Introduction

For decades, insurers have promoted annuities as “safe” retirement products—whether offered inside 401(k) plans, 403(b) plans, or used in large pension risk transfer (PRT) deals. But recent developments suggest insurers themselves are eroding the transparency and prudence standards that fiduciaries must meet under ERISA. By lobbying for secrecy, suppressing solvency disclosures, and hiding their spread profits, insurers are virtually ensuring that plaintiffs’ attorneys will argue these contracts amount to prohibited transactions under ERISA §406.

This article builds on my earlier work:

1. Annuities as Prohibited Transactions via ChatGPT¹

2. Annuities Flunk Prohibited Transaction Exemptions²

3. Diversification Abandoned: Why Fiduciaries Must Rethink Fixed Annuities and PRTs³

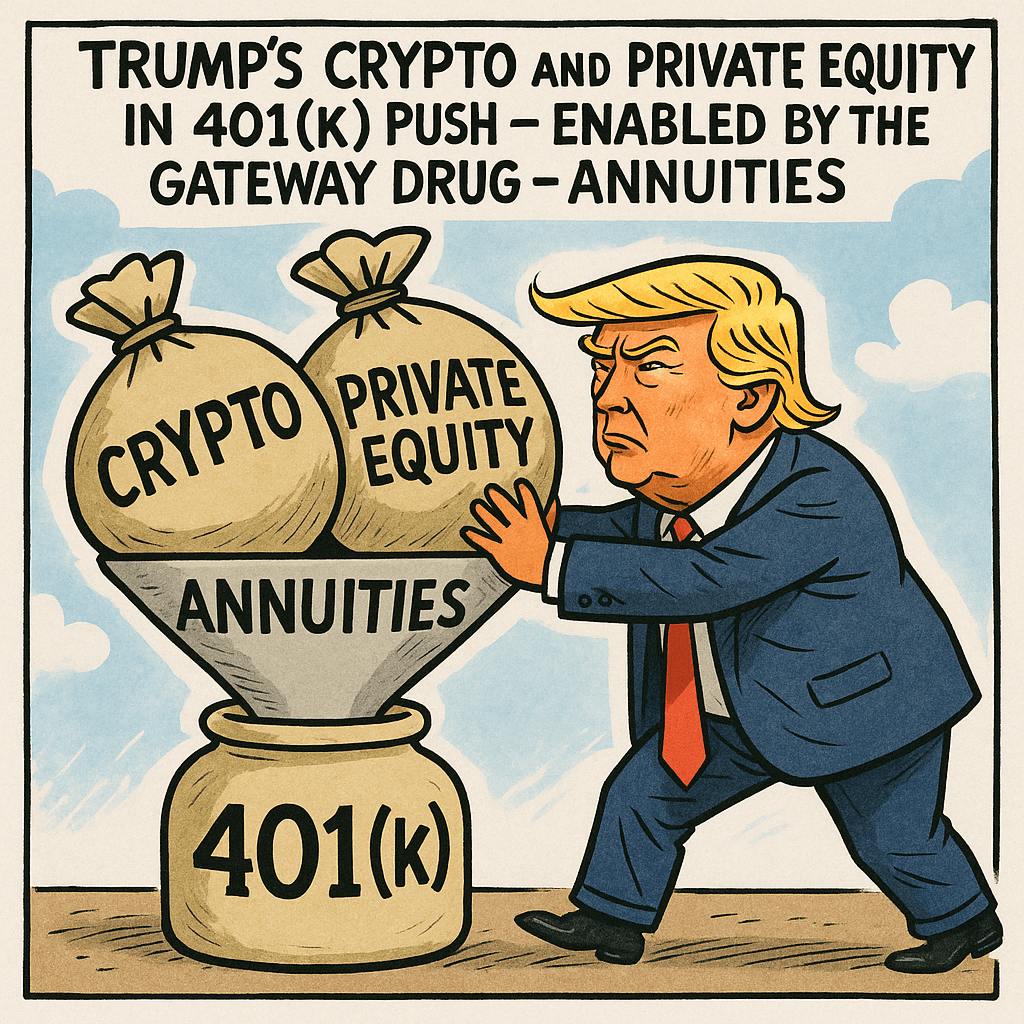

4. Four Sets of Books: How Trump’s 401(k) Push Opens the Door to Accounting Chaos⁴

5. State Guarantee Associations Behind Annuities Are a Joke⁵

6. PRT Annuities Should Be Prohibited Unless Sponsors Prove Prudence⁶

I. Secrecy Around Prudential and New Jersey Insurers

A researcher recently noticed that quarterly statutory filings of Prudential (domiciled in New Jersey) are not available on S&P Capital IQ. Why? Because New Jersey Statute 17-23-1 makes quarterly statements confidential: “Quarterly statements shall be confidential and shall not be subject to public inspection…”⁷

This means one of the largest providers of PRT annuities in the country shields crucial solvency data from plan sponsors, fiduciaries, participants, and even researchers. Fiduciaries relying on Prudential annuities cannot access the same information they would demand of any mutual fund or bank counterparty.

II. NAIC’s Push to Hide Risk-Based Capital Scores

The National Association of Insurance Commissioners (NAIC) is now moving to extend this secrecy nationwide. In a 2025 proposal (p.56 of NAIC CADTF meeting packet⁸), regulators suggest prohibiting any public reporting or dissemination of an insurer’s Risk-Based Capital (RBC) ratio. The Society of Actuaries has opposed this move, warning that transparency is essential.

III. The Spread Profits Problem

As I detailed in ‘Four Sets of Books’⁴, insurers earn vast hidden profits by crediting plan participants only 2–3% while investing their general accounts at 6–8%. Unlike asset managers who must disclose fees, insurers keep their “spread” opaque. Cases like Cunningham v. Cornell University suggest courts will increasingly demand disclosure of how insurers make their money. Refusals to disclose will support claims of prohibited transactions.

IV. Why This Matters for 401(k) and PRT Litigation

Fixed annuities and guaranteed investment accounts offered inside 401(k)s are increasingly challenged as prohibited transactions, especially when recordkeepers steer participants into affiliated insurance products. The secrecy around solvency metrics compounds the fiduciary risk.

In Pension Risk Transfers, when a plan sponsor transfers billions in obligations to a single insurer, the current rule fiduciaries must prove the annuity provider is financially strong. (I believe that this rule could be challenged since even a strong annuity provider may not live up to Imprudent Conduct Standards) If solvency data is withheld, plaintiffs can argue that fiduciaries could not have satisfied their duty to monitor and therefore, engaged in a prohibited transaction.

V. The Coming Litigation Wave

With insurers lobbying to suppress information, fiduciaries are left in an impossible position. Courts will not accept “we couldn’t get the data” as a defense. Instead, lack of transparency will be framed as evidence that annuities:

1. Fail ERISA’s prudence standard.

2. Trigger prohibited transaction rules.

Conclusion

By suppressing solvency disclosures, hiding spread profits, and lobbying for even greater secrecy, insurers are accelerating their own downfall in the courts. What once passed as prudence will now be reframed as prohibited self-dealing. Fiduciaries who continue to use annuities—whether in 401(k)s or PRTs—without demanding full transparency may soon find themselves on the losing end of ERISA litigation.

Footnotes

¹ https://commonsense401kproject.com/2025/06/13/annuities-are-prohibited-transactions-via-chat-gpt/

² https://commonsense401kproject.com/2025/05/10/annuities-flunk-prohibited-transactions-exemption-scotus-ruling-will-open-floodgates-of-litigation/

³ https://commonsense401kproject.com/2025/07/27/diversification-abandoned-why-plan-fiduciaries-must-rethink-fixed-annuities-and-pension-risk-transfers/

⁴ https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/

⁵ https://commonsense401kproject.com/2025/06/24/state-guarantee-associations-behind-annuities-are-a-joke/

⁶ https://commonsense401kproject.com/2024/12/17/pension-risk-transfer-annuities-should-be-prohibited-the-burden-of-proof-is-on-plan-sponsors-to-justify-that-they-are-prudent/

⁷ N.J. Stat. §17-23-1.

⁸ NAIC, Capital Adequacy Task Force, Special National Meeting Packet (2025), p.56.

Andy Barr’s Financial Industry Backers

Andy Barr’s Financial Industry Backers Apollo Global Management

Apollo Global Management JPMorgan Chase & Co.

JPMorgan Chase & Co. The Epstein Backdrop

The Epstein Backdrop