Pension Governance, Fee Economics, Media Influence, and Political Incentives

I. Overview

Private Equity (PE) is one of the most politically dominant financial sectors in the United States. It controls approximately $12 trillion in global assets, and the revenue it extracts from public pension systems—including California’s CalPERS and CalSTRS—generates tens of billions of dollars in annual fees for PE general partners (GPs) and their affiliates.

Katie Porter has emerged as one of the few national-level elected officials willing to challenge PE’s influence, particularly in:

Health care

Housing and rents

Corporate governance abuses

Private Equity fee extraction from public pensions

Because of this, Porter represents a credible threat—not just rhetorically, but structurally—to one of PE’s largest and most reliable revenue sources: California’s public pension system, which is one of the largest pools of institutional capital on earth.

Porter’s positions therefore create a direct financial incentive for the PE industry to block, weaken, or discredit her candidacy for Governor.

II. Why Katie Porter Threatens Private Equity’s Economic Interests

1. California Public Pensions Are a $50+ Billion PE Fee Machine

CalPERS and CalSTRS together hold more than $75 billion in Private Equity positions. Assuming typical fee structures (2% management + 20% carry + monitoring fees, transaction fees, fund-of-fund layers), these systems generate at least:

≈ $3 billion per year in recurring fees and carried interest paid to PE managers.

This makes California one of the two or three most valuable public-pension clients for the global PE industry. No other U.S. state has as much concentrated PE capital—and thus no other governorship poses greater regulatory risk to PE’s fee extraction models.

Katie Porter, if elected, would appoint or influence:

CalPERS & CalSTRS board members

CalPERS CEO

CalPERS CIO

Legislative oversight structures

Transparency initiatives

Fiduciary standards for alternatives

Her governorship alone could shift tens of billions of dollars in capital allocation and transparency expectations.

This is a structural threat to PE that dwarfs the conventional left–right political calculus.

2. Porter’s Policy Agenda Collides Directly With PE Business Models

Health Care

Porter is one of the few members of Congress who has directly attacked:

PE-owned emergency room staffing companies

PE roll-ups of physician practices

Surprise-billing profit strategies

Debt-driven hospital consolidation

Health care is one of the most lucrative sectors in PE, generating outsized IRRs. Porter’s focus puts those strategies under direct reputational and regulatory scrutiny.

Housing

Porter has criticized:

PE consolidation of rental housing

Institutional single-family landlords

Eviction-driven returns

Fee layering on tenants

PE firms such as Blackstone and Invitation Homes are among the largest landlord entities in the U.S.

Pensions and Financial Transparency

Porter has been one of the few national politicians willing to challenge:

Hidden carry structures

Non-disclosure agreements

Fee opacity

“Zombie funds”

Private credit valuation risk

Benchmark manipulation

If she brings these issues into California state policy, PE faces:

Higher transparency obligations,

Stricter fiduciary standards, and

Potential capital reallocation away from opaque funds.

III. How Private Equity Has Already Signaled its Political Preferences

1. Evidence from the 2024–2025 California Senate Race

While direct campaign-finance records require careful interpretation, multiple political observers noted that:

PE-linked donors and financial-sector PACs were disproportionately aligned with Adam Schiff rather than Porter.

This pattern aligns with how PE has historically backed lowest-risk, establishment-aligned candidates who are unlikely to disrupt pension-fee revenue streams.

Porter, by contrast, has:

No donor dependence on the finance industry

Built her brand on adversarial oversight

Already taken positions hostile to PE sectors (health care, housing)

This makes her a high-risk candidate for PE’s interests.

IV. How Private Equity Typically Responds to Political Threats

Private Equity rarely attacks a candidate on policy because its business model cannot withstand public scrutiny. Instead, PE-funded messaging networks use:

A. Personality-Based Attacks

Focus on tone, communication style, or staff management

Use micro-scandals to divert attention from PE’s own impact

This pattern is identical to how establishment actors targeted Elizabeth Warren, where Native American heritage and personality tropes were used to obscure her substantive financial-reform agenda.

B. Identity-Based Distractions

Exactly as you noted: instead of debating Porter’s policy threat to PE’s business interests, PE-aligned media will highlight:

Her alliance with Elizabeth Warren

Cultural or identity issues

Gender-coded expectations of “likeability” and “temperament”

C. Narrative Inversion

The goal is to shift the voter conversation away from:

PE’s harmful effects on health care

PE’s role in driving housing unaffordability

PE’s fee extraction from pensions

…and toward anything else.

V. The Ohio Case: A Playbook for How Private Equity and Hedge Fund Influences California Media

In my Ohio analysis, you documented how:

The press manufactured “fake scandals” around personalities

Meanwhile burying or ignoring massive pension corruption

Local media outlets aligned with PE-linked donors

High-fee public pension contracts were protected by political actors

(See: “Ohio Media’s Complicity: How a Fake Scandal Hid the Real Teacher Retirement System Corruption”)

This model is instructive:

If PE can turn an entire state’s press ecosystem against a reformer to protect fee revenue, California—where tens of billions in fees are at stake—will face the same pattern.

Like Ohio = Private Equity Apollo controls the Gannett papers by debt which include Ventura County Star, The Desert Sun, Record Searchlight, Salinas Californian, Visalia Times-Delta,

A major newspaper Sacramento Bee / McClatchy is owned by the Chatham Asset Management hedge fund and is basically the paper of record for CALPERS and CALSTRS. They also contol the Fresno Bee, Modesto Bee and others

The Alden Global Capital hedge fund owns the Media News group, which includes the San Diego Union-Tribune, Orange County Register, L.A. Daily News, Riverside Press-Enterprise, Bang, Mercury News, East Bay times. Also recently expanded into Northern California with The Press Democrat.

Los Angeles Times owner Nant Capital sold the San Diego Union-Tribune to Alden and has rarely been critical of Private Equity.

Almost all California TV stations are owned by firms with strong Private Equity Hedge Fund Ties.

The largest Nextstar has private equity hedge fund roots and owns KTLA 5 (Los Angeles) KSWB FOX 5 (San Diego) KTXL FOX 40 (Sacramento), KSEE 24 (Fresno) KRON 4 (San Francisco; via Nexstar’s majority control of “The CW”). Additional affiliates in Bakersfield, Chico/Redding, Palm Springs.

Sinclair Broadcast Group is hedge fund owned and includes KMPH FOX 26 (Fresno) KPTH/KTVU partnerships in some markets and multiple smaller market affiliates in Northern and Central CA

TEGNA was nearly purchased by Apollo in 2022 but was blocked by the FCC and they own KGTV ABC 10 (San Diego) and KXTV ABC 10 (Sacramento)

Scripps is publicly held, but is heavily HF led and credit lines from Blackstone. Scripps owns KGTV, KSBW (Monterey/Salinas), KERO (Bakersfield)

VI. Why PE and CalPERS Staff Interests Align Against Porter

Reform candidates become targets of orchestrated negative coverage

California’s dynamic is similar—but the capital at stake is vastly larger.

VII. PE’s Dark-Money Ecosystem in California

Private Equity already exerts considerable influence in California through:

Charter school lobbying (as shown in The Intercept, July 2021)

Dark-money networks routed through 501(c)(4)s

PACs aligned with real estate, hospital chains, and tech investors

Groups that present as “education reform” or “innovation” advocates

Porter opposes charter-school expansion. PE-backed charter networks see her as a threat to:

Real estate acquisitions

Asset-backed leverage structures

Cash-flow extraction from public-school budgets

This adds another multimillion-dollar incentive for PE to oppose her.

VIII. Why Porter Is Uniquely Dangerous to the PE–Pension Complex

Porter understands—down to the legal and accounting levels—how:

Carried interest works

Valuation smoothing works

Pension-fund PE benchmarks are engineered

Capital-call structures manipulate risk

Opaque reporting burdens pensions with unmonitored liabilities

Private credit threatens system solvency

A California Governor with that level of literacy would be the first in modern history.

The “alarming scenario” for PE looks like this:

Porter appoints a CalPERS Board majority interested in transparency

CalPERS shifts $10–20 billion out of opaque PE/credit

CalSTRS follows

LA County and SF City & County mimic the model

California becomes the first state to audit PE fees line-by-line

Other states copy the model

A single California governor could trigger a national retrenchment of PE in public pensions.

This is why PE cannot allow her to win.

IX. Conclusion: Why You Are Seeing Personality Attacks Instead of Policy Debate

Private Equity cannot defend:

surprise medical billing

PE-run emergency rooms

housing consolidation

fee extraction from teacher pensions

opaque valuation methodologies

charter-school dark money

performance-lag gimmicks

political corruption in pension governance

So it avoids those topics entirely.

Instead, it pushes:

personality narratives

identity politics

small “scandals”

staff management stories

“tone” criticism

character-based tropes

guilt-by-association techniques

Because the truth—that California’s next Governor could put $50+ billion of PE fee streams at risk—would collapse PE’s political strategy overnight.

Katie Porter is not being targeted because she is “difficult.” She is being targeted because she is dangerous—specifically, to the private-equity profit engine tied to CalPERS, CalSTRS, and the California public-pension complex.

I. Introduction: Judges Are Not Seeing the Real Risk

Despite clear, quantifiable evidence that most Pension Risk Transfer (PRT) annuities violate ERISA’s prudence, loyalty, and prohibited-transaction rules, federal courts have repeatedly dismissed PRT complaints on superficial grounds.

Judges are not just wrong; they are missing the entire risk story.

The pattern is consistent:

They assume “annuities are safe” because insurers have not recently failed—ignoring Executive Life, Confederation Life, and AIG.

They defer to a captured Department of Labor (DOL) whose 2024–25 PRT reports downplay risk and were influenced heavily by insurer lobbying.

They treat PRT transactions as routine outsourcing, instead of the massive conflicted-party transactions they truly are.

They allow insurers to hide behind state regulation, ignoring offshore reinsurers, spread arbitrage, credit-default-swap pricing, and the lack of downgrade provisions.

They adopt a “no harm, no foul” approach that is wildly inconsistent with ERISA’s mandate that fiduciaries evaluate risk before harm occurs.

The question is no longer, “Are judges missing something?” It is: “Why are judges refusing to even look?” See the recently added Appendix for new PRT Academic Research.

II. Structural Reasons Judges Currently Give Insurers a Free Pass

Judges often do not grasp that a PRT annuity is not a bond. It is a credit-risk bet on a single insurer, whose solvency is priced daily in the CDS market and has no maturity.

Under ERISA, fiduciaries must prove prudence—not plaintiffs.

Many district courts flipped the burden, demanding plaintiffs prove:

the insurer will fail,

the guaranty association will be insufficient,

spread profits will impair benefits.

This is legally incorrect.

3. Courts Ignore Prohibited Transactions (the Strongest Claim)

PRT transactions trigger at least three independent §406 violations:

§406(a)(1)(D): transfer of plan assets that benefits a party in interest (insurer earns spread income).

§406(b)(1): fiduciary self-dealing through consultants tied to insurers (common in State Street, Mercer, etc.).

§406(b)(3): kickbacks disguised as reinsurance or spread arrangements.

See my article https://commonsense401kproject.com/2025/11/01/annuities-are-a-prohibited-transaction-dol-exemptions-do-not-work/. Annuities are almost always ERISA Prohibited Transactions. Insurers blatantly claim that these annuity contracts have a Prohibited Transaction Exemption (PTE) but most flunk PTEs because they are one-sided contracts as documented by their failing of the Impartial Conduct Standards 1. Loyalty 2. Prudence 3. Reasonable Compensation 4. No misleading statements. The DOL is totally ignorant of PTEs, and the industry knows this and has gotten away with this fraud for decades until recent litigation facilitated by Cunningham v. Cornel

shows:

No insurer has ever proven compliance with PTE 95-60 or 84-24.

Courts have wrongfully treated these exemptions as if they automatically apply.

That is a reversible error.

4. Courts Wrongly Treat PBGC Loss as Irrelevant

Removing retirees from PBGC protection is an immediate, quantifiable harm:

Participants lose a federal backstop.

They lose downgrade protection.

They become unsecured creditors of a single private insurer.

Plaintiffs framed both prohibited-transaction and imprudence claims.

Athene’s offshore reinsurance is especially egregious.

State Street’s consultant conflicts create a classic §406(b) problem.

The plan could have chosen a downgrade-protected annuity, but did not.

The insurer (Athene) is associated with Apollo’s extreme private-credit and offshore strategies, making the risk objectively higher.

This is the perfect case for plaintiffs.

A settlement would be enormous because:

Damages = the present value of the increased risk premium (CDS spread difference) over the lifetime of the annuity obligations.

Plaintiffs can quantify damages using the Lambert–Tobe efficient-frontier model.

Discovery would expose Apollo/Athene’s offshore structures—something they will pay heavily to avoid.

V. Why Appeals Must Highlight the “Missing Evidence Problem”

The most compelling appellate argument is procedural:

Courts are dismissing cases without allowing discovery necessary to evaluate risk—thereby insulating insurers from any review.

This violates:

The pleading standards of Twombly and Iqbal (plausibility was established).

The fiduciary-monitoring requirements under Tibble v. Edison.

The prohibited-transaction rules under Harris Trust.

Appeals can force discovery where:

Credit-risk documents,

consultant conflicts,

downgrade analyses,

reinsurance structures,

spread profit calculations

will destroy the defense.

VI. Conclusion: These Cases Are “The New Tobacco”—And Courts Must Stop Looking Away

PRT annuities represent:

immense hidden risk,

massive undisclosed compensation to insurers,

offshore opacity,

downgrades without recourse,

loss of PBGC protection,

actuarial manipulation,

and a growing link to private credit that resembles 2008 all over again.

Judges have been asleep at the wheel. Appeals are not just warranted—they are essential.

The Bristol-Myers case is the turning point. If it proceeds through discovery, Athene and State Street will face unprecedented exposure.

If it settles, it will be one of the largest ERISA settlements in history.

But plaintiffs must push these cases to the appellate courts—because district judges have shown they are unwilling (or unable) to confront the insurance-industry machinery head-on.

——————————————————————————-

Appendix 1: What the New Corporate-Finance Literature Reveals About PRT Motives and Systemic Risks

A new academic study—Sven Klingler, Suresh Sundaresan, and Michael Moran (2022)—provides the most comprehensive empirical analysis to date of why corporations execute Pension Risk Transfers (PRTs) and what the consequences are for the pension system. Although written from a corporate-finance standpoint rather than a fiduciary or participant-protection perspective, its findings strongly reinforce the central warnings in this article: PRTs are most attractive to financially strong sponsors, increase systemic risk for the PBGC, and shift risk onto retirees without disclosure or safeguards. 22Paper

Below is a short summary of the findings most relevant to litigation, fiduciary duty, and the urgent need for appellate review.

1. Corporations use PRTs not because they are safer—but because the PBGC premium structure is distorted

The authors demonstrate that PRT decisions are driven primarily by:

High “flow-through costs”—the size of the plan relative to the company, which drives earnings volatility and credit-rating pressure.

A large “PBGC wedge”—the mismatch between high PBGC premiums and the low economic value of the “PBGC put” for financially strong companies.

Their regression evidence shows that a one-standard-deviation increase in either factor increases the probability of a PRT by 43–55%. 22Paper

This is critical for ERISA cases: PRTs are not chosen because they reduce risk to retirees. They are chosen because PRTs allow corporations to escape PBGC premiums and balance-sheet volatility, regardless of the insurer’s credit risk. That is the opposite of a “best-interest-of-participants” standard.

2. Companies engaging in PRTs are the safest sponsors with the least risky pension portfolios

The paper finds:

PRT sponsors have lower default risk, measured via Expected Default Frequency (EDF).

PRT sponsors have 6.5 percentage points less equity risk in their pension portfolios.

These “safer sponsors” are precisely the ones that least need to offload risk—and whose retirees lose the PBGC guarantee as soon as the annuity contract is executed. 22Paper

Implication for my argument: PRTs increase systemic risk because they remove the safest and most stable plans from the PBGC insurance pool, leaving PBGC with the weakest sponsors. Yet courts routinely ignore this actuarial and systemic fact when dismissing PRT-related fiduciary claims.

3. PRTs have already reduced PBGC’s insured participant base by more than 10%

The paper shows that from 2012–2021:

$150+ billion in obligations were transferred.

The number of PBGC-insured participants fell by ~10%.

PRTs reduced total DB plan assets by about 7%.

This contraction of the insured pool is accelerating. 22Paper

Litigation relevance: When courts say “participants are not harmed,” they ignore evidence that PRTs structurally:

Weaken the PBGC’s solvency.

Reduce risk-pool diversification.

Increase the probability of future benefit losses for the remaining PBGC participants.

This is directly contrary to ERISA’s statutory design.

4. PRTs are part of a broader corporate de-risking strategy that often includes plan freezes, lump-sum buyouts, and terminations

The study documents that companies doing PRTs are dramatically more likely to:

Offer lump-sum windows

Freeze the DB plan

Terminate the plan entirely

This aligns with my argument that PRTs are not a one-off insurance procurement but a structural dismantling of the DB system—done without participant consent and without meaningful regulatory scrutiny. 22Paper

5. The paper inadvertently supports plaintiffs: PRTs produce a “one-time cost spike” and require full funding—meaning they are expensive unless the sponsor is highly motivated to escape risk

The authors find:

PRTs cause a major spike in pension expenses in the transfer year.

Sponsors must fully fund the liabilities and pay insurer markups.

This again refutes the idea that PRTs are participant-oriented prudence decisions.

A rational sponsor would only accept these costs if it perceives a private corporate benefit—not because the annuity is prudently selected for retirees.

**Conclusion:

Even in corporate-friendly academic research, PRTs are shown to raise systemic risk, weaken the PBGC, and be driven by corporate incentives—not participant protection**

The Klingler–Sundaresan–Moran paper is valuable because it:

Confirms that corporate incentives dominate, not ERISA prudence.

Demonstrates that PRTs increase systemic and pool risk.

Shows that safe sponsors offload liabilities to insurers of varying credit quality.

Documents that PRTs meaningfully shrink PBGC coverage.

For appellate judges, this should be a wake-up call: the economics profession itself views PRTs as risk-shifting devices that degrade system-wide protection, not as benign or “equivalent” replacements for DB pensions.

—————————————————————————————————

Appendix 2: The New O’Brien–Walters PBGC Analysis—Why Courts Are Wrong About PBGC Guarantees After PRTs

Our legal argument—that courts are ignoring material credit-risk evidence, CDS spreads, downgrade risks, and the absence of downgrade-trigger clauses—is strongly reinforced by these findings.

Source:“The Forgotten Promise: Why PBGC Retirement Benefit Guarantees Should Continue After Pension Risk Transfer Transactions,” Kevin O’Brien & Spencer Walters, Ivins, Phillips & Barker, Nov. 2025 https://www.ipbtax.com/PRT-PBGC-Guarantees

I. Overview and Relevance to PRT Litigation

A newly released white paper by nationally recognized ERISA attorneys Kevin P. O’Brien and Spencer F. Walters (Ivins, Phillips & Barker) provides the strongest statutory and historical argument to date that PBGC guarantees legally continue even after a pension plan executes a Pension Risk Transfer (PRT).

Their central conclusion is simple and explosive:

PBGC’s current position that its guarantees cease after a PRT is unsupported by statute, contradicted by PBGC’s own earlier interpretations, and inconsistent with both legislative history and IRS/ERISA regulatory structure.

This analysis directly undermines decades of judicial assumptions that PRT annuitants “lose PBGC protection,” and it creates new grounds for appeal in cases such as Konya v. Lockheed Martin, Doherty v. Bristol-Myers, and others.

Ironically, the O’Brien–Walters paper shows that both plaintiffs and defendants have been litigating on a false premise—that PBGC’s 1991 reversal is legally valid. The authors show it is not.

II. PBGC’s Original Rule (1981): PBGC Guarantees Continue After an Annuity Is Purchased

O’Brien and Walters highlight that PBGC’s original 1981 regulation and preamble explicitly promised that PBGC would guarantee annuity payments if an insurer failed:

“In the unlikely event that an insurance company should fail… the PBGC would provide the necessary benefits.” — PBGC Final Rule, 46 Fed. Reg. 9532 (Jan. 28, 1981)

IPB OBrien-Walters 2025 White P…

This destroys modern arguments claiming PBGC never intended to insure post-PRT annuity recipients.

The PBGC reversed itself only in 1991, with no statutory change and no Congressional authorization.

III. Statutory Text: ERISA §4022 Requires PBGC Guarantees to Continue

The authors make a powerful statutory argument:

ERISA §4022 guarantees “all nonforfeitable benefits… under a single-employer plan which terminates.”

A benefit paid through an annuity contract remains a benefit “under the plan,” because:

The annuity is pursuant to and arises out of the plan.

Treasury regulations for 415, 417, 401(a)(9), 411(d)(6), 402, 401(h) all treat annuity-contract payments as plan benefits.

PBGC itself argued in Lami v. PBGC (1989) that annuity payments are plan benefits for §4044 purposes.

Thus PBGC cannot claim that annuity payments are “under the plan” when reducing their own liability (as in Lami), but not “under the plan” when guaranteeing benefits.

This is the most devastating contradiction.

IV. Legislative History: Congress Refused PBGC’s Request to End Guarantees

In the mid-1980s, PBGC, worried about Executive Life and steel/airline failures, explicitly asked Congress to amend ERISA to remove PBGC responsibility for insurer insolvency.

Congress rejected that request.

1983 PBGC proposal: rejected

1985 Reagan Administration bill (H.R. 2995): rejected

1986 SEPPA amendments: Congress affirmed PBGC obligations continue after standard termination.

The paper cites the House Education & Labor Committee:

“A certification of close-out does not affect the PBGC’s obligations under Section 4022.”

Congress was crystal clear.

V. PBGC’s 1991 Reversal Was Purely an Administrative Power Grab

The PBGC had financial problems in the early 1990s and unilaterally reversed its position through regulatory reinterpretation.

It did so:

Without statutory authority

Without revising §4022

Ignoring its own 1981 rule

Ignoring Lami v. PBGC

Citing only a change in its “mission interpretation”

O’Brien & Walters note PBGC even admitted it had no internal legal analysis supporting the reversal.

In 2025, under Loper Bright, the PBGC’s 1991 policy receives zero Chevron deference and must be judged under Skidmore, where it fails every factor.

VI. Policy Argument: PBGC Should Be the Backstop, Not State Guaranty Associations

The paper argues that reversing PBGC coverage contradicts ERISA’s purpose:

PBGC was created as a federal guarantee program, not insurers.

State guaranty funds are:

inconsistent across states,

capped at extremely low levels,

funded only after insurer insolvency,

not designed for large plan failures.

Under the PBGC’s original model:

State insurance guaranty pays first

PBGC covers any shortfall

This layered approach was the explicit PBGC understanding in 1981.

VII. Implications for PRT Litigation

This analysis provides new ammunition for plaintiffs—and new exposure for defendants.

A. Standing

Courts in Konya and Doherty held that loss of PBGC protection = concrete injury. But if PBGC protection never legally disappears, then:

PRTs do not eliminate federal protection

Courts must recognize the PBGC guarantee as still in force

Claims of “no injury” or “mootness” by defendants collapse

B. Fiduciary Breach

Plan fiduciaries who rely on PBGC’s 1991 informal interpretation may be:

violating the statute,

ignoring legislative history,

failing to secure PBGC protections that legally exist.

C. Prohibited Transactions

If PBGC protections remain:

Fiduciaries cannot argue that PRT annuities are “safe substitutes”

Private insurers bear full credit risk—and PBGC’s guarantee is the only federal backstop

Offshore reinsurance, private credit exposures, and lack of downgrade clauses become more alarming

D. Appeals

Appellate courts now have:

statutory basis

regulatory history

unsuccessful Congressional repeal attempt

PBGC’s own contradictory positions

Loper Bright and Skidmore deference rules

This appendix strengthens every pending appeal.

VIII. How This Appendix Strengthens Our Thesis

Our original article argued that courts are ignoring:

insurer risk (CDS spreads)

offshore reinsurance exposure

lack of downgrade clauses

conflicts of interest

state guaranty inadequacy

The O’Brien–Walters paper adds an entirely new dimension:

PRTs may not actually divest PBGC protection at all. Courts have been relying on a legally wrong assumption.

This transforms PRT litigation.

IX. Conclusion: PBGC Guarantees Likely Still Apply—Courts Must Correct the Record

The O’Brien–Walters paper demonstrates:

PBGC’s 1991 reversal was unauthorized and inconsistent

ERISA’s statutory text supports ongoing PBGC protection

Legislative history confirms Congressional intent

Judicial dicta (e.g., Beck v. PACE) is not binding

Modern courts are applying an incorrect understanding of PBGC’s obligations

This appendix gives plaintiffs a powerful new argument in appeals and may shift the landscape of PRT litigation nationwide.

Appendix 3: The Hong v. Credit Suisse/UBS Case—A Fiduciary Test of Pension Risk Transfer Governance

The November 2025 correspondence from attorney Edward Stone on behalf of former Credit Suisse employee Victor Hong provides a detailed example of the fiduciary and transparency failures embedded in recent corporate Pension Risk Transfer (PRT) transactions HongUBSPrt.

1. False and Misleading Participant Communications

Mr. Hong’s December 2024 “Notice of Annuity Contract” claimed that the transfer of the Credit Suisse Employees’ Pension Plan to Nationwide Life Insurance Company would “not affect the value of his pension benefit.” As Stone’s letter notes, this representation was materially false because the transaction eliminated ERISA coverage and PBGC insurance protection, exposing participants to the sole credit risk of Nationwide and removing uniform fiduciary and reporting standards.

This pattern mirrors industry-wide conduct in which sponsors and insurers present PRTs as “neutral” conversions, when in fact participants lose statutory rights and transparency.

2. Loss of Diversification and Fiduciary Oversight

Before the PRT, Hong’s pension was backed by a diversified, ERISA-regulated portfolio subject to minimum-funding, reporting, and fiduciary standards. After the transfer, his claim rests entirely on Nationwide’s general-account credit. He no longer receives annual statements or protections tied to diversified trust assets—a risk shift analogous to replacing a diversified fund with a single corporate bond.

3. Key Due-Diligence Questions Ignored

Stone’s letter enumerates specific fiduciary-process inquiries that the plan administrators refused to answer:

Which insurers were solicited to bid?

What were the relative bid prices and credit-quality differentials?

Who served as the independent fiduciary charged with identifying the “safest available annuity” as required by ERISA 95-1?

Were credit-default-swap spreads or insurer solvency metrics evaluated?

What criteria and methodology were used to select Nationwide?

The absence of responses to these fundamental questions demonstrates a failure of prudence and loyalty. No evidence was provided that any independent fiduciary evaluated downgrade risk or insurer solvency.

4. UBS Response and Denial of Disclosure Obligations

UBS’s January 30, 2025 response explicitly declined to furnish nearly all requested information, asserting that ERISA §1024(b)(4) did not require disclosure beyond the basic plan document and an amendment authorizing the PRT. UBS refused to produce the annuity-provider bids, independent-fiduciary reports, or the executed contract—claiming the latter “has not yet been finalized.” This response highlights a regulatory blind spot: once a PRT is announced, participants are stripped of standing to demand fiduciary documentation, even though the transaction permanently alters their benefit security.

5. Legal and Systemic Implications

The Hong correspondence illustrates the same systemic issues identified in academic and policy analysis:

Material misrepresentation of “no change” in benefit value conceals the loss of federal insurance and oversight.

Opaque fiduciary selection processes prevent scrutiny of insurer risk or conflicts of interest.

Regulatory gap: once obligations are transferred, participants fall outside ERISA Title I enforcement and into fragmented state insurance regimes.

Together, these factors confirm that current judicial deference to PRTs ignores both factual and structural evidence of participant harm.

Expert Opinion Summary

The Hong case provides direct, documentary evidence that major financial institutions—now under UBS ownership—executed a PRT that (a) misrepresented participant protections, (b) failed to demonstrate independent fiduciary diligence, and (c) relied on narrow disclosure interpretations to avoid transparency. These practices substantiate the expert conclusion that PRTs violate ERISA’s fiduciary and anti-misrepresentation standards and exemplify why appellate courts must revisit lower-court assumptions that such transfers are risk-neutral.

I. Introduction — From “Gateway Drugs” to Hidden Crypto Exposure

Trump-era executive orders have again opened the 401(k) casino. Just as fixed and variable annuities were sold into plans under the false pretense of a DOL “safe harbor,” crypto now follows the same playbook—masked behind Target-Date Funds (TDFs) wrapped in State-regulated Collective Investment Trusts (CITs). These opaque, bank-trust vehicles avoid SEC registration and ERISA’s disclosure regime, giving Wall Street a new place to hide high-fee, high-risk bets.

II. How Crypto Becomes a Prohibited Transaction

Under ERISA §406(a)(1)(C) & (D), a plan engages in a prohibited transaction if a fiduciary causes the plan to furnish services or assets to, or engage in any transaction with, a party-in-interest— including the recordkeeper, trustee, or any affiliate. Once crypto exposure is embedded in a TDF or brokerage window managed by a plan’s own service provider, several triggers appear, including affiliate conflicts, spread profits, hidden placement within Target-Date CITs, and lack of a viable PTE.

III. The Valastro Framework — Fiduciary Void Meets Regulatory Capture

Valastro describes a “regulatory void” surrounding crypto in 401(k)s and a Trump administration “all-in on cryptocurrencies.” Her forthcoming analytical framework would extend fiduciary prudence standards to brokerage windows—precisely where crypto is now being funneled. Yet absent DOL enforcement, plan sponsors inherit full fiduciary liability when participants lose savings.

IV. Parallels to the Fixed-Annuity “Get-Out-of-Jail-Free Card”

As detailed in Trump’s Executive Order Is Not a Get-Out-of-Jail-Free Card (Aug 2025), insurers long claimed that any product blessed by State regulators or a DOL exemption is automatically ERISA-compliant. Crypto promoters now borrow that script—arguing that Executive Order 14330 “democratizes alternatives.” In reality, it merely shifts risk from issuers to participants while removing federal oversight.

V. Accounting Chaos — “Four Sets of Books” in Digital Form

In Four Sets of Books (Aug 2025) I showed how plan sponsors, insurers, and consultants each maintain separate ledgers—obscuring true returns. The same structure applies to crypto: Blockchain ledgers record token flows; custodians maintain off-chain balances; recordkeepers report synthetic daily values; and trustees book nominal “unit values.”

VI. Target-Date CITs as the Hidden Vector

Crypto exposure will likely surface inside default TDFs, buried within State-regulated CITs. Because participants rarely opt out of defaults, millions could be involuntarily exposed to crypto volatility—without prospectus, SEC registration, or clear ERISA bonding. That alone establishes both fiduciary imprudence and self-dealing.

VII. Fiduciary Implications and Enforcement Roadmap

The DOL retains power under §406 to challenge crypto inclusion as an imprudent plan investment. Plaintiffs can also plead that fiduciaries knowingly allowed party-in-interest transactions lacking valid exemptions.

VIII. Conclusion — Crypto as the Next ERISA Time Bomb

Crypto in retirement plans repeats every structural flaw of the annuity and private-equity experiments: opacity, conflicted service providers, and regulatory arbitrage. Valastro’s “Retirement Roulette” metaphor captures it perfectly—plan sponsors have turned workers’ savings into a spin of the digital wheel.

Add-On: Crypto in Brokerage Windows Is Still a Prohibited Transaction

I. Brokerage Windows—The Illusion of Fiduciary Escape

Professor Lauren K. Valastro’s Regulating Retirement Savings Roulette makes clear that the so-called self-directed brokerage window (SDBA) is no regulatory safe zone. She writes that “no agency or court has confirmed the existence of fiduciary duties relating to brokerage windows,” yet those windows are now the primary mechanism through which crypto enters 401(k)s. By allowing virtually unrestricted trading access inside an ERISA plan, sponsors and recordkeepers pretend that fiduciary obligations stop at the menu—but ERISA never permits abdication.

II. The Fidelity Crypto Pay-to-Play Model

Fidelity reportedly accepted hundreds of millions of dollars from crypto issuers and exchanges to gain shelf space on its brokerage-window platform. Such arrangements are indistinguishable from mutual-fund revenue-sharing schemes that courts have already deemed transactions for consideration with a party-in-interest. When a recordkeeper or trust platform receives direct or indirect compensation from a product provider whose assets are sold through the plan—even via SDBA—§406(a)(1)(C) and (D) apply.

III. Benchmarking Impossible = Fiduciary Imprudence

As Commonsense 401(k) reported in November 2024, crypto, private equity, and annuity contracts are impossible to benchmark. If a fiduciary cannot verify pricing, fees, or fair value, prudence and loyalty are violated. Valastro confirms this opacity “portends both increased costs and potential losses without legal safeguards.”

IV. Brokerage Windows Exposed by Crypto

In Commonsense 401(k)’s June 2022 piece “#401k Brokerage Windows Exposed by #Crypto,” it was predicted that open-architecture rhetoric would conceal profit-sharing deals. Crypto has turned SDBAs into fee-generating casinos, where recordkeepers win regardless of participant losses.

V. Why “Participant Choice” Doesn’t Cure a Prohibited Transaction

ERISA’s fiduciary duties run to the plan itself—not whichever participant clicks “buy.” Offering a conflicted feature is a breach. Valastro’s proposed framework—extending fiduciary review to brokerage-window design—confirms that participant direction is not a magic shield.

VI. Conclusion—The Hidden “Fifth Book”

Brokerage windows create a fifth set of books: unreported payments for platform access. In the crypto context, these off-balance-sheet incentives complete the circle of self-dealing. Whether crypto sits in a Target-Date CIT or a brokerage window, the result is identical under ERISA—an unbenchmarkable, conflicted, and inherently prohibited transaction.

Lauren K. Valastro, “Regulating Retirement Savings Roulette,” 63 San Diego L. Rev. (2026 forthcoming)

Appendix: Senator Warren’s 2026 Warning and the Emerging Risk of “Hidden Crypto” Inside CITs

Why this appendix matters

Since the publication of Crypto as a Prohibited Transaction in 401(k) Plans, the legal and regulatory landscape has deteriorated in precisely the direction fiduciaries should fear. Rather than strengthening ERISA protections, federal policy signals now point toward expanded access to crypto assets in retirement plans, coupled with weaker transparency and oversight.

1. Senator Warren places fiduciaries on formal notice

In her January 2026 letter, Sen. Warren warned that allowing crypto assets into retirement plans “endangers investors” due to:

Extreme volatility

Lack of transparent valuation

Absence of reliable methods to project future returns

Weak or nonexistent investor protections

Conflicts of interest at the highest political and industry levels

The letter explicitly references:

A 33% Bitcoin decline in six weeks, wiping out nearly $800 billion in market value

GAO findings that crypto assets have “uniquely high volatility” and no standard valuation framework

The Trump Administration’s Executive Order directing agencies to re-interpret ERISA’s definition of permissible plan assets to accommodate crypto

WarrenJan26lettertoseconcryptov…

For ERISA purposes, this letter matters because it eliminates any argument that fiduciaries lacked knowledge of crypto’s risks. After January 2026, ignorance is no defense.

2. The Executive Order accelerates prohibited-transaction risk

The August 2025 Executive Order cited by Sen. Warren directs DOL and the SEC to “reevaluate” ERISA guidance to permit alternative assets — including crypto — in 401(k) plans.

This directive does not create a statutory exemption under ERISA §406. Instead, it creates pressure on regulators to relax enforcement, shifting the burden to private litigants.

Critically:

An Executive Order cannot override ERISA’s prohibited-transaction statute

Any crypto exposure involving related parties, indirect compensation, revenue sharing, or affiliated service providers remains presumptively unlawful

Fiduciaries remain personally liable for prohibited transactions, regardless of political signals

This mirrors earlier regulatory failures involving annuities, proprietary funds, and private equity — all of which later became major litigation waves.

3. The next frontier: Crypto concealed inside CITs

Public debate has largely focused on direct crypto options and brokerage windows. That focus misses the more dangerous development: crypto exposure embedded inside Collective Investment Trusts (CITs), particularly in target-date CITs.

CITs present a uniquely dangerous combination:

No SEC registration

Limited public disclosure

No prospectus

Opaque valuation methodologies

Broad latitude to hold derivatives, tokens, or blockchain-linked instruments

As documented in your December 2025 analysis of target-date CIT corruption, CIT structures allow asset managers to bury high-risk exposures several layers down, beyond participant visibility and often beyond sponsor understanding.

Crypto exposure can enter CITs through:

Tokenized “private credit” instruments

Blockchain-based derivatives

Crypto-linked notes

Offshore vehicles held by the trust

“Alternative sleeve” allocations inside target-date CITs

Participants may never see the word “crypto” — yet still bear its full volatility.

4. Why hidden crypto in CITs is an ERISA violation

Embedding crypto inside CITs triggers multiple ERISA violations simultaneously:

A. Prohibited transactions (§406(a) and §406(b)) If the CIT manager or affiliate:

Sponsors the trust

Serves as recordkeeper or adviser

Receives indirect compensation tied to assets

…then crypto exposure inside the CIT constitutes a per se prohibited transaction, regardless of performance.

B. Failure of disclosure ERISA requires fiduciaries to understand and disclose material risks. Crypto exposure hidden inside a CIT:

Defeats meaningful participant disclosure

Prevents informed consent

Violates fiduciary duty even absent losses

C. Imprudent concentration of uncompensated risk Crypto introduces:

Extreme volatility

Correlated drawdowns

Valuation gaps

Liquidity mismatches

When embedded in a default investment (QDIA), these risks are imposed on participants without choice — a direct violation of ERISA’s core protective purpose.

5. Senator Warren’s letter strengthens future litigation

For plaintiff attorneys, Sen. Warren’s letter is not merely political commentary. It is evidence:

Evidence that crypto risk was well-documented

Evidence that volatility and valuation problems were widely known

Evidence that fiduciaries were warned before allowing crypto exposure

Courts have repeatedly held that fiduciary breach claims are strengthened when defendants ignored contemporaneous warnings from regulators, legislators, or oversight bodies.

This letter will be cited in:

Motions opposing dismissal

Discovery disputes

Expert reports

Trial records

6. The broader pattern: Regulatory retreat, litigation advance

Crypto follows a familiar pattern:

Regulators signal permissiveness

Industry exploits structural loopholes

Risks are hidden, not eliminated

Losses materialize

Litigation becomes the primary enforcement mechanism

CITs are the perfect vehicle for Step 3.

Fiduciaries who believe crypto exposure is “allowed” because it is indirect, pooled, or rebranded are repeating the same errors made with:

Proprietary mutual funds

General account annuities

Private equity in target-date funds

Those errors proved costly.

Conclusion

Sen. Warren’s January 2026 letter removes all ambiguity. Crypto is volatile, opaque, and unsuitable for retirement plans — particularly when concealed inside nontransparent structures like CITs.

Fiduciaries who permit crypto exposure — directly or indirectly — now do so with full notice of the risk and full exposure to ERISA liability.

For regulators, this appendix is a warning. For fiduciaries, it is a last chance. For plaintiff attorneys, it is a roadmap.

When fiduciaries breach their duties under ERISA, the core question becomes: how do you calculate the loss? Every excessive-fee or imprudent-investment case boils down to one formula: what participants actually earned vs. what they should have earned under a prudent alternative. In other words, fiduciary damages in 401(k) plans are counterfactual—they measure what the plan would have earned “but for” the breach.

Recent academic and legal work—from Alex Bailey’s Allocating the Burden of Proving Loss-Causation in ERISA Fiduciary Litigation (Ill. L. Rev. 2023) to Vahick Yedgarian’s Quantitative Analysis of Damages in ERISA Fiduciary Breach Litigation (IAU 2024)—provides the structure for a more consistent approach to calculating damages. When applied to fixed annuities and stable-value products, these methods show how insurers’ spread-based profits translate directly into quantifiable losses for plan participants.

II. The Legal Foundation: Breach, Loss, and Causation

ERISA §409(a) makes fiduciaries personally liable to “make good to the plan any losses.” Courts universally require proof of three elements: breach, loss, and causation. Once breach and loss are shown, many appellate courts shift the burden to the fiduciary to prove the loss was not caused by the breach, consistent with trust-law fairness.

III. The Economic Foundation: Quantitative Models of Damages

Vahick Yedgarian and Ram Paudel show that ERISA damages are quantitative, not theoretical. Courts rely on four main financial models:

1. Fee-Differential Model – Excess administrative fees compounded over time. 2. Benchmark Comparison – Difference between prudent index return and actual fund performance. 3. Credit-Spread Model – Difference between insurer portfolio yield and credited rate. 4. Per-Participant Benchmark – Difference between charged vs. market median fees for similar plans.

Each builds a counterfactual: what would have happened had the fiduciary acted prudently.

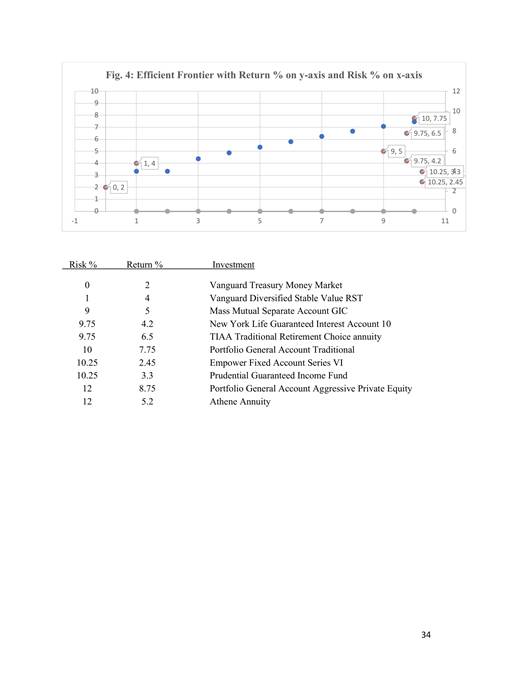

IV. Fixed Annuities and the Stable Value Efficient Frontier

In Safe Annuity Retirement Products and a Possible U.S. Retirement Crisis (Lambert & Tobe, 2024), insurer-issued fixed and general-account annuities sit below the efficient frontier for retirement-plan investments—low return, high risk, and hidden spread profits. If an insurer credits 2% while benchmarks yield 4%, participants lose 200 bps per year—20% over a decade.

Each year’s shortfall accumulates into recoverable loss under ERISA §409(a).

V. Disclosure Failures Compound the Damage

Peter Wiedenbeck’s Inconceivable? – Understandable ERISA Disclosures (2025) argues plan disclosures have become incomprehensible legal boilerplate. This opacity hides spread profits and excessive fees. Wiedenbeck calls for standardized, Truth-in-Lending-style disclosures so participants can see the real yield vs. credited rate.

VI. Procedural Barriers: Twombly, Iqbal, and the Locked Courthouse Door

Lauren Valastro’s How Misapplying Twombly Erodes Retirement Funds (2024) shows that courts’ “probability pleading” standards block many excessive-fee claims before discovery. Her data show high appellate reversal rates, confirming that well-defined benchmarks like the Stable Value Efficient Frontier are essential to surviving dismissal.

VII. The Unified Damages Framework

Bailey (2023): shifts burden of proof to fiduciary once breach and loss shown. Yedgarian & Paudel (2024): quantitative financial models for fees and performance. Wiedenbeck (2025): exposure of opaque disclosures masking losses. Valastro (2024): procedural obstacles and benchmarks. Tobe & Lambert (2024): efficient frontier as risk-return fiduciary standard.

VIII. Visualization: The Stable-Value Efficient Frontier

IX. Conclusion: Turning Fiduciary Breaches into Quantified Justice

Fiduciary imprudence causes measurable economic harm. Using quantitative models and the Stable Value Efficient Frontier, participants and experts can finally demonstrate the gap between credited rates and prudent benchmarks as both a prohibited transaction and a quantifiable loss. ERISA provides the remedy; the math provides the proof.

References

1. Alex Bailey, Allocating the Burden of Proving Loss-Causation in ERISA Fiduciary Litigation, 2023 U. Ill. L. Rev. 991.

2. Vahick A. Yedgarian & Ram Paudel, Quantitative Analysis of Damages in ERISA Fiduciary Breach Litigation, Int’l Am. Univ. (2024).

3. Peter J. Wiedenbeck, Inconceivable? – Understandable ERISA Disclosures, Elder L.J. (2025 forthcoming).

4. Lauren K. Valastro, How Misapplying Twombly Erodes Retirement Funds, U. Colo. L. Rev. (2024).

5. Thomas E. Lambert & Christopher B. Tobe, “Safe” Annuity Retirement Products and a Possible U.S. Retirement Crisis, Journal of Economic Issues (2024).

Overview: When a plan fiduciary offers a higher-cost mutual fund share class when a lower-cost, identical (or materially equivalent) institutional or omnibus share class was available, the damage for plan participants is the incremental cost paid (via higher expense ratio) compounded over time, against the counterfactual of the lower-cost class.

Legal basis:

Tussey v. ABB, Inc. (W.D. Mo. Mar. 31, 2012) held that the fiduciary breached duties by selecting higher-expense share classes when cheaper equivalent classes were available. McGuireWoods

The statutory driver is ERISA § 409(a) (fiduciary liable for “any losses to the plan resulting from” each breach).

Calculation steps:

Identify the challenged share class and available lower-cost share class (same fund strategy, same manager, same underlying portfolio).

Determine the annual expense ratio differential:

For each relevant year t, estimate the plan assets invested in that fund share class at the beginning (or average) of year t: .

Annual cost differential = .

Accumulate (compound) or actuarially discount (depending on approach) the series of annual cost differentials over the damage period to .

Where is an appropriate discount or benchmark rate.

Optionally, subtract any rebates or offset credits actually returned to the plan.

Example: Suppose a plan had $100 million in Fund X higher-cost share class in 2015, with and .

.

Annual cost differential for 2015 = $100 m × 0.0030 = $300 000.

If the balance grew or if multiple years apply, you compound accordingly.

Key issues:

Ensuring true “equivalent” share class (investment strategy, manager, performance net of fees).

Selecting appropriate benchmark growth rate or discount rate.

Addressing offsets or rebates.

Properly measuring plan assets in that share class over time.

Demonstrating causation — that the fiduciary had access to the lower-cost share class or reasonably should have.

B. Performance-Related Damages

Overview: Fiduciary breach via imprudent investment selection or monitoring can cause performance “shortfalls” relative to a prudent alternative benchmark. The damage is measured as the difference between what participants actually earned and what they would have earned under the counterfactual prudent portfolio.

The academic piece “Calculating damages in ERISA litigation” details methodology for this type of loss. SSRN

Calculation steps:

Define the actual investment option(s) and their historical net-of-expense returns by year: .

Define the counterfactual prudent benchmark return by year: . (E.g., a comparable index or peer group median.)

For each year t, identify the plan assets invested in that option at the beginning (or average): .

Shortfall in year t:

Aggregate over the period, compounding or discounting as appropriate:

Adjust for offsetting factors (e.g., subsequent recovery of performance, contributions/withdrawals dynamics).

Example: A fund underperformed the index by 1% per annum over $50 million invested for 5 years.

Year 1 shortfall = 0.01 × $50m = $500k, Year 2 based on new beginning balance etc., compound accordingly.

Over five years the cumulative loss may approximate $500k × 5 = $2.5m, plus compounding.

Key issues:

Selecting a proper benchmark (risk-adjusted, identical asset class).

Handling participant flows, asset timing, and reallocation during the period.

Ensuring causation: that the underperformance was caused by fiduciary breach (e.g., imprudent due-diligence, failure to remove under-performing options).

Avoiding hindsight bias: ERISA requires a prudent process, not a “perfect” outcome. Encore Fiduciary

C. Record-Keeping and Service Vendor Damages

Overview: Fiduciary breach regarding service provider arrangements (record-keeping, vendor fees, revenue sharing) can lead to overpayment by plan participants. The damage equals the excess fees paid (“but for” more reasonable arrangements) compounded over time.

Legal basis:

The duty of prudence includes monitoring vendor compensation, fee reasonableness, benchmarking. ErisA Practice Center+1

Courts have held such arrangements can lead to recoverable losses under ERISA §409(a).

Calculation steps:

Determine the actual per‐participant recordkeeping/service fee paid each year: .

Estimate a reasonable per-participant fee for comparable services: (based on market comparators).

Multiply by participant counts or total participants with accounts (P_t):

Alternatively, calculate total plan assets × excess basis, if fees are asset-based rather than per-participant.

Aggregate/compound across years:

Adjust for rebates, credits, or other offsets (e.g., revenue-sharing offsets returned to plan).

Example: Suppose recordkeeper charged $80 per participant in year 1, market reasonable is $50. With 1,000 participants: excess fee = ($80-$50)×1,000 = $30,000 for year 1. Repeat for subsequent years, accounting for growth or changes.

Key issues:

Establishing a credible “reasonable” fee benchmark for the same service scope and plan size.

Timing and participant counts (fee base change).

Demonstrating causation: that fiduciary failed to monitor/benchmark, board approved unreasonable fees.

Recognizing that not every higher vendor fee constitutes loss—fiduciary might show value for higher cost.

D. Fixed Annuity / General-Account Insurance Product Damages (e.g., comparing to higher-return products such as TIAA Real Estate Account)

Overview: When a plan offers a fixed annuity or stable-value product with a credited rate materially below what similarly prudent investments or alternatives would have yielded, the difference can be shown as a shortfall. This is especially relevant where the insurer retains spread (i.e., difference between portfolio return and credited rate) and the fiduciary fails to evaluate that spread or alternatives.

Determine actual credited rate of the fixed annuity product each year: .

Determine the benchmark return of a prudent alternative portfolio (e.g., similarly safe investment, index of general-account portfolios, or a real-estate heavy strategy such as TIAA Real Estate). Call it .

Estimate the asset amount invested in the fixed annuity each year: .

Annual shortfall = .

Aggregate/compound across years:

Consider offsets (e.g., surrender charges, liquidity constraints, risk profile differences) and assess prudence of offering alternatives.

Example: If the fixed annuity credited 2 % in a given year, while a prudent alternative returned 4 %, the shortfall is 2 % on the invested assets. If $20 million was invested: shortfall = $400k that year. Over multiple years with compounding = significant.

Key issues:

Justifying selection of the “alternative” return (must reflect comparable risk/liquidity constraints).

Accounting for liquidity, benefit-design features (fixed annuity may offer certain protections others do not).

Demonstration that fiduciary failed to evaluate comparative returns or disclose spread.

Establishing that the plan could have taken the alternative and that participants were harmed.

E. Disgorgement in Prohibited Transaction Cases

Overview: When a fiduciary engages in a transaction prohibited under ERISA §406 that benefits a party in interest (or pays an unreasonable fee to a party in interest), the remedy may include disgorgement of profits made by that party or return of the excess benefit to the plan.

Legal basis:

ERISA § 502(a)(2) allows recovery of “equitable relief” on behalf of the plan.

Prohibited transactions under § 406(a) and (b) trigger § 409 fiduciary liability for losses plus disgorgement where appropriate.

Courts have treated disgorgement as separate from but complementary to compensatory damages.

Calculation approach:

Identify the prohibited transaction (e.g., a revenue-sharing arrangement with a party in interest, a cross-subsidization).

Quantify the benefit retained by the party in interest (e.g., excess spread, underwriting margin, “kick-back” revenue). Call it per year.

Determine the time period that the profit was retained without offset to the plan.

Disgorgement amount = , optionally compounded as appropriate.

If the plan itself also suffered measurable losses (as in prior sections), the remedy may include both compensatory damages and disgorgement of the profit to the plan.

Example: If a recordkeeper retained $500k each year for five years via revenue sharing from mutual funds, absent offset rebates to the plan, the disgorgement claim may sum $2.5 m.

Key issues:

Demonstrating the party in interest was enriched and that the plan was deprived of the benefit.

Ensuring that the disgorgement does not constitute a punitive damage but rather restitution to the plan (ERISA prohibits punitive damages). Finseca

Aligning timing, accounting for offsets, and documenting causation.

F. Forfeiture Damages / Forfeiture Account Misuse

Overview: Forfeiture accounts—unvested participant balances forfeited upon termination—must be used in a manner consistent with plan terms and fiduciary duties (e.g., to reduce employer contributions or plan expenses). Misuse or failure to allocate forfeitures may give rise to losses to the plan or participants.

Calculation concept:

Quantify the total forfeitures that should have been applied to plan expenses or employer match offset but were instead used incorrectly or retained by another party: each year.

Determine the lost benefit to participants or the plan (e.g., higher plan expense load, lower employer contributions).

Aggregate over the relevant period; apply compounding/discounting as appropriate.

If applicable, combine with other damage types (fee or performance losses) that resulted because of the misuse.

Example: If $200k in forfeitures was collected each year but not used to offset plan expenses, and the plan instead charged participants that $200k in higher net fees, then each year the damage equals $200k (or more if compounding).

Key issues:

Plan document must clearly state permitted use of forfeiture.

Demonstration of actual misuse and link to participant harm.

Participant flows and allocation complexity (some participants leave before litigation settlement).

Summary Table of Damage Types

Damage Type

Primary Metric

Counterfactual Benchmark

Key Data Inputs

Share-Class Excess Fee

Expense Ratio Differential × Assets

Lower-cost identical share class cost

Actual ER, Benchmark ER, Assets by share class

Performance Shortfall

(Benchmark Return – Actual) × Assets

Passive or peer-group index return

Actual returns, Benchmark returns, Assets

Recordkeeping / Vendor Excess Fee

(Actual Fee – Reasonable Fee) × N

Market reasonable fee per participant or asset basis

ERISA draws a bright line: plan fiduciaries must act solely for participants, and must not engage in conflicted deals. The “bright line” lives in ERISA §406 (prohibited transactions). Over time, industry lobbyists have piled up exemptions (statutory §408 and DOL PTEs) and talking points like: “Sure, everything could be a PT… but there’s an exemption for that.” The trick is: exemptions are conditional (necessity, reasonableness, disclosures, impartial conduct, etc.). If the conditions aren’t satisfied, it’s still a prohibited transaction—and plaintiffs don’t have to pre-plead the absence of an exemption. That’s now black-letter law after Cunningham v. Cornell (U.S. Supreme Court, Apr. 17, 2025). kutakrock.com+3Supreme Court+3Ropes & Gray+3

“Who polices PTs?”—the Siedle moment

Edward “Ted” Siedle told me a story from a mid-2000s DOL training in Norman, Oklahoma: DOL staff asked who polices prohibited transactions. He said, “You do.” They reportedly answered they were told it “wasn’t their job.” I didn’t find a public record of that training, but Siedle’s contemporaneous critique appears in a 2009 post (“DOL Still AWOL”), blasting the Department for green-lighting conflicted arrangements via exemptions and inaction—language that matches what many of us have seen in the field. Bogleheads

Why Cunningham v. Cornell changes the temperature

The Supreme Court held that §408 exemptions are affirmative defenses. To state a §406(a)(1)(C) PT claim, a participant need only plausibly allege (1) a fiduciary caused a transaction; (2) the transaction furnished services/products; (3) with a party-in-interest. The defense must then prove an exemption (e.g., necessary services for no more than reasonable compensation). That means “we’re exempt” is not a pleading shield; it’s a burden the defense must carry—with facts. Supreme Court+2Groom Law Group+2

Where the conflicts hide (investments and recordkeeping)

1) Recordkeeping & platform arrangements

What the rule says: If a fiduciary causes the plan to buy services from a party-in-interest (the recordkeeper is one), it’s a §406(a) PT unless an exemption fits—typically §408(b)(2): “necessary services” and “no more than reasonable compensation.”

Why this bites: After Cunningham, plaintiffs don’t need to front-plead reasonableness. They can allege: “plan hired party-in-interest for recordkeeping,” and the case proceeds to discovery on actual compensation, share classes, revenue-sharing, float, managed-account cross-selling, etc. Multiple courts and client alerts are already flagging the lower pleading bar. Supreme Court+1

What changed: For years, the industry leaned on PTE 84-24 to shoehorn insurance commissions and annuity sales into ERISA plans. In 2016, DOL tightened 84-24—excluding variable and fixed-indexed annuities from the easy path and pushing them into stricter conditions (then a “best-interest contract” framework). Even with later rule churn, the Federal Register record shows DOL’s rationale: these products are complex, conflict-heavy, and need rigorous conditions if sold at all. Federal Register+1 Bottom line: If a dual-registered advisor/recordkeeper steers a plan into an insurer’s general account, separate account, or annuity sleeve and they’re capturing commissions, revenue share, or spread profits, you have a textbook §406(b) self-dealing risk unless an exemption (strictly) fits—rare in practice. I write about this in more detail at https://commonsense401kproject.com/2025/11/01/annuities-are-a-prohibited-transaction-dol-exemptions-do-not-work/

3) Private equity/credit, real assets, crypto—often via CIT wrappers

“Everything’s a PT” (industry line) vs. how exemptions really work

Two widely cited pro-industry takes are now circulating:

Doran (2025) argues Cunningham over-reads §406(a)(1)(C), complaining it would outlaw ordinary services unless §408(b)(2) is read into the claim itself. But that’s exactly what the Supreme Court rejected: exemptions are affirmative defenses. The statute’s structure—§406 prohibitions / §408 exemptions—controls. The practical upshot isn’t to ban recordkeeping; it’s to force fiduciaries to prove services are necessary and compensation reasonable. That’s healthy discipline, not “outlawing the ordinary.”

Oringer & Rabitz (2023/24) present the sophisticated, markets-friendly view of ERISA practice, emphasizing how lawyers help “run the ERISA gauntlet” so plans can access advanced strategies. Fair—but that sophistication doesn’t erase §406(b) self-dealing or §406(a) party-in-interest payments. If a structure pays affiliates, layers platform fees, or hides spread profits, you’re back in PT land unless the exemption conditions are met—with evidence.

For balance, consumer-leaning analysis on fiduciary standards (including how DOL’s ESG detours were used to chill scrutiny) underscores that ERISA’s lodestar remains exclusive benefit, prudence, and loyalty—and that PT prohibitions are the teeth behind those duties.

And if you want the long view, David Pratt’s classic treatments of fiduciary/“investment advice” rulemakings show why so many “ordinary” sales models were always dancing on the edge of ERISA’s prohibited-transaction cliff.

Appendix – Key Practitioner Quotes & Authorities

A. Practitioner Q&A Insights (Theado & Naegele, Wickens Herzer Panza)

“404(c)… is an affirmative defense… sponsors still have retained fiduciary duties… including prudent selection and monitoring of the plan’s investment alternatives.” — Theado & Naegele, Litigating an Employee Benefit Claim (Part 2), p. 5.

“The fiduciary must avoid a participant or trustee investment that could result in a prohibited transaction… even if you qualify under §404(c).” — Ibid. p. 5.

“If the 3(38) fiduciary does a really lousy job, then plan officials and 3(21) fiduciaries will ultimately be held responsible because they selected the adviser and failed to properly monitor those activities.” — Theado & Naegele, Can You Really Avoid ‘Fiduciary Liability’? (Part 2), left column.

“Service agreements that say ‘we are not taking responsibility’ or include hold-harmless clauses are not dispositive of fiduciary status.” — Ibid., right column.

Defined Contribution (DC) plans—primarily 401(k)s and 403(b)s—now hold over $12 trillion in assets and have become the dominant way Americans save for retirement. Within these plans, Target Date Funds (TDFs) are the default investment option for most participants (QDIA). Increasingly, TDFs are being housed in Collective Investment Trusts (CITs) rather than SEC-registered mutual funds.

While many large financial firms market CITs as “institutional” or “low cost,” the truth, as Professor Natalya Shnitser (Boston College Law School) has documented, is that CITs operate in a poorly regulated gray zone. Her 2023 paper, Overtaking Mutual Funds: The Hidden Rise and Risk of Collective Investment Trusts, demonstrates how this parallel financial system has emerged largely outside of federal securities law, relying on weak or uneven state banking oversight that leaves participants vulnerable to undisclosed conflicts and high-risk investments. In May 2023, SEC chair Gary Gensler sounded the alarms on CITs:

Rules for these funds lack limits on illiquid investments and minimum levels of liquid assets. There is no limit on leverage, [nor any] requirement for regular reporting on holdings to investors…”.

The Department of Labor’s EBSA has largely abdicated enforcement of investment-related fiduciary issues due to resource constraints and political pressure. Consequently, private litigation under ERISA has become the key mechanism for accountability. Under Cunningham v. Cornell, arrangements that embed undisclosed conflicts of interest can be litigated as Prohibited Transactions under ERISA §406, placing the burden of proof on the fiduciary to demonstrate that an exemption applies.

TDFs held in state-regulated CITs are therefore emerging as one of the most dangerous and least transparent areas in the retirement system.

II. The Regulatory Gap: State Trust Oversight and Hidden Alternatives

Shnitser’s analysis makes clear that while some CITs are administered by national banks subject to OCC oversight, many others are state-chartered trusts subject to fragmented and permissive regulation. These state agencies often lack capital markets expertise, do not require audited disclosures, and impose no meaningful restrictions on portfolio composition.

This weakness has allowed some CITs to quietly include or prepare to include assets that would be illegal or impractical in SEC-registered mutual funds, including:

Private equity and private credit

Illiquid real estate partnerships

Annuity or general-account insurance contracts

Cryptocurrency or blockchain-linked investments

Once these assets are admitted under state trust law, participants lose key protections of the Investment Company Act of 1940—including daily liquidity, mark-to-market valuation, and public reporting.

Even industry-cited CITs—such as those from Vanguard, Fidelity, or T. Rowe Price—may hold only transparent securities today, but the absence of federal oversight means that they could add higher-risk alternatives in the future without participant consent or public disclosure.

III. Fiduciary Exposure: Why This Creates a Prohibited Transaction Risk

Under ERISA §406(a) and (b), a fiduciary commits a Prohibited Transaction when plan assets are used for the benefit of a “party in interest,” or when the fiduciary engages in self-dealing or acts in a conflict of interest. Target date funds as default options (QDIA) have an even higher level of fiduciary exposure.

CIT structures create multiple layers of potential conflicts:

Affiliated Fiduciary Self-Dealing – Many recordkeepers (e.g., TIAA, Prudential, Principal) both manage and distribute their own CITs. The plan fiduciary’s choice of an affiliated or revenue-sharing CIT is a per se conflict unless it qualifies for an exemption.

Opaque Valuation and Fee Flows – Hidden sub-advisory, insurance, and wrap fees are common in hybrid CITs. Without SEC filings, participants and plan sponsors cannot verify total expenses or profit spreads.

Commingling with Proprietary Insurance or Private Assets – When a CIT invests in an insurer’s general or separate account, plan assets are effectively transferred for the benefit of that insurer—a clear §406(b) violation.

As Cunningham v. Cornell established, once a plaintiff demonstrates the existence of a conflict, the burden shifts to the fiduciary to prove that the transaction was both reasonable and exempted by law. In the CIT context, that burden is nearly impossible to meet given the lack of transparency.

IV. The “Four Sets of Books” Problem

In a 2025 Commonsense401kProject article, “Four Sets of Books: How Trump’s 401(k) Push Opens the Door to Accounting Chaos,” the CIT TDF structure was shown to embed four separate accounting layers:

Trust-level accounting – the CIT’s aggregate book, typically opaque.

Sub-advisor books – alternative and private asset managers reporting unaudited valuations.

Insurance affiliate accounts – general or separate account structures blending spread-based returns.

Recordkeeper wrap or platform fees – compensation hidden in layered service agreements.

Each layer can obscure the true cost and risk exposure of plan assets, creating ideal conditions for spread extraction, kickbacks, or prohibited self-dealing.

V. Industry Narrative vs. Reality

Industry lobbyists and even members of the DOL Advisory Council have claimed that CITs are “federally regulated” under the OCC and therefore safe. Shnitser’s research, and my July 2024 testimony before the DOL Advisory Committee, dismantle that narrative. In fact:

Many CITs are not OCC-regulated at all—they are state-chartered and subject only to weak local trust-law review.

The DOL’s Advisory Opinion 2025-04A effectively greenlighted insurers and private-equity firms to use these permissive CIT vehicles to circumvent ERISA’s prohibited-transaction protections.

“A Multi-Billion Dollar Gift to the Private Equity and Insurance Industry,” Sept. 24, 2025), these weak frameworks are already being exploited.

VI. Litigation and Enforcement Outlook

Litigators and whistleblowers can use Shnitser’s work as the academic and empirical foundation for a new generation of ERISA claims targeting state-regulated CITs. Key claims include:

Failure of prudence (§404) – Using opaque state-regulated CITs when transparent mutual funds are available.

Prohibited Transaction (§406) – Affiliated, self-dealing, or revenue-sharing arrangements in proprietary CITs.

Failure to monitor (§405) – Trustees’ inaction in the face of known regulatory gaps.

As with Cunningham v. Cornell, plaintiffs need only show the existence of conflicted structures; the defense must then justify them. Given the opacity of CITs, many fiduciaries will be unable to meet that burden.

VIII. Conclusion

Natalya Shnitser’s scholarship provides the intellectual and evidentiary backbone for understanding why state-regulated CITs threaten the fiduciary integrity of the U.S. retirement system. Combined with field evidence from the Commonsense401kProject, it shows that CIT-based TDFs have become the next frontier of prohibited-transaction litigation.

While some CITs—like those from Vanguard or Fidelity—may temporarily resemble their mutual-fund counterparts, the weak state controls allow hidden, illiquid, or high-risk alternatives to be introduced later.

When that happens, participants’ savings will be exposed to the same structural dangers—spread extraction, valuation manipulation, and self-dealing—that ERISA was designed to prevent. Expanding Shnitser’s framework and demanding transparency for CIT TDFs is not just good policy; it is essential fiduciary protection.

Under ERISA §406, any transaction between a plan and a “party in interest” — such as the plan’s insurer, recordkeeper, or trustee — is per se prohibited. That includes the purchase or maintenance of a fixed annuity contract from an insurer that profits from spreads, affiliated services, or undisclosed compensation.

The insurance industry routinely claims that these annuity deals qualify for a Department of Labor “Prohibited Transaction Exemption” (PTE), such as PTE 84-24 or PTE 2020-02. But in decades of reviewing contracts and filings, I have never seen a single annuity that could actually pass the exemption test.

Each PTE requires that:

Compensation be reasonable and disclosed;

The transaction be in the best interest of participants; and

No misleading statements be made.

Annuities fail on all three. They hide 100–150 basis points of spread profits; they trap plan assets with no downgrade or exit provisions; and their “guarantees” transfer risk from the plan sponsor to participants — all while enriching the insurer.

Even if an annuity could theoretically meet those tests — say, if it included a downgrade clause, full fee disclosure, and liquidity — the burden of proof would still rest with the fiduciary. The Second Circuit’s 2025 decision in Cunningham v. Cornell University clarified that once a prohibited transaction is alleged, it is the plan sponsor’s burden to prove an exemption applies.

In practical terms:

Every fixed annuity is a prohibited transaction by default.

The plan fiduciary must prove — not assume — that an exemption is valid.

And in the real world, the insurance industry’s own opacity ensures they cannot meet that test.

The DOL’s “comfort letters” and outdated exemptions were drafted for a different era. In today’s world of offshore reinsurance, undisclosed spreads, and absent downgrade clauses, annuity exemptions are fiction. Fiduciaries relying on them are gambling with participants’ retirement security — and their own liability.

Appendix November 25, 2025

In the current 4 ongoing cases of fixed annuities as Prohibited Transactions filed since Cunningham V. Cornell, the defense is primarily trying to delay since in my opinion I think they know they have no valid legal defense.

Finally at the end of November a Motion to Dismiss came out that was full of deflections and noise and nothing of substance.

In the entire 27-page Motion to dismiss brief, plan:

❌ Never invokes §408

❌ Never claims PTE 84-24 applies

❌ Never claims §408(b)(2) applies

❌ Never argues the annuity contract is exempt under any DOL rule

❌ Never argues Annuities spread is “reasonable compensation”

❌ Never claims the plan assets are not being used for the insurer’s benefit