in accepting opaque proprietary economics as part of a safe process — which dovetails with Intel’s concern about how courts treat benchmarks without probing the underlying economics.

4. Regulatory Capture and the Fiduciary Standard’s Erosion

Watkins’s commentary repeatedly underscores a broader institutional issue: regulatory capture, where the very agencies tasked with protecting workers tilt too heavily toward industry risk minimization.

In The DOL’s Pizarro v. Home Depot Amicus Brief…, he observes that:

Regulators have shifted toward interpretations that emphasize procedural compliance over fiduciary duty grounded in economic substance, transparency, and loyalty to participants, a pattern that disadvantages claimants and advantages industry defenders.

This regulatory shift mirrors judicial trends that:

Require plaintiffs to overcome stringent procedural banners (like meaningful benchmarks);

Allow defendants to hide behind process boxes;

Tolerate industry amici positions that diminish the core fiduciary obligations.

In the Intel litigation, this context matters because the Supreme Court’s treatment of pleading standards can either reinforce or reverse this trend. If courts continue to elevate procedural hurdles (like benchmarks) above substantive inquiry into transparency, risk, and conflicts, the regulatory erosion Watkins describes will be cemented in doctrine.

5. What Judges and Amici Miss When They Focus on Benchmarks

From Watkins’s Home Depot insights, three interlocking lessons emerge that should inform how we read Intel:

A. Benchmarks Are Not a Substitute for Disclosure or Loyalty: Benchmarks are tools for analysis — but they do not deliver material information to participants nor do they safeguard against conflicted economics.

B. Procedural Immunities Cannot Cure Conflicted Economics: Neither a checklist of steps nor an absence of a meaningful benchmark at the pleadings stage can justify a decision where economic risks and conflicts were not disclosed.

C. Regulatory and Judicial Emphasis on Procedural Thresholds Encourages Secrecy: When regulators and courts raise procedural bars (e.g., benchmarks before discovery), they inadvertently incentivize opacity, not fiduciary candor.

Watkins’s critiques show that fiduciary duty is both procedural and substantive — it demands transparency and duty of loyalty, not just procedural boxes.

6. Implications for Intel’s Outcome and Fiduciary Law

Taken together, Watkins’s writings on Home Depot illuminate three key takeaways relevant to the Supreme Court’s consideration of benchmarks in Intel/Anderson:

Benchmarks cannot be elevated to a doctrinal requirement that displaces core fiduciary obligations — especially where proprietary economics and conflicts are in play.

Judicial or regulatory moves toward proceduralism (benchmarks before discovery) embed the same kind of fiduciary illusions that Intel criticizes — secrecy, veneer of process, and reliance on industry dicta.

A correct fiduciary analysis must center economic substance, transparency, and conflict disclosure — not shortcut substitutes like early benchmarks.

In other words, Intel should be read as an opportunity to reaffirm fiduciary law’s core values, not to entrench a pleading-stage benchmark regime that rewards secrecy and shields conflicted conduct — the very trends Watkins has decried in Pizarro.

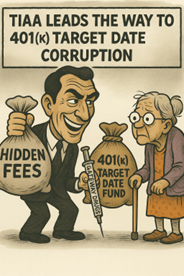

TIAA and its academic partners want you to believe they have discovered a free lunch in retirement investing: add a fixed annuity to a target date fund, and you magically get higher returns and lower risk.

That claim is now being aggressively promoted through a new TIAA Institute / Charles River Associates (CRA) paper, The Impact of TIAA Traditional in Target Date Glidepaths. The paper concludes that target date funds (TDFs) including TIAA Traditional “outperform” conventional TDFs across virtually every scenario—especially because the annuity appears to reduce volatility while maintaining bond-like returns.

There’s just one problem.

The “low risk” that drives these results isn’t real, and the analysis completely ignores the upcoming legal issue: fixed annuities issued by TIAA are prohibited transactions under ERISA when mixed into 401(k) target date funds.

This is not an academic quibble. It is the same kind of modeling sleight-of-hand that courts have rejected in employer stock cases, stable value cases, and valuation fraud cases for decades.

The Core Trick: Fake Volatility

TIAA’s modeling rests on a simple but profoundly misleading assumption: that TIAA Traditional has lower volatility than bonds.

Why does it appear that way?

Because annuities are not marked to market.

TIAA Traditional’s returns are not set by market prices. They are set by internal crediting decisions, made at TIAA’s discretion, based on assets held in TIAA’s opaque general account. Losses are smoothed. Gains are withheld. Risk is buried on the insurer’s balance sheet.

That doesn’t make risk disappear—it just hides it.

Calling this “lower volatility” is like calling a non-traded REIT safer than public real estate because the price doesn’t move. Courts don’t buy that logic, and fiduciaries shouldn’t either.

Bonds and Annuities Are Not the Same — TIAA Admits This (Then Ignores It)

In a quiet but telling footnote, the TIAA Institute paper admits:

“Per the Investment Company Act of 1940, an annuity cannot be part of a mutual fund.”

That should have been the end of the analysis.

Instead, TIAA proceeds to do exactly what the law forbids in substance if not in form: it embeds an insurance contract inside collective investment trusts and managed accounts and then models it as if it were a bond fund.

But annuities are not bonds:

They are illiquid

They cannot be freely sold

They often cannot be exited without delay or penalty

Annuitization is frequently irrevocable

There are no downgrade or termination rights

Participants bear insurer credit risk, not market risk

Diversification theory assumes liquidity. Once liquidity is gone, correlation statistics are meaningless. You are not “rebalancing” risk—you are locking it in.

The Prohibited Transaction Elephant in the Room

Most strikingly, the TIAA Institute analysis never mentions ERISA §406 prohibited transactions. Not once.

That omission is not accidental. It is essential to the conclusion.

Here is the reality TIAA’s modeling ignores:

TIAA is the recordkeeper

TIAA is the annuity issuer

TIAA sets the crediting rates

TIAA retains the spread

TIAA is therefore a party in interest multiple times over

Under ERISA, when a fiduciary causes a plan to transact with itself—or retain a product that generates undisclosed compensation—that transaction is presumptively illegal, regardless of performance.

And make no mistake: TIAA Traditional generates compensation.

“No Fees” Is a Myth — The Spread Is the Fee

TIAA repeatedly claims that Traditional has “no fees.” That is simply false.

The compensation is taken as spread—the difference between what TIAA earns in its general account and what it credits to participants. Independent reporting, including NBC News, has reported that the hidden spread is around 150 basis points annually.

Importantly, this spread figure was not disputed by TIAA when given the chance by NBC.

Spread is compensation. Undisclosed compensation retained by a fiduciary is the textbook definition of ERISA §406(b)(1) self-dealing.

No amount of glidepath modeling can legalize that.

Performance Does Not Cure a Prohibited Transaction

This is where TIAA’s entire argument collapses.

After the Supreme Court’s decision in Cunningham v. Cornell, plaintiffs do not need to plead around exemptions. Defendants must prove them.

That means:

You do not get to justify self-dealing because a model looks good

You do not get to ignore conflicts because returns are “competitive”

You do not get to replace law with regression analysis

If a transaction is prohibited, the remedy is disgorgement, not benchmarking.

Why This Matters for Courts, Fiduciaries, and Plaintiffs

Target date funds are now the default investment for tens of millions of workers. Embedding insurance contracts inside them—without liquidity, transparency, or ERISA-compliant compensation structures—creates a perfect storm:

Participants cannot exit

Fiduciaries cannot monitor properly

Conflicts are structural, not incidental

Losses may not show up until it’s too late

We have already seen courts reject “prudent process theater” in other contexts. The same reckoning is coming here.

.

Bottom Line

TIAA’s target date modeling works only if you accept three false premises:

That hidden risk is no risk

That illiquid insurance contracts are bonds

That ERISA’s prohibited transaction rules don’t apply

None of those premises survives serious scrutiny.

Once annuities are properly treated as what they are—ongoing transactions with a party in interest that generate undisclosed compensation—the supposed diversification and risk reduction disappear.

What’s left is a glidepath built on a legal and economic illusion.

Related Commonsense 401(k) Project articles:

TIAA Exposed for Excessive Hidden Annuity Spread Fees — Again

Appendix: TIAA Is Not Alone — Target Date Funds Are Quietly Filling Up with Insurance Contracts

One of the most predictable responses to criticism of TIAA’s target-date modeling is: “This isn’t just TIAA — everyone is doing it.”

That response is meant to normalize the problem. In reality, it does the opposite.

Recent Morningstar reporting confirms what fiduciary litigators and independent analysts have been seeing for several years: a growing number of target-date funds are quietly embedding fixed annuities inside 401(k) default investments — outside SEC regulation, with minimal transparency, and with little understanding by plan sponsors or participants of what they actually own.

This appendix explains why that trend is dangerous, legally flawed, and ripe for litigation.

Morningstar Confirms the “Hidden Trend”

In a 2025 article titled “A Hidden Trend Is Changing 401(k) Plans — Here’s What It Means for Investors,” Morningstar documents the increasing use of annuity-based components inside target-date strategies, particularly in large plans that use collective investment trusts (CITs).

Morningstar presents this as an innovation. It is better understood as regulatory arbitrage.

Key points Morningstar inadvertently confirms:

These target-date products are not SEC-registered mutual funds

They are primarily state-regulated CITs or managed accounts

The annuity components are illiquid, opaque, and insurer-controlled

Risk and return characteristics are not comparable to securities

That matters, because SEC-registered mutual funds correctly prohibit fixed annuities. They have done so for decades, precisely because annuities:

Are not market-priced securities

Cannot be fairly valued daily

Introduce issuer credit risk

Embed compensation through spread rather than disclosed fees

CITs, by contrast, sit in a regulatory gray zone — particularly state-chartered CITs, which often lack meaningful federal oversight.

These Are Not Synthetic Stable Value Products

Industry defenders often try to blur the lines between:

Synthetic stable value (e.g., Vanguard RST, Fidelity MIPS), and

Insurance general-account or separate-account annuities

They are not the same.

Synthetic stable value:

Uses transparent bond portfolios

Has independent wrap providers

Has explicit fees

Has market-observable returns

Generates little or no insurer spread profit

By contrast, the annuities now appearing in target-date funds are, in my opinion, almost entirely general-account (GA) or separate-account (SA) insurance products, for a simple reason:

There is no meaningful spread profit in true synthetic stable value.

Insurers and recordkeepers are not pushing annuities into target-date funds for diversification. They are doing it because spread is far more profitable than explicit fees — and far harder for fiduciaries to monitor.

Empower Pushes the Envelope Even Further

Empower has gone beyond traditional fixed annuities and is now actively marketing:

Index annuities, and

Target-date structures that explicitly combine annuities with private equity exposure, including partnerships with Blackstone.

Empower proudly announced the launch of what it called the “first ever zero-fee index fund.” That claim deserves skepticism.

“Zero fee” does not mean “no compensation.” It almost always means:

Compensation is embedded

Returns are engineered

Pricing is discretionary

Spread replaces fees

At the same time, Empower has partnered with Blackstone to insert private equity into retirement default investments — layering illiquidity on top of illiquidity, and valuation opacity on top of opacity.

This is not diversification. It is complexity as camouflage.

The Great Gray Stable Value Appendix Tells the Truth

The most revealing disclosure may come not from critics, but from industry documents themselves.

In an appendix to the Great Gray Collective Investment Trust stable value fund, the sponsor discloses material issues with the underlying Empower General Account Fixed Annuity.

Most importantly, the document states that the crediting rate process is “discretionary and proprietary.”

That single sentence is devastating.

It is a direct admission that:

Returns are not the transparent output of a portfolio

Returns are not market-based

Returns are not priced competitively

Returns are the product of internal insurer decision-making

That is the definition of general-account spread mechanics.

For ERISA purposes, it means:

Participants do not receive the return of the assets backing the contract

The insurer retains the difference

The compensation is undisclosed

The fiduciary cannot independently verify reasonableness

Why This Matters Under ERISA

Once fixed annuities are embedded inside target-date funds:

The plan is in an ongoing transaction with a party in interest

Compensation is taken through spread

The fiduciary cannot monitor or benchmark returns

Liquidity is lost without participant consent

Risk is shifted from markets to the insurer’s balance sheet

Performance modeling does not cure any of that.

After Cunningham v. Cornell, fiduciaries cannot rely on:

“Everyone is doing it”

“The glidepath looks good”

“The model outperforms”

If the structure is a prohibited transaction, the remedy is disgorgement, not better charts.

The Bigger Picture

Target-date funds were supposed to simplify retirement investing.

Instead, they are becoming the Trojan horse through which:

Fixed annuities

Index annuities

Private equity

Opaque insurance economics

are quietly introduced into ERISA plans — without SEC oversight, without transparent pricing, and without meaningful participant understanding.

TIAA may be the most visible example. It is no longer the only one.

Bottom Line

Morningstar is right about one thing: There is a hidden trend changing 401(k) plans.

But what it means for investors is not innovation or safety.

It means:

Less transparency

More conflicts

More prohibited transactions

And a coming wave of litigation

Target-date funds are no longer just glidepaths.

They are becoming distribution platforms for insurance spread and alternative-asset fees — and ERISA was never designed to allow that.

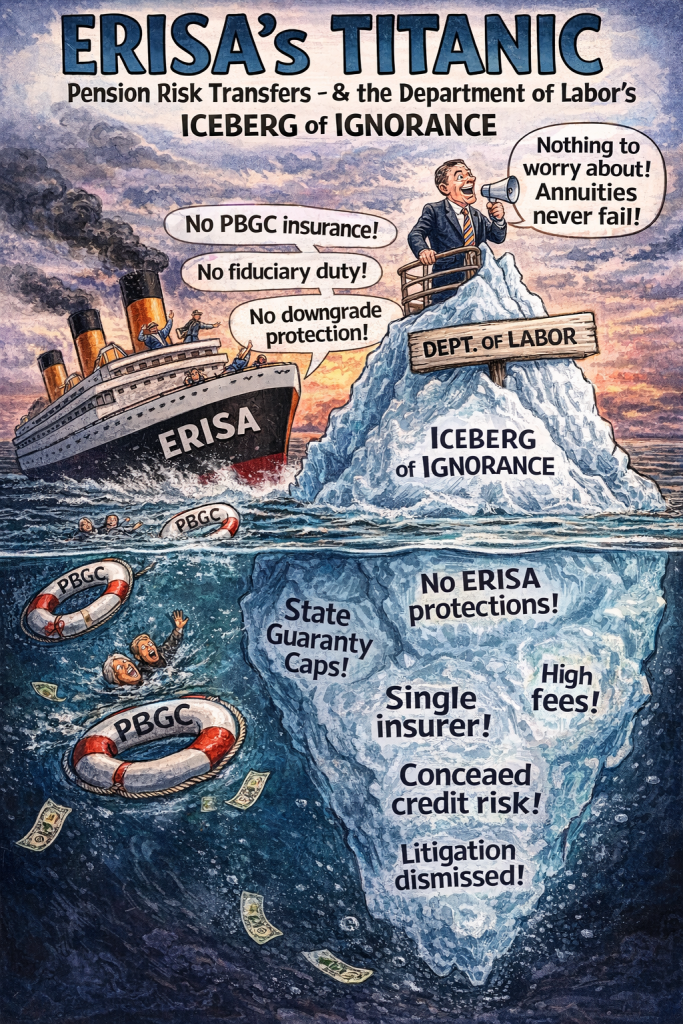

On January 9, 2026, the U.S. Department of Labor filed an amicus brief defending Pension Risk Transfer (PRT) annuities—arguing, astonishingly, that stripping retirees of ERISA protections, PBGC insurance, and diversified pension trusts causes no material harm to participants.

This brief is not a neutral statement of law. It is an industry advocacy document that—if accepted by courts—would effectively legalize the quiet dismantling of defined benefit pensions, one annuity contract at a time.

Below is why the DOL’s position is fundamentally inconsistent with ERISA, economics, and basic fiduciary duty.

1. The DOL’s Central Fiction: “Nothing Material Changes for Participants”

The DOL claims that when a pension is transferred to an insurer via a PRT, participants are “entitled to the same benefits” and therefore suffer no cognizable harm.

This is demonstrably false.

When a PRT occurs, participants immediately lose:

PBGC insurance — a federal backstop worth hundreds of thousands of dollars per participant

ERISA Title I fiduciary protections — prudence, loyalty, prohibited transaction rules

Federal disclosure and reporting rights

Diversification of backing assets — replaced with a single insurer credit

Any ability to enforce ERISA standards going forward

Calling this “no material change” is like saying replacing a diversified investment portfolio with a single unsecured corporate bond is “economically equivalent.”

2. PBGC Insurance Is Real Money — Not a Technicality

The DOL brief treats PBGC insurance as if it were a formality that can be discarded without consequence.

That position collapses under basic math.

PBGC publishes maximum guaranteed benefits every year. For a retiree age 65 in 2025, the present value of PBGC protection exceeds $1.1 million. Lose that protection, and the participant bears the full downside risk of insurer impairment, downgrade, or insolvency.

After a PRT:

PBGC coverage is gone forever

State guaranty associations are capped, fragmented, and far weaker

There is no federal backstop

If PBGC insurance were meaningless, Congress would not have created it, funded it, or regulated it for 50 years.

3. The Brief Abuses Thole to Create Fiduciary Immunity

The DOL leans heavily on Thole v. U.S. Bank to argue that participants lack standing unless insurer failure is “certainly impending.”

This is a gross misapplication of Thole.

Thole addressed fluctuations in plan investments within an ongoing ERISA plan. It did not bless fiduciaries’ ability to:

Strip statutory protections

Transfer participants to weaker legal regimes

Ignore credit and downgrade risk

Concentrate retirement security in a single insurer

Loss of ERISA protections and PBGC insurance is a present injury, not a speculative one.

Under the DOL’s logic, fiduciaries could sell pensions to any insurer—no matter how risky—so long as collapse has not yet occurred.

That would turn ERISA into a “wait until retirees are harmed” statute, which is the opposite of what Congress intended.

4. IB 95-1 Is Being Quietly Rewritten as a “Check-the-Box” Safe Harbor

The DOL insists that Interpretive Bulletin 95-1 is purely about “process,” not outcomes.

That is revisionist history.

IB 95-1 requires fiduciaries to act for the purpose of obtaining the safest available annuity. Safety is not a memo. It is a risk outcome.

Yet under the DOL’s litigation posture:

CDS spreads are ignored

Downgrade risk is ignored

Contractual lock-ins are ignored

Lack of termination or portability rights is ignored

A “process” that predictably results in riskier annuities is not prudent. It is negligent.

5. The Most Damning Omission: Downgrade Risk Doesn’t Exist (According to DOL)

The amicus brief never seriously grapples with downgrade risk—the single most important risk in long-dated annuity contracts.

PRT annuities typically:

Lack downgrade-trigger exit rights

Lack of collateral posting requirements

Lock participants into deteriorating credits

Transfer upside to insurers, downside to retirees

Without downgrade provisions, participants are trapped in a slow-motion credit failure with no remedy.

If PRT annuities were truly safe, insurers would offer downgrade protections. They don’t—because doing so would reduce profits and increase capital requirements.

6. “No Annuity Has Ever Failed” Is Not a Fiduciary Standard

The DOL reassures courts that no PRT annuity has failed yet.

That argument has been used before:

Subprime CDOs (pre-2008)

AIG Financial Products

Silicon Valley Bank

ERISA is a forward-looking fiduciary statute, not a tombstone statute.

By the time an annuity fails, retirees have already lost.

7. ERISA Was Designed to Avoid Exactly This Outcome

The DOL’s brief celebrates the shift from federal ERISA protections to state insurance regulation.

That is historically backwards.

ERISA was enacted because:

State regulation was fragmented

Workers were unprotected

Promises were broken

PRTs reverse that progress—quietly and permanently.

The Bottom Line

The Department of Labor’s PRT amicus brief is not pro-worker. It is pro-insurer, pro-employer, and anti-enforcement.

If courts adopt this framework:

Fiduciaries will be immune from scrutiny

PBGC protections can be stripped without consequence

Downgrade risk will be ignored

ERISA will become unenforceable until after retirees are harmed

That is not statutory interpretation. It is regulatory surrender.

PRT cases must be appealed—not just for retirees today, but to preserve the very idea that ERISA means something tomorrow.

Appendix: How Courts Are Weaponizing Thole to Immunize Pension Risk Transfers — The Verizon Case Study

The recent dismissal of the Verizon Pension Risk Transfer (PRT) case by Judge Alvin Hellerstein is a textbook example of how Thole v. U.S. Bank is being misused to eviscerate ERISA’s core protections for defined-benefit pension participants. The decision illustrates precisely why the Department of Labor’s January 2026 PRT amicus brief is so dangerous—and why appellate courts must intervene.

1. The Verizon Plaintiffs Alleged Immediate, Concrete Harm — Not Speculative Injury

The Verizon retirees alleged far more than abstract risk. According to the First Amended Complaint, Verizon transferred $5.7 billion in pension assets covering 56,000 retirees to Prudential (PICA) and RGA, permanently removing participants from:

ERISA Title I fiduciary protections

PBGC insurance coverage

Uniform federal disclosure and enforcement rights

The complaint details that retirees went from uncapped, lifetime PBGC protection to state guaranty association caps—often $250,000–$500,000 per lifetime, depending on state of residence, with immediate haircut risk in states like California (80% cap) 2025-04-25 [dckt 55] PL FIRST A…. in addition the solvency of State guarantee associations are https://commonsense401kproject.com/2025/06/24/state-guarantee-associations-behind-annuities-are-a-joke/ That is not conjecture. That is quantifiable, present economic harm.

Yet the court dismissed the case on standing grounds, holding that because benefits were still being paid today, no Article III injury existed.

2. This Is Not Thole — This Is the Destruction of Statutory Rights

Thole involved participants in an ongoing defined-benefit plan complaining about plan-level investment losses where benefits remained fully guaranteed by the sponsor and PBGC.

The Verizon case is fundamentally different:

Thole

Verizon PRT

Plan remained intact

Plan terminated

ERISA protections remained

ERISA protections eliminated

PBGC backstop intact

PBGC backstop extinguished

Sponsor still liable

Sponsor fully discharged

Judge Hellerstein nevertheless treated the case as indistinguishable from Thole, holding that loss of ERISA protections, PBGC insurance, and federal enforcement rights is not a cognizable injury unless and until an insurer fails 2026-01-08 [dckt 97] Opinion An….

That reasoning converts ERISA into a post-collapse remedy, not a preventive fiduciary statute.

3. The Court Ignored Congress’s Explicit Response to Executive Life

The Verizon complaint correctly traced Congress’s reaction to the Executive Life collapse, which wiped out tens of thousands of annuitized retirees in the early 1990s. Congress responded with:

The Pension Annuitants Protection Act (PAPA)

A new statutory cause of action under ERISA § 502(a)(9)

DOL’s Interpretive Bulletin 95-1, requiring fiduciaries to seek the safest available annuity

The Verizon court acknowledged these statutes—but rendered them meaningless by holding that participants cannot sue until after catastrophe strikes.

That reading nullifies § 502(a)(9) entirely.

4. Downgrade Risk Was Pleaded — and Ignored

The Verizon plaintiffs alleged detailed facts showing that PICA and RGA:

Relied heavily on affiliated captive reinsurers

Used Modified Coinsurance (ModCo) to inflate capital ratios

Had affiliated exposures exceeding $72 billion, dwarfing surplus

Operated through regulation-light jurisdictions

These are not default allegations. They are downgrade-pathway allegations—exactly the type of slow-motion credit deterioration that destroys annuity value long before insolvency.

Yet the court dismissed these allegations as irrelevant because no payment had yet been missed.

This mirrors the DOL amicus brief’s central flaw: treating annuity credit risk as binary (fail / not fail) rather than probabilistic and dynamic.

5. The Decision Confirms the Worst-Case Scenario of the DOL’s Amicus Brief

The DOL argues that participants lack standing to challenge PRTs absent imminent insurer collapse. The Verizon decision shows where that logic leads:

Fiduciaries may ignore downgrade risk

Fiduciaries may choose cheaper, riskier annuities

Fiduciaries may strip PBGC protection without consequence

Courts will dismiss suits with prejudice

In Verizon, the court did exactly that—dismissing the case with prejudice, despite extensive factual allegations, expert declarations, and historical precedent.

6. The Practical Result: ERISA Becomes Unenforceable in PRT Cases

Under the Verizon / DOL / Thole framework:

A participant cannot sue before a downgrade

Cannot sue after a downgrade

Cannot sue until benefits are cut

And by then, ERISA no longer applies

This is not statutory interpretation. It is functional repeal by judicial doctrine.

Bottom Line

The Verizon decision is not an outlier. It is the inevitable outcome of the DOL’s current litigation posture on PRTs.

By misusing Thole, courts are transforming ERISA from a protective fiduciary statute into a “wait-for-collapse” regime—exactly the failure Congress sought to prevent after Executive Life.

This case should not be the model. It should be the warning.

Why This Appendix Matters

This appendix demonstrates, with a real case and a real dismissal, that the DOL’s amicus brief is not theoretical harm—it is already reshaping outcomes. Courts are no longer asking whether annuities are safe. They are asking only whether retirees have already been harmed.

Without them, plans are locked into a death spiral toward default. With them, annuities can actually work within a responsible fiduciary framework. By Chris Tobe, CFA

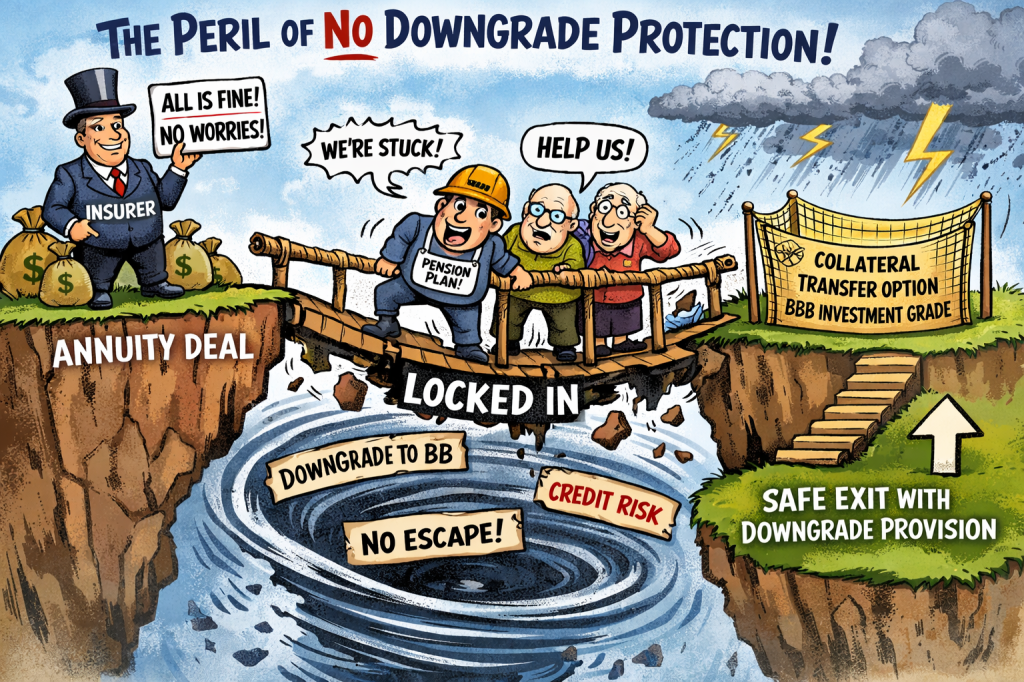

All annuities in plans, fixed annuities, and lifetime income annuities in DC plans need downgrade provisions. However, the largest immediate use is the Pension Risk Transfer (PRT) annuities, which allow defined benefit plans to offload longevity risk. But there’s a hidden structural flaw in most annuity contracts: no downgrade protection. In plain English, that means a plan can pay millions or billions to an insurer and then be held hostage if the insurer’s credit deteriorates.

This is not a hypothetical risk. Recent litigation and real-world defaults show that without contractual protections tied to credit quality, plans are effectively locked into a downward spiral that can lead to underfunding, distress, or worse — a default without protection from any agency like the PBGC.

What’s a Downgrade Provision — and Why It Matters

A downgrade provision is a contractual term that triggers plan protections if the insurer’s credit rating slips below agreed thresholds. These protections can include:

Mandatory collateral posting

Escrow or trust funding for future liabilities

Termination or transfer rights

Step-up pricing or premium refunds

In other words: if the insurer’s credit weakens, the plan gains leverage and protection.

Without downgrade protections, plans have no recourse until the insurer fails outright.

Why Current Annuities Trap Plans in a Death Spiral

Most PRT contracts do not include meaningful downgrade provisions. Plans that sign these deals typically:

Pay upfront premiums that are irrevocable

Give up the assets and liability control

Lose leverage if the insurer’s credit deteriorates

Are left with nothing but hope that the insurer stays solvent

This creates a lock-in effect:

The plan can’t go back to the market

It can’t demand collateral

It can’t shift to a stronger carrier

It can’t adjust to changing market conditions

If the insurer is later downgraded — from A to BBB, or BBB to BB — the plan has zero contractual rights to protect its interests. The result? A death spiral where liabilities are fixed but the counterparty becomes riskier and less reliable.

PRT’s Best Annuity Would Have Downgrade Provisions

DOL with PRT’s calls for the best available annuity. The best possible annuity for a plan isn’t necessarily the lowest-priced one. It’s the one that:

Complies with the plan’s Investment Policy Statement