TIAA and its academic partners want you to believe they have discovered a free lunch in retirement investing: add a fixed annuity to a target date fund, and you magically get higher returns and lower risk.

That claim is now being aggressively promoted through a new TIAA Institute / Charles River Associates (CRA) paper, The Impact of TIAA Traditional in Target Date Glidepaths. The paper concludes that target date funds (TDFs) including TIAA Traditional “outperform” conventional TDFs across virtually every scenario—especially because the annuity appears to reduce volatility while maintaining bond-like returns.

There’s just one problem.

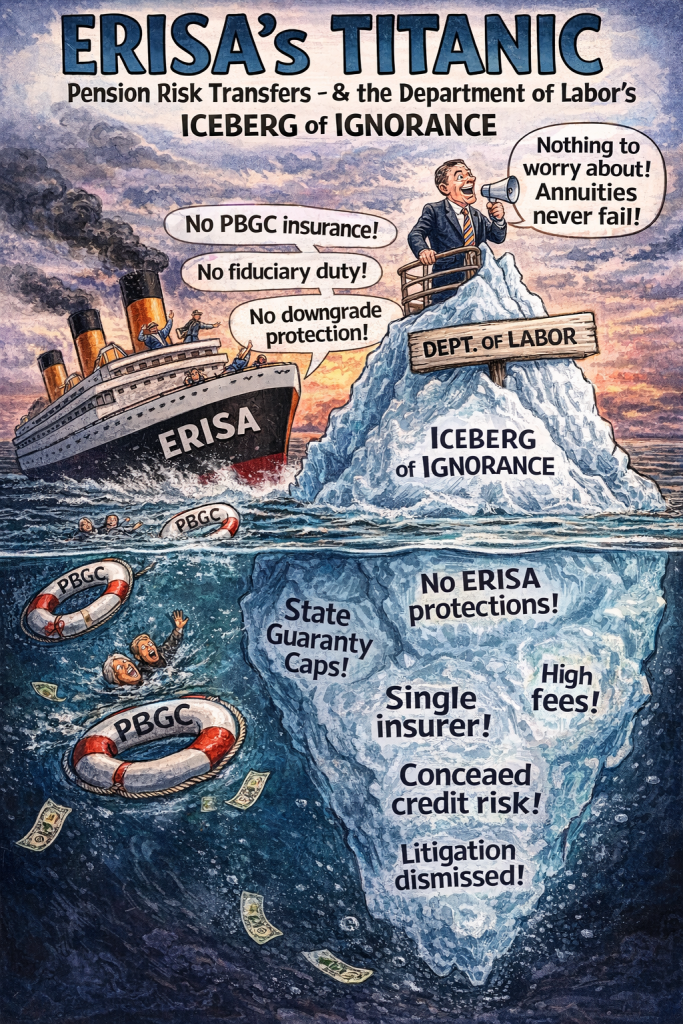

The “low risk” that drives these results isn’t real, and the analysis completely ignores the upcoming legal issue: fixed annuities issued by TIAA are prohibited transactions under ERISA when mixed into 401(k) target date funds.

This is not an academic quibble. It is the same kind of modeling sleight-of-hand that courts have rejected in employer stock cases, stable value cases, and valuation fraud cases for decades.

The Core Trick: Fake Volatility

TIAA’s modeling rests on a simple but profoundly misleading assumption: that TIAA Traditional has lower volatility than bonds.

Why does it appear that way?

Because annuities are not marked to market.

TIAA Traditional’s returns are not set by market prices. They are set by internal crediting decisions, made at TIAA’s discretion, based on assets held in TIAA’s opaque general account. Losses are smoothed. Gains are withheld. Risk is buried on the insurer’s balance sheet.

That doesn’t make risk disappear—it just hides it.

Calling this “lower volatility” is like calling a non-traded REIT safer than public real estate because the price doesn’t move. Courts don’t buy that logic, and fiduciaries shouldn’t either.

Bonds and Annuities Are Not the Same — TIAA Admits This (Then Ignores It)

In a quiet but telling footnote, the TIAA Institute paper admits:

“Per the Investment Company Act of 1940, an annuity cannot be part of a mutual fund.”

That should have been the end of the analysis.

Instead, TIAA proceeds to do exactly what the law forbids in substance if not in form: it embeds an insurance contract inside collective investment trusts and managed accounts and then models it as if it were a bond fund.

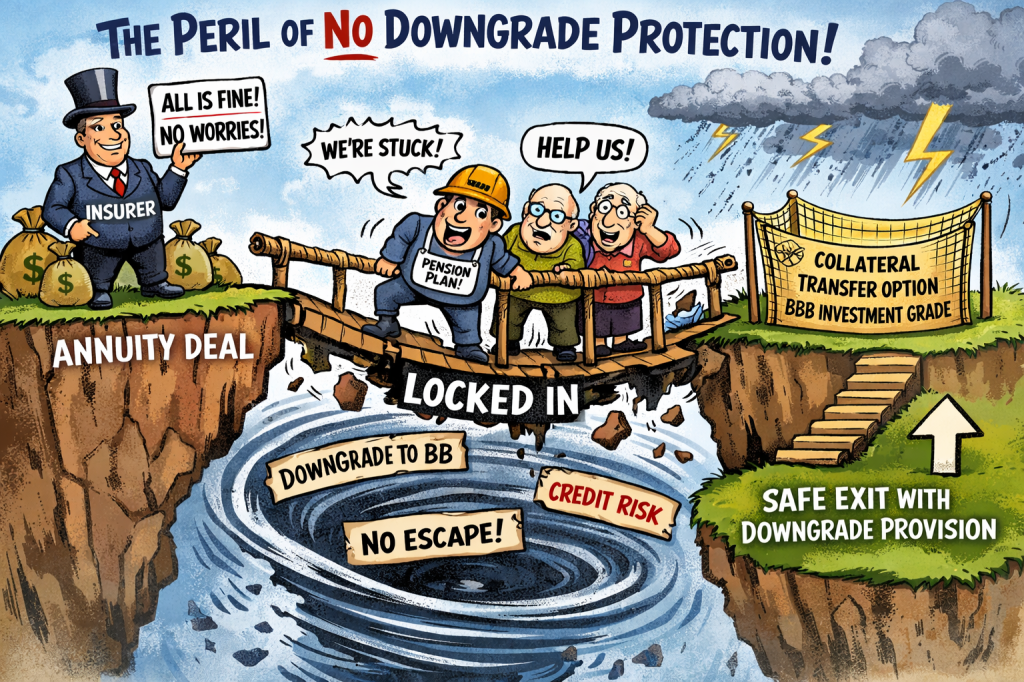

But annuities are not bonds:

- They are illiquid

- They cannot be freely sold

- They often cannot be exited without delay or penalty

- Annuitization is frequently irrevocable

- There are no downgrade or termination rights

- Participants bear insurer credit risk, not market risk

Diversification theory assumes liquidity. Once liquidity is gone, correlation statistics are meaningless. You are not “rebalancing” risk—you are locking it in.

The Prohibited Transaction Elephant in the Room

Most strikingly, the TIAA Institute analysis never mentions ERISA §406 prohibited transactions. Not once.

That omission is not accidental. It is essential to the conclusion.

Here is the reality TIAA’s modeling ignores:

- TIAA is the recordkeeper

- TIAA is the annuity issuer

- TIAA sets the crediting rates

- TIAA retains the spread

- TIAA is therefore a party in interest multiple times over

Under ERISA, when a fiduciary causes a plan to transact with itself—or retain a product that generates undisclosed compensation—that transaction is presumptively illegal, regardless of performance.

And make no mistake: TIAA Traditional generates compensation.

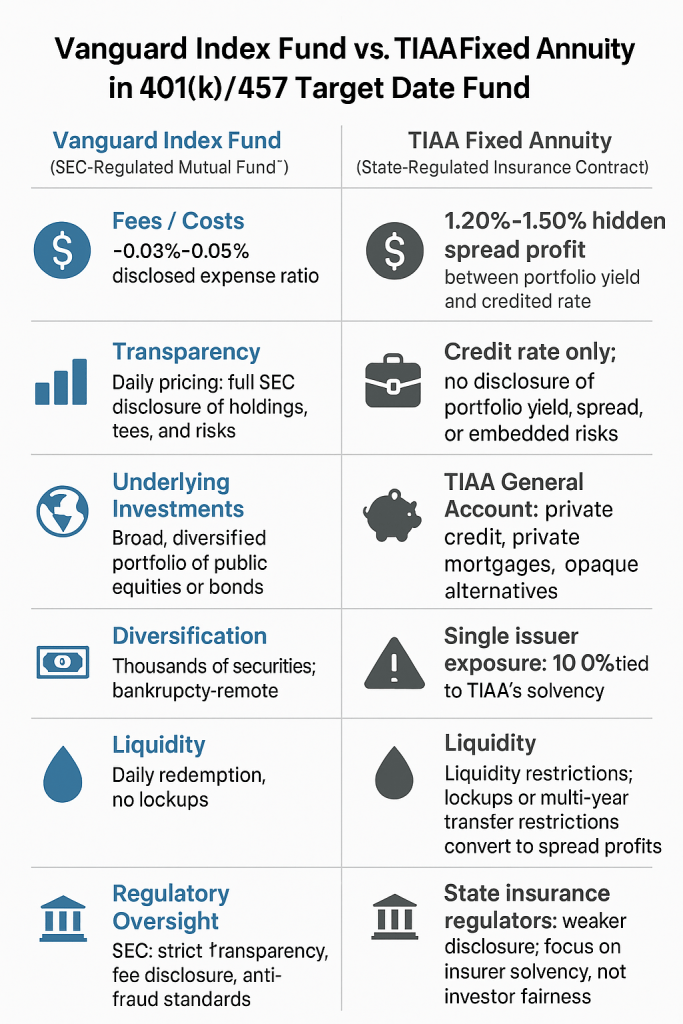

“No Fees” Is a Myth — The Spread Is the Fee

TIAA repeatedly claims that Traditional has “no fees.” That is simply false.

The compensation is taken as spread—the difference between what TIAA earns in its general account and what it credits to participants. Independent reporting, including NBC News, has reported that the hidden spread is around 150 basis points annually.

Importantly, this spread figure was not disputed by TIAA when given the chance by NBC.

Spread is compensation. Undisclosed compensation retained by a fiduciary is the textbook definition of ERISA §406(b)(1) self-dealing.

No amount of glidepath modeling can legalize that.

Performance Does Not Cure a Prohibited Transaction

This is where TIAA’s entire argument collapses.

After the Supreme Court’s decision in Cunningham v. Cornell, plaintiffs do not need to plead around exemptions. Defendants must prove them.

That means:

- You do not get to justify self-dealing because a model looks good

- You do not get to ignore conflicts because returns are “competitive”

- You do not get to replace law with regression analysis

If a transaction is prohibited, the remedy is disgorgement, not benchmarking.

Why This Matters for Courts, Fiduciaries, and Plaintiffs

Target date funds are now the default investment for tens of millions of workers. Embedding insurance contracts inside them—without liquidity, transparency, or ERISA-compliant compensation structures—creates a perfect storm:

- Participants cannot exit

- Fiduciaries cannot monitor properly

- Conflicts are structural, not incidental

- Losses may not show up until it’s too late

We have already seen courts reject “prudent process theater” in other contexts. The same reckoning is coming here.

.

Bottom Line

TIAA’s target date modeling works only if you accept three false premises:

- That hidden risk is no risk

- That illiquid insurance contracts are bonds

- That ERISA’s prohibited transaction rules don’t apply

None of those premises survives serious scrutiny.

Once annuities are properly treated as what they are—ongoing transactions with a party in interest that generate undisclosed compensation—the supposed diversification and risk reduction disappear.

What’s left is a glidepath built on a legal and economic illusion.

Related Commonsense 401(k) Project articles:

- TIAA Exposed for Excessive Hidden Annuity Spread Fees — Again

- https://commonsense401kproject.com/2025/09/21/tiaa-exposed-for-excessive-hidden-annuity-spread-fees-again/

Appendix: TIAA Is Not Alone — Target Date Funds Are Quietly Filling Up with Insurance Contracts

One of the most predictable responses to criticism of TIAA’s target-date modeling is:

“This isn’t just TIAA — everyone is doing it.”

That response is meant to normalize the problem. In reality, it does the opposite.

Recent Morningstar reporting confirms what fiduciary litigators and independent analysts have been seeing for several years: a growing number of target-date funds are quietly embedding fixed annuities inside 401(k) default investments — outside SEC regulation, with minimal transparency, and with little understanding by plan sponsors or participants of what they actually own.

This appendix explains why that trend is dangerous, legally flawed, and ripe for litigation.

Morningstar Confirms the “Hidden Trend”

In a 2025 article titled “A Hidden Trend Is Changing 401(k) Plans — Here’s What It Means for Investors,” Morningstar documents the increasing use of annuity-based components inside target-date strategies, particularly in large plans that use collective investment trusts (CITs).

Morningstar presents this as an innovation. It is better understood as regulatory arbitrage.

Key points Morningstar inadvertently confirms:

- These target-date products are not SEC-registered mutual funds

- They are primarily state-regulated CITs or managed accounts

- The annuity components are illiquid, opaque, and insurer-controlled

- Risk and return characteristics are not comparable to securities

That matters, because SEC-registered mutual funds correctly prohibit fixed annuities. They have done so for decades, precisely because annuities:

- Are not market-priced securities

- Cannot be fairly valued daily

- Introduce issuer credit risk

- Embed compensation through spread rather than disclosed fees

CITs, by contrast, sit in a regulatory gray zone — particularly state-chartered CITs, which often lack meaningful federal oversight.

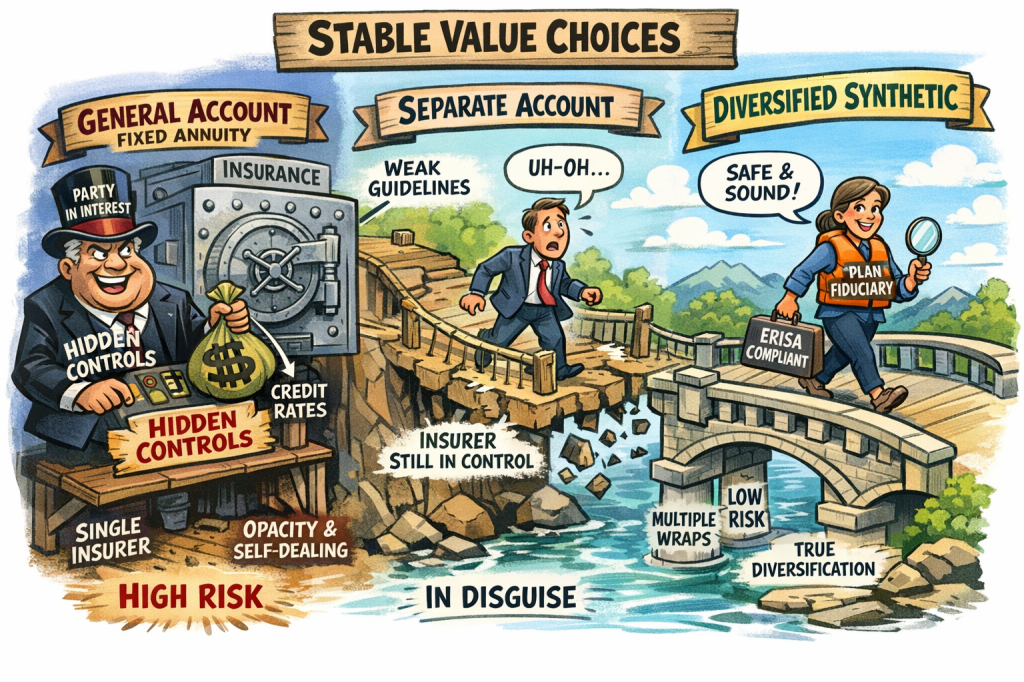

These Are Not Synthetic Stable Value Products

Industry defenders often try to blur the lines between:

- Synthetic stable value (e.g., Vanguard RST, Fidelity MIPS), and

- Insurance general-account or separate-account annuities

They are not the same.

Synthetic stable value:

- Uses transparent bond portfolios

- Has independent wrap providers

- Has explicit fees

- Has market-observable returns

- Generates little or no insurer spread profit

By contrast, the annuities now appearing in target-date funds are, in my opinion, almost entirely general-account (GA) or separate-account (SA) insurance products, for a simple reason:

There is no meaningful spread profit in true synthetic stable value.

Insurers and recordkeepers are not pushing annuities into target-date funds for diversification. They are doing it because spread is far more profitable than explicit fees — and far harder for fiduciaries to monitor.

Empower Pushes the Envelope Even Further

Empower has gone beyond traditional fixed annuities and is now actively marketing:

- Index annuities, and

- Target-date structures that explicitly combine annuities with private equity exposure, including partnerships with Blackstone.

Empower proudly announced the launch of what it called the “first ever zero-fee index fund.” That claim deserves skepticism.

“Zero fee” does not mean “no compensation.” It almost always means:

- Compensation is embedded

- Returns are engineered

- Pricing is discretionary

- Spread replaces fees

At the same time, Empower has partnered with Blackstone to insert private equity into retirement default investments — layering illiquidity on top of illiquidity, and valuation opacity on top of opacity.

This is not diversification. It is complexity as camouflage.

The Great Gray Stable Value Appendix Tells the Truth

The most revealing disclosure may come not from critics, but from industry documents themselves.

In an appendix to the Great Gray Collective Investment Trust stable value fund, the sponsor discloses material issues with the underlying Empower General Account Fixed Annuity.

Most importantly, the document states that the crediting rate process is “discretionary and proprietary.”

That single sentence is devastating.

It is a direct admission that:

- Returns are not the transparent output of a portfolio

- Returns are not market-based

- Returns are not priced competitively

- Returns are the product of internal insurer decision-making

That is the definition of general-account spread mechanics.

For ERISA purposes, it means:

- Participants do not receive the return of the assets backing the contract

- The insurer retains the difference

- The compensation is undisclosed

- The fiduciary cannot independently verify reasonableness

Why This Matters Under ERISA

Once fixed annuities are embedded inside target-date funds:

- The plan is in an ongoing transaction with a party in interest

- Compensation is taken through spread

- The fiduciary cannot monitor or benchmark returns

- Liquidity is lost without participant consent

- Risk is shifted from markets to the insurer’s balance sheet

Performance modeling does not cure any of that.

After Cunningham v. Cornell, fiduciaries cannot rely on:

- “Everyone is doing it”

- “The glidepath looks good”

- “The model outperforms”

If the structure is a prohibited transaction, the remedy is disgorgement, not better charts.

The Bigger Picture

Target-date funds were supposed to simplify retirement investing.

Instead, they are becoming the Trojan horse through which:

- Fixed annuities

- Index annuities

- Private equity

- Opaque insurance economics

are quietly introduced into ERISA plans — without SEC oversight, without transparent pricing, and without meaningful participant understanding.

TIAA may be the most visible example. It is no longer the only one.

Bottom Line

Morningstar is right about one thing:

There is a hidden trend changing 401(k) plans.

But what it means for investors is not innovation or safety.

It means:

- Less transparency

- More conflicts

- More prohibited transactions

- And a coming wave of litigation

Target-date funds are no longer just glidepaths.

They are becoming distribution platforms for insurance spread and alternative-asset fees — and ERISA was never designed to allow that.

SOURCES

https://www.morningstar.com/funds/hidden-trend-is-changing-401k-plans-heres-what-it-means-investors

https://www.empower.com/press-center/empower-launches-first-ever-zero-fee-index-fund

. https://greatgray.com/wp-content/uploads/2025/05/0.08-Stable-Value-Funds-2024-Final.pdf