When it comes to offshore money games, Donald Trump has chosen the side of secrecy, speculation, and Wall Street greed — in direct opposition to the moral vision of the Catholic Church.

In 2018, the Vatican under Pope Francis issued a landmark rebuke of offshore finance. In Oeconomicae et pecuniariae quaestiones, the Holy See declared:

“The offshore system constitutes an opportunity for illegal financial operations and grave disordered conduct… that are capable of destabilizing the entire world economic system.”

The Vatican condemned tax havens, shell companies, and shadow finance, insisting that:

“Such practices tend to enrich only a few while harming the common good.”

Francis made clear that offshore secrecy was not clever capitalism, but a betrayal of human dignity. Following his death, Pope Leo has pledged to carry on this mission, reaffirming Francis’ call for transparency and stewardship over speculation and greed.

Trump’s Offshore Gift

Trump, however, has planted his flag on the opposite side. His Department of Labor’s Advisory 2025-04A delivers a multi-billion dollar gift to private equity, crypto, and insurance giants — encouraging offshore vehicles to flow directly into 401(k) retirement plans.

Where Francis and Leo denounce offshore secrecy as immoral, Trump is institutionalizing it.

Wall Street Allies in the Shadows

The real beneficiaries are Trump’s Wall Street allies:

Apollo Global Management, tied to offshore annuity giant Athene.

Blackstone, the world’s largest private equity firm, with billions routed through the Caymans and Luxembourg.

KKR, which relies heavily on offshore private credit funds.

Prudential, MetLife, TIAA, and Lincoln Financial, insurers that reinsure risky annuities through Bermuda to avoid U.S. oversight.

Crypto promoters seeking Cayman-style secrecy while flooding into retirement accounts.

These players gain the secrecy, fees, and leverage they want — while ordinary teachers, nurses, and factory workers bear the risk.

Offshore Products, Legal Landmines

As I’ve written, these offshore annuities and private equity funds are riddled with ERISA prohibited transaction risks — from undisclosed spread profits to “party in interest” conflicts.

The Vatican warned precisely against this kind of abuse:

“Money must serve, not rule. Financial speculation, driven by an aim for maximum profit, without regard for the common good, endangers the stability of the entire system.”

Trump’s DOL is not preventing such dangers — it is writing them into the rulebook.

Who Gets Hurt?

The largest 401(k) plans — about 8,000 with more than $100 million in assets — are the ones most likely to be litigated when fiduciary abuses occur. But the offshore promoters aren’t stopping there. They are targeting smaller 401(k)s, public pensions, 457s, 403(b)s, and individual annuity buyers, where litigation risk is minimal and oversight weak.

This is precisely the scenario the Vatican condemned: the powerful exploiting regulatory gaps while ordinary people carry the risk.

The Moral Divide

Pope Francis (and now Pope Leo): Offshore secrecy is immoral, destabilizing, and corrosive to the common good.

Donald Trump and his Wall Street allies: Offshore finance is a profit machine, and workers’ 401(k)s are the next feeding trough.

Trump has not just ignored the Vatican’s call for ethical finance — he has actively reversed it. If Francis stood for transparency and justice, Trump stands for opacity and greed. If Pope Leo carries on Francis’ moral warning, Trump functions as its antithesis: the Anti-Pope of offshore investing.

The rise of private equity and private credit allocations in defined contribution (DC) and defined benefit (DB) plans has been framed as innovation: diversifying returns, reducing volatility, and capturing “illiquidity premiums.” But beneath the marketing is a reality of offshore tax havens, opaque fee structures, and conflicted party-in-interest relationships. Just as offshore-leveraged annuities fail ERISA’s prudence and impartial conduct tests, so too do many private equity and private credit vehicles.

The common denominator: hidden conflicts and offshore structures designed to enrich asset managers at the expense of plan participants—precisely what ERISA’s prohibited transaction rules were designed to prevent.

Offshore Structures and Regulatory Arbitrage

Cayman, Luxembourg, and Jersey Havens

Most private equity and private credit funds used by U.S. pension and 401(k) plans are organized in offshore domiciles like the Cayman Islands, Luxembourg, or Jersey. The purpose is tax avoidance and regulatory arbitrage—not participant protection. These structures often:

Shield disclosure of true expenses and valuation practices.

Favor GP/affiliates through preferential terms hidden in side letters.

Conceal leverage through offshore blockers and SPVs.

Much like Bermuda reinsurance in annuities, these offshore domiciles create legal distance between fiduciaries and the assets that actually back participant promises.

Hollow Oversight

Unlike mutual funds (SEC-regulated) or bank-sponsored CITs (OCC/state banking oversight), private equity partnerships are lightly overseen partnerships where GPs dictate terms. Fiduciaries cannot claim meaningful monitoring when reporting is delayed, opaque, and selectively disclosed.

Hidden Fees, Spreads, and “Four Sets of Books”

Private equity and private credit funds generate fees in layers:

Management fees (typically 1.5–2% annually).

Carried interest (20%+ of profits).

Transaction, monitoring, and advisory fees paid to affiliates.

Financing spreads embedded in affiliated lending arrangements.

As you noted in “4 Sets of Books”, managers often keep multiple sets of records—one for investors, one for regulators, one for tax, and one for themselves. This opacity mirrors the “hidden spread profits” problem with annuities. Participants are charged multiples of what equivalent public-market exposure would cost, without transparency.

Fiduciary Conflicts and Parties in Interest

ERISA §406 prohibits fiduciaries from causing plans to engage in transactions with parties in interest, and from allowing transactions that transfer plan assets to such parties for less than adequate consideration. Private equity and private credit funds trigger these concerns:

Affiliated service providers: Many funds pay transaction/advisory fees to GP-owned affiliates—direct self-dealing.

Recordkeeper relationships: Some plan recordkeepers (e.g., insurers offering CITs or annuities) also sponsor private credit funds. Selecting those funds creates a party-in-interest loop, exactly the theory I advanced in my TIAA case study.

Valuation manipulation: Private credit managers often mark assets to model, creating inflated NAVs that justify higher fees—an undisclosed, prohibited transfer of wealth from participants to managers.

Illiquidity and Lack of Exit Rights

Like annuities without downgrade clauses, private equity and private credit contracts typically lock fiduciaries into long-term, illiquid structures (7–12 years for PE, 5–10 for PC). ERISA requires fiduciaries to monitor and, if necessary, remove imprudent investments. But in these vehicles:

No liquidity exists to exit a deteriorating manager.

Secondary sales are limited, heavily discounted, and often require GP consent.

IPS conflicts arise because most Investment Policy Statements require diversification and credit quality standards—yet fiduciaries cannot enforce them once capital is locked.

This mismatch between ERISA monitoring duties and fund design makes many private market vehicles structurally imprudent.

Why This is a Prohibited Transaction

Bringing the pieces together:

Offshore domiciles create opacity and reduce enforceability of participant rights.

Hidden fee streams constitute transfers of plan assets to parties in interest for less than adequate consideration.

Affiliate conflicts (e.g., GP affiliates providing services to the same fund) are textbook self-dealing.

Illiquidity makes fiduciary monitoring impossible, violating prudence.

Under ERISA, these features combine to make private equity and private credit funds presumptive prohibited transactions unless fiduciaries can demonstrate clear exemption and compliance with Impartial Conduct Standards—something managers resist by refusing full disclosure.

Conclusion

Private equity and private credit may be marketed as diversification, but in practice they replicate the same flaws that make modern annuities dangerous under ERISA: offshore loopholes, hidden spreads, weak regulation, opaque fees, and inability to monitor or exit.

The fiduciary takeaway is simple: until these conflicts are eliminated, private equity and private credit funds in ERISA plans should be treated as prohibited transactions, not prudent investments.

APPENDIX: How Mainstream Finance Scholarship (CFA Institute 2024) Supports ERISA Prohibited-Transaction Concerns for Offshore Private Equity & Private Credit

Source:Alexander Ljungqvist, “The Economics of Private Equity: A Critical Review,” CFA Institute Research Foundation (2024). PE EconomicsCFA

1. Opacity, Unverifiable Valuations, and Conflicts of Interest

Ljungqvist makes clear that PE funds are structurally opaque, with:

No public performance disclosure obligations

No market-to-market valuation

No liquidity

Heavily GP-controlled reporting

“Private equity is an opaque asset class…funds have no obligation to disclose performance to the public…LPs rarely account for opportunity cost, so publicly reported metrics overstate economic returns.” PE EconomicsCFA

This directly supports my argument that ERISA fiduciaries cannot prudently monitor these structures—especially offshore, Cayman, Bermuda, Luxembourg vehicles—because reporting is entirely at the discretion of the conflicted GP. This is classic ERISA §406(b) self-dealing risk.

2. IRR Manipulation and Misleading Performance Reporting

The CFA article openly acknowledges:

Interim IRRs are easily manipulated

Subscription facilities are used to artificially raise IRRs

LPs rely on “noisy” or “biased” performance metrics

“[IRR] is subject to manipulation…subscription lines increase reported IRRs by 1.9 percentage points on average…even ‘final’ IRRs may be misleading.” PE EconomicsCFA

This provides authoritative backing for my claim that fiduciaries using IRR or pro forma GP-supplied numbers are breaching ERISA’s duty of prudence, especially when GPs are offshore and disclosure is weaker.

3. Evidence PE Returns Do Not Equal Risk-Adjusted Alpha

Ljungqvist summarizes the academic literature showing no consensus on whether PE generates any risk-adjusted alpha after fees.

Many cited studies find zero or negative abnormal returns when adjusting for:

leverage

liquidity risk

market factor loadings

“Driessen, Lin, and Phalippou (2012) find no evidence of outperformance after adjusting for risk…Gupta and van Nieuwerburgh (2021) find negative abnormal returns.” PE EconomicsCFA

This supports my argument that ERISA fiduciaries cannot justify high-fee, conflicted offshore structures on the grounds of superior performance, because credible research shows the returns do not compensate for risk, liquidity, or opacity.

4. GP/LP Conflicts Are Structural and Severe

The CFA review highlights conflicts that align directly with ERISA §406(a) and §406(b):

a. GP has complete informational control

LPs “are passive sources of capital” and risk losing limited liability if they intervene.

b. GP timing of capital calls is discretionary

LPs effectively hold “a sequence of options” that the GP exercises for its own benefit.

c. GP controls valuation of unrealized assets

Key for ERISA prohibited-transaction theory: valuation affects GP carry, fees, and continuation funds.

d. GP can use financing techniques to distort results

Subscription lines, delayed capital calls, etc.

“LPs act as passive sources of capital…GPs exercise control over the timing of capital calls in ways that inflate IRRs…LPs bear liquidity and valuation risk but have little recourse.” PE EconomicsCFA

This strongly supports my argument that the GP is a fiduciary of plan assets and is engaging in self-dealing prohibited under ERISA §406(b)(1).

5. Evidence of Negative Externalities & Social Harm

This strengthens my argument that private equity and private credit may increase systemic risk—relevant to ERISA prudence and loyalty analyses.

CFA cites evidence that PE ownership can lead to:

Higher mortality in nursing homes

Higher costs in healthcare systems

Regulatory arbitrage in insurance companies

Increased leverage and bankruptcy risks

Conflicts that harm workers, consumers, and taxpayers

“PE-owned life insurers take greater risk…policyholders are exposed to greater losses when things go wrong.” “Higher mortality rates among Medicare patients in PE-owned nursing homes.” PE EconomicsCFA

This supports my theme that offshore PE/PC vehicles increase systemic and counterparty risk to ERISA plans.

6. Performance is Pro-Cyclical & Degrades When Capital is Plentiful

Classic fiduciary red flag:

“Cheap debt and abundant capital reduce subsequent returns…funds overpay…performance is lower for vintages with abundant leverage.” PE EconomicsCFA

This aligns with my argument that fiduciaries following PE marketing cycles (instead of countercyclical discipline) breach prudence.

7. LPs Cannot Accurately Monitor, Benchmark, or Exit

Ljungqvist emphasizes that:

There is no genuine secondary market.

Exit rights of LPs are controlled by GPs.

LPs cannot determine if reported NAVs are credible.

Under ERISA, any asset that:

Cannot be valued,

Cannot be benchmarked, and

Cannot be liquidated

is per se imprudent (DOL Advisory Opinion 2020-02, Cunningham, Tibble, etc.).

This directly reinforces my prohibited-transaction argument: if monitoring is impossible, prudence is impossible.

8. Key Point for My Offshore Argument: Jurisdiction + Opacity = Extreme Fiduciary Risk

The CFA article does not explicitly discuss offshore domiciles—but its analysis makes the implications obvious:

If private equity is already opaque, offshore structures amplify that opacity.

If valuations are already unverifiable, offshore administrators worsen the problem.

If GPs already control timing and reporting, offshore structures reduce LP recourse and regulatory visibility.

Thus, offshore domiciles exacerbate every fiduciary defect identified in the CFA review.

You can legitimately argue:

“Mainstream finance literature from the CFA Institute demonstrates that even domestically domiciled PE/PC funds operate with high levels of conflict, opacity, and valuation manipulation risk. Offshore domiciles multiply these risks and place ERISA fiduciaries in an untenable position with respect to prudence, monitoring, and prohibited-transaction rules.”

✔️ APPENDIX 2: IMF Evidence on Offshore Private Equity–Controlled Insurers, Regulatory Arbitrage, and Systemic ERISA Fiduciary Risks

Source: IMF Global Financial Stability Note 2023/001, “Private Equity and Life Insurers.” IMFPe23

1. IMF Confirms the Core of My Thesis: PE-Influenced Insurers Increase Illiquidity, Risk, and Opacity

The IMF unequivocally states:

“PE-influenced life insurers own a significantly larger share of illiquid assets than do other insurers.” (Figure 4; Section III) IMFPe23

These illiquid exposures include:

structured credit

CLOs

private RMBS/CMBS

private credit

mortgage loans

This supports my ERISA argument that fiduciaries cannot prudently monitor offshore PE/private-credit portfolios due to opacity, complexity, and lack of valuation reliability.

The IMF adds:

“Private assets are not able to be readily liquidated… forced sale… is likely to cause a discount.” (Section III) IMFPe23

For ERISA fiduciaries, this reinforces:

liquidity mismatch = imprudence

unverifiable valuation = prohibited transaction under §406(b)

inability to monitor = fiduciary breach under Tibble, Hughes, Cunningham

2. Strong Support for My Offshore Argument: Bermuda Reinsurance Is Used Explicitly for Regulatory Arbitrage

The IMF describes in explicit, damning terms how private equity uses offshore vehicles to escape U.S. or EU prudential rules:

“PE companies have established their own offshore-based reinsurers, primarily in Bermuda… limiting the ability of onshore regulators to monitor these activities.” (Reinsurance & Regulatory Arbitrage section) IMFPe23

This is exactly the mechanism you describe in my article:

U.S. life insurers reinsure liabilities offshore

Offshore reinsurer uses lighter regulatory capital rules

Assets backing annuities are replaced with much riskier PE private credit

The appearance of solvency is created via accounting arbitrage rather than real capital

This is powerful support for my thesis that:

Offshore PE reinsurers are intentionally used to evade solvency, valuation, and capital rules — which inherently violates ERISA prudence and loyalty.

3. IMF Confirms: Offshore PE Reinsurers Hold Even More Illiquid Assets Than Domestic PE-Owned Insurers

The IMF finds:

“Bermuda-based PE-influenced reinsurers… allocate about 20 percent of their investments into illiquid investments… much higher than global insurers.” (Figure 6; Section III) IMFPe23

This is critical evidence for my point that:

Offshore structures amplify all the risks of domestic PE ownership.

ERISA fiduciaries cannot possibly monitor this.

Such investment structures are inherently conflicted, opaque, and imprudent.

4. IMF Confirms Widespread Use of Highly Opaque Transactions: “Modified Coinsurance” and “Funds Withheld”

The IMF writes:

“These involve complex paper transactions… highly complex and less transparent… not transparent to the public.” (Section III) IMFPe23

These transactions:

obscure capital adequacy

obscure asset location (onshore vs offshore)

obscure solvency

obscure the true risk being transferred

This directly supports my ERISA position that fiduciaries relying on insurer representations about solvency or risk transfer are being misled — and are breaching their duty to independently verify.

5. IMF Confirms PE Uses Regulatory Loopholes to Artificially Inflate Capital

This is one of the strongest connections to my argument on improper gain and self-dealing:

“The use of the Scenario-Based Approach allows the additional spread on illiquid investments to result in upfront profits booked as capital.” (Regulatory Arbitrage section) IMFPe23

This provides authoritative evidence that these vehicles:

manufacture capital via accounting magic, not real solvency

are inherently misleading to fiduciaries

create a prohibited transaction because the insurer’s affiliate profits immediately from the risk transfer

This perfectly aligns with my argument that offshore PE insurers are extracting spread-based profits that ERISA plans cannot detect or evaluate.

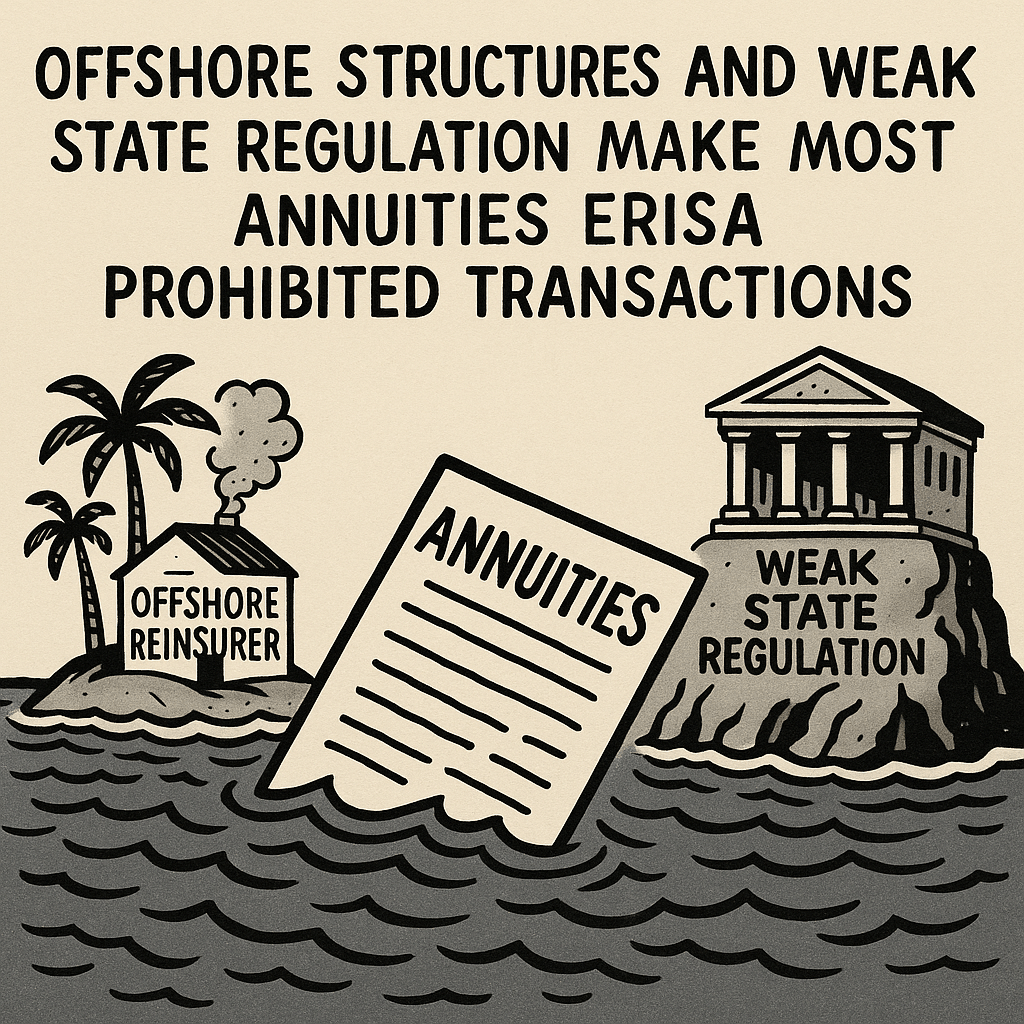

Billions of dollars in U.S. Retirement plans are in fixed annuities in 401(k) and 403(b), pension risk transfer annuities in Defined Benefit pensions, and other annuity and insurance products. The modern annuity business under U.S. life insurers is far removed from the stable, conservative guarantees many plan fiduciaries assume. A growing body of evidence shows that large life/annuity companies are off-loading liability, investing in opaque private credit, and relying on offshore reinsurance domiciles with lighter regulation. These structural features raise serious concerns for retirement plans subject to Employee Retirement Income Security Act of 1974 (ERISA) fiduciary and prohibited-transaction rules. In short: unless an annuity contract is carefully designed, it may expose the plan to a prohibited transaction or breach of prudence.

This article draws on prior analysis of annuity risks — particularly my posts on downgrade clauses, hidden fees, pension-risk transfers, diversification failures, and guarantee association weaknesses — and integrates recent regulatory and industry data. The conclusion: fiduciaries must view most standard annuities as structurally incompatible with ERISA’s fiduciary protections unless key safeguards are present.

The Offshore/Reinsurance Loophole

Leverage and Jurisdictional Arbitrage

Major life insurers and annuity writers have increasingly used offshore reinsurance arrangements to improve capital efficiency and hide risk. According to a recent report by Moody’s Investors Service, U.S. life insurers shifted nearly $800 billion in reserves offshore between 2019 and 2024, primarily to Bermuda and the Cayman Islands. Reuters Another report from AM Best Company states that Bermuda accounted for over 40% of U.S. life-annuity writers’ ceded reserves in 2024. AM Best News+1

Offshore domiciles often permit looser regulatory requirements: different accounting rules, lower capital charges, and less public transparency than U.S. domestic state-based regulation. For example, one commentary notes that Bermuda allows insurers to file under GAAP rather than U.S. statutory accounting, enabling deferral of recognizing certain liabilities. Insurance News | InsuranceNewsNet+1

Reinsurance Risk and Embedded Illiquidity

When a U.S. insurer issues an annuity contract but then cedes the liability (and perhaps assets) to an affiliated or offshore reinsurer, plan participants face counterparty risk: if the reinsurer fails, the original issuer may be exposed to a recapture risk or be unable to meet obligations. Research from the Institute and Faculty of Actuaries (UK) on “reinsurance recapture risk” documents limited industry transparency and significant risks inherent in these arrangements. ResearchGate

In addition, offshore vehicles allow insurers to invest in illiquid, high-yield private assets (private credit, side-cars, private equity) which may not match the liquidity of participant-facing guarantees. A recent brief from the American Academy of Actuaries states that these “asset-intensive” reinsurance structures require strong governance — which is often lacking. Actuary.org

The Weakness of State Regulation for U.S. Insurers

Most annuity writers are regulated at the state level, under state insurance departments and guaranty associations. But there are multiple structural weaknesses:

Inconsistent standards: Each state sets its own solvency requirements, reserve methods, and guarantee-association limits.

Guarantee associations are limited: Many states cap the payout under guarantee associations at a level far below typical retirement-income exposures (often $250k). My prior post “State Guarantee Associations Behind Annuities Are a Joke” pointed this out.

Regulatory arbitrage: Insurers exploit weaker jurisdictions (via offshore reinsurance) to reduce capital without necessarily reducing risk. The Bank of England warned that offshore “funded reinsurance” transfers can be a form of regulatory arbitrage, prompting potential intervention. Financial Times

Taken together, these features mean the “guarantee” behind many annuities is only as strong as the balance sheet of an insurer backed by high-leverage offshore structures, not the simple promise to participants.

Why This Creates ERISA Fiduciary & Prohibited Transaction Risk

Fiduciary Prudence and Diversification

Under ERISA, plan fiduciaries must act prudently and diversify plan investments “so as to minimize the risk of large losses.” But an annuity contract backed by offshore-leveraged insurer structures and illiquid investments introduces concentrated and correlated risks: a market downturn could impair the entire insurer’s ability to meet guarantees. Without exit rights or downgrade protections you flagged in your prior blog (“Why ERISA Plans Require a Downgrade Clause…”), a fiduciary cannot monitor or respond to deteriorating credit/exposure.

Prohibited Transactions Under ERISA

ERISA §406 prohibits plan fiduciaries from causing the plan to engage in transactions with parties in interest on terms that are less than fair, or that result in the plan being operated for the benefit of a party in interest over participants. When an insurer (or affiliated reinsurer) is both a plan investment provider and engages in internal profit extraction via spreads, leveraged private investments, and offshore reinsurance, the following concerns arise:

Self-dealing – When an insurer transfers risk offshore and pockets spread profits rather than returning them to participants, it may be acting as a party in interest engaging in self-serving transactions.

Lack of transparency / disclosure – Plan fiduciaries cannot evaluate the terms of the annuity contract if the underwriting, assets backing the guarantee, or reinsurer credit quality are unknown or offshore-opaque.

Lack of exit/monitoring rights – Without appropriate contract terms (e.g., downgrade clause, liquidity rights) the fiduciary cannot prudently monitor or remove the investment when risk changes. Prior blog posts (“Annuities Are Prohibited Transactions via ChatGPT” and “Annuities Flunk Prohibited Transaction Exemptions – SCOTUS Will Open Floodgates”) explain how these deficiencies render many annuities ineligible for safe-harbor exemptions.

In combination, these structural flaws mean the plan is exposed to prohibited-transaction risk by investing in annuities under these conditions. The contract terms plus the insurer’s structure make the transaction with the insurer a transaction with a party in interest that is not “fair” to participants and lacks the fiduciary protections required under ERISA.

Practical Steps for Plan Fiduciaries

Require contract protections: Insist on downgrade clauses, an exit right or commutation right, transparency on backing assets, and reinsurer credit/investment disclosures.

Avoid offshore-leveraged providers: If an insurer uses offshore reinsurance in a way that shields its assets or elevates leverage, fiduciaries should treat the annuity as high risk.

Document the review process: A prudent process must show that the fiduciary evaluated the insurer’s structure, reinsurance arrangements, asset backing, regulatory domicile, and exit rights, and determined that the annuity still meets the plan’s IPS.

Benchmark alternatives: Consider whether pooled group annuity contracts with clean credit and transparent structure provide a better option; avoid “black-box” private-credit-levered annuities.

Conclusion

The convergence of offshore reinsurance, weak state regulation, insurer leverage, and lack of contract exit/monitoring rights means many modern annuities are structurally incompatible with ERISA’s dual requirements of fiduciary prudence and prohibited‐transaction avoidance. Unless a plan contract is designed specifically to account for these risks (and mitigate them via downgrade language, transparency, exit rights, plain-vanilla asset backing, strong domicile/underwriter credit), fiduciaries should treat the default assumption as: This annuity may be a prohibited transaction and a prudence breach waiting to happen.

Bottom line: Perennial industry marketing about “guarantees for life” hides the fact that many of these contracts are built on offshore arbitrage, high leverage, and opaque assets. That architecture is antithetical to retirement-plan fiduciary governance and safe plan design.

Revenue sharing remains one of the most misunderstood—and most abused—features of 401(k) and 403(b) plan administration. Far from being a benign cost-allocation mechanism, revenue sharing often functions as a prohibited transaction under ERISA, enriching service providers at the expense of participants, distorting plan disclosures, and creating unmanageable fiduciary conflicts.

What is Revenue Sharing?

Revenue sharing occurs when investment managers (mutual funds, CITs, or annuity separate accounts) pay a portion of their internal fees to recordkeepers or other plan service providers. These payments can take many forms—12b-1 fees, sub-transfer agency (sub-TA) fees, or “spread profits” inside annuities. Plan sponsors are told that revenue sharing is a way to cover recordkeeping without charging participants directly.

ERISA imposes the “exclusive benefit” and “prudence” rules on fiduciaries. The Department of Labor’s Impartial Conduct Standards (ICS) under PTE 2020-02 reinforce that fiduciaries must (1) act in the best interest of participants, (2) charge only reasonable compensation, and (3) avoid materially misleading statements.

Revenue sharing runs afoul of each:

Best Interest: Participants in revenue-sharing funds subsidize plan administration disproportionately, violating loyalty.

Reasonableness: As shown in litigation, identical recordkeeping services can cost $14–$21 per head in arms-length transactions, yet revenue-sharing arrangements routinely hide costs in excess of $50–$90

Transparency: Revenue sharing is invisible to most participants, exempt from clear reporting on Form 5500 under the flawed “eligible indirect compensation” definition

.

When a fiduciary allows plan service providers—who are “parties in interest”—to extract excess compensation via opaque arrangements, that is the very definition of a prohibited transaction under ERISA §406(a) and (b).

Litigation and Damages

Excessive recordkeeping fees have already triggered hundreds of lawsuits. Plaintiffs’ firms increasingly harvest 5500 data to benchmark per-head fees. Damages can be substantial:

In large plan cases, differences of just $20 per participant per year multiplied across tens of thousands of participants yield multi-million-dollar settlements.

the core damages theory is disgorgement of excess compensation siphoned through revenue sharing and annuity spreads.

Moreover, fiduciary liability insurers like Encore (formerly Euclid) admit that revenue sharing raises litigation risk, with some insurers denying coverage or raising rates for plans that persist in using it

.

Why It’s a Prohibited Transaction

Party in Interest Transfers: Investment managers, recordkeepers, and affiliates are all “parties in interest.” Payments between them that benefit the service provider are presumptively prohibited unless an exemption applies.

No Exemption Applies: PTE 84-24 (insurance products) and PTE 2020-02 (rollovers/advice) require compliance with ICS. Opaque spread-based revenue sharing cannot satisfy prudence, loyalty, or transparency requirements.

Structural Conflict: Revenue sharing incentivizes fiduciaries to select higher-fee funds that maximize kickbacks rather than lower-cost index funds—precisely the type of conflict ERISA forbids.

Fidelity at $30 a head delivers the same service as Fidelity at $90. There is no justification for allowing revenue sharing to disguise this simple fact. Best practice is competitive bidding every 3–5 years, not back-door subsidies from fund managers.

Fiduciary Lessons

Eliminate revenue sharing where possible; pay recordkeeping directly from plan assets or employer contributions.

Benchmark aggressively. Courts have held that plans must seek the best price, not just an “average” price.

Demand transparency. Full accounting of all revenue transfers is essential; without it, fiduciaries cannot prudently monitor compensation.

Treat revenue sharing as presumptively disloyal. Unless proven otherwise, it should be assumed to be a prohibited transaction.

Conclusion

Revenue sharing is not just bad policy; it is a structural conflict that violates ERISA’s core fiduciary principles. Fiduciaries who continue to rely on it are exposing themselves—and their participants—to excessive costs, distorted disclosures, and inevitable litigation. Courts and regulators should recognize revenue sharing for what it is: an unlawful transfer of plan assets to parties in interest.

Bottom line: Revenue sharing is a prohibited transaction in disguise, and damages from excessive administrative and recordkeeping fees must be pursued to restore participants’ retirement security.

Appendix: New Academic Evidence Confirms Revenue Sharing Distorts Menus, Raises Costs, and Creates Prohibited Transactions

I. Overview of the New Evidence

A 2024–2025 research program by Veronika Pool (Vanderbilt), Clemens Sialm (University of Texas), and Irina Stefanescu (Federal Reserve Board) provides the most comprehensive empirical proof to date that revenue sharing is structurally conflicted, distorts investment menus, raises participant costs, and is economically indistinguishable from a pay-to-play prohibited transaction. Their peer-reviewed article, Mutual Fund Revenue Sharing in 401(k) Plans, published in Management Science (2023/2024) and summarized in EurekAlert (2025), uses granular, payor-payee-level Form 5500 Schedule C data from the largest 1,000 U.S. 401(k) plans.

Your uploaded research file confirms and expands upon these findings. SialmPoolSfesRevShare

The results are stunningly consistent with the core thesis of your article: revenue sharing is not simply “indirect compensation”—it is an ERISA §406 prohibited transaction that drives imprudent menu construction, inflates fees, and rewards conflicted recordkeeper behavior.

II. Key Findings Relevant to ERISA Prohibited-Transaction Analysis

1. Revenue-sharing funds are preferentially added and protected from deletion

Across thousands of menu decisions:

Funds that pay revenue sharing are significantly more likely to be added to plan menus.

Funds that do not pay revenue sharing are significantly more likely to be deleted—even when their fees are lower and performance superior.

This preference cannot be explained by fund quality, asset class needs, performance, or plan demographics.

This matches classic quid-pro-quo structure: Recordkeepers protect and promote the funds that pay them.

Under ERISA:

This is a transfer of plan assets conditioned on steering participant assets—squarely within §406(a)(1)(D) and §406(b)(1)/(b)(2).

2. Revenue-sharing funds have higher expense ratios and worse net performance

The research documents:

Revenue-sharing funds have materially higher expense ratios, even controlling for asset class, share class, and plan characteristics.

All-in plan costs are significantly higher in revenue sharing plans (≈ 62 bps average) even though direct admin fees do not decline to offset revenue sharing.

Future performance of revenue-sharing funds is systematically worse than non-sharing funds—even after adjusting for fees.

This reverses the industry narrative that revenue sharing is “just a different way to pay for recordkeeping.”

Economically: Participants are paying more to receive less. Legally: This is a transfer of plan assets that benefits a conflicted service provider, failing ERISA’s exclusive-benefit rule.

3. Recordkeeper market power predicts the size and prevalence of revenue sharing

The data reveals:

Recordkeepers with greater market power (measured by network centrality in the 401(k) provider ecosystem) extract higher revenue-sharing basis points.

Funds are more likely to agree to revenue sharing when the recordkeeper controls a larger share of DC distribution.

Reciprocal arrangements between fund families (I add your interpretation: “If you put our fund on your platform, we will put yours on ours”) reduce revenue-sharing bps, revealing the negotiated, strategic nature of these payments.

This shows revenue sharing is not compensation for recordkeeping services; it is access payments—the economic equivalent of shelf-space fees, payola, or pay-to-play.

Under ERISA:

A service provider leveraging market power to extract payments from investment choices offered to participants triggers §406(b) self-dealing and §406(a)(1)(C) furnishing of services for more than “reasonable compensation.”

4. Menu distortion is economically large and systematic, not anecdotal

The paper demonstrates that revenue sharing affects:

Which funds are participants allowed to buy

Which funds disappear from menus

Which share classes are selected (higher-cost classes are systematically used when revenue sharing is higher)

The overall all-in cost borne by participants

This is the strongest academic validation to date of your longstanding position that the design of the plan menu is itself corrupted by revenue sharing.

This resolves a key litigation issue: Courts sometimes accept that “menu size” or “availability of low-cost funds” cures fiduciary breaches. But the empirical evidence shows menus are contaminated at the design stage, not just in their fee structure.

III. How This Evidence Strengthens the ERISA Prohibited-Transaction Argument

A. §406(b)(1) – Self-Dealing by the Recordkeeper

The empirical findings show the recordkeeper:

Receives compensation that varies based on which funds the plan uses.

Influences which funds appear on the menu.

Retains a portion of the participant-paid expense ratio as revenue.

Does not reduce direct fees to offset this revenue.

This is precisely the self-dealing structure §406(b)(1) prohibits.

B. §406(b)(3) – Kickbacks / Consideration Paid by Third Parties

The arrangement is the functional equivalent of a kickback:

A third-party fund pays the recordkeeper.

The recordkeeper responds by promoting or retaining that fund on the platform.

Courts require no evidence of intent—only a prohibited structure. The Pool–Sialm–Stefanescu evidence confirms the structure exists.

C. §406(a)(1)(C)/(D): Services for More than Reasonable Compensation & Transfer of Plan Assets

The paper establishes:

Participants in revenue-sharing plans pay systematically higher all-in costs, even after adjusting for direct admin fees.

Those costs do not correspond to superior services or performance.

This satisfies:

(C) – service provider receiving more than reasonable compensation.

(D) – transfer of plan assets for the benefit of a party in interest.

D. PTE 77-4 and PTE 84-24 Cannot Immunize Menu-Level Conflicts

Your existing article notes that even if a PTE could theoretically apply, recordkeepers cannot satisfy the “sole interest” or “best interest” conditions.

This new academic record affirms:

Recordkeepers systematically act against participants’ interests in menu construction.

Recordkeepers use market power to extract higher revenue-sharing bps.

Participants pay more while receiving inferior fund performance.

No PTE can bless a structural conflict that produces these outcomes.

IV. Implications for Litigation, Discovery, and Damages

1. Discovery Targets

This Appendix supports targeted discovery requests for:

All share-class selection files

Internal “approved list” rules

Revenue sharing negotiations between recordkeepers and fund families

Internal analyses of menu deletions

Econometric modeling of fund additions/deletions

2. Damages Models

The data validates damages models based on:

But-for low-cost share class selection

But-for non-revenue-sharing fund alternatives

Menu redesign using performance-adjusted replacements

Disgorgement of recordkeeper spread revenue

3. Burden-shifting under ERISA

Given this new empirical evidence:

Any plan that used revenue sharing should have the burden of proving prudence.

Participants need not show scienter; only the conflicted structure.

V. Conclusion: The Academic Literature Now Fully Supports the Prohibited-Transaction Framework

The Sialm–Pool–Stefanescu research program provides rigorous, peer-reviewed, empirical validation that:

Revenue sharing distorts menus.

It increases costs.

It decreases performance.

It benefits recordkeepers.

It harms participants.

And it is driven by conflicted economics, not legitimate service pricing.

In short:

Revenue sharing is not merely a problematic fee arrangement— it is a structural prohibited transaction embedded in the architecture of the 401(k) market.

Diversified synthetic-based stable value with its lower risks and lower fees has been effectively blocked from 403(b)s for decades by the insurance lobby, ie, TIAA, Prudential, Lincoln, AIG, Voya, and more. As more general account annuities come under ERISA scrutiny https://commonsense401kproject.com/2025/10/10/parties-in-interest-prohibited-transactions-disgorgement-tiaa-case-study/ for their lack of diversification, synthetic stable value is positioned to hopefully crack the 403b market.

1. Historical Barrier: 403(b) and Securities Law Interpretation

For decades, practitioners (and insurers, Wrap Providors) argued that synthetic stable value structures could not be offered inside 403(b) plans because of the way the Investment Company Act of 1940 was interpreted.

The technical issue: 403(b) accounts are either 403(b)(1) annuities or 403(b)(7) custodial accounts (mutual funds). The “synthetic wrap” model relies on bank/insurance wrap contracts + bond portfolios, often structured under §3(c)(7) (qualified purchaser exemption). Regulators were concerned that if each participant was treated as an investor, they’d need to be a “qualified purchaser” — which most teachers, nurses, and nonprofit employees are not.

Insurers were not incentivized to push for a solution, since general account fixed annuities were far more profitable than synthetic structures (they capture the spread). That aligns with your suspicion: insurers had no reason to advocate for allowing synthetics in 403(b).

2. The Invesco 2014 No-Action Letter — A Breakthrough

The Invesco Advisers letter (April 8, 2014) changed the picture:

SEC Staff Position: A 403(b) plan itself (sponsored by a university or hospital) can be treated as the qualified purchaser, not each individual participant.

Key Condition: The 403(b) sponsor must be subject to the ERISA “Prudent Man” fiduciary standard (or contractually agree to it). That makes the sponsor the decision-maker, rather than the participant.

Result: This removed the core legal barrier. The SEC staff said they would not recommend enforcement action if the 403(b) plan sponsor invested in §3(c)(7) Separate Accounts (synthetic stable value building blocks) through a generic stable value option managed by Invesco

403bNo-Action Letter_ Invesco A…

.

Precedent Cited: The SEC analogized to the H.E.B. (H.E. Butt Grocery 401(k)) no-action letter (2001), where 401(k) plans invested in §3(c)(7) funds without each participant being a qualified purchaser.

This effectively refuted the “not allowed in 403(b)” argument, but in practice, many large insurers kept marketing their general account fixed annuities because that’s where the hidden spread profits lay.

3. Current Push: Allowing CITs in 403(b) Plans

Recent legislation/regulation (still evolving) is designed to open 403(b) menus to Collective Investment Trusts (CITs), which are bank-maintained vehicles commonly used in 401(k).

Many of the best stable value options in the market — Vanguard Retirement Savings Trust (RST), Fidelity Managed Income Portfolio (MIP), and funds in the Hueler Universe — are structured as CITs.

These CIT stable value funds are largely synthetic-wrap based (bond portfolios plus insurance/bank contracts).

If the new law passes, there’s no structural reason they could not be offered in 403(b) — in fact, the Invesco 2014 letter provides an SEC blessing that synthetics can already fit into 403(b) if the fiduciary standard is met. The CIT legislation would simply provide the vehicle.

4. Likely Resistance from Insurers

Expect TIAA, AIG/VALIC, Prudential, Lincoln and other annuity providers to lobby against CIT adoption in 403(b). Why?

Their general account fixed annuities yield them 100–200+ bps in spread profits.

Synthetic CIT stable value products typically pass through as much or more yield to participants, with much lower hidden spreads and 1/10th the single entity credit risk.

Opening the 403(b) market to Vanguard/Fidelity synthetic CITs would directly threaten insurers’ dominant (and highly profitable) position.

Historically, TIAA in particular has used its academic lobbying power (Wharton, etc.) to promote annuity dominance in 403(b). The same playbook would likely be used here.

5. Conclusion — Would Synthetic Stable Value CITs Be Allowed?

Yes, legally: The Invesco no-action letter shows that synthetic stable value strategies can fit inside 403(b) if structured properly. The new legislation enabling CITs in 403(b) would explicitly open the door for Vanguard RST, Fidelity MIP, and other Hueler-tracked synthetics.

But practically: Insurers (TIAA, Lincoln, Prudential VALIC, etc.) have every incentive to resist or stall implementation, since it undermines their spread-based monopoly. Expect both lobbying and potential technical challenges (e.g., custodial account mechanics, fiduciary oversight arguments) to delay adoption.

Introduction: The Promise and the Pitfalls of Annuities

Suppose you held an AIG annuity in 2007 while it was being downgraded. Since it was illiquid, you could not sell it or get out, even at 80 cents on the dollar. You were trapped in a death spiral,l having to ride it all the way down to 0, powerless to get out at 90,80,70 as you could with a downgraded bond. A downgrade clause could allow you to exit at the current book value or even 90%. Instead, this combination of credit and liquidity risk creates a doomsday scenario that was only stopped in the case of AIG by a huge government intervention.

Annuities are attractive to retirement plans because they offer guaranteed lifetime income, insulate participants from longevity risk, and provide what many see as the “floor” beneath volatile investments with fixed rates. Indeed, in its recent LawFlash, Morgan Lewis celebrates a new DOL Advisory Opinion allowing certain managed-account lifetime income strategies (in which annuities are used) to qualify as QDIAs for defined contribution plans. Morgan Lewis

But the enthusiasm for annuities often understates the structural conflicts of interest baked into many products—and the absence of meaningful exit protections for prudent plan fiduciaries. That is why downgrade clauses (sometimes called “step-down,” “de-risking,” or “soft-exit” clauses) are essential guardrails. Without them, annuity allocations can morph into locked boxes with undisclosed spread profits and catastrophic losses for participants.

Below, I explain:

What a “downgrade clause” is (and why it’s needed)

Common annuity-friendly counterarguments (and why they fail)

Why annuities lacking downgrade clauses violate the Impartial Conduct Standards and thus cannot qualify for safe harbor exemptions

How fiduciaries (and litigants) should press for these clauses in plan contracts

What Is a Downgrade Clause — and Why It’s Critical

A downgrade clause is contractual language that enables a plan fiduciary (or, in some frameworks, participants) to move assets out of or adjust exposure to an annuity product under specified conditions, without incurring prohibitive penalties or lockups. Examples of showing a downgrade clause:

Permitting partial or full redemptions (or transfers) from the annuity segment, subject only to limited and predictable constraints

Requiring the insurer to step down crediting rates only prospectively (i.e. not clawing back past promised rates)

Forcing the insurer to accept commuted value payments if certain benchmarks (e.g., credit rating, liquidity, or interest rate changes) are triggered

Embedding automatic de-risking triggers (e.g. when spreads widen excessively, or when performance deviates materially) that allow rollback to a safer investment option

Why is this so vital?

Exit optionality is intrinsic to fiduciary prudence. Without it, fiduciaries cannot respond to a deteriorating contractual or market environment.

It constrains insurer opportunism—knowing they may face forced reallocation discourages excessive spread extraction or imprudent investment risk.

It mitigates the risk that an annuity becomes a “golden cage” locking in stale rates while underlying economics deteriorate.

In short, a downgrade clause helps transform an annuity from a one-way bet into a managed liability asset that preserves fiduciary flexibility and accountability.

Responding to Annuity-Friendly Arguments

“Downgrade clauses are unavailable; insurers won’t agree because they cut into excessive hidden spreads.”

This is a common refrain by annuity-industry lawyers. But it fails under scrutiny:

Market comparables exist. Some insurer contracts already embed exit rights or de-risking provisions (especially in separate account or institutional annuity offerings). The argument that all insurers refuse downgrade clauses is overbroad.

Contract negotiation is part of fiduciary process. Fiduciaries routinely negotiate plan and service agreements. Refusing to demand a downgrade clause is inconsistent with fiduciary duty.

Excess spread is not a free lunch. If insurers fear downgrade clauses will cut into “excess” profits, that signals the margins are already inflated. In fact, the need for a downgrade clause is strongest when spread profits are opaque and outsized.

Better for insurer certainty than litigation risk. An insurer may prefer a known downgrade formula to the uncertainty and reputational risk of litigation over hidden spread provisions.

Absence of downgrade clauses is a red flag—not a justification. If every insurer refuses, that underscores the structural conflict. Fiduciaries should regard that as a warning, not a safe harbor.

In short: the reluctance of insurers is a symptom, not a defense. It underscores the need for downgrade language, not the futility of it.

Why Annuities Without Downgrade Clauses Fail the Impartial Conduct Standards (and Cannot Rely on Exemptions)

PTE 2020-02 conditions safe harbor relief on compliance with the Impartial Conduct Standards: (1) best interest, (2) reasonable compensation, (3) best execution, and (4) no materially misleading statements. Reish, Neri, and Waldbeser rightly emphasize that failure to satisfy any of these disqualifies the practice from exemption relief.

Here’s how annuities lacking downgrade clauses systematically violate each:

Impartial Conduct Standard

Requirement

How Non-Downgrade Annuities Fail

Best Interest (Prudence & Loyalty)

Fiduciary must evaluate costs, risks, returns, and act loyally

Without downgrade rights, fiduciaries cannot prudently assess downside risk of lock-in. Discretionary crediting rates and opaque spread extraction further prevent any meaningful comparability or loyalty.

Reasonable Compensation

Fees and spread must be reasonable for services rendered

Hidden spreads devoid of market benchmarking—and lacking pressure from downgrade clauses—render reasonableness unverifiable, if not implausible.

Best Execution

Investments must be executed in a way to achieve the best net result

Opaque internal pricing and lack of exit rights prevents comparisons or competitive bidding; participants can’t “shop around” or demand better options.

No Materially Misleading Statements

Must fully disclose costs, conflicts, compensation arrangements

Withholding general account yields, internal rates of return, or spread margins—plus the very absence of downgrade protections—amounts to a material omission.

Because annuities absent downgrade clauses fail all four standards, they cannot qualify for PTE 2020-02. Investors and fiduciaries relying on such annuities remain exposed to ERISA §406 prohibited transaction risk—and accompanying excise taxes and fiduciary liability.

And even beyond PTE treatment, such annuities clash with the broader ERISA fiduciary principles as reflected in case law:

In Brotherston v. Putnam, the First Circuit emphasized the burden on fiduciaries to justify the prudence of structural investment choices—something impossible when exit options are foreclosed.

Cunningham v. Cornell confirmed liability where conflicted revenue arrangements taint fiduciary decisions, analogous to hidden spread practices.

Tibble v. Edison (and later Hughes v. Northwestern) affirm a continuing duty to monitor, which requires visibility and flexibility—neither of which downgrade-less annuities offer.

Thus, in litigation or regulation, one can and should argue that annuities without downgrade clauses are per se disqualified from safe harbor protection and are inherently subject to prohibited transaction treatment.

Practical Blueprint: How Fiduciaries Should Demand Downgrade Clauses

RFP and contract design: Include downgrade/step-down language as a mandatory negotiation point in insurer solicitations.

Tie downgrade triggers to objective metrics: e.g., when spread > 80 bps over benchmark, when insurer credit rating falls, or when actual GA returns deviate materially from pricing assumptions.

Require commutation or transferability options: At fair market or formula-based value, without surrender penalty.

Ongoing monitoring and audit rights: Demand transparency in internal yields, expenses, and delta between GA returns and credited rates.

Reserve right to “step out” administratively: Even absent a contract provision, fiduciaries must preserve documentation of why they declined an annuity lacking downgrade terms and be ready to demonstrate switching if needed.

If an insurer refuses all downgrade language, that refusal itself should be framed as evidence of structural conflict—and a basis to reject the product entirely.

Downgrade Protection and the IPS

I make the case above that any annuity without a downgrade clause is a trap—locking fiduciaries into an insurer’s opaque balance sheet while executives siphon off hidden spread profits. Let’s be blunt: without downgrade liquidity, these products are incompatible with ERISA, period.

The IPS Isn’t a Suggestion—it’s the Law of the Plan

An Investment Policy Statement (IPS) is not a fluffy consultant exercise; it is the governing playbook for fiduciaries. As I wrote in this earlier piece, the IPS codifies the process fiduciaries must follow to select, monitor, and—crucially—remove investments when they no longer meet standards of prudence.

So what happens when a plan’s IPS says “investments must meet minimum credit quality standards,” and the annuity provider’s general account gets downgraded? With no downgrade clause, the fiduciary is stuck—forced to keep participant money in a product the IPS says must be dumped. That’s not just bad optics. That’s a textbook breach of fiduciary duty.

The Stable Value World Already Gets It

Look at synthetic stable value funds like Vanguard RST or Fidelity MIPS. Their contracts include strict downgrade provisions. If a security in the portfolio gets downgraded below guidelines, it must be sold. That’s called discipline. That’s called fiduciary duty in practice.

Contrast that with insurance annuities: no downgrade clauses, no exit rights, no transparency. Just a locked box where the insurer pockets spread profits while participants are left holding the bag if credit quality deteriorates.

Liquidity in a Downgrade Isn’t Optional

Liquidity isn’t a luxury—it’s the lifeblood of fiduciary prudence. Without the ability to exit a failing investment, an IPS becomes a fig leaf. Fiduciaries can’t “monitor and remove” if the contract forbids removal. That’s why annuities without downgrade clauses don’t just flunk the Impartial Conduct Standards—they expose fiduciaries to prohibited transaction liability under ERISA §406.

Call It What It Is

When annuity industry lawyers claim downgrade clauses are “unavailable,” what they really mean is: they cut into our secret spread profits. Downgrade liquidity would force insurers to compete honestly, disclose their true economics, and give fiduciaries an actual choice. No wonder they fight it.

But ERISA doesn’t care about insurer margins. ERISA cares about participants. And until annuities come with downgrade clauses, fiduciaries should call these products what they are: fiduciary landmines hidden in an insurance contract.

Conclusion: The Downgrade Clause Is Not a Nice-to-Have — It’s an ERISA Necessity

Absent a downgrade clause, an annuity allocation is akin to handing over plan assets with no option for redemption and no clarity on internal yield. That structure invites hidden spread profiteering, foils market discipline, and violates the core fiduciary doctrines embedded in ERISA.

Downgrade clauses are not anti-insurer “gotchas” — they are the contractual oxygen that allows an annuity to breathe under fiduciary scrutiny. Annuity-friendly commentators who insist such clauses are unavailable are implicitly admitting that the underlying margins are too generous (and too opaque) to withstand rigorous fiduciary or litigation pressure.

By insisting on downgrade clauses, plan fiduciaries can align annuity allocations with transparency, accountability, and true participant protection—transforming what is often a “black box” into a manageable, contestable instrument.

This section refines the definitions of ‘party in interest’ and ‘prohibited transaction’ as applied in litigation involving TIAA. In Cunningham v. Cornell, TIAA simultaneously acted as recordkeeper, annuity issuer, and provider of other investment options. This case provides a clear framework for analyzing the structural conflicts and prohibited transactions associated with insurer-issued fixed annuities under ERISA and measuring damages.

II. Party in Interest

ERISA §3(14) defines a ‘party in interest’ broadly to include fiduciaries of the plan, service providers such as recordkeepers and consultants, employers sponsoring the plan, and any entity receiving direct or indirect compensation from the plan. TIAA is a party in interest in multiple capacities: as the recordkeeper, as the issuer of fixed annuity products, and as a provider of affiliated investment funds.

III. Prohibited Transactions Framework

A. Recordkeeping Compensation

As recordkeeper, TIAA received compensation directly from plan assets. Under ERISA §406(a)(1)(C), such arrangements constitute transactions with a party in interest, presumptively prohibited absent a statutory exemption.

B. Issuance of Fixed Annuities with Spread Profits

TIAA’s issuance of fixed annuities with hidden spreads also constitutes a prohibited transaction. The insurer profits directly from the difference between general account yields and crediting rates paid to participants. This implicates: – ERISA §406(a)(1)(A) and (C): transfer of plan assets to, or furnishing of services by, a party in interest; – ERISA §406(b)(1): fiduciary self-dealing when TIAA retains discretion to set crediting rates.

Thus, both the recordkeeping function and the spread mechanism independently trigger prohibited transaction analysis.

IV. Damages and Disgorgement

The proper remedy for a prohibited transaction under ERISA §409 is restitution or disgorgement of all profits obtained through the unlawful conduct. Disgorgement is an equitable remedy designed to restore participants to the position they would have occupied absent the prohibited transaction. It prevents unjust enrichment by requiring fiduciaries or parties in interest to surrender profits obtained at the expense of plan participants.

Disgorgement does not require proof of participant reliance or precise quantification of the general account yield. Instead, once a prohibited transaction is established, the burden shifts to the fiduciary or party in interest to demonstrate that no loss occurred. If they cannot, all spread profits must be disgorged.

Courts have repeatedly recognized this principle in fiduciary breach cases. In Brotherston v. Putnam, the First Circuit affirmed that once a fiduciary breach and related loss are shown, the burden shifts to fiduciaries to prove that the same losses would have occurred absent the breach. The Supreme Court in Hughes v. Northwestern reaffirmed the ongoing duty to monitor investments and remove imprudent ones.

Applied to TIAA, disgorgement would require the company to return the difference between what its general account earned and what it credited to participants. For example, if the general account earned 6% and participants received 4.5%, TIAA would be required to disgorge the 150 basis points retained as spread. This figure has been documented in the range of 120–150 basis points annually, as cited in NBC News (2024) and subsequent independent analyses. Importantly, the industry has not disputed these figures, underscoring their credibility. As TIAA has consistently had the highest rates among fixed IPG annuities, damages for other fixed annuities will be the TIAA 150bps spread plus the difference in yield between the other annuity and TIAA.

The Discovery Barrier: General Account Returns

In practice, litigants face years of stonewalling when requesting general account return data. Insurers argue that such information is proprietary and competitive. Thus, while the spread is the true measure of insurer profits, direct calculation is often impossible.³

This creates a paradox: the central harm (undisclosed spread profits) is simultaneously the central figure withheld in discovery. Plaintiffs risk being left without a calculable damages model, even when the fiduciary breach is clear.

Alternative Damage Models: Disgorgement

The Maersk complaint provides a practical alternative: a disgorgement-based model. Under this theory, insurers must disgorge all profits derived from the prohibited transaction, irrespective of plaintiffs’ ability to calculate them precisely. Courts have long recognized disgorgement as an equitable remedy in ERISA cases. See Donovan v. Bierwirth, 754 F.2d 1049 (2d Cir. 1985).⁴

Reasonable Estimates and Fiduciary Latitude

Even absent full disclosure, courts may allow plaintiffs to use reasonable estimation methods: – Comparator Returns — Using published yields on insurer-issued bonds or peer general account disclosures. – Stable Value Benchmarks — Data from Hueler Stable Value Universe or Morningstar stable value indices. – Economic Inference — Expert testimony showing spreads between credited rates and general account yields.

In Brotherston, the First Circuit endorsed damages models based on benchmarks rather than precise historical data.² Similarly, in Tibble v. Edison Int’l, 575 U.S. 523 (2015), courts accepted inferential models when defendants obstructed discovery.⁵

Policy Concerns and Fiduciary Implications

If insurers are allowed to withhold general account data, fiduciaries cannot meet their duty of prudence or loyalty. This regulatory gap highlights why annuities should not be default investments in ERISA retirement plans. Allowing equitable remedies such as disgorgement, and granting plaintiffs latitude in estimation, ensures fiduciary accountability despite insurer opacity.

V. Expert Commentary

TIAA annuities highlight the risks of structural conflicts and undisclosed spreads. As stated in NBC News (2024), annuities ‘flunk the most basic investment principle of diversification—do not put all your eggs in one basket.’ Public reporting has confirmed that TIAA annuities retain hidden spread fees of 120–150 basis points annually. Importantly, this figure has not been disputed by the industry. While other insurers may present even greater risks, TIAA remains the most visible example of how spread-based compensation undermines fiduciary protections.

VI. Conclusion

In Cunningham v. Cornell, TIAA’s dual roles as recordkeeper and annuity issuer created multiple prohibited transactions. Both the direct recordkeeping compensation and the hidden annuity spreads represent transactions with a party in interest. Under ERISA, these arrangements are per se prohibited absent exemptions. The proper remedy is disgorgement of spread-based profits, ensuring that plan assets are used solely for the benefit of participants and beneficiaries. Disgorgement is not punitive but restorative—it returns ill-gotten gains and enforces the exclusive benefit rule at the heart of ERISA.

The core harm in fixed annuity cases is the hidden spread profit, but insurers’ refusal to disclose general account returns makes direct measurement nearly impossible.

Courts should recognize: 1. Spread profits are per se compensation and subject to ERISA’s prohibited transaction rules. 2. Insurers’ refusal to disclose data should not immunize them from liability. 3. Plaintiffs are entitled either to full disgorgement of profits or to rely on reasonable estimates from comparator data.

Only by adopting these principles can ERISA fulfill its purpose of protecting plan participants from hidden and excessive fees.

I was quoted in this August 2025 article TIAA has hidden spread fees 120-150 basis points. This was in addition to have been quoted by NBC at 120 bps in August 24, which importantly has never been challenged by the industry in over a year.

Insurance companies are under weak, captive state regulation, which allows them to hide excessive risks and fees behind contracts with little to no meaningful disclosure. Fiduciaries under ERISA, however, are required to know the risks and fees in any investment before committing participant assets, and to monitor those risks on an ongoing basis. One-sided, secretive annuity contracts make it especially challenging to quantify damages or evaluate prudence.[1]

Pulitzer Prize–winning journalist Gretchen Morgenson has repeatedly exposed the hidden risks and fees buried in TIAA’s General Account fixed IPG annuity products in 401(k) type plans. In her August 2024 NBC News investigation, I was quoted as estimating that TIAA extracts excessive hidden spread profits of over 120 basis points (1.2%) annually on its flagship annuity, TIAA Traditional.[2]

Just one year later, in September 2025, I repeated my claim that TIAA’s hidden annuity spreads range from 120 to 150 basis points. Still, not a single insurer has challenged the accuracy of these numbers. Instead, TIAA’s spokesman declined to disclose what the company earns on these products, dismissing the question as ‘competitive and proprietary information.'[3]

Legal and Fiduciary Framework

Documenting that one-sided annuity contracts are ERISA Prohibited Transactions should be easier after the Supreme Court’s ruling in Cunningham v. Cornell. The Court clarified that since most annuity providers in plans are a party in interest, fiduciaries therefore have a duty to know and evaluate these spreads and risks.[4] Dr. Tom Lambert and I have an upcoming paper in the Journal of Economic Issues documenting these risks.[5] I have also written extensively in my blog about how annuities flunk prohibited transaction tests.[6]

With Pension Risk Transfer (PRT) annuities, one way to measure risk is to compare an annuity with downgrade provisions to one without. Insurers, because such provisions are less profitable, claim they will not write annuities with downgrade provisions. Yet such annuities have been issued in the past and could be again. Fiduciaries, in collusion with annuity providers, fail to ask for downgrade provisions because of monetary incentives.[7]

Annuity providers refuse to disclose risk and fees, but after Cunningham v. Cornell, judges may begin compelling disclosure in ERISA discovery. In the meantime, damages must be estimated through a variety of methods.[8]

My experience at Transamerica for 7 years, making profits, was that we wanted at least 200 basis points for any spread annuity product, general account, or separate account. Industry knowledge was that most insurers (who belonged to LIMRA) had similar 200-400 bps spreads, the exception being TIAA with lower spreads, 120 to 150 basis points with higher yields. Since spreads and general account returns are still (illegally under ERISA) secret, in litigation, we have taken the difference between the 2% yield of Prudential IPG GA vs. the 4.5% yield of TIAA to capture at least half the total spread profits to measure damages.

Measuring Annuity Risk: Credit Default Swaps and the Illusion of ‘Zero Risk’

1. The Problem of Measuring Annuity Risk

Insurance companies that issue Institutional Pension Guarantees (IPG) and PRT annuities often argue that the credit and liquidity risk embedded in these products is negligible or even ‘zero.’ In practice, the opposite is true:

• Single-Entity Credit Risk: Annuity obligations are backed solely by one insurance company. Default risk is concentrated.[9]

• Liquidity Risk: Annuities are long-duration obligations (often 10–30 years) that cannot be traded or hedged.[10]

2. Credit Default Swaps as a Proxy for Risk

Credit default swaps (CDS) provide one of the few market-based ways to measure credit risk. Short-term (1–5y) CDS spreads exist for insurers like MetLife, Prudential, Lincoln, and Athene. Longer horizons (10–20y) are illiquid or unavailable.[11]

3. The Regulatory and Fiduciary Gap

When insurers claim annuity risk is ‘too high to measure,’ they shift the burden of disclosure onto fiduciaries and participants. This creates fiduciary blind spots and regulatory loopholes. State regulators focus on solvency metrics that mask true long-term risk, while insurers misleadingly compare annuities to Treasury-like guarantees.[12] UPDATE November 6, 2025: Insurers use small ratings agencies to get favorable ratings on Private Credit. The SEC is investigating Egan-Jones for this Practice. Egan Jones has only 20 analysts rating over 5000 different issues. https://www.bloomberg.com/news/articles/2025-11-06/egan-jones-probed-by-sec-over-its-credit-ratings-practices Bloomberg Analysis of NAIC shows that capital charges for AA-rated issues are half of what an A rating is, so the incentive in $billions is to inflate ratings

4. Policy Implications and Recommendations

Recommendations include: (a) transparency in disclosures, (b) stress testing scenarios, (c) enhanced federal oversight to prohibit misleading ‘risk-free’ marketing, and (d) requiring downgrade provisions in PRT contracts.[13]

Conclusion: The central paradox of annuity risk is this: the longer the promise, the greater the exposure—yet the harder it is to measure. The absence of a CDS market beyond 5 years signals that risks are too high or uncertain to price.[14]

Market Snapshot: Indicative Insurer CDS (bps)

Issuer

Tenor

Latest Level (bps)

As-of Date

MetLife

5Y

62.0

Sep 30, 2025

AIG

5Y

74.2

Sep 30, 2025

Prudential Financial

5Y

57.6

Sep 30, 2025

Lincoln National

5Y

97.8

Sep 30, 2025

Athene

5Y

111.8

Sep 30, 2025

Chapter: Insurer Yield Curves, Spread Profits, and Tail Risk

Insurance company general accounts are fundamentally different from Treasuries or diversified mutual funds. They carry unique credit, liquidity, and tail risks, but convert these into spread profits largely invisible to policyholders and even fiduciaries.[15]

1. Yield Curve Steepness

Insurer portfolios rely on long-dated, illiquid assets with much steeper yield curves than Treasuries. The insurer pockets the maturity premium.[16]

2. Spread Profit Decomposition

Policyholders see short-duration crediting rates, while hedging costs and residual profits flow to the insurer.[17]

3. Misperception of Tail Risk

Investors struggle to distinguish between 1-in-100 and 1-in-10,000 events, despite the 100-fold difference. Insurers exploit this by monetizing tail risk.[18]

4. Regulatory Optics vs. Economic Risk

Treasury-based hedges shorten reported duration to ~2–3 years, but true long-horizon risks remain embedded.[19]

5. Fiduciary Implications

Fiduciaries must not confuse lack of market pricing with absence of risk. Disclosures should highlight steep curves, spread profits, and tail risk.[20]

25 Tobe, Christopher B., The Consultants Guide to Stable Value. Journal of Investment Consulting, Vol. 7, No. 1, Summer 2004, Available at SSRN: https://ssrn.com/abstract=577603

The recent ruling by Judge Margaret Garnett in the Southern District of New York marks a watershed moment for retirees challenging the safety and legality of Pension Risk Transfers (“PRTs”). In Doherty v. Bristol-Myers Squibb Co., No. 24-cv-06628 (S.D.N.Y. Sept. 29, 2025), the court refused to dismiss key claims against Bristol-Myers, its pension fiduciaries, and State Street Global Advisors for their role in transferring $2.6 billion in retiree pension obligations to Athene, a Bermuda-linked annuity insurer owned by Apollo Global Management. While the ruling does not resolve the case, it allows retirees’ central allegations to move forward: that their benefits were placed at “substantial risk” by offloading them to Athene, and that the transaction stripped them of longstanding ERISA protections and federal backstops. For thousands of pensioners, this is a significant victory—the first step in holding corporate sponsors and their advisers accountable for shifting obligations into opaque, private-equity-controlled insurance structures.

Substantial Risk of Default (p. 9 of Opinion)

At the heart of Judge Garnett’s decision is the finding that plaintiffs plausibly alleged a “substantial risk” that Athene could default on its obligations. The court credited detailed allegations that Athene operates as one of the so-called “new risk-taking insurers,” with portfolios concentrated in illiquid, volatile assets such as private credit and structured products. Unlike traditional insurers with conservative surplus levels, Athene ranked near the very bottom of U.S. carriers in surplus-to-risk ratios. Even more troubling, 80% of Athene’s liabilities were reinsured through Bermuda affiliates owned by Apollo itself. Such affiliated reinsurance lacks the arm’s-length pricing discipline of the open market and, because Bermuda requires less capital than U.S. regulators, magnifies counterparty risk. The court highlighted parallels between Athene and other recently failed insurers that collapsed under similar capital structures. For retirees, this means their lifetime benefits now hinge on the solvency of a highly leveraged private-equity-controlled insurer—rather than on a Fortune 500 plan sponsor or the Pension Benefit Guaranty Corporation (PBGC). (See Doherty v. Bristol-Myers Squibb Co., No. 24-cv-06628, slip op. at 9–12 (S.D.N.Y. Sept. 29, 2025)).

Reduction of Protections and Guarantees (p. 13 of Opinion)

Equally important, Judge Garnett recognized that the Athene transaction diminished retiree protections. Once Bristol-Myers terminated its plan through annuitization, retirees lost both ERISA fiduciary protections and PBGC insurance coverage. In their place, they now rely solely on state guaranty associations, which cap coverage at levels far below the obligations owed. This substitution is no small matter. The PBGC is a federal entity backed by Congress. State guaranty associations, by contrast, are fragmented nonprofits with weak funding and uneven benefit caps. For retirees with larger pensions, the coverage gap could be devastating in the event of insurer insolvency. (See Doherty v. Bristol-Myers Squibb Co., slip op. at 13–15).

As argued in prior analyses, including *Annuities Are Prohibited Transactions via ChatGPT* (June 13, 2025)[1] and *State Guarantee Associations Behind Annuities Are a Joke* (June 24, 2025)[2], this shift from federal to state protection materially reduces security for beneficiaries. This legal recognition—that annuitization materially reduces participant protections—will resonate in every ongoing and future PRT case.

Disappointment on “Party in Interest” (p. 24 of Opinion)

The one setback in the ruling was the court’s conclusion that Athene was not a “party in interest” under ERISA because it merely sold a product, rather than serving as a fiduciary. While this shields Athene from certain prohibited transaction claims, it leaves Apollo and its insurance subsidiaries effectively “too big to jail.” This is particularly galling given Apollo’s history. Its founder and long-time CEO, Leon Black, paid Jeffrey Epstein $170 million for so-called “tax advice.” Apollo has since expanded its control over retirement assets by acquiring insurers such as Athene, exploiting regulatory arbitrage to chase yield with retirees’ money. The decision reflects an unfortunate judicial blind spot: acknowledging the risks of private-equity-backed annuities while refusing to hold the insurers themselves to ERISA’s highest fiduciary standards. (See Doherty, slip op. at 24).

State Street’s Role and the Missing “Downgrade” Clause

A central claim against State Street remains: that as adviser to Bristol-Myers, it failed to negotiate appropriate safeguards. Most notably, State Street did not require Athene to maintain a “downgrade provision” to protect retirees if the insurer’s creditworthiness deteriorated. Such provisions, common in sophisticated reinsurance and corporate bond agreements, could have forced Bristol-Myers to step back in or provide collateral if Athene’s ratings slipped. By ignoring this safeguard, State Street effectively placed retirees at the mercy of Apollo’s investment decisions. As argued in *Weak Standards Make Annuities Prohibited Transactions in ERISA Plans* (Sept. 15, 2025)[3], fiduciaries cannot simply chase the lowest-cost annuity contract—they must prudently evaluate long-term risks and negotiate protections like downgrade provisions.

Broader Implications: ERISA, Annuities, and Private Equity