Over the last decade, private equity has been sold to pension funds as the cure for everything: low interest rates, weak public-market returns, and supposedly “inefficient” markets that only elite managers can exploit. Yet as the evidence accumulates, a different picture has emerged. Study after study suggests that the performance story underpinning the expansion of private equity into pension portfolios may itself be a carefully constructed illusion. When returns are properly measured and compared, the promised outperformance often evaporates. As documented in the analysis “Private Equity Performance: A Systematic Deception,” https://commonsense401kproject.com/2026/01/25/private-equity-performance-a-systematic-deception/, the reporting conventions used by private equity managers—particularly the use of internal rate of return and selectively constructed benchmarks—can obscure the true economic performance delivered to investors.

Recent research continues to reinforce this concern. A steady stream of academic and policy studies has challenged the assumption that private equity consistently outperforms public markets. Reports from policy groups and academic researchers have increasingly found that, once fees and risk are properly accounted for, private equity often performs no better—and sometimes worse—than simple public-market alternatives. These findings have been echoed in recent research from Harvard Business School and other institutions examining the structure of private equity returns. In short, the claim that pensions must invest in private equity to meet their obligations is becoming harder to sustain. https://www.evidenceinvestor.com/post/private-equity-in-your-pension https://pestakeholder.org/reports/private-equity-underperforms/

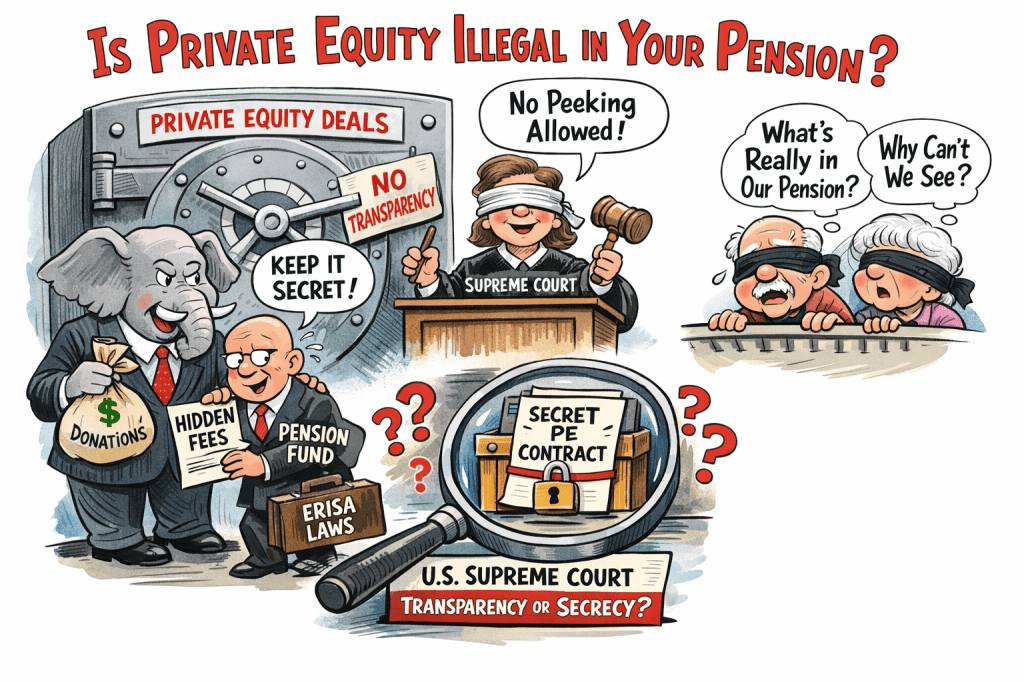

Performance, however, is only part of the story. Private equity also brings unusually high fees and complex risks. When pension plans receive full transparency on these elements—returns, costs, leverage, and contractual structures—the investment often appears far less attractive. In fact, a detailed analysis titled “Private Equity as an ERISA Prohibited Transaction” https://commonsense401kproject.com/2025/10/27/private-equity-as-an-erisa-prohibited-transaction/ argues that, when properly disclosed, many private equity arrangements would struggle to meet the fiduciary standards required under U.S. pension law. Under the Employee Retirement Income Security Act (ERISA), fiduciaries must act solely in the interest of plan participants and must avoid conflicts of interest and excessive compensation. Private equity’s opaque fee structures and related-party arrangements raise serious questions under those standards, as well as under the fiduciary laws governing many state and local public pension systems. UK, Canada, and Austrailian laws are less direct but carry the same overall fiduciary principles.

This creates a fundamental problem. If private equity cannot survive under full transparency, the only way to place it inside pension plans is to obscure it. The growing use of complex investment vehicles—such as layered target-date funds and other multi-asset structures—has increasingly allowed private equity exposures to be embedded within broader portfolios where the underlying contracts and fee arrangements remain difficult for participants to see. As described in the analysis of the H-E-B 401(k) case, these structures can effectively hide private equity exposures inside retirement plans while limiting the ability of participants to evaluate the true costs and risks. https://commonsense401kproject.com/2026/01/21/the-ny-times-missed-the-real-h-e-b-401k-story/ A WSJ article by Jason Zweig started to look at some of the structures used to hide private equity ie. State regulated CITs https://commonsense401kproject.com/2025/12/07/wall-street-journal-exposes-target-date-cit-corruption-but-theyve-only-scratched-the-surface/

The legal battle over transparency is now reaching the highest levels of the U.S. judicial system. In litigation involving a major corporate retirement plan, participants have sought access to the underlying private equity arrangements embedded in their plan’s investment options. The case has drawn the attention of the U.S. Supreme Court, but notably the Court is not being asked to decide whether private equity itself is legal inside pension plans. Instead, the issue is far more basic: whether plan participants are allowed to see the contracts and information necessary to evaluate the investment at all.

This fight over transparency has attracted extraordinary attention from the financial industry and from regulators. The Department of Labor under the Trump administration—whose political environment included significant financial support from private equity firms such as Apollo, Carlyle, Blackstone, and KKR—submitted arguments supporting a ploy called “meaningful benchmarks” https://commonsense401kproject.com/2026/01/20/why-the-meaningful-benchmark-standard-is-a-judicial-illusion-built-for-wall-street/ that would limit the disclosure obligations faced by plan fiduciaries. If those arguments prevail, the result would be a legal framework in which private equity investments can remain embedded in retirement plans while the participants whose savings are at stake may never see the underlying agreements.

In effect, the Supreme Court case has become a referendum on secrecy. https://commonsense401kproject.com/2026/01/17/the-supreme-courts-intel-case-is-about-secrecy-fake-benchmarks-and-fiduciary-illusions/ If participants are denied access to the relevant information, the legality of the private equity investment can never be meaningfully tested. It could be perfectly lawful—or it could violate fundamental fiduciary duties. But without transparency, the question cannot even be asked.

That reality highlights the deeper issue facing pension systems around the world. The debate is often framed as whether private equity delivers higher returns which looks more suspect every day. Yet the more fundamental question is whether pension beneficiaries have the right to know what they own. If the investment truly benefits them, transparency should strengthen the case for it. If it cannot withstand transparency, the problem may not be the disclosure rules—it may be the investment itself.

The Supreme Court’s Intel decision will therefore determine more than the outcome of a single lawsuit. It will decide whether the legal system allows retirement savers to look inside the black box that increasingly holds their future security. Until that box is opened, the question will remain unresolved: not simply whether private equity performs, but whether it can legally exist inside a pension plan at all. The temporary blocking of transparency means $billions to the Private Equity industry, while participants will not see the losses until it is too late.

Appendix A – United Kingdom: The Same Problem Under a Different Name

The United Kingdom does not use the American language of ERISA prohibited transactions, but the basic legal problem looks remarkably similar once the fog clears. UK pension trustees operate under a strict “best interests of members” duty and a prudent-person investment standard. The law expects trustees to ensure that pension assets are invested with proper regard for security, liquidity, diversification, and profitability. It also explicitly warns that investments not traded on regulated markets—exactly the category where private equity lives—must be kept at prudent levels.

That framework sounds reasonable until one asks a simple question: how can trustees demonstrate prudence if they cannot even see the full economics of the investment?

Private equity depends heavily on opaque valuations, irregular reporting, and complicated fee layers that are often buried in partnership agreements rather than disclosed in plain view. The more one examines the structure, the more the “best interests” obligation begins to collide with the way the asset class actually operates. Trustees are expected to evaluate performance, compare alternatives, and document why an investment benefits members. But the private equity industry’s preferred reporting conventions—internal rates of return, smoothed valuations, and selective benchmarking—make that evaluation extraordinarily difficult.

UK regulators already understand the problem. The Pensions Regulator has repeatedly warned trustees that private markets require far stronger governance, deeper due diligence, and heightened scrutiny of costs and risks. That warning alone is telling. Investments that are inherently compatible with fiduciary obligations do not usually require constant reminders about the dangers of opacity.

So the British version of the question is slightly different from the American one. It is not simply “Is private equity illegal in your pension?” It is this: how can trustees prove that a highly opaque, illiquid, high-fee asset class satisfies their legal duty to act in members’ best interests when the case for the investment becomes weaker as transparency increases?

In other words, the same contradiction exists in the UK that appears in the United States. Private equity may not violate the law automatically—but the more sunlight applied to the investment, the harder it becomes to reconcile with the duties trustees are sworn to uphold.

Appendix B – Canada: Fiduciary Duty Meets the Black Box

Canada’s pension laws differ in structure from ERISA, but they revolve around the same foundational principle: fiduciaries must act prudently and solely in the interests of beneficiaries. Pension administrators are legally required to exercise the care, diligence, and skill of a prudent person managing someone else’s assets. They must also avoid conflicts of interest and ensure that plan governance protects beneficiaries.

That sounds straightforward—until private equity enters the picture.

The private equity model thrives on opacity. Fees are layered and often partially hidden. Valuations are subjective and frequently delayed. Benchmark comparisons are difficult because the investments are illiquid and priced internally. These characteristics are not incidental quirks of the asset class; they are structural features.

For a fiduciary, those features present a problem. Canadian law expects pension administrators to understand the investments they approve and to evaluate whether they genuinely serve the interests of beneficiaries. But how can an administrator confidently perform that duty when the full economics of the investment may not even be visible?

Canada also preserves an important principle that resonates with the transparency fight now unfolding in the United States: beneficiaries have rights to information about the plans that hold their retirement savings. Pension law in several provinces provides inspection rights and disclosure obligations that are meant to prevent retirement systems from becoming black boxes.

Private equity pushes directly against that principle. The industry frequently insists that its partnership agreements and detailed fee arrangements remain confidential. In effect, beneficiaries are asked to trust that their money is being invested prudently while the most important details remain hidden.

So Canada’s version of the debate arrives at the same uncomfortable question facing American courts. If an investment can only function inside a pension plan when its true economics are shielded from scrutiny, how can administrators claim they are fulfilling their fiduciary duty of care?

Canada may not frame the issue as an ERISA prohibited transaction. But the logic leads to the same place: the more opaque the investment structure becomes, the more difficult it is to reconcile with fiduciary responsibility.

Appendix C – Australia: Transparency Meets Private Equity

Australia’s superannuation system may provide the clearest international test of the private-equity-in-pensions debate because the regulatory framework places extraordinary emphasis on member outcomes and transparency.

Superannuation trustees are subject to a “best financial interests” duty that requires them to demonstrate that every investment decision benefits members. Regulators also impose extensive disclosure obligations, strict governance standards, and performance testing designed to compare funds against measurable benchmarks.

In theory, this framework should create one of the most transparent retirement systems in the world.

But private equity does not fit comfortably inside that system.

Australian regulators have already expressed concern about the valuation and liquidity risks associated with unlisted assets such as private equity. These investments are difficult to price, often depend on internal valuations, and may be slow to reflect changes in market conditions. When markets fall sharply, public assets reprice immediately. Private assets often move slowly, creating the illusion of stability where none may actually exist.

That illusion can distort performance comparisons, making portfolios appear more stable or more successful than they truly are.

Regulators have therefore pushed for stronger governance, independent valuations, and better oversight of unlisted asset pricing. Those warnings reveal a deeper truth: private equity’s core mechanics sit uneasily inside a system built around transparency and accountability.

The Australian debate ultimately mirrors the American one. If superannuation trustees must prove that every investment serves members’ best financial interests, they must be able to measure its costs, risks, and performance honestly.

Yet private equity’s structure—layered fees, opaque valuations, and limited disclosure—makes that proof extremely difficult.

Which leads to the same unavoidable question now confronting pension systems worldwide: if an investment only works when its true economics remain hidden, does it really belong in a retirement system that is supposed to operate in the open?