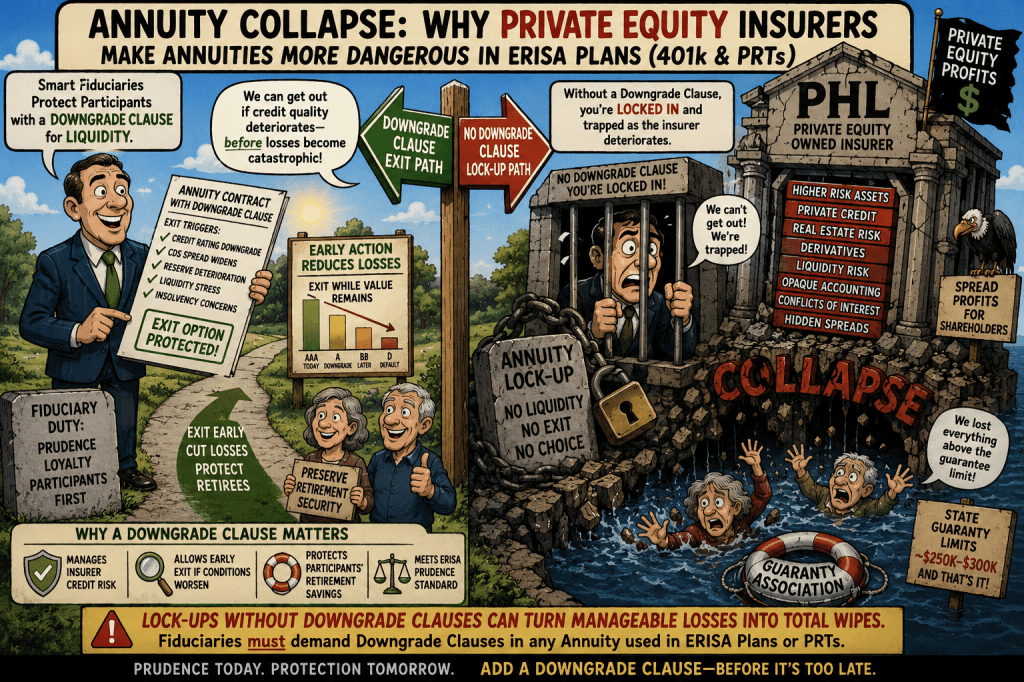

The collapse of PHL Variable Insurance Company and the new litigation against LPL Financial provide one of the clearest modern examples of why insurer-issued annuity products represent a growing and poorly understood danger inside retirement plans.

According to the newly filed complaint, the alleged harm was not that the underlying separate account investments suddenly disappeared. Rather, policyholders allegedly lost the ability to access, surrender, exchange, or reposition their retirement assets once Phoenix entered rehabilitation.

As attorney Adam Gana explained:

“The issue is not whether the underlying separate account investments disappeared. According to the complaint, the harm stems from policyholders losing the ability to access, surrender, exchange, or otherwise reposition their assets once PHL entered rehabilitation.”

That distinction is critically important for ERISA litigation involving fixed annuities and insurer general account and separate account products in 401(k) and 403(b) plans. It also covers lifetime income annuities and Pension Risk Transfer (PRT) annuities in ERISA Defined Benefit Plans.

For years, insurers and some plan consultants have marketed general account fixed annuities as “stable value” or “capital preservation” investments. But the Phoenix collapse again demonstrates that policyholders are not simply investing in a conservative bond portfolio. They are becoming unsecured creditors of a leveraged insurance company whose liabilities can become frozen during periods of financial distress.

This is precisely the type of liquidity and counterparty risk that synthetic stable value structures were designed to reduce.

Unlike insurer general account annuities, diversified synthetic stable value structures generally separate the fixed income portfolio from the wrap provider’s balance sheet. If one wrap provider weakens or fails, plans can often replace the wrap provider while maintaining participant ownership of the underlying assets.

In contrast, insurer general account annuities typically trap participants inside the insurer’s balance sheet itself. Once the insurer enters rehabilitation or experiences severe financial stress, participants can lose practical access to their money even if the underlying investments continue to exist.

The Phoenix litigation also highlights a major structural problem with insurer-issued fixed annuities in 401(k) plans: most contain no meaningful downgrade protection clauses.

In institutional synthetic stable value contracts, downgrades are accommodated with step-up clauses. A typical synthetic stable value CIT like the Vanguard RST may have 6 diversified wrappers. If the credit quality of one wrap provider deteriorates below specified levels, there are contractural provisions that the other 5 wrappers step up and take the coverage allocation of the downgraded wrapper. Vanguard RST successfully did this with AIG in 2007 before the bailout was certain, and would have had little effect even if the government had let AIG collapse.

But many insurer-issued fixed annuities in 401(k) plans contain no comparable participant protections. Plans remain trapped even after significant credit deterioration in what I have called a death spiral.

The complaint against LPL alleges that Phoenix annuities were no longer recommended after ratings downgrades and other warning signs emerged following the 2008 financial crisis, yet existing policyholders allegedly were not warned about the insurer’s deteriorating financial condition.

That allegation directly parallels one of the central fiduciary concerns now emerging in ERISA prohibited transaction litigation involving fixed annuities:

If insurers, consultants, or recordkeepers understood the growing credit risks associated with insurer balance sheets, why were retirement plan participants not given meaningful liquidity protections or downgrade escape rights?

The issue becomes even more troubling in employer retirement plans because participants often have no practical ability to negotiate terms, review insurer solvency risk, or monitor complex insurance company balance sheets.

In many 401(k) plans, the insurer is simultaneously:

the product manufacturer,

the credit counterparty,

the spread-profit recipient,

and frequently a party in interest to the plan.

That structure creates precisely the kind of conflicted transaction ERISA’s prohibited transaction rules were designed to scrutinize.

The Department of Labor’s historical exemptions for insurance company general account products were largely built around assumptions that insurers were highly regulated, conservatively capitalized, and operationally stable. But the modern insurance industry increasingly relies on:

private credit,

structured finance,

derivatives,

affiliated asset managers,

offshore reinsurance,

and opaque valuation practices.

The Phoenix collapse demonstrates that these are not hypothetical concerns.

Even when “market losses” do not immediately appear in participant statements, policyholders can still suffer catastrophic harm through the loss of liquidity, surrender rights, transfer rights, and control over retirement assets.

That reality fundamentally weakens the common defense argument that insurer-issued annuities are “safe because participants never lost principal.”

Loss of liquidity itself can constitute enormous economic harm.

For ERISA fiduciaries, the key question is no longer simply whether an insurer can maintain book-value accounting during normal conditions. The question is whether participants are being exposed to uncompensated insurer-credit and liquidity risks without adequate contractual protections.

The Phoenix litigation may become one of the strongest modern real-world examples supporting the argument that insurer general account annuities are fundamentally different from diversified stable value structures — and that many plans failed to adequately evaluate those differences.

It also strengthens the broader argument that insurer-issued fixed annuities in 401(k) plans deserve heightened scrutiny under ERISA’s prohibited transaction framework, particularly where:

no downgrade clauses exist,

no independent market valuation exists,

participants cannot freely exit,

insurers profit from spread capture,

and affiliated parties control multiple sides of the transaction.

For years, the insurance industry has argued that these products are safer because they avoid mark-to-market volatility.

Phoenix demonstrates the opposite reality:

Sometimes the greatest risk is not volatility. It is discovering that your retirement assets are locked inside a failing insurer when you need them most.

A Common Sense Framework for 401(k), 403(b), CIT, and Target-Date Fund Fiduciaries

Introduction

Private equity and other private-market investments are increasingly being pushed into participant-directed retirement plans through target-date funds, CITs, interval funds, evergreen vehicles, and semi-liquid wrappers. Fiduciaries are often told these products provide “diversification,” “institutional access,” and “enhanced returns.”

However, private equity products differ fundamentally from traditional mutual funds and public securities. They involve limited transparency, subjective valuation, conditional liquidity, complex fee structures, leverage, and performance reporting methodologies that are often not comparable to public-market investments.

Oxford Professor Ludovic Phalippou recently warned the Department of Labor that “asset neutrality should not mean metric neutrality, disclosure neutrality, or governance neutrality.”https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6847259

This checklist is designed to help ERISA fiduciaries identify hidden risks, conflicts, prohibited transaction concerns, and misleading performance claims before adding private-market exposure to participant-directed retirement plans.

I. Performance Measurement & Benchmarking

□ 1. Avoid reliance on IRR as the primary performance metric

Internal Rate of Return (“IRR”) is not equivalent to mutual fund or index returns and does not measure investor wealth compounding. IRR is heavily influenced by cash-flow timing, subscription lines, early exits, dividend recapitalizations, and leverage.

Professor Phalippou notes that private equity firms such as KKR and Apollo have reported remarkably stable since-inception IRRs for decades, despite radically different market conditions, demonstrating how IRR can become mathematically “sticky” rather than economically meaningful.

Fiduciary Questions

Is IRR being compared directly to public market annualized returns?

Is IRR being used to justify superiority over index funds?

Are subscription credit lines artificially inflating IRR?

Is the fiduciary receiving actual cash-flow-based investor outcome analysis?

□ 2. Require Public Market Equivalent (PME) analysis

Fiduciaries should require cash-flow-based PME benchmarking rather than marketing-based IRR comparisons.

PME analysis should:

Be specified ex ante

Match geography, leverage, sector, currency, and risk

Be net of all fees and expenses

Compare against realistic investable alternatives

Fiduciary Questions

Was the benchmark selected before evaluating performance?

Is the benchmark investable and liquid?

Does the benchmark reflect similar leverage and sector exposure?

Is the comparison apples-to-apples?

□ 3. Compare the entire target-date product—not merely the private sleeve

Private equity allocations are frequently embedded inside target-date funds, collective investment trusts, or multi-layered structures.

The relevant fiduciary question is not:

“Did the private sleeve outperform?”

The relevant question is:

“Did the total participant product improve expected participant outcomes after all fees, liquidity limits, valuation risk, leverage, and complexity?”

Fiduciary Questions

Would a simple public-market implementation likely achieve similar outcomes?

Is the private sleeve adding measurable participant value after all costs?

Is volatility being artificially suppressed through stale or subjective valuations?

II. Fee Transparency & Hidden Compensation

□ 4. Require consolidated all-in fee disclosure

Private equity fees frequently extend far beyond “2 and 20.”

Potential hidden costs include:

Portfolio-company monitoring fees

Transaction fees

Financing fees

Broken-deal expenses

Advisory fees

Platform fees

Subscription-line costs

Distribution compensation

Affiliate payments

Feeder fund expenses

Consulting and placement fees

Professor Phalippou emphasizes that “knowing fees are 2%-20%-8% does not convey the actual economic burden.”

Fiduciary Questions

What percentage of gross investment gain is ultimately retained by participants?

Are affiliate payments fully disclosed?

Are portfolio-company fees rebated or retained?

Is compensation flowing to parties in interest?

□ 5. Examine revenue-sharing and platform conflicts

Private-market products often generate indirect compensation to:

Recordkeepers

Consultants

OCIO providers

Target-date managers

Placement agents

Wealth platforms

CIT trustees

Fiduciary Questions

Does any service provider receive compensation tied to private-market allocations?

Are fiduciaries receiving fully transparent compensation reports?

Are private-market products steering participants toward higher-fee structures?

III. Valuation, NAV, and Fair Pricing

□ 6. Scrutinize NAV-based pricing mechanisms

Many semi-liquid and evergreen structures use Net Asset Value (“NAV”) as:

Subscription pricing

Redemption pricing

Fee calculation basis

Performance reporting basis

This creates substantial conflicts when valuations are subjective.

Professor Phalippou notes that investors may subscribe or redeem at prices materially disconnected from actual market-clearing values.

Fiduciary Questions

Are secondary market discounts materially below stated NAV?

Who determines the NAV?

Can the manager influence valuation inputs?

Are stale marks suppressing volatility?

□ 7. Evaluate continuation funds and affiliated transactions

Continuation vehicles, GP-led secondaries, and cross-fund sales create inherent conflicts where the manager may influence both price and process.

Fiduciary Questions

Are fairness opinions truly independent?

Does the manager control both sides of the transaction?

Are participants effectively buying marked-up assets from affiliated entities?

IV. Liquidity & Stress Testing

□ 8. Conduct stress-based liquidity analysis

Quarterly liquidity windows, gates, redemption caps, and side pockets may function normally during stable markets but fail during stressed conditions.

Fiduciary Questions

What occurs during mass participant withdrawals?

What happens if public markets decline sharply?

How would the product behave during a plan termination or sponsor bankruptcy?

Could remaining participants become trapped in illiquid assets?

□ 9. Analyze first-mover advantage risk

Semi-liquid structures may reward early redeemers while leaving remaining participants with concentrated illiquid exposure.

Fiduciary Questions

Are liquid assets sold first during redemption stress?

Does the portfolio become progressively riskier after withdrawals?

Could later participants bear disproportionate valuation losses?

V. Complexity & Governance Risk

□ 10. Treat complexity itself as a fiduciary risk factor

Complexity is not merely operational—it can conceal:

Hidden fees

Affiliate conflicts

Leverage

Valuation manipulation

Benchmark gaming

Illiquidity

Risk concentration

Fiduciary Questions

Can participants reasonably understand the structure?

Can fiduciaries independently evaluate the underlying holdings?

Does complexity benefit participants—or intermediaries?

□ 11. Investigate consultant and adviser conflicts

Professor Phalippou specifically warns that adviser reliance should not substitute for fiduciary judgment.

□ 13. Evaluate whether “availability” is being sold rather than prudence

Higher-fee products are often justified based on “access” or “institutional availability,” even where comparable public-market exposure exists at dramatically lower cost and greater transparency.

Fiduciary Questions

Is private-market exposure truly necessary?

Would public-market alternatives likely provide similar participant outcomes?

Is illiquidity being confused with sophistication?

VII. Common Sense Participant Protection Questions

Before adding private equity exposure, fiduciaries should ask:

Would I fully explain this structure to participants in plain English?

Could participants independently verify valuation and performance claims?

Could participants easily understand total fees?

Would the product remain attractive if fully transparent?

Is the structure designed primarily for participant benefit—or intermediary profit extraction?

Conclusion

Private equity is not automatically prudent or imprudent under ERISA. But private-market products require significantly greater scrutiny because they involve:

subjective valuation,

conditional liquidity,

opaque fee structures,

benchmark manipulation risk,

leverage,

and substantial conflicts of interest.

As Professor Ludovic Phalippou recently warned the Department of Labor, fiduciaries must distinguish “asset neutrality” from “metric neutrality, disclosure neutrality, and governance neutrality.”

ERISA fiduciaries should not treat private-market products as ordinary mutual funds merely because they are packaged inside a target-date fund, CIT, or retirement wrapper.

Retirement savers deserve transparent pricing, meaningful benchmarking, stress-tested liquidity, fair valuation practices, and fully disclosed conflicts before their retirement savings are exposed to private-market risk.

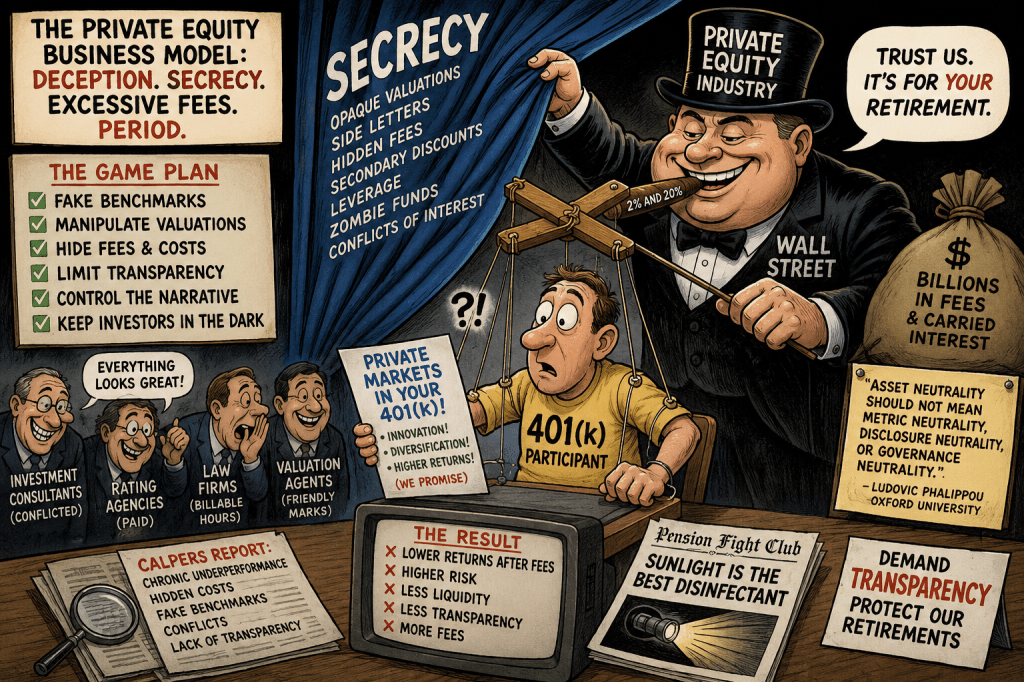

The private equity industry does not merely prefer secrecy. It requires secrecy.

Without opaque valuations, manipulated benchmarks, hidden fees, and misleading performance metrics, the industry’s excessive fee structure could not survive in a competitive marketplace.

That is the uncomfortable truth at the center of the Department of Labor’s proposal to open 401(k) plans to private equity products. And after reviewing more than 40,000 public comments submitted to the DOL, none stands out more than the analysis submitted by Professor Ludovic Phalippou of Oxford University — arguably the world’s leading academic expert on private equity performance and valuation.

The industry’s defenders talk endlessly about “innovation,” “access,” and “democratization.” Ludo talks about math.

As Phalippou explains in his formal DOL submission, the private equity industry’s favorite performance metric — Internal Rate of Return (IRR) — is not actually a measure of investor wealth compounding at all. It is a discount-rate formula that can be heavily manipulated through timing, subscription lines, dividend recaps, and cash-flow engineering.

In plain English: private equity markets returns in a way that would never be tolerated in public mutual funds.

Phalippou demolishes the fantasy using the industry’s own numbers.

KKR has reported roughly 26% since-inception IRRs for almost twenty years straight. Apollo has reported approximately 39% since-inception private equity IRRs for decades. If those numbers reflected actual investor wealth compounding, Apollo’s original funds would theoretically be worth sums approaching the GDP of the United States.

That is not investing. That is marketing arithmetic.

Phalippou’s central point is simple but devastating:

“Asset neutrality should not mean metric neutrality, disclosure neutrality, or governance neutrality.”

The private equity industry survives because it is allowed to compare apples to oranges while charging exponentially higher fees than transparent public markets.

And that deception is spreading.

The Entire Business Model Depends on Preventing Transparency

If private equity managers were forced to:

disclose all fees like SEC mutual funds,

use public-market-equivalent benchmarks,

fully report portfolio-company fees,

mark assets honestly,

disclose secondary-sale discounts,

reveal side letters,

and compare performance against low-cost index funds,

the economics of the industry would collapse.

That is why transparency itself has become the industry’s existential threat.

The recently released independent forensic CalPERS investigation highlights exactly how this system operates inside the nation’s largest public pension.

The report documents:

chronic underperformance,

hidden and understated investment costs,

fake “custom” benchmarks,

consultant conflicts,

opaque valuations,

zombie private-equity funds,

and aggressive resistance to transparency.

The report’s findings are extraordinary because CalPERS is not some small fringe pension.

against low-cost public alternatives, the illusion breaks down.

The Industry Knows Transparency Is the Real Threat

The most revealing quote in the entire CalPERS investigation may be this statement from CalPERS CEO Marcie Frost on CNBC:

“CalPERS is not sharing the limited partnership agreements. CalPERS is not sharing any side letters… We are extremely transparent… But frankly, private markets are private for a reason…”

That single sentence captures the entire private-equity model.

Private markets are “private” because transparency threatens fees.

The secrecy protects:

side-letter arrangements,

valuation games,

portfolio-company fees,

subscription-line engineering,

fee layering,

secondary-sale discounts,

political relationships,

and benchmark manipulation.

The industry cannot tolerate sunlight because sunlight would expose how much of private equity’s reported “alpha” comes from:

stale marks,

leverage,

fee extraction,

and benchmark engineering.

“Pension Fight Club” Exposes the Fear

The movie Pension Fight Club captures something the industry desperately wants to avoid: ordinary retirees beginning to ask questions.

The film repeatedly focuses on:

secrecy,

intimidation,

missing records,

hidden fees,

consultant conflicts,

and retaliation against pension critics.

One recurring theme is that pension beneficiaries are treated as adversaries once they demand transparency. Free trailer at https://pensionfightclub.com/ low fee for full movie.

That aligns perfectly with the findings of the CalPERS investigation, which documented coordinated efforts by pension officials and industry allies to undermine participant scrutiny and participant-funded investigations.

The message from the industry is clear:

Participants may fund the system. But they are not supposed to understand the system.

The DOL’s Proposed Rule Is a Gift to Wall Street

The DOL claims its proposal is “asset neutral.”

But there is no such thing as neutrality when one side:

As Phalippou warns, allowing private equity into participant-directed retirement plans without strict disclosure and benchmarking rules does not reduce risk.

It merely transfers the risk to retirement savers.

The irony is overwhelming.

ERISA imposed strict disclosure rules on mutual funds precisely because regulators recognized that retirement savers could not evaluate opaque products.

Now the DOL proposes opening 401(k)s to products far more opaque than anything ERISA originally allowed.

This is not modernization.

It is deregulation for Wall Street’s most secretive and highest-fee industry.

The Core Problem Is Not Complexity — It Is Incentives

Private equity defenders constantly argue that critics simply “do not understand” sophisticated investments.

That is false.

The issue is not complexity.

The issue is incentives.

The industry earns dramatically higher fees when:

valuations are opaque,

benchmarks are fictional,

costs are hidden,

and comparisons are impossible.

Transparency threatens the economics of the business itself.

That is why private equity fights:

public records requests,

disclosure reform,

benchmark standardization,

independent valuation review,

and participant oversight.

If private equity truly delivered superior risk-adjusted returns after all fees and expenses, transparency would help the industry.

Instead, the industry treats transparency as an existential danger.

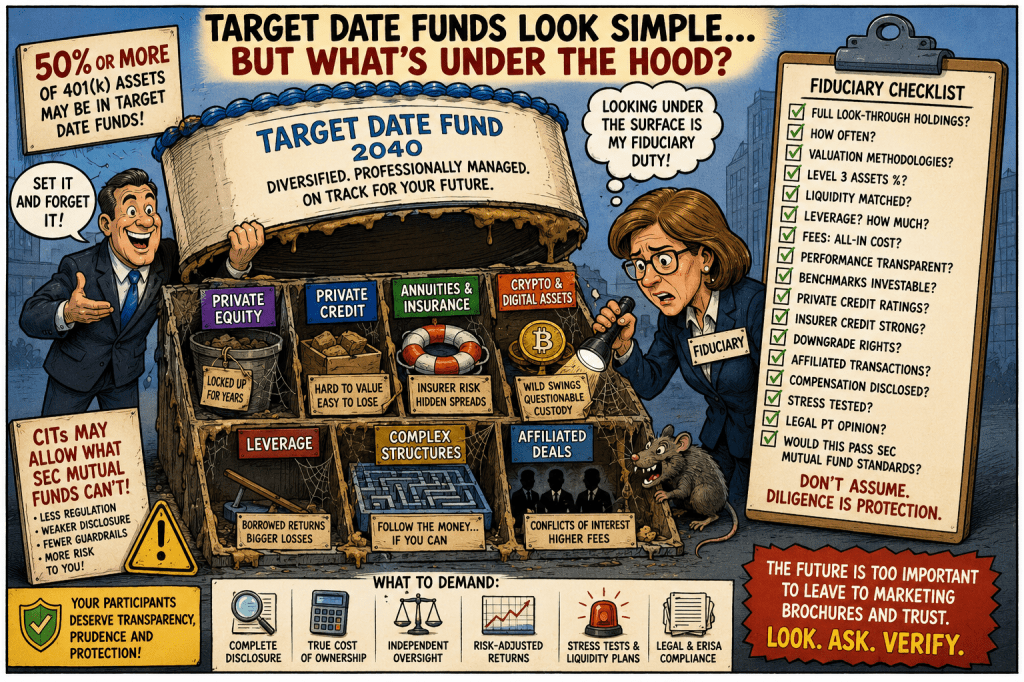

Looking “Under the Hood” of CIT-Based Target Date Funds

Core Fiduciary Principle

Target Date Funds (“TDFs”) frequently comprise 50% or more of total 401(k) assets and often serve as the plan’s Qualified Default Investment Alternative (“QDIA”).

but each underlying investment component individually.

Historically, most Target Date Funds operated within SEC-registered mutual funds, where:

accounting standards,

valuation rules,

leverage restrictions,

liquidity requirements,

performance reporting,

and fee disclosure obligations provided meaningful investor protections.

However, increasingly, Target Date Funds are being moved into weakly regulated state-bank Collective Investment Trusts (“CITs”), where fiduciaries may encounter:

hidden leverage,

opaque valuation methodologies,

affiliated transactions,

undisclosed spread compensation,

private credit,

private equity,

insurance products,

crypto exposure,

and other difficult-to-value assets that historically were restricted, impractical, or prohibited within SEC mutual funds.

The fiduciary obligation therefore requires substantially enhanced due diligence.

I. TARGET DATE FUND STRUCTURE REVIEW

A. Vehicle Structure

Questions

Is the TDF:

SEC mutual fund,

CIT,

insurance separate account,

managed account,

or hybrid structure?

Who regulates the structure?

Is the CIT overseen by:

OCC,

state banking regulator,

or trust company?

Key Concern

State-bank CITs may operate under materially weaker disclosure and transparency requirements than SEC mutual funds.

B. Underlying Holdings Transparency

Questions

Are complete underlying holdings disclosed?

How frequently?

Daily?

Quarterly?

Annually?

Is “look-through” transparency available for all underlying vehicles?

Red Flags

“Proprietary confidential holdings”

Delayed reporting

Aggregated or vague asset descriptions

Refusal to disclose private holdings

II. UNDERLYING ASSET CLASS REVIEW

A. Private Equity Exposure

Questions

Does the TDF contain:

private equity,

venture capital,

co-investments,

secondary funds,

continuation vehicles?

Required Due Diligence

PME benchmarking

IRR vs. time-weighted return comparison

Fee layering analysis

Capital call liquidity modeling

Valuation methodology review

Key Questions

Are valuations independently verified?

Are assets Level 3?

Are marks controlled by the manager?

Are continuation funds used to avoid losses?

Red Flags

Non-investable benchmarks

IRR-only reporting

Missing public market comparisons

Hidden carried interest

Subscription credit lines

B. Private Credit Exposure

Questions

Does the TDF contain:

direct lending,

private debt,

BDC exposure,

CLOs,

NAV loans,

structured credit,

mezzanine lending?

Required Due Diligence

Default stress testing

Recovery analysis

Liquidity modeling

Mark-to-market methodology review

Critical Questions

Who rates the underlying private credit?

Moody’s?

S&P?

Fitch?

KBRA?

internal models?

Egan-Jones?

Are ratings investment grade only because of weak methodologies?

Red Flags

Level 3 pricing

Internal marks

Illiquid side pockets

Affiliated originations

Weak independent valuation

C. Annuity / Insurance Exposure

Questions

Does the TDF contain:

fixed annuities,

guaranteed income products,

synthetic wraps,

insurance separate accounts,

guaranteed minimum withdrawal products?

Required Due Diligence

Insurer CDS spreads

Credit ratings

State insurance regulator review

Downgrade clause analysis

Spread compensation disclosure

General Account asset review

Critical Questions

Is there a downgrade termination clause?

What percentage of General Account assets are:

Treasuries,

private credit,

commercial real estate,

structured products?

Is the insurer privately owned by private equity?

Red Flags

No liquidity rights

Book-value-only accounting

No mark-to-market transparency

Captive reinsurance

Hidden spread compensation

D. Crypto / Digital Asset Exposure

Questions

Is there direct or indirect crypto exposure?

Through:

ETFs,

venture funds,

tokenized assets,

miners,

stablecoins,

exchanges,

private blockchain vehicles?

Required Due Diligence

Custody review

Valuation review

Counterparty review

Liquidity analysis

Regulatory status review

Red Flags

Offshore custodians

Unregulated exchanges

Token valuation opacity

Leverage

Staking arrangements

III. ACCOUNTING AND VALUATION REVIEW

A. Mark-to-Market Transparency

Questions

Which assets are:

Level 1,

Level 2,

Level 3?

What percentage relies on:

models,

appraisals,

manager discretion?

Key Concern

CITs may create “stale NAV” problems where risk is materially understated.

B. Performance Benchmarking

Questions

Are benchmarks:

investable,

transparent,

independently calculated?

Red Flags

CPI-plus benchmarks

Custom blended benchmarks

Self-created benchmarks

Non-public benchmark methodologies

Required Analysis

Compare:

actual returns,

volatility,

drawdowns,

Sharpe ratios, against:

low-cost public index alternatives.

C. Smoothing and Return Manipulation

Questions

Are valuations artificially smoothed?

Does the TDF show unusually low volatility inconsistent with underlying risks?

Red Flags

“Too smooth” performance

Reduced reported volatility from appraisal-based assets

Infrequent pricing

IV. LIQUIDITY AND REDEMPTION RISK

A. Liquidity Mismatch

Questions

Can daily participant liquidity be supported if:

underlying assets are multi-year illiquid investments?

Key Concern

401(k) participants may have daily liquidity rights while underlying assets may require:

years to liquidate,

lockups,

gates,

or side pockets.

B. Suspension Rights

Questions

Can:

withdrawals,

transfers,

exchanges,

or redemptions be suspended?

Red Flags

Gate provisions

Market stress restrictions

Delayed NAV processing

V. FEES, SPREADS, AND CONFLICTS

A. Layered Fees

Questions

Are there:

management fees,

performance fees,

carried interest,

wrap fees,

consulting fees,

sub-advisory fees,

recordkeeping revenue sharing?

Required Analysis

Calculate:

total look-through cost,

all indirect compensation,

embedded spread compensation.

B. Proprietary Product Conflicts

Questions

Are underlying investments:

proprietary,

affiliated,

revenue-sharing arrangements,

or tied to recordkeeper compensation?

Red Flags

Proprietary CITs

Affiliated private funds

Captive insurance products

Shelf-space payments

VI. REGULATORY AND LEGAL REVIEW

A. SEC vs. CIT Protections

Questions

Which SEC protections are absent because the TDF operates as a CIT?

Important Areas

Performance fee restrictions

Liquidity rules

Independent board oversight

Valuation controls

Public disclosure standards

B. ERISA Prohibited Transaction Analysis

Required Question

Has independent ERISA counsel issued a written legal opinion explaining:

why the TDF structure does not involve prohibited transactions,

why all compensation is reasonable,

and why affiliated arrangements comply with ERISA §§406(a) and 406(b)?

Special Concern

Underlying:

annuities,

proprietary private credit,

insurance products,

and affiliated private funds may create hidden party-in-interest conflicts.

VII. STRESS TESTING

Required Scenario Analysis

Stress Events

30% private credit markdown

commercial real estate collapse

insurer downgrade

liquidity freeze

crypto crash

redemption run

private equity write-downs

Questions

What happens to:

participant balances,

liquidity,

transfer rights,

NAV calculations,

and fiduciary exposure?

VIII. CORE FIDUCIARY QUESTIONS

Fiduciaries Should Ask:

Transparency

Can we fully explain every major underlying investment?

Liquidity

Are participants promised daily liquidity backed by illiquid assets?

Valuation

Are assets genuinely marked to market?

Compensation

Is hidden spread or affiliated compensation present?

Benchmarking

Are returns genuinely superior after all fees and risks?

Prudence

Would these investments survive SEC mutual fund scrutiny?

IX. DOCUMENTATION REQUIREMENTS

Committee Files Should Include

Full look-through holdings

Asset class risk memoranda

Independent valuation reviews

Benchmark comparisons

Liquidity stress tests

Prohibited Transaction legal opinions

Fee and spread analyses

CDS and insurer reviews

Regulatory assessments

X. CENTRAL FIDUCIARY WARNING

The movement of Target Date Funds from SEC mutual funds into opaque CIT structures may permit inclusion of:

hidden leverage,

private credit,

private equity,

annuities,

crypto exposure,

and difficult-to-value assets that historically faced meaningful SEC constraints.

Because TDFs frequently represent the majority of participant retirement assets, fiduciaries must analyze each underlying component investment individually — not merely rely on the Target Date Fund label, branding, or consultant assurances.

The fiduciary duty is not to trust the surface level fund.

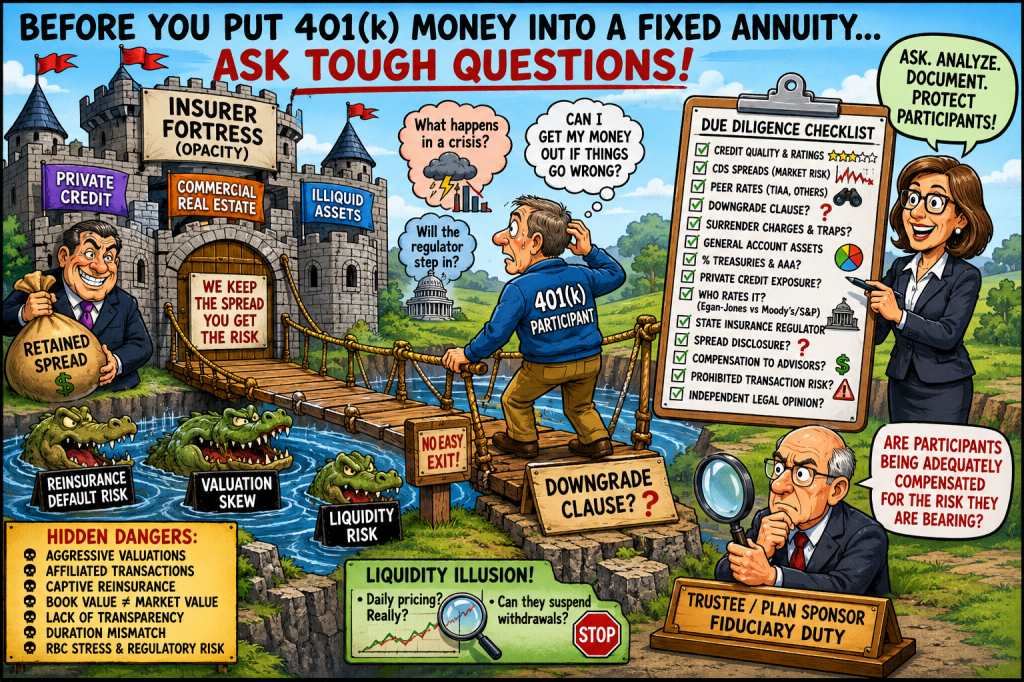

This checklist is intended to assist ERISA fiduciaries, consultants, investment committees, and plan sponsors in evaluating fixed annuity products offered within 401(k), 403(b), stable value, guaranteed income, or pension risk transfer structures.

The objective is to determine:

whether the annuity provides adequate compensation for insurer credit and liquidity risk,

whether the contract may involve prohibited transaction concerns,

whether hidden spread compensation exists,

and whether the product is prudent relative to available alternatives.

I. CREDIT QUALITY AND MARKET-BASED RISK REVIEW

A. Public Debt Yield Comparison

Questions

What yield is the insurer currently paying on publicly traded senior notes?

What spread over Treasuries does the market require?

How does the annuity credited rate compare to:

senior note yields,

subordinated debt yields,

institutional funding costs,

and peer insurer bond spreads?

Key Analysis

If the insurer issues senior notes at 5.3% while crediting annuity holders only 3.0%, evaluate:

retained spread,

hidden compensation,

and whether participants are undercompensated for insurer credit risk and illiquidity.

Documentation

Current note prospectuses

TRACE bond yields

Bloomberg yields

Treasury spread analysis

B. Credit Default Swaps (CDS)

Questions

What is the insurer’s current 5-year CDS spread?

Has CDS widened materially over:

1 year,

3 years,

or since contract inception?

Does the CDS market imply deterioration inconsistent with insurer ratings?

Key Analysis

CDS spreads may provide a more market-sensitive measure of insurer default risk than rating agencies.

Suggested Thresholds

<50 bps = lower perceived risk

50–100 bps = moderate concern

100 bps = elevated concern

Rapid widening = potential early warning signal

Documentation

Bloomberg CDS data

ICE/CMA pricing

Historical spread charts

C. Ratings Review

Questions

What are the:

Moody’s,

S&P,

Fitch,

AM Best ratings?

Are ratings on:

negative outlook,

watchlist,

or downgrade review?

Have ratings agencies cited:

commercial real estate,

private credit,

liquidity,

or valuation risks?

Important

Ratings often lag actual market deterioration.

Documentation

Ratings reports

Outlook changes

Recent downgrade history

II. CONTRACT STRUCTURE AND LIQUIDITY

A. Downgrade Clause

Critical Question

Does the annuity permit termination or liquidation upon:

ratings downgrade,

CDS widening,

RBC deterioration,

or insolvency concerns?

Questions

Is there a downgrade trigger?

At what level?

BBB?

BB?

Can assets be moved without:

surrender charges,

market value adjustments,

or penalties?

Key Analysis

Absence of downgrade rights may expose participants to trapped-credit risk.

Interviewer: Jeffrey H. Snyder Guest: Christopher Tobe, CFA, CAIA Topic: ERISA litigation, annuity risk, private credit, target-date funds, and pension transparency Film Referenced: Pension Fight Club

Introduction

Jeffrey Snyder: Christopher, welcome back. You’ve been deeply involved in ERISA litigation and fiduciary analysis for years, especially surrounding retirement-plan annuities and alternative investments. There seems to be a new wave of litigation developing around these products. What are you seeing?

Christopher Tobe: What we’re seeing now is a widening divide between the very largest retirement plans and the mid-sized plans that receive far less public attention. The mega-plans attract headlines, but many of the most significant fiduciary issues are occurring in plans ranging from roughly $100 million to $1 billion in assets—particularly regional hospital systems and similar employers.

A major issue is the use of fixed annuity products paying participants approximately 2%, while comparable products in the marketplace are paying closer to 4% or higher. That spread can represent a very large transfer of value away from participants over time.

The litigation focus increasingly comes down to a simple question: Are participants receiving reasonable value for the risks they are taking?

The Hidden Economics of Fixed Annuities

Snyder: You spent years inside the insurance industry helping structure these products. Explain how the economics actually work.

Tobe: I spent seven years at Transamerica helping manufacture and manage these products, including separate-account and synthetic annuity structures. One of the least understood aspects of the industry is the insurer spread.

Insurance companies may earn 6% or 7% on underlying investments—today often including private credit, private mortgages, and less liquid assets—while crediting participants only 2%.

The difference becomes the insurer’s spread.

That spread is rarely transparent. In many cases, participants have no meaningful way to evaluate whether they are being compensated fairly relative to the underlying risks.

Some providers, such as TIAA, historically paid substantially higher crediting rates and maintained lower spreads. Other providers may pay rates far below market alternatives.

From a litigation standpoint, those differences become measurable damages.

Snyder: There has been growing concern about insurance companies loading up on private credit exposure. Is that risk being underestimated?

Tobe: Yes—significantly underestimated.

Many people still assume insurance-company general accounts primarily hold traditional investment-grade bonds. Increasingly, that is no longer true.

Today, many insurers are heavily invested in private credit and less transparent structured investments. Participants often do not realize that their supposedly “safe” retirement products may contain substantial liquidity and credit risk.

In my view, these products can represent some of the riskiest investments inside retirement plans precisely because participants bear risks they cannot properly see or evaluate.

The fundamental fiduciary question becomes whether these structures constitute prohibited transactions under ERISA and whether plan fiduciaries fully understand the embedded conflicts.

Snyder: Retirement-income solutions are being heavily marketed right now. Are plan sponsors prepared for the fiduciary responsibilities that come with them?

Tobe: I remain skeptical of placing annuity products inside retirement plans.

Participants who want annuities can purchase them independently outside the plan structure. Embedding them inside ERISA plans creates additional fiduciary complexity and litigation exposure.

Despite the marketing push, actual adoption of many of these products remains relatively modest. The larger issue continues to be traditional fixed annuity arrangements and the lack of transparency surrounding them.

Many fiduciaries still do not fully understand how these products are priced, how spreads are generated, or how much risk is being transferred to participants.

Snyder: Target-date funds now dominate many retirement plans. What are fiduciaries missing?

Tobe: About half of retirement-plan assets are now invested through target-date structures, which means fiduciaries absolutely must understand what is inside them.

Many target-date funds are well-designed products. But fiduciaries cannot simply compare performance charts without understanding the underlying asset allocation and investment structure.

Asset allocation drives the majority of long-term outcomes.

Much of the litigation surrounding target-date funds ignores that reality. Two funds with different glide paths, different equity allocations, or different exposure to private assets should not automatically be compared as if they are interchangeable.

The real question is transparency: What exactly does the participant own?

Collective Investment Trusts and Regulatory Arbitrage

Snyder: You’ve raised concerns about collective investment trusts, or CITs. Why?

Tobe: Traditional SEC-regulated mutual funds operate under robust disclosure and accounting standards. Increasingly, however, retirement plans are moving toward state-regulated collective investment trusts.

Some CITs are entirely appropriate. Others are beginning to incorporate harder-to-value investments such as private equity, private credit, and annuity structures.

My concern is that the industry is gradually moving toward less transparent regulatory environments.

Whenever financial structures become more opaque, fiduciary risk increases.

Plan sponsors need to understand not only the investment itself, but also the regulatory framework governing it and the protections—or lack of protections—available to participants.

Transparency and the Problem of “Black Box” Investing

Snyder: You often talk about transparency as the core issue. Why is it so important?

Tobe: Because transparency ultimately determines accountability.

With traditional mutual funds, fiduciaries can generally see the underlying holdings, pricing mechanisms, and expenses.

With many contract-based investments—annuities, private equity partnerships, private credit vehicles, and certain alternative structures—that visibility disappears.

Once transparency disappears, meaningful oversight becomes much more difficult.

That is true in both ERISA plans and public pension systems.

Snyder: You recently released a documentary film titled Pension Fight Club. What is the film about?

Tobe: The film examines the growing conflicts surrounding public pensions, private equity, hidden fees, and pension governance.

It includes pension trustees, whistleblowers, journalists, fiduciary experts, and former public officials discussing how secrecy increasingly dominates parts of the pension-investment system.

One of the most troubling realities is that even pension trustees themselves are sometimes denied access to underlying private equity contracts and side letters.

That level of secrecy creates enormous governance concerns because these arrangements can involve billions of dollars in commitments, substantial hidden fees, and highly subjective valuation methodologies.

Many of the same transparency issues we see emerging in 401(k) litigation also exist inside large public pension systems.

pensionfightclub.com

Closing Thoughts

Snyder: What is the larger takeaway for fiduciaries and retirement investors?

Tobe: The central issue is transparency.

Participants, fiduciaries, and trustees cannot properly evaluate risks they are not allowed to see.

Whether we are discussing annuities, private credit, collective investment trusts, or private equity, the common theme is the gradual migration toward more opaque investment structures.

That trend increases both fiduciary risk and systemic risk.

The retirement system functions best when investments are transparent, independently priced, and fully understandable to the people whose retirement savings are at stake.

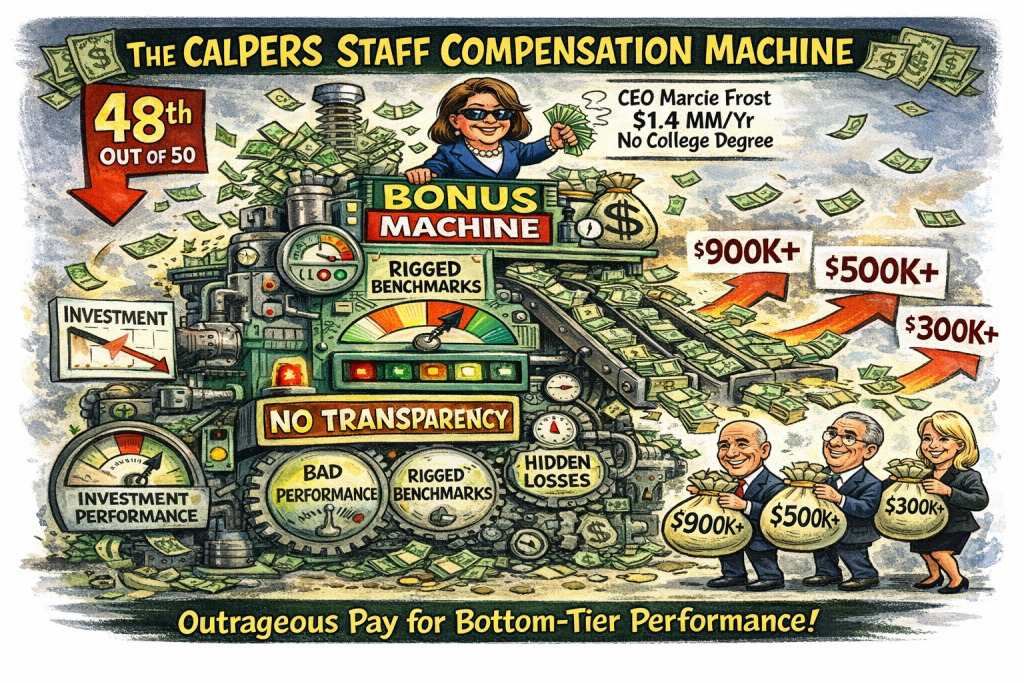

The fund’s staffers receive “excessive compensation” despite its dismal performance. Four executives make more than $1 million a year, another four more than $900,000 and 26 earn between $500,000 and $900,000.

From the new groundbreaking CalPERS report and NBC report . CALPERS CEO Marcie Frost made $1.4mm despite not having a college degree and is one of 8 making over $900,000 a year. There are 34 making over $500,000 a year and 86 making over $300,000 a year. This is not only an insult to taxpayers and government employees but is so excessive it might endanger the tax status of the plan. These salaries are so excessive that even a mid-level investment employee, the Managing Investment Director of ESG, was singled out in a recentoversight letter from the U.S. House Committee on Education and the Workforce to officials at CalPERS for making $624,024 as one of the factors in challenging the tax status of the plan. https://edworkforce.house.gov/uploadedfiles/02.12.26_calpers_loss_oversight_letter_will_instructions.pdf

Excessive Staff Compensation Driven by Bogus Benchmarks

Compensation levels at CalPERS now extend far beyond the norms of public administration. The Governor of California earns approximately $234,000 annually, yet dozens of CalPERS employees earn multiples of that amount. CEO compensation increased from roughly $406,000 in 2018 to more than $1.24 million in 2024, an increase of more than 200 percent—far outpacing the wage growth of the public workers whose retirement security the fund exists to protect.

Executive incentives rely heavily on CalPERS’ custom policy benchmarks and discretionary organizational metrics rather than direct comparison to transparent market benchmarks. As a result, compensation can rise even during periods marked by leadership instability, governance controversy, and poor investment performance.

Compensation advisor GCA benchmarks CalPERS executives against private-sector investment professionals, despite fundamental differences in risk exposure, compensation volatility, and personal capital at risk inflating compensation bands while requiring no performance accountability.

In short, CalPERS pays higher than private sector salaries for investment performance that would result in termination in the private sector. An independent Inspector General would fundamentally alter the structure in which salaries are justified, evaluate the relationship between compensation escalation and measurable long-term net performance, as well as recommend claw back or deferral structures tied to realized economic outcomes rather than interim marks.

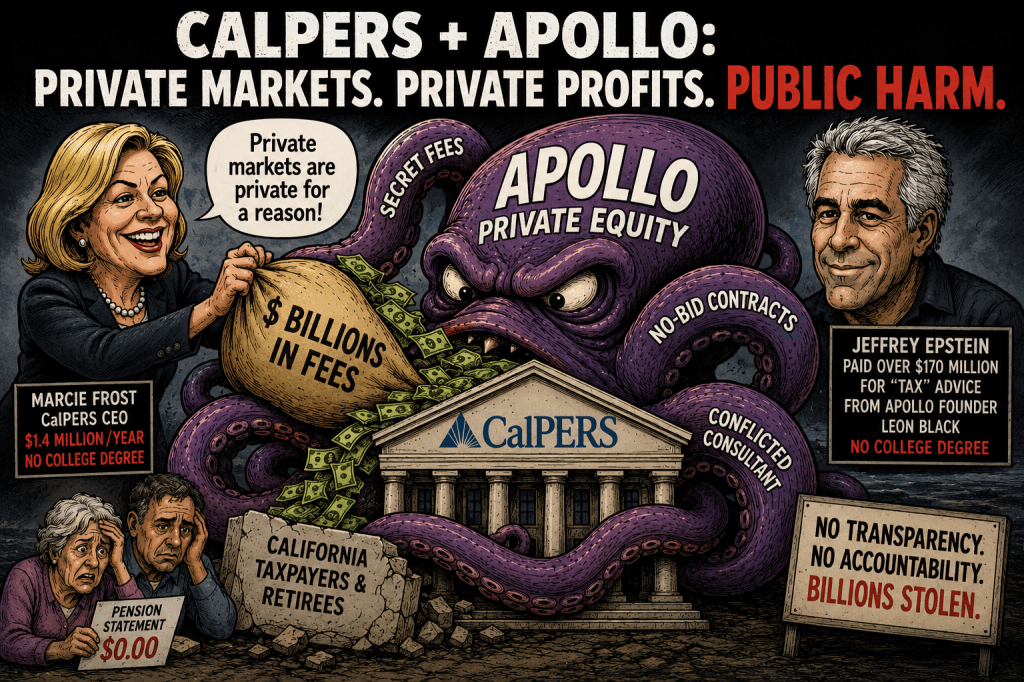

Our new 255 page Forensic investigation CalPERS: America’s Misled and Misleading Pension Leader captures the twisted relationship CALPERS has with Private Equity whose 4 leading players are Apollo, KKR, Blackstone & Carlyle where CALPERS invests billions. Private Equity extracts from CA Taxpayers over $5 billion a year in fees from secret no-bid contracts with CALPERS. https://www.rpea.com/view/download.php/news/calpers-investigation-report

In an 2025 interview with CNBC’s “Squawk on the Street”, CalPERS CEO Marcie Frost after smirking, gratuitously reassured her Private Equity Partners:

Frost refused to provide any unredacted Private Equity contract of over 400 from open records request for the Forensic Investigation in timely matter.

Frost is paid $1.4 million per year and like Jeffrey Epstein does not have a college degree.

Our report mostly covers the overall twisted relationship with Private Equity but I wanted to focus on the most sick relationship of all, Apollo. The report does break 3 major Apollo related stories.

2. Apollo admits that 75-80% of its assets are from public pensions. CalPERS as major US pension leader has contributed $billions to Apollos profits.

3. Apollo total commissions to xCalpers Trustee Villabous – who committed suicide – were significantly higher $35mm vs. $22 mm in placement agent fees which was number most widely circulated. The SEC number did not include the $13.2 mm commission Villabous got from CALPERS purchasing an equity stake in Apollo stock. It cites and references the AFT and AFLCIO letters tying Apollo to Jeffrey Epstein. And the following table.

CALPERS corruption was so broad that despite the Forensic Investigation being 255 pages only a few pages were dedicated to Apollo. So, I have put together a piece on a timeline that explores more issues in depth.

For years before the current Private Debt meltdown and the Jeffrey Epstein scandal CALPERS has been in a conflicted relationship with Apollo. Since 2000 it is estimated that CALPERS has paid $10 to $14 billion in fees to Apollo in secret no-bid contracts. In 2007 it actually purchased an ownership interest in Apollo. CALPERS supposed independent investment consultant Wilshire is secretly owned by Apollo. These conflicts continued for decades and are still going on. A former Trustee collected $35 million in secret commissions from Apollo but died from “suicide” before he could be put in prison. However, the CALPERS Executive Director did go to prison for 5 years on Apollo related transactions. This period in time overlaps the time (2005-2019) when Leon Black of Apollo was the largest funder of Jeffrey Epstein admitting to paying over $170 million to him for “tax” advice.

CalPERS in 1998 put $150 million in the Apollo Investment Fund IV, and in 2001 $250 million Apollo Investment Fund V. But in 2007 it went to a new level.

Alfred Villalobos served as and was on the CalPERS’ Board from 1992 to 1995. After leaving the CALPERS board he eventually in the early 2000s created his placement agent firms ARVCO and CF partners which received over 95% of its revenue strictly from Apollo. Charles “Chuck” Valdes served on the CalPERS board for 25 years and was Chair of the Investment Committee from 1988 to 1999 and again from 2005 to 2007. Federico Buenrostro was a Senior California state official before joining CALPERS as CEO in 2002.

Villalobos, via his placement agency ARVCO contracted with Apollo Management VI, L.P. on or about May 25, 2005, for a $650 million investment. Villalobos received $3,864,734 in commissions secretly from Apollo for this placement.

Villalobos successfully induced CalPERS to invest $200 million in Apollo Alternative Assets, L.P. on or about July 27, 2006, and received a $4.4 million commission from Apollo.

Villalobos, Valdes, and Buenrostro made a ten-day trip together in November of 2006, ostensibly to attend the two-day Capital Markets Conference in Dubai. They flew together from San Francisco to London on November 17,2006 and then from London to Dubai the next day. Then on to Hong Kong, where they were picked up by a limousine. They then took a 30-minute helicopter ride from Hong Kong to Macau, a famous gambling location. https://oag.ca.gov/news/press-releases/brown-files-suit-against-former-calpers-officials-and-freezes-assets-alfred?

In May of 2007 a senior CalPERS investment officer Leon Shahinian responsible for evaluating a multibillion-dollar Apollo Private Equity commitment was invited to a due diligence meeting with Leon Black at Apollo’s offices in New York prior to attending a black-tie event at the Museum of Modern Art (“MOMA”) honoring Apollo founder Leon Black. Shahinian made no effort to book a commercial flight to New York, choosing instead to accept former trustee now placement agent Alfred Villalobos’ offer to fly with him there by private jet.

Villalobos and ARVCO, his placement agent firm apparently paid for all the travel arrangements for the trip, and later billed Apollo over $8,000 for the suite and related hotel charges, over $1,500 in car service fees, and over $50,000 for the use of the private jet. Villalobos was later reimbursed for these costs by Apollo, including the jet.

One month after his trip to New York, Shahinian made a presentation to the Investment Committee of the Board chaired by Valdes regarding the proposed investment in Apollo Management VII, L.P and it was approved in July 2007. Villalobos received a secret $3.5 million commission from Apollo for this transaction.

In September 2007, CalPERS purchased a $601 million ownership stake (8.6%) in Apollo ahead of Apollo’s listing on Goldman Sachs’ private exchange. After the buy in, the relationship went to a higher level. Villalobos received a secret $13.2 million commission from Apollo for this transaction.

In early 2008 Villalobos placed several Apollo European funds and received $1 million in commissions. CalPERS invested $1 billion in Apollo Credit Opportunity on or about April 15, 2008, and as compensation, Villalobos received $9,070,833 in commissions from Apollo.

For nearly 2 years this scheme operated in silence until the SEC sent a formal inquiry to Villalobas firm ARVCO on July 17, 2009, and some stories around placement agents dribbled out in late 2009 by the Sacramento Bee. The scheme was not caught by any CALPERS internal controls, and many believe it was Buenrostro’s x-wife who was listed as providing testimony to the U.S. DOJ.

The Steptoe report focused on Villalobos and Buenrostro who were guilty but covered up many others who should have received more scrutiny especially Epstein linked Apollo. Philip S. Khinda (lead author of the review report) simultaneously negotiated and then memorialized in a “new strategic relationship agreement” with Apollo Global Management in a April 16, 2010 letter addressed to Leon D. Black, explicitly praising Apollo’s cooperation with the still-ongoing review. https://documents.latimes.com/calpers-special-review/?_gl=1*1pjpo7m*_gcl_au*NTcwOTU0NTEyLjE3NjkzNjUyNDk

So while Apollo paid the placement agent fees (kickbacks) over $35 million to Villalobos and made the $billions in excessive fees they escaped any accountability for this scandal. Coincidentally, Steptoe & Johnson were Epstein’s criminal attorneys when he died in prison in 2019.

The media attention did not break big until 2010 with articles in the Wall Street Journal and New York Times. The California Attorney General filed Civil Actions, and the FBI and other agencies opened criminal probes May-June 2010.

In April 2012, the SEC charged former CalPERS CEO Federico Buenrostro and his close associate/placement agent and former trustee Alfred Villalobos with falsifying investor disclosure letters to induce Apollo to pay placement-agent fees the SEC said Apollo supposedly would not otherwise have paid without those disclosure letters. In August 2014, the U.S. Attorney’s Office (NDCA) described a superseding indictment alleging Villalobos conspired with Buenrostro in connection with a $3 billion CalPERS investment into Apollo-managed funds, that Villalobos acted as Apollo’s placement agent through ARVCO, and that fraudulent investor disclosure letters were created after CalPERS offices declined to sign.

In January 2015, Villalobos died in what authorities described as an apparent suicide, just before trial in the CalPERS corruption case. Buenrostro was sentenced to 5 years in prison. Reporting at the time underscored that Apollo itself was not accused of wrongdoing in that episode (above the law)— that even though they benefited the most from the corruption they appeared to be immune from any accountability.

Apollo was rewarded with continuing exposure and significant growth. CalPERS’ Private Equity Program performance table lists Apollo Investment Fund VIII (2013)with a $350 million commitment. This is in addition to an additional $800 million commitment to Private Credit.

CALPERS is regularly referred to as “America’s top Pension fund” and is seen by other pensions as a first mover and policy setter. Apollo co-founder Joshua Harris admitted at a 2013 meeting of the Philadelphia Board of Pensions that the firm’s capital base was overwhelmingly dependent on public retirement systems. Asked directly whether Apollo had many public pension investors, Harris responded bluntly that “almost all” of Apollo’s capital came from public funds, estimating that roughly 75% to 80% of Apollo’s capital was supplied by public pension plans. Many other state pension plans invested $billions with Apollo based on CALPERS lead. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

While CALPERS has refused to disclose any of these Apollo contracts unredacted in our open records request, Pennsylvania accidently released their Apollo Investment Fund VIIIcontract, (which is the same one CalPERS has) and it is publicly available on the Naked Capitalism web site. https://trove.nakedcapitalism.com/LPAs/verified-as-LPAs/Apollo_Investment_Fund_VIII_LPA_S1.pdf Apollo agreements make use of offshore vehicles, parallel structures, and non-California governing law. The contracts embed the possibility of NAV smoothing, delayed recognition of impairment, and performance presentation that cannot be independently reconstructed. Each agreement centralizes valuation authority in the General Partner. Independent valuation is not mandated as binding. Audit rights are limited. Third-party valuation is discretionary. Apollo explicitly permitted affiliates to engage in other investment activities, to manage competing funds, to allocate opportunities among affiliated vehicles, and to pursue co-investment structures. In 2016 Apollo Private Equity was fined $52 million by the SEC for Investor Protection violations misleading fund investors about fees and excessive expenses and I could find no record of CALPERS addressing this.

On Jan. 25, 2021, Apollo filed a SEC Form 8-K that included two exhibits: a letter from then-CEO Leon Black to Apollo’s limited partners, and an investigative report from the law firm of Dechert LLP. The Dechert report takes pains to minimize Epstein’s ties with other Apollo executives, including CEO Marc Rowan. https://www.sec.gov/Archives/edgar/data/1411494/000119312521016405/d118102d8k.htm

In 2021, Wilshire was acquired by private equity firms CC Capital Partner and Motive Partners. That same year, Apollo Global Management, Inc., acquired up to a 24.9 percent minority stake in Motive’s management company and Apollo and its affiliates became limited partners in Motive managed vehicles. To our knowledge this was not disclosed to board. Having you so-called independent consultant Wilshire owned by a manager Apollo that they are supposed to evaluate is an egregious conflict of interest.

Performance losses based on Apollo’s own self-reported numbers are around $3 billion. Actual losses may be another $1billion or more if Apollo Private Credit and Private Equity were marked to market.

that Apollo itself and CEO Marc Rowan had much deeper ties to Jeffery Epstein than previously disclosed in the 2001 SEC filing and that Apollo chief Marc Rowan consulted Epstein on firm’s tax affairs.

The February 2026 complaint filed with the U.S. Securities and Exchange Commission by the American Federation of Teachers and American Association of University Professors who both represent CALPERS members alleges that Apollo’s disclosures may have been materially incomplete or misleading.

The complaint goes into detail the contradiction of the 2021 SEC disclosures and the recently disclosed Epstein Files uncovered by the FT.

The unions asked the Commission to investigate whether Apollo’s prior disclosures about it and its executives’ ties to Jeffrey Epstein painted an “inaccurate and incomplete picture.” Their letter pointed to newly released Epstein documents referring to Marc Rowan, including meetings at Apollo’s offices, breakfasts involving Rowan, Leon Black, and Epstein, discussions of donor-advised funds, tax matters, a possible Apollo inversion, and other business-related contacts. The letter concluded that the 2021 disclosures may have offered “an inaccurate depiction of the extent of Apollo’s ties with Jeffrey Epstein” and said the SEC should investigate whether the statements were materially false or misleading.

However, CalPERS has spent $millions in staff hours trying to block even this small amount of transparency. https://www.calpers.ca.gov/documents/202605-full-agenda-item08a-02-a/download?inline With the support of Private Equity industry CalPERS at this time seems to have killed this Private Equity transparency bill, denying it a hearing.

The conflicted CALPERS – Apollo relationship has cost participants and taxpayers $billions. Excessive fees as high as $14 billion. Additional performance drag of many more $billions.

With Apollos culture being exposed by the Epstein connections, it is way past time for CALPERS to part ways with this parasitic vendor.

The collapse of PHL Variable Insurance Company should end the myth that annuities are somehow “safe” simply because they are wrapped in insurance company marketing language. What happened at PHL is not just an isolated insurance failure. It is a warning sign for the entire retirement system—especially for ERISA plans using annuities inside 401(k)s and Pension Risk Transfer (“PRT”) deals. Any ERISA plan with an Annuity without a downgrade clause is at high risk.

PHL Variable—a private equity-owned insurer—collapsed after years of deterioration and is now heading toward liquidation, leaving many policyholders facing potentially massive losses above state guaranty limits.

The mainstream retirement industry keeps pretending annuities are equivalent to government-backed guarantees. They are not. They are unsecured obligations of highly leveraged insurance companies increasingly tied to private equity and private credit risk.

That distinction matters enormously under ERISA.

The PHL collapse exposes the fundamental fraud embedded in the modern annuity sales pitch to retirement plans. Participants are told they are buying “guaranteed income.” In reality, they are often buying concentrated exposure to a single insurer’s opaque balance sheet, private credit portfolio, derivatives exposure, and liquidity management strategy.

This is precisely why annuities in ERISA plans increasingly look like prohibited transactions.

The Department of Labor’s recent pro-annuity guidance ignores the central issue: the retirement system is being pushed toward products where the real risks are hidden inside insurance-company accounting structures that participants cannot evaluate. The underlying investments are often illiquid, privately valued, and shielded from normal SEC-style transparency. As discussed previously on Commonsense 401(k), many of these risks are amplified through state-regulated Collective Investment Trusts (“CITs”) and insurance separate accounts that avoid meaningful public disclosure.

PHL demonstrates what happens when the illusion breaks.

State guaranty associations that the annuity industry point to are a farce

This becomes especially dangerous in Pension Risk Transfers which have 100% annuity coverage.

In a traditional defined benefit plan, retirees have protections through ERISA fiduciary duties and the Pension Benefit Guaranty Corporation. But once liabilities are dumped into an annuity structure through a PRT transaction, participants become exposed primarily to insurer solvency risk and limited guaranty association protections.

That is a massive downgrade in protection that the industry rarely discusses honestly.

The irony is staggering. Pension sponsors claim they are “de-risking” by shifting obligations to insurers. In reality, they may simply be replacing diversified pension funding structures with concentrated exposure to private equity-driven insurers increasingly loaded with private credit, commercial real estate, leveraged loans, and exotic structured assets.

The PHL collapse also destroys one of the central talking points used by annuity advocates: that insurance company failures are extremely rare and therefore not economically meaningful.

The modern insurance industry is not the same industry it was twenty years ago.

Private equity firms have aggressively moved into life insurance and annuity markets because retirement assets represent one of the largest pools of permanent capital in the world. Firms like Apollo Global Management transformed insurers such as Athene Holding into engines for gathering annuity assets and investing them into higher-risk private credit strategies. The economic model depends heavily on earning hidden spreads between what insurers make on investments and what they credit to retirees.

That creates an unavoidable conflict of interest.

The more risk the insurer takes internally, the larger the potential spread profits for shareholders and private equity sponsors. But retirees bear the ultimate solvency risk.

This is exactly why the PHL story should terrify fiduciaries considering annuity-heavy target-date funds or PRT transactions.

ERISA fiduciaries are supposed to act solely in participants’ interests. Yet many annuity arrangements involve opaque compensation, undisclosed spread profits, affiliated recordkeepers, proprietary CITs, and insurer-controlled valuation systems. Participants cannot independently evaluate the underlying risks because the accounting itself is often non-transparent.

The retirement industry calls this “innovation.”

A more accurate term may be “regulatory arbitrage.”

Even worse, the accounting structure of many insurance products can hide deteriorating asset values for years. As discussed previously in DOL 401(k) Fiduciary Rule Enables Accounting Fraud, private credit and insurance assets are often not marked to market in ways participants would recognize from mutual funds or public securities. This allows risk to accumulate quietly until a solvency event occurs.

That appears increasingly relevant in the PHL collapse.

The industry still insists annuities belong inside 401(k) default investments despite the fact that participants cannot meaningfully evaluate insurer balance sheets, CDS spreads, private credit concentrations, liquidity stress, or reinsurance chains.

Would any prudent fiduciary knowingly concentrate retirees into a single opaque private-credit vehicle with limited transparency, weak liquidity, and capped guaranty protection?

That is effectively what many annuity structures have become. Fixed annuities are in 2000 of the largest 8000 plans over $100 million in size and in bigger numbers in small plans. The new trend is to hide annuities into poorly state regulated CITs.

The PHL collapse should force courts, regulators, and fiduciaries to reconsider the entire legal framework surrounding annuities in ERISA plans. If these products expose participants to undisclosed insurer spread compensation, opaque accounting, affiliated-party conflicts, and substantial insolvency risk, then the prohibited transaction questions become unavoidable.

Even beyond the immediate losses, the PHL collapse exposes another major fiduciary failure in annuity structures used inside ERISA plans and Pension Risk Transfers: the lack of meaningful liquidity and downgrade protections. Any annuity used in a 401(k), stable value fund, or PRT transaction should contain a clear downgrade-triggered exit clause allowing fiduciaries to reduce or terminate exposure if the insurer’s credit quality materially deteriorates. That is standard risk management in many bond and derivative markets, yet retirement annuities are often structured as one-way lockups where participants remain trapped as the insurer weakens. Without downgrade clauses tied to credit ratings, CDS spreads, reserve deterioration, or liquidity stress, retirees can be forced to ride an insurer all the way into collapse. Fiduciaries should not be required to wait until losses approach 100% before acting. The ability to exit a deteriorating insurer early—while there is still market value left—is essential prudence under ERISA, particularly now that many annuity providers are deeply tied to private equity-driven private credit strategies.

The industry keeps calling annuities “guaranteed.”

PHL reminds us that the guarantee is only as strong as the insurer standing behind it.

The battle for Northern Kentucky is no longer just another Republican primary. It has become a referendum on whether a genuine grassroots constitutional conservative can survive against the combined pressure of billionaire money, national political machines, and what many activists increasingly call the “Epstein Class” — the network of elite power brokers, lobbyists, mega-donors, intelligence-connected operatives, and influence organizations that shaped both parties for decades.

At the center of this political storm stands Thomas Massie — perhaps the single most independent Republican in Congress. Massie has repeatedly broken with party leadership, challenged endless wars, opposed surveillance expansions, criticized corporate welfare, and most importantly for many Kentuckians, became one of the loudest voices demanding full transparency on the Jeffrey Epstein files.

That stance changed everything.

Massie’s bipartisan push with Democrats to force release of Epstein-related records put him on a collision course not only with entrenched Washington power, but also with enormous political money. According to multiple national reports, this primary has become one of the most closely watched Republican races in America precisely because it tests whether independent-minded conservatives can survive after opposing the establishment consensus.

The race is now flooded with outside influence. a coordinated effort by billionaire-funded Super PACs, AIPAC-aligned interests, and national donor networks to destroy a congressman who refused to stay quiet on Epstein, Israel policy, surveillance, spending, and foreign wars.

Massie himself has framed the race as a fight against “Israel first billionaires” and national money trying to overpower local voters in Northern Kentucky. Whether voters agree with that framing or not, the financial imbalance is undeniable. Millions of dollars have poured into a congressional primary that ordinarily would attract little national attention.

For activists connected to the broader Epstein transparency movement, this election carries symbolic importance far beyond Kentucky’s 4th District. They see Massie as proof that one of the few remaining independent members of Congress can still challenge powerful interests publicly — and survive.

That is why this election feels existential to many grassroots voters.

The establishment message is simple: Fall in line. Stop asking questions. Accept the approved narrative.

But the grassroots message is different: Who really controlled Epstein? Who benefited? Why are so many records still hidden? And why are politicians who demand answers suddenly targeted with overwhelming financial opposition?

Northern Kentucky voters now stand at the center of that conflict.

Massie’s supporters argue that if someone with his name recognition, fundraising base, and deep local roots can be defeated by outside money and national pressure campaigns, then independent representation in Congress may effectively be over. They see this race as one of the clearest modern examples of grassroots politics versus institutional power.

For Kentucky activists involved with Epstein transparency efforts, the stakes feel even larger than party politics. They believe the public is only beginning to understand how deeply interconnected intelligence operations, billionaire finance, lobbying networks, media influence, and political protection systems may have been within the Epstein orbit.

And in their eyes, Thomas Massie crossed an unforgivable line: He kept asking questions.

This week’s election will reveal whether Northern Kentucky still values independent representation — or whether modern congressional politics has become too dominated by national money and coordinated influence campaigns for true grassroots candidates to survive.