“Cerulli Edge—U.S. Retirement Edition,” finds that as of 2024, 91% of asset managers believe guaranteed lifetime income options carry a negative stigma. “Annuities continue to face perception issues due to high fees, complexity, lack of transparency, and concerns about insurer solvency, all of which deter plan participants,” says Idin Eftekhari, a senior analyst at Cerulli. “The tradeoff between liquidity and a guaranteed income stream is unappealing for many participants.[iii]

The argument that you need annuities to provide lifetime income is debunked as well.

Cerulli also points to lower cost transparent liquid methods of providing monthly income called “structured drawdown strategies” as superior alternatives to annuities.[iv]

Annuities are a Fiduciary Breach

I wrote in 2022 that all annuities are a fiduciary breach [v] While Guaranteed Income Annuities are still small in 401(k)s, I believe they are being used to justify even worse annuity products like IPG Fixed Annuities and Index annuities. Immediate Participation Guarantee (IPG) is a Group fixed annuity contract (GAC) written to a group of investors in a DC Plan and not individuals. [v]

IPG group annuities have no maturity, and set whatever rate they want without a set formula.

Annuities are contracts that are an ERISA Prohibited Transaction. Annuity providers claim their products are subject to Prohibited Transaction Exemption 84-4, but I have found that most annuities I have seen do not qualify for the exemption.[vi]

Annuity contracts are regulated by weak state insurance commissioners, and most plan sponsors are clueless to that fact. The National Association of Insurance Commissioners (NAIC) sets weak national standards, but some state insurance commissioners have even weaker regulations. NAIC’s prime goal is to prevent any national regulation or transparency as evidenced in this letter to Congress. [vii] NAIC is currently trying to hide insurers Risk Based Capital (RBC) scores to hide significant risk from consumers. [viii]

There is an attempt to hide annuities in Target Date Funds in weak state regulated CIT’s in which I testified on to the DOL Advisory Committee in July 2024.[ix]

Annuity contracts shift all the fiduciary burden from themselves to the plan. Thus, the burden of proof is on plan sponsors regarding if their plan annuity qualifies for an exemption from being classified as a prohibited transaction.[x]

Annuities Credit & Liquidity Risk High & Getting Higher

A recent Federal Reserve paper exposes poor state & offshore regulation of Life Insurance companies that issue Annuities. The FED’s main problem is the hiding and understating of credit, liquidity & leverage risks.[xi]

The FED economists contend that life and annuity issuers make investments in what amount to loans to risky firms look stronger by funneling the weak loans through arrangements — such as business development companies, broadly syndicated loan pools, collateralized loan obligations, middle-market CLOs and joint venture loan funds — that qualify for higher credit ratings.[xii]“These arrangements seek to shift portfolio allocations towards risky corporate debt while exploiting loopholes stemming from rating agency methodologies and accounting standards.”[xiii]

Insurance risk experts Larry Rybka, Thomas Gober, Dick Weber Michelle Gordon highlight the addition of risks from Reinsurance in a recent trade publication. Rybka says The life insurance and annuities industry, he said, has become “like the Wild West.” Carriers are abusing reinsurance,”[xiv] “It’s a shell game and, in general, the regulators are not paying attention,” said Dick Weber,[xv]Gober says It’s not just offshore reinsurers that can largely skirt U.S. accounting standards, he said. There are also “captive” reinsurance companies within the U.S. mostly in Vermont, South Carolina, and Delaware. “The lack of transparency with these affiliated reinsurance companies, both captive and offshore, is the single biggest threat to U.S. policyholders and annuitants,” said Gober.[xvi]

Michelle Gordon says that advisors should check the creditworthiness of any insurance companies they recommend to clients, she said, though most don’t or can’t because of lax ratings standards. “The non-codification of insurance advisement results in sub-optimization of consumer protections,” she said.[xvii]

Fiduciaries should be aware of these risks and have a duty to defend and justify these risks if they put annuities in their plans.

Annuities should not be allowed in 401(k)s. ERISA created the concept of Prohibited Transactions to prohibit any investments with clear Conflicts of Interest. I testified to the ERISA Advisory Council – US Department of Labor in July of 2024 on the danger of allowing annuities to be hidden inside of Target Date Funds. [i] I have co-written a paper with Economics Professor Tom Lambert on the excessive risks of annuities.[ii]

Perhaps with the exception of Crypto and Private Equity no investment better describes what should be a prohibited transaction more than annuity contracts.

Annuities are a Fiduciary Breach for 4 basic reasons.[iii]

Single Entity Credit Risk

Single Entity Liquidity Risk

Hidden fees spread and expenses

Structure -weak cherry-picked state regulated contracts, not securities and useless reserves

So why do we still see annuities in 401k plans? The reason is intense lobbying by the insurance industry, that has blocked any transparency or oversight.

Annuity providers claim to be barely legal by relying on an Prohibited Transaction Exemption (PTE 84-4) a “get out of jail free card” obtained by $millions of lobbying by the insurance industry.

Biden Fiduciary Rule

The new Biden Fiduciary rule would provide transparency that would further expose these annuity products’ conflicts of interests. The insurance industry has forue shopped in Texas in the Fifth Circuit for judges who agree with blocking transparency to block it for now.

At the Certified Financial Planner Board of Standards Connections Conference in Washington October 2024, DOL officials called out annuities as prohibited transactions. [iv] Ali Khawar, principal deputy assistant secretary for the Employee Benefits Security Administration, laid out the reasons why the Biden Labor Department continues to fight for a fiduciary rule ““To me it continues to be kind of nonsensical that you’re expecting any of your clients to walk into someone’s office and have in their head: ‘I’m dealing with this person who’s going to sell insurance to me, this person is relying on [Prohibited Transaction Exemption] PTE 84-24, not [PTE] 2020-02. Those things shouldn’t mean anything to the average American. And we shouldn’t expect them to.”

broker-dealer space transformed what it means to be in the advice market,” Khawar said. “When we looked at the insurance market, though, we didn’t quite see the same thing.”

Under the National Association of Insurance Commissioners’ model rule, for example, “compensation is not considered a conflict of interest,” Khawar said. “So there are pretty stark differences between what you see in the CFP standard, the Reg BI standard, and what has now been adopted by almost every state, one notable exception of New York, which has adopted a standard that is significantly tougher than the NAIC model rule.”[v]That process is “the CFP standard, the DOL standard, it’s the SEC standard for investment advisors and it’s Reg BI,” Reish continued. What it’s not? “The NAIC model rule,” Reish said.

“The NAIC model rule does not require the comparative analysis[vi]

Khawar added: “It’s not going to matter whether you’re providing advice about an annuity, a variable annuity, fixed income annuity, indexed annuity, security or not.” The goal with the 2024 rule, Khawar added, is to “have a common standard across the retirement landscape so that all retirement investors would be able to make sure that when someone is marketing up front best-interest advice, that that’s the standard they’d be held to by the regulator and the customer.”

Under the Employee Retirement Income Security Act, “being a fiduciary is critical to the central question of whether or not the law or consumer protections have fully kicked in or not,” Khawar added.

The Government Accounting Office wrote a piece in August in support of the Biden Fiduciary rule. They saw the problem as so severe that they suggested that IRS step in to help the DOL Better Oversee Conflicts of Interest Between Fiduciaries and Investors especially in the Insurance Annuity Area. [vii] Senator Elizabeth Warren in defense of the Biden Fiduciary rule prepared a report on the numerous conflicts of interest in annuity commissions and kickbacks. [viii]

Annuities days of hiding behind PTE 84-4 are over

Prohibited transaction exemptions are subject to meeting certain requirements. They include

The Impartial Conduct Standards.

Written Disclosures.

Policies and Procedures

Annual Retrospective Review and Report

The Impartial Conduct Standards have 4 major obligations.

A. Care Obligation

B. Loyalty Obligation

C. Reasonable compensation limitation

D. No materially misleading statements (including by omission)

Care Obligation

This obligation reflects the care, skill, prudence, and diligence – similar to Prudent Person Fiduciary standard. Diversification is one of the most basic fiduciary duties. Fixed annuities flunk this with single entity credit and liquidity risk. Diligence is nearly impossible with misleading nontransparent contracts, and the lack of plan/participant ownership of securities. The Federal Reserve in 1992 exposed the weak state regulatory and reserve claims.[ix]

Loyalty Obligation

Annuity contracts are designed to avoid all fiduciary obligation with no loyalty to participants. Secret kickback and commissions place the financial interests of the Insurers and their affiliates over those of retirement investors.[x]

The exemption requires the advisor to show their loyalty with a “Fiduciary Acknowledgement Disclosure.” Annuity contracts avoid any fiduciary language or responsibility.

Reasonable compensation limitation

Annuities have a total lack of disclosure of profits, fees and compensation. They have secret kickback commissions.

A number of lawsuits have settled with claims of excessive secret fees and spreads. An Insurance executive bragged at a conference of fees over 200 basis points (2%) in 2013. [xi]

No materially misleading statements (including by omission)

Annuities have numerous material misleading statements, including the total lack of disclosure of spread/fees. They claim principal protection, but some fixed annuity contracts recently have broken the buck and violated their contracts. The written disclosures under weak state regulations omit critical information on risks and fees.

Most plans with annuities do not have Investment policy statements, since most fixed annuities would flunk them on diversity and transparency and not be allowed. Annuities cannot provide the transparency to follow CFA Institute Global Performance Standards (GIPS) so they do not comply.[xii] Most 401(k) committees with insurance products do not review such annuity products, since they clueless on what they are. Consultants for plans with annuities do not review the annuities most of the time since they are conflicted and they themselves receive kickbacks from annuity providers.

Annuities as a Prohibited Transaction

Annuities hide most of their compensation. They are typically secret no bid contracts with no transparency and numerous conflicts of interest. They are subject to weak state regulations (sometimes categorized as NAIC guidelines). Many times they are a party of interest and shift profits from annuities to make other fees appear smaller.

Annuities are clearly prohibited transactions, but have used their lobbying power in Washington and in states to exempt themselves from all accountability.

Liability-driven investing is a common concept in connection with defined benefit plans. I first heard the term used in a article by Marcia Wagner of the Wagner Group. Liability-driven investing refers to the selection of investments that are best designed to help the plan secure the returns needed by the plan to fulfill their obligations under the terms of the plan.

It has always struck me that the liability-driven concept is equally applicable to designing defined contribution plans such as 401(k) and 403(b) plans. Better yet, by factoring in fiduciary risk management principles, defined contribution plans can create the best of both worlds, win-win plans that provide prudent investment options while minimizing or eliminating fiduciary risk.

Plan sponsors often unnecessarily expose themselves to fiduciary liability simply because they do not truly understand what their duties are under ERISA. One’s fiduciary duties under ERISA can be addressed by asking two simple questions.

1. Does Section 404(a) of ERISA explicity require that a plan offer the category of investments under consideration? 2. If so, could/would inclusion of the investment under consideeration result in uunecessary liability exposure for the plan?

As for the first question, Section 404(a)1 of ERISA does not explicity require that any specific category of investment be offered within a plan. As SCOTUS stated in the Hughes decision2, the only requirement under Section 404(a) is that each investment option offered within a plan be prudent under fiduciary law. Furthermore, as SCOTUS stated in its Tibble decision3, the Restatement of Trusts (Restatement) is a valuable resource in addressing and resolving fiduciary issues.

As for the second question, Section 90 of the Restatement, more commonly known as the “Prudent Investor Rule,” offers three fundamental guidelines addressing the importance of cost-consciousness/cost-efficiency of a plan’s investment options:

The last bullet point highlights a key aspect of 401(k)/403(b) fiduciary prudence and cost-efficiency – commensurate return for the additional costs and risks assumed by the plan participant. In terms of actively managed mutual funds, research has consistently and overwhelmingly shown that the majority of actively managed mutual funds are cost-inefficient:

99 % of actively managed funds do not beat their index fund alternatives over the long term net of fees.4

Increasing numbers of clients will realize that in toe-to-toe competition versus near-equal competitiors, most active managers will not and cannot recover the costs and fees they charge.5

[T]here is strong evidence that the vast majority of active managers are uable to produce excess returns that cover their costs.6

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.7

The Active Management Value RatioTM (AMVR) Several years ago I created a simple metric, the AMVR. The AMVR is based on the research of investment icons such as Nobel laureate Dr. William F. Sharpe, Charles D. Ellis, and Burton L. Malkiel. The AMVR allows plan sponsors, trustees, and other investment fiduciaries to quickly determine whether an actively managed fund is cost-efficient relative to a comparable index fund. The AMVR allows the user to assess the cost-efficiency of an actively managed fund from several perspecitives.

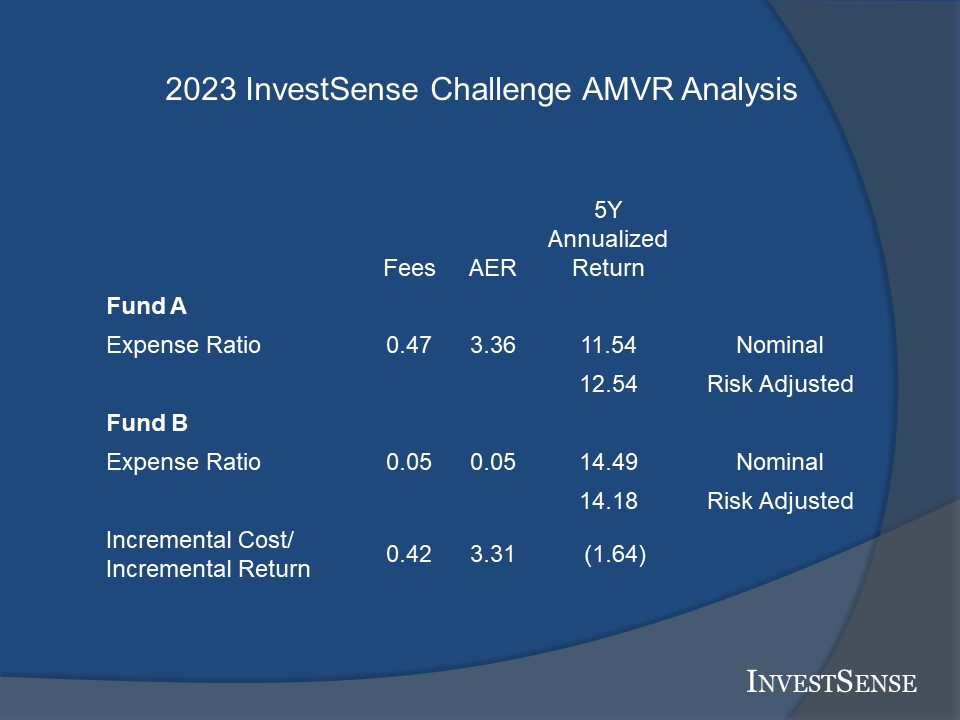

The slide below shows an AMVR analysis comparing the retirement shares of a popular actively managed fund, the Fidelity Contrafund Fund (FCNKX), and the retirement shares of Vanguard’s Large Cap Growth Index Fund (VIGAX). The analysis compares the two funds over a recent 5-year time period. When InvestSense provides forensic services, we provide both a five-year and ten-year analysis to determine the consistency of any cost-efficiency/cost-inefficiency trend.

An AMVR analysis can provide any amount of detail the user desires. On a basic level, the fact that the actively managed fund failed to outperform the comparable index fund benchmark immediately indicates that the actively managed fund is imprudent relative to the Vanguard fund.

Add to that the fact that the actively managed fund imposed an incremental, or additional, cost of 42 basis points without providing any corresponding benefit for the investor. A basis point is a term commonly used in the investment world. A basis point equals 1/100th of one percent (0.01). 100 basis points equals 1 percent.

So the bottom line is that the actively managed fund underperformed the benchmark Vanguard fund and imposed an additional charge without providing a commensurate return for the extra charge. A fiduciary’s actions that result in wasting a client’s or a beneficiary’s money is never prudent.8

If we treat the actively managed fund’s underpreformance as an opportunity cost, and combine that cost with the excess fee, we get a total cost of 2.06. The Department of Labor and the General Accountability Office have determined that over a twenty year time period, each additional 1 percent in costs reduces an investor’s end-return by approximately 17 percent.9 So, in our example, we could estimate that the combined costs would reduce an investor’s end-return by approximately 34 percent. This is not an example of effective wealth management.

The AMVR is calculated by dividing an actively managed fund’s incremental correlation-adjusted costs by the fund’s incremental risk-adjusted return. The goal is an AMVR score greater than zero, but equalt to or less than one, which indicates that costs did not exceed return. While the user can simply use the actively managed fund’s incremental cost and incremental returns based on the two funds’ nominal, or publicly reported, numbers, the value of such an AMVR calculation is very questionable.

A common saying in the investment industry is that return is a function of risk. In other words, as comment h(2) of Section 90 of the Restatement states, investors have a right to receive a return that compensates them for any additional costs and risks they assumed in investing in the investment. The Department of Labor has taken a similar stand in two interpretive bulletins.10 That is why a proper forensic analysis always uses a fund’s risk-adjusted returns.

While the concept of correlation-adjusted returns is relatively new, it arguably provides a better analysis of the alleged value-added benefits, if any, of active management. The basis premise behind correlation-adjusted costs is that passive management often provides all or most of the same return provided by a comparable actively managed fund. As a result, the argument can be made that the actively managed fund was imprudent since the same return could have been achieved by passive management alone, without the wasted excess costs of the actively managed fund.

Professor Ross Miller created a metric called the Active Expense Ratio (AER).11 Miller explained that actively managed funds often combine the costs of passive and active management in such a way that it is hard for investors to determine if they are receiving a commensurate return. The AER provides a method of separating the cost of active management from the costs of passive management.

The AER also calculates the implicit amount of active management provided by an actively managed fund, a term that Miller refers to as the actively managed fund’s “active weight.” Miller then divides the active fund’s incemental costs by the fund’s active weight to calculate the actively managed fund’s AER.

Miller found that an actively managed fund’s AER is often 400-500 percent higher than the actively managed fund’s stated expense ratio. In the AMVR example shown above, dividing the actively managed fund’s incremental correlation-adjusted costs by the fund’s active weight would result in an implicit expense ration approximately 700 percent higher than the fund’s publicly stated incremental cost (3.31 vs. 0.42). Based on the AER, these significantly higher costs would be incurred to receive just 12.5 percent of active management.

Using the same 1:17 percent analysis for each additional 1 percent in costs/fees, using the AER metric and the active fund’s underperformance would result in a projected loss of approximately 84 percent over twenty years. So much for “retirement readiness.”

Additional information on the AMVR can be found at my “The Prudent Investment Fiduciary Rules” blog and searching under “Active Management Value Ratio.”

Fiduciary Risk Management and Annuities I have written numerous posts about annuities on both my “The Prudent Investment Fiduciary Rules” blog and my “CommonSense InvestSense” blog. Fortunately, the inherent fiduciary liability issues can be addressed by using the same two question fiduciary risk management approach that was mentioned earlier, with the answer to both questions being “yes.” Therefore, a liability-designed 401(k)/403(b) plan will totally avoid the inclusion of annuities, in any form, within the plan.

As a former securities compliance director, I am very familiar with the questionable marketing techniques used by some annuity companies, including the ongoing refusal to provide full transparency with regard to spreads and other financial information. Both ERISA and Department of Labor interpretive bulletions have stressed the importance of providing material information to plan sponsors and plan participants so that they can make informed decisions about including annuities within a plan and about whether to invest in annuities.

The two blogs provide analyses of various types of annuities, especially variable annuities and fixed indexed annuities. My basic advice to my fiduciary risk management clients is simple – “if you don’t have to go there…don’t!”

Annuities are complex and confusing investments, with numerous potential fiduciary liability “traps.” Annuity advocates often try to further confuse and intimidate plan sponsors by engaging in technical details. I strongly recommend adopting my response – stop them before they begin and simply explain that ERISA does not require that pension plans offer annuities within a plan. Therefore, from a fiduciary risk management standpoint, there is no reason to offer any type of annuity within the plan.

Going Forward Three fiduciary risk management questions that I often ask both myself and my fiduciary clients:

Why is it that cost/benefit analysis is often used by businesses to determine the cost-efficiency of a proposed project, but yet cost-efficiency is rarely used by plan sponsors and other investment fiduciaries to determine the cost-efficiency of investments being considered by a pension plan or other fiduciary entity?

Why is it that plan sponsors will blindly accept conflicted advice from “advisers” without requiring that the adviser document the prudence of their recommendations througn prudence/breakeven analyses such as the AMVR or an annuity breakeven analysis?

Why do plan sponsors insist on making it so unnecessarily difficult and costly by refusing to see the simplicity, praticality, and prudence of the federal government’s Thrift Saving Plan?

The three bullet points remind me of one of my favorite quotes – “there are none so blind, as they who will not see.” I am not sure to whom it should be properly atttributed. The two most cited sources are the Bible and Jonathan Swift.

The point of this post is to emphasize that ERISA compliance is not that difficult to accomplish if a plan talks with the right people and approaches the compliance issues right from the start, when actually designing or re-designing the plan . If that is not possible, there are relatively simple ways to transaction into a liability-driven plan.

One of the services InvestSense provides is fiduciary prudence oversight services. By using fiduciary prudence and risk management compliance tools such as the AMVR and annuity breakeven analyses, and requiring that all plan advisers and investment consultants document their value-added proposition with such validating documents, a plan sponsor can significantly and efficiently simplify the required administration and monitoring of their 401(k) or 403(b) plan.

Notes 1. 29 CFR § 2550.404(a); 29 U.S.C. § 1104(a). 2. Hughes v. Northwestern University., 142 S. Ct. 737, 211 L. Ed. 2d 558 (2022) 3. Tibble v. Edison International, 135 S. Ct 1823 (2015). 4. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010). 5. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e. 6. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016. 7. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).99 8. Uniform Prudent Investor Act, https://www.uniformlaws.org/viewdocument/final-act-108?CommunityKey=58f87d0a-3617-4635-a2af-9a4d02d119c9 (UPIA). 9. Pension and Welfare Benefits Administration, “Study of 401(k) Plan Fees and Expenses,” (DOL Study) http://www.DepartmentofLabor.gov/ebsa/pdf; “Private Pensions: Changes needed to Provide 401(k) Plan Participants and the Department of Labor Better Information on Fees,” (GAO Study). 10. 29 CFR Section 2509.94-1 )(IB 94-1) and Section 2509.15-1 (IB 15-1). 11. Ross Miller, “Evaluating the True Cost of Active Management by Mutual Funds,” Journal of Investment Management, Vol. 5, No. 1, 29-49 (2007) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=746926.

Copyright InvestSense, LLC 2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought

To invest in annuities, you must look the other way at one of most basic investment principals -diversification, i.e., “do not put your eggs in one basket”[1]

In my latest submitted paper, cowritten with economist Tom Lambert, ““Safe” Annuity Retirement Products and a Possible U.S. Retirement Crisis,” we expose the fact that the “emperor has no clothes,” as the life insurance Industry has flooded billions of dollars into advertising, lobbying, commissions, and trade articles with misinformation on annuities with everyone afraid to call out the obvious fiduciary problems – single entity credit and liquidity risk. Excessive monopolistic profits through secret spread fees have remained hidden with no federal regulation or oversight.

We disprove the misleading claim by insurance companies that annuities are primarily backed by a portfolio of high-quality fixed income securities. We show that only 12.5% of the portfolio of the highest rated insurer, TIAA, is highly rated securities (AA & AAA bonds).

We reveal the weakness of the state guarantee associations behind annuities, which are so flimsy they cannot even get the lowest junk grade rating from S&P or Moody’s.

We show that annuities have the highest liquidity risk of any investment in retirement plans. Even when an annuity provider’s credit risk is downgraded, investors cannot get out, even when downgraded to junk and are stuck in a death spiral all the way to default.

Hopefully, the Department of Labor’s new fiduciary rules will be enacted and protect participants in private sector retirement plans from these risks.[2]

Plans and Investors need greater transparency and true fiduciaries, not insurance salesmen – advisors who do not have insurance licenses and who will not be tempted by the huge commissions in annuities.

I want to applaud the Biden Administration on bringing Annuity Junk fees into the light of day to protect investors.

I want to focus on the effect of annuity junk fees in current ERISA protected defined contribution plans (I will address401(k) and 403(b) and cover rollover junk annuity fees in another article.) While the White House release mentions the savings in current plans from index annuities, I think that fixed annuities savings could be much larger over $9 billion a year. (It is important to note that fixed annuities and index annuities in government defined contribution plans in both 457 and 403(b) are not protected by ERISA and add to many more billions of dollars.)

My $9 billion a year comes from industry figures on General Account fixed annuities at $386 billion and separate account fixed annuities at $76 billion in ERISA defined contribution assets. [i]

However, it is important to note that the largest provider of fixed annuities in defined contribution plans (governed by ERISA) is TIAA, which has substantially lower fees and commissions, than the other mainstream insurance providers

Fixed annuities for the most part do not disclose fees and are rate based. For example, when a similar competitive fixed annuity in a plan like TIAA pays 4% many insurers only pay 2% – pocketing the spread. Bloomberg quoted an insurance executive bragging about these hidden 2%+ in fees at a Wall Street conference.[ii] These hidden spread fees have the same negative effect on investors that disclosed mutual fund fees have.

HOW DO I KNOW THIS I currently consult on excessive fees in insurance products. I spent 7 years making insurance products for Transamerica Life (TA), one of the largest U.S. insurance companies. I was an officer of seven different TA companies governed by four different states. I saw the need for federal intervention, as insurers had the ability to select the state regulator with the loosest regulations and lowest capital requirements.

RISKS One of the most basic fiduciary principles is diversification. Annuities make a mockery of this principle with their single entity credit and liquidity risk. [iii]

After the first annuity risk crisis in 1992 the Federal Reserve wrote a major paper on the weakness of state regulations in the insurance area. [iv]

In 2008 Federal Reserve Chairman Ben Bernanke said about these annuity products “workers whose 401(k) plans had purchased $40 billion of insurance from AIG against the risk that their stable-value funds would decline in value would have seen that insurance disappear.”[v]Even when the federal government steped up to control risk in annuity products after the 2008 financial crisis, the insurance industry used its immense lobbying ability to thwart regulations and maximize profits. [vi]

ACCOUNTABILITY In light of recent money market rates of over 5%, these low 2-3% annuity rates in 401(k)’s in far riskier products are especially troubling, costing investors billions of dollars in retirement savings while taking much higher risks.

Hopefully, these junk fee rules will slow the growth of these high fee high risk products inside of 401k plans. The latest con game is selling annuities under the guise of Guaranteed Income. [vii]

Hopefully, this junk annuity initiative will expose some of the 401(k) target date funds which are burying index and fixed annuities inside weakly state regulated Collective Investment Trusts (CIT)s. [viii]

Hopefully, 401(k) consultants who claim to be somewhat independent will be exposed by showing how they use their insurance licenses for additional backdoor commissions.[ix]

Hopefully, within 401(k) plans they will either replace fixed annuities with diversified lower risk synthetic stable value products or at the minimum pay competitive rates like TIAA. [x]

This Biden Annuity Junk Fee initiative will save retirement investors billions. Please do not let the Insurance Industry water it down to line their own pockets.

Chris Tobe, CFA, CAIA is a national expert on excessive fees in retirement plans. He has written 4 books and dozens of articles on transparency, excessive fees & corruption in investments. His own firm Tobe Consulting has advised on over 70 ERISA legal cases on behalf of investors who have lost money through risky and/or high fee investments. He serves as Chief Investment Officer for a minority woman owned pension consulting firm out of New Orleans the Hackett Robertson Tobe group

The Investment Policy Statement (IPS) for a pension plan or other investment pool is a critical element in the governance and is a main fiduciary control on investments.

As stated in the IFEBP Investment Policy Handbook, “If an employee benefit plan does not have an investment policy statement, it does not have an investment policy.”[i] Chris Carosa, in his Forbes column, says a “401(k) IPS is a legal document that serves as the solid compliance backbone of the plan”.[ii]Josh Itzoe in his book, the Fiduciary Formula, says about an IPS, “I believe a written investment policy is the only way to demonstrate a thoughtful process and make well informed, prudent investment decisions consistent with the fiduciary requirements imposed by ERISA.” [iii]

A major U.S. regional ERISA law firm for plans remarked,

Since most plans maintain an IPS, not having one can be seen as ‘outside the lines’ and may subject the plan’s fiduciary compliance to greater scrutiny. In fact, it is not hard to imagine a plaintiff’s firm arguing that a plan’s failure to have an IPS is de facto evidence of a fiduciary breach.[iv]

In the CFA standards for Pension Trustees says “Effective trustees develop and implement comprehensive written investment policies that guide the investment decisions of the plan (the “policies”).” [v]The CFA Code assumes any investments of any size will have an Investment Policy Statement (IPS).

The Society for Human Resources Management (SHRM) outlined the percentage of defined contribution plans with an Investment Policy Statement. Basically 90% for plans over $50mm in 2008, most likely much higher today[ii] The complete breakdown was as follows:

$10 million or less – 68%

$10 million to $50 million – 78%

$50 million to $500 million – 90%

$500 million to $1 billion – 89%

More than $1 billion – 92%

I believe any plan without an IPS is in fiduciary breach and they should be reviewed annually. [i].

by James W. Watkins, III, J.D., CFP Board Emeritus™ member, AWMA®

Recent developments in the 401(k) and 403(b) litigation arena suggest that a major change is coming to said landscapes, none more so than the amicus brief that the Department of Labor’s (DOL) recently filed with the 11th Circuit in connection with Pizarro v. Home Depot, Inc. (Home Depot).

But first, a little background. First, in Hughes v. Northwestern University1, SCOTUS upheld the provisions of ERISA Section 404(a) by ruling that each individual investment option within a plan must be legally prudent. Then, in Forman v. TriHealth, Inc.2, the Sixth Circuit suggested that dismissal of 401(k) actions based on the alleged cost of discovery to plans is premature and inequitable, Chief Judge Sutton stating that

“This wait-and-see approach also makes sense given that discovery holds the promise of sharpening this process-based inquiry. Maybe TriHealth “investigated its alternatives and made a considered decision to offer retail shares rather than institutional shares” because “the excess cost of the retail shares paid for the recordkeeping fees under [TriHealth’s] revenue-sharing model….” Or maybe these considerations never entered the decision-making process. In the absence of discovery or some other explanation that would make an inference of imprudence implausible, we cannot dismiss the case on this ground. Nor is this an area in which the runaway costs of discovery necessarily cloud the picture. An attentive district court judge ought to be able to keep discovery within reasonable bounds given that the inquiry is narrow and ought to be readily answerable.”3

“The fact that other courts have not suggested the use of “controlled” discovery has always interested me, it that is seems perfect for 401(k)/403(b) litigation. In controlled discovery, the plaintiffs would submit all discovery requests to the court for approval. As Judge Sutton suggested, since the only discovery that would be needed at this preliminary stage would be regarding whether the plan complied with the legal independent and objective investigation and evaluation requirement, the discovery request could be as simple as “any and all materials relied upon by the plan sponsor in determining that each investment option with the plan was legally prudent, including, but limited to reports, analyses, third-party research and analyses, notes, advertisements, articles, books, magazines and other publications.”4

The DOL Amicus Brief On February 10, 2023, the DOL filed an amicus brief (DOL brief) with the 11th Circuit in connection with the Home Depot case. I believe that the DOL’s amicus brief may be instrumental in finally creating a universal and equitable application of the ERISA in the legal system.

As a fiduciary risk management counsel, I am actually more interested in the macro aspects of the amicus brief since it would have a much broader national application. For that reason, I am not going to get into the specifics of the Home Depot case. The amicus brief gave a brief analysis of the issues involved in the case. The brief identified the question before the 11th Circuit:

“Whether, in an action for fiduciary breach under 29 U.S.C. § 1109(a), once the plaintiff establishes a breach and a related plan loss, the burden shifts to the fiduciary to prove the loss is not attributable to the fiduciary’s breach.”

The brief then addressed the issues with the district court’s ruling and the issues that the 11th Circuit should consider.

“The district court did not grapple with whether to import trust law’s burden shifting rule because it erroneously that this Court in Willett had already decided that plaintiffs exclusively bear the loss-causation burden in ERISA cases. But Willett did not even consider burden shifting, let alone reject it. If anything, Eleventh Circuit precedent—including Willett itself—supports applying trust law’s burden shifting rule to ERISA fiduciary breach cases.”5

“While Willett did not explicitly address burden shifting, other Eleventh Circuit cases have endorsed the rationale behind it. This Court has long acknowledged that ERISA “embod[ies] a tailored law of trusts” and has cautioned that courts should engage in a thorough analysis before determining that a “prominent feature of trust law” does not apply where ERISA is silent. Useden, 947 F.2d at 1580, 1581 (recognizing the “incorporation of procedural trust law principles” in ERISA). To determine whether a rule should be incorporated into ERISA’s common law, the Eleventh Circuit instructs that “courts must examine whether the rule, if adopted, would further ERISA’s scheme and goals.” 6

“Moreover, by adopting burden shifting, this Court would promote uniformity in the governance of ERISA plans by aligning with its sister circuits that already apply a burden-shifting framework for proving loss causation in ERISA fiduciary breach cases.”7

As I said, I believe that the DOL’s amicus has a far greater implications for 401(k)/403(b) litigation. The DOL’s amicus brief essentially adopted the earlier argument of both the 1st Circuit Court of Appeals in their Brotherston decision, and the Solicitor General in its amicus brief to SCOTUS. All three noted that trust law supports the idea that in cases involving a fiduciary relationship, the general rule that a plaintiff must prove all part of its cases, is replaced by shifting the burden of proof as to causation to the fiduciary/plan sponsor.

“As the Supreme Court and this Court have recognized, where ERISA is silent, principles of trust law—from which ERISA is derived—should guide the development of federal common law under ERISA. Trust law provides that once a beneficiary establishes a fiduciary breach and a related loss, the burden on causation shifts to the fiduciary to show that the loss was not caused by the breach. That is why five circuits have held that once an ERISA plaintiff proves a fiduciary breach and a related loss to the plan, the burden shifts to the fiduciary to prove the loss would have occurred even if it had acted prudently.”8

“When a statute is silent on how to assign the burden of proof, the “default rule” in civil litigation is that “plaintiffs bear the burden of persuasion regarding the essential aspects of their claims.” But “[t]he ordinary default rule, of course, admits of exceptions.” Id. One such exception is found in the common law of trusts, from which ERISA’s fiduciary standards derive. Tibble v. Edison Int’l, 575 U.S. 523, 528 (2015). Trust law provides that “when a beneficiary has succeeded in proving that the trustee has committed a breach of trust and that a related loss has occurred, the burden shifts to the trustee to prove that the loss would have occurred in the absence of the breach.”9 (citing Restatement (Third) of Trusts § 100 cmt. f}.

“As Judge Friendly explained, ‘Courts do not take kindly to arguments by fiduciaries who have breached their obligations that, if they had not done this, everything would have been the same.’”10

“This burden-shifting framework reflects the trust law principle that “as between innocent beneficiaries and a defaulting fiduciary, the latter should bear the risk of uncertainty as to the consequences of its breach of duty.” Trust law requires breaching fiduciaries to bear the risk of proving loss causation because fiduciaries often possess superior knowledge to plan participants and beneficiaries as to how their plans are run.”11 (citing Restatement (Third) of Trusts § 100 cmt. f.)

Citing Brotherston, the amicus brief notes that

“Given that an ‘ERISA fiduciary often . . . has available many options from which to build a portfolio of investments available to beneficiaries,’ the First Circuit reasoned that ‘it makes little sense to have the plaintiff hazard a guess as to what the fiduciary would have done had it not breached its duty in selecting investment vehicles, only to be told ‘guess again.”” The court thus held that “once an ERISA plaintiff has shown a breach of fiduciary duty and loss to the plan, the burden shifts to the fiduciary to prove that such loss was not caused by its breach.'”12

“[T]rust law’s burden-shifting rule ‘comports with the structure and purpose of ERISA,’ which is “to protect ‘the interests of participants in employee benefit plans and their beneficiaries.’ To require that the plaintiff—who has already proven a breach and a related loss—also prove that the loss would not have occurred absent the breach ‘would provide an unfair advantage to a defendant who has already been shown to have engaged in wrongful conduct, minimizing the fiduciary provisions’ deterrent effect.’”13

The amicus brief went on to address the general position of federal circuit court jurisdictions with regard to shifting the burden of proof on causation in ERISA actions.

“The First, Second, Fourth, Fifth, and Eighth Circuits unequivocally hold that, once a plaintiff has proven a breach of fiduciary duty and a related loss to the plan, the burden shifts to the fiduciary to prove that the loss was not caused by the breach.14

Going Forward As I said earlier, I believe the DOL’s amicus brief has the potential to have a significant impact in 401(k) and 403(b) litigation, especially when combined with the Northwestern and TriHealth factors. While I see numerous issues that plan sponsors will need to consider, I believe that three key issues that will need to be considered are selection of and reliance on third-party consultants, reconsideration of fiduciary disclaimer clauses, and inclusion of annuities in pension plans, in any form.

While the district court cited the 6th, 9th and 10th circuits in support of not shifting the burden of proof as to causation, the DOL pointed out that in the cases cited by the district court, “the Sixth and Ninth Circuit cases did not directly address loss causation at all.”15 As for the 10th Circuit’s refusal to adopt shifting the burden of proof on causation, the DOL pointed out that the 10th Circuit’s position was purportedly based on the 11th Circuit’s misinterpretation of of its own decision in Willett.16

1. Selection and Reliance on Third-Party Consultants It continues to amaze me that plan sponsors blindly rely on the advice of mutual funds and insurance agents rather than experienced ERISA attorneys. Despite the warnings of the courts that such practices are in clear violation of ERISA, the courts have warned plan sponsors that such practices are impractical.

“A determination whether a fiduciary’s reliance on an expert advisor is justified is informed by many factors, including the expert’s reputation and experience, the extensiveness and thoroughness of the expert’s investigation, whether the expert’s opinion is supported by relevant material, and whether the expert’s methods and assumptions are appropriate to the decision at hand. One extremely important factor is whether the expert advisor truly offers independent and impartial advice.”17

“[The plan sponsor] relied on FPA, however, and FPA served as a broker, not an impartial analyst. As a broker, FPA and its employees have an incentive to close deals, not to investigate which of several policies might serve the union best. A business in FPA’s position must consider both what plan it can convince the union to accept and the size of the potential commission associated with each alternative. FPA is not an objective analyst any more than the same real estate broker can simultaneously protect the interests of “can simultaneously protect the interests of both buyer and seller or the same attorney can represent both husband and wife in a divorce.”18

Whether voluntarily or as a result of a decision by SCOTUS, I believe that there is little doubt that the Restatement’s position on the shifting of the burden of proof as to causation will become the universal rule in ERISA actions.

2. Reconsideration of Fiduciary Disclaimer Clauses They have never made sense from a fiduciary liability standpoint. They make even less sense now with the consensus position of the DOL, the 1st Circuit Court of Appeals, and the Solicitor General on the shifting of the burden of proof as to causation.

As I have explained to plan sponsors, trustees and my other fiduciary risk management clients, this is basic argument an ERISA should make in claiming that granting a plan adviser a fiduciary disclaimer clause is in itself a breach of one’s fiduciary duties.

So, you hired a plan adviser because you did not feel confident in your ability to properly evaluate the prudence of investment options for the plan; yet you agreed to provide the plan adviser with a fiduciary disclaimer clause, arguably releasing the plan provider from any liability for providing poor investment advice and harming the plan participants, resulting in the selection and evaluation being right back in your hands, and in so doing, essentially acknowledged your negligence and a breach of your fiduciary duties.

As I tell my clients, if a plan adviser feels the need to request a fiduciary disclaimer clause, in essence telling you they have no confidence in the quality of their advice, should that not raise a huge red flag for plan sponsors? Don’t go there!

3. Inclusion of Annuities in Pension Plans “Guaranteed income for life” But as my late friend, insurance adviser Peter Katt, used to say, “at what cost?”

Annuity advocates refuse to acknowledge the inherent fiduciary liability issues with annuities. With SECURE and SECURE 2.0, visions of sugarplums danced in the heads of every annuity advocate.

Annuity advocates like to try to ignore the potential fiduciary liability issues by discussing all the various “bells and whistles” that annuities offer. And I used to engage in such nonsense, forgetting the sound advice to “never argue with someone who believes their own lies.”

Even before the DOL’s amicus brief, I warned my clients that annuities were a fiduciary trap. Smart plan sponsors do not voluntarily assume unnecessary fiduciary liability exposure.

I tell my clients that whenever considering potential investment options for a pension plan or a trust, use this simple two question test:

1. Does ERISA or any other law expressly require you to include the specific investment in the plan/trust? 2. Would/Could the inclusion of the investment potentially expose you and the plan/trust to unnecessary fiduciary liability exposure?

I have been receiving calls and emails telling me that some annuity agents have been telling plan sponsors that SECURE and/or SECURE 2.0 require them to include annuities in their plans. Simply not true. I have told my clients to actually recite the two question test to any annuity agent. FYI – with regard to annuities, the answers are “no” to question number one, and “yes” to question number two.

Plan participants that want to invest in an annuity are obviously free to do so – outside the plan where there would be no potential fiduciary liability issues for a plan sponsor.

Many plan sponsors unnecessarily expose themselves to fiduciary liability exposure because they do not truly understand their fiduciary duties under ERISA. ERISA does not require a plan sponsor to offer a specific investment simply because a plan participant would like to invest in the product. Again, they are free to open a personal account outside the plan and invest in any product they are interested in.

I predict significant changes in ERISA litigation over the next two years, as SCOTUS is called on to resolve the two remaining primary issues blocking a unified standard for determining 401(k)/403(b) litigation-the ‘apples and oranges” argument and the shifting the burden of proof on causation. The 1st Circuit, the Solicitor General and the DOL have already properly decided the issues. Now all that is left is for SCOTUS to officially endorse their arguments in order to guarantee plan participants the rights and protections promised them by ERISA.

Copyright InvestSense, LLC 2023. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.

The CFA Institute Pension Trustee Code of Conduct (Code) sets the standard for ethical behavior for a pension plan’s governing body. [i] It is a global standard that applies to both defined benefit (DB) and defined contribution (DC)plans, but I believe is consistent with ERISA fiduciary standards for 401(k) plans. The Code has 10 fundamental principles of ethical best practices. I am going to focus on 5 of them, the areas where we see many plans falling short of the standards.

Principle # 2. Act with prudence and reasonable care. The point regarding seeking appropriate levels of diversification[ii] is typically followed with most larger plans; but, we do see a number of mid-size and smaller plans taking single entity credit and liquidity risk in annuities and other insurance products. [iii] A particular non-diversified insurance product, lifetime income, is trying to break into even the largest plans, but with little success. [iv]

Another point is that service providers and consultants be independent and free of conflicts of interest. [v][vi] Again, most larger plans hire independent providers, but we do see a number of mid-size and smaller plans hire dually registered consultants who not only are registered investment providers, but are also registered as brokers or insurance agents, with the ability to get a commission. [vii]

Principle #3. Act with skill, competence, and diligence. Ignorance of a situation or an improper course of action on matters for which the trustee is responsible or should at least be aware is a violation of this code. “Trustee” in this case refers to each individual on the 401(k) committee plus the plan as a whole. We have seen many 401(k) committee members lacking awareness of the investment details in options of the plan.

Specifically, this principle points out the need ror awareness of how investments and securities are traded, their liquidity, and any other risks. Certain types of investments, such as hedge funds, private equity, or more sophisticated derivative instruments, necessitate more thorough investigation and understanding than do fundamental investments, such as straightforward and transparent equity, fixed-income, or mutual fund products. [viii]

With investments that have non-SEC regulated securities like illiquid contract-based products like crypto, [ix] private equity,[x] annuities and other insurance products, [xi] many times the 401(k) committees are not aware of the risks and hidden fees and have not thoroughly investigated them on such matters, especially those buried in target date funds and in brokerage windows.

Principle #5. Abide by all applicable laws Generally, trustees are not expected to master the nuances of technical, complex law or become experts in compliance with pension regulation. Effective trustees …consult with professional advisers retained by the plan to provide technical expertise on applicable law and regulation. [xii]

Principle #3 suggests that assets that are not straightforward and transparent securities, such as crypto, private equity and annuities/insurance products contracts, require additional legal scrutiny. I would assume that no crypto product would pass a good fiduciary law audit. I would claim that it would be the fiduciary duty of the plan going into any private equity or annuity contract (separate account or general account) – to have a side letter in which the manager/or insurance company agrees to take.

1. ERISA Fiduciary duty

2 Provide liquidity if the investment experiences difficulty. With insurance products, this can be done with a downgrade clause, i.e., “in the event that the insurance company’s debt is downgraded below investment grade by any major rating agency, the plan will be returned its contract value in cash within 30 days.”

3. “Most Favored Nation Clause, guaranteeing that the manager /insurance company does not provide a lower fee or higher rate to any other plans

Ownership of underlying securities is key to a plan’s risk exposure, especially liquidity risk, and when complex instruments are involved, it is the duty of the plan committee to get competent legal advice on these investment contracts.

Principle #7. Take actions that are consistent with policies Effective trustees develop and implement comprehensive written investment policies that guide the investment decisions of the plan (the “policies”). Most of the largest plans have Investment Policy Statements (IPS). The Code expects any plan to have them.

I believe any plan without an IPS is in fiduciary breach. I believe many conflicted consultants, as discussed in Principle #2, recommend that plans do not draft an IPS since it would expose their own conflicts. Most of the riskier assets in Principles #3 and #5, like crypto, private equity and annuities, would not be allowed under a well written IPS due to the excessive risks and hidden fees involved.

Trustees should … draft written policies that include a discussion of risk tolerances, return objectives, liquidityrequirements, liabilities, tax considerations, and any legal, regulatory, or other unique circumstances. Review and approve the plan’s investment policiesas necessary, but at least annually, to ensure that the policies remain current.[xiii]Some plans may have an Investment Policy Statement (IPS), but do not regularly review it or apply it rigorously to their investments.

Select investment options within the context of the stated mandates or strategies and appropriate asset allocation. Establish policy frameworks within which to allocate risk for both asset allocation policy risk and active riskas well as frameworks within which to monitor performance of the asset allocation policies and the risk of the overall pension plan.[xiv]

While asset allocation is a major component of DB plans – US DC plans now have over 50% of their assets in asset allocated investments, primarily target date funds.[xv] In most plans, the target date funds are the Qualified Default Investment Alternative (QDIA), which makes it essential that each target date sleave be addressed in the Investment Policy Statement.

Principle #10. Communicate with participants in a transparent manner. While the DOL forces some fee disclosure on each plan investment, it is not complete with non-securities like crypto, private equity and annuities as standalone options[xvi], in brokerage windows or inside target date funds. [xvii]

Revenue sharing is a shady non-transparent way some plans make their own participants pay for administrative costs; it does not hold up under these CFA standards in my opinion. [xviii]

Given the similarity between ERISA’s fiduciary requirements and the CFA Institute Pension Trustee Code of Conduct, 401(k) plan sponsors could greatly mitigate their litigation risk by looking at the Code. Furthermore, it is just the prudent and the right thing to do as a fiduciary.

Chris Tobe, CFA, CAIA is the Chief Investment Officer with Hackett Robertson Tobe (HRT) a minority owned SEC registered investment advisor and recently was awarded the CFA certificate in ESG investing. At HRT Tobe is leading up the institutional investment consulting practice for both DB and DC Pension plans. He also does legal expert work on pension investment cases.

Past industry experience includes consulting stints at New England Pension Consultants (NEPC) and Fund Evaluation Group. Tobe served on investment committee of the Delta Tau Delta Foundation for over 20 years served as a Trustee and on the Investment Committee for the $13 billion Kentucky Retirement Systems from 2008-12. Chris has published articles on pension investing in the Financial Analysts Journal, Journal of Investment Consulting and Plan Sponsor Magazine. Chris has been quoted in numerous publications including Forbes, Bloomberg, Reuters, Pensions & Investments and the Wall Street Journal.

Chris earned an MBA in Finance and Accounting from Indiana University Bloomington and his undergraduate degree in Economics from Tulane University. He has the taught the MBA investment course at the University of Louisville and has served as President of the CFA Society of Louisville. As a public pension trustee in, he completed both the Program for Advanced Trustee Studies at Harvard Law School and the Fiduciary College at Stanford University.

At the end of each quarterly, I update the five and ten-year Active Management Value Ratio analyses for the non-index based mutual funds in the top ten funds in “Pensions & Investments” list of most commonly used mutual funds in U.S. defined contribution.

Given the recent performance of the markets, it should come as no surprise that the 5 and 10-Year AMVR analyses of the six most popular non-index mutual funds in U.S. defined contribution plans remain relatively unchanged.

Interesting to note that for both the 5 and 10-year period, only Vanguard PRIMECAP Admiral shares managed to qualify for an AMVR ranking.

Also interesting to note the importance of factoring in a fund’s risk-adjusted returns. On the 5-year AMVR analyses, factoring in risk-adjusted returns turned AF’s Washington Mutual Fund’s incremental return from (0.90) on nominal returns, to a positive 0.13. Admittedly, a small positive number, but still a significant change.

On the 10-year AMVR analyses slide, factoring in the fund’s risk-adjusted returns turned their incremental return from (0.57) (nominal) to 0.57 (risk-adjusted.) Likewise for Fidelity Contafund, where an incremental return of (0.79) (nominal) turned into a small, yet positive, 0.09.

Overall, the song remains the same, with the majority of actively managed funds being unable to overcome the combination of the weight of higher fees and cost and high r-squared/correlation of returns number to beat the index of comparable index funds

And so, we continue to see 401(k) actions alleging a breach of fiduciary duties by plan sponsors. Of note, we are seeing an increasing number of cases focusing on target date funds (TDFs). I expect to see more actions involving TDFs, as the AMVR provides compelling evidence of the imprudence of the active versions of such funds. I will post an updated analysis of the active and index versions of both the Fidelity Freedom and TIAA-CREF Lifestyle TDFs next week

Somehow some judges are buying this fallacy that participants get better recordkeeping by paying substantially more for it. They are accepting this myth without proof and are actually blocking the transparency which would expose this truth by denying discovery.

Low-Cost recordkeeper Employee Fiduciary says “There are few industries where the phrase “you get what you pay for” is less applicable than the 401(k) industry. That’s because equally competent 401(k) providers can charge dramatically different fees for comparable administration services and investments.[i] Employee Fiduciary comes out with an example weekly on huge savings in recordkeeping. [ii]

There are no material differences in quality of recordkeeping services Fidelity at $30 a head is same service as Fidelity at $90 a head. There are really no material differences that a participant can tell between any recordkeepers, they get statements and have access to a web site. –

Smug articles gloat on how courts have blocked transparency of discovery for so called differences in record keeping quality that no participants or anyone in the industry can even measure. [iii] As attorney James Watkins says “Requiring a plaintiff to plead specific information known only to the defendant, without an opportunity to discover such specifics, is obviously just an attempt to protect plans.”

In this absurd insult to justice and transparency, some judges are putting the initial burden of proof on participants where the plan is deliberately hiding the critical information needed to fulfill that burden.

In addition, revenue sharing is an another way to help hide excessive recordkeeping fees, as some judges ignore these obvious issues. A 2021 study by experts from the Federal Reserve and leading universities says higher fees are not associated with better performance; to the contrary, “The future performance of revenue-sharing funds is weaker than that of non-sharing funds. The bulk of the under-performance is driven by higher fees, though revenue sharing funds display lower performance even after accounting for fees.”[iv]

Revenue sharing does not hold up during discovery and this has been confirmed by the fiduciary liability insurance industry, which put much higher litigation risk on plans with revenue sharing and either denying coverage or raising rates significantly. [v]

There are some instances of additional administrative services couched as education that can, in fact, be harmful to participants. Especially insurance providers, and especially in hospitals which are known to provide commissioned salespeople who actually try to push participants into higher fee funds and cross-sell them on imprudent outside investments as well.

Competitive recordkeeping costs have been established at $30 to $50 per heard for plans over $200 million in assets. There are no material differences in the quality of recordkeeping. Judges are dismissing fees double to such fees for identical services. The fact that such fees are largely ignored because they are non-transparent in no way reduces the significant harm they cause to participants.