The campaign to push private equity into America’s 401(k) plans has largely been driven by Wall Street lobbyists, consultants, and asset managers. What has been missing has been an independent academic critique. That gap is starting to disappear.

Next, BYU Law Professor William Clayton and Duke Law Professor Elisabeth de Fontenay have submitted what may be the most comprehensive academic comment letter yet opposing the Department of Labor’s proposed 401(k) private-equity rule. Their accompanying Duke Law Journal article, Private Equity for All: The Paradoxical Push to Democratize Private Markets, expands the analysis even further. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6899998

For years, The CommonSense 401(k) Project has argued that the push into private equity was never primarily about helping retirees. The BYU/Duke paper reaches remarkably similar conclusions—but from mainstream legal scholarship rather than litigation or policy advocacy. That matters.

They Reject the Entire “Democratization” Narrative

Perhaps the paper’s greatest contribution is its willingness to challenge the central marketing slogan of the private-equity industry. For years Americans have been told:

“Retail investors deserve access to investments only rich institutions have enjoyed.”

Clayton and de Fontenay ask a much harder question. What if democratization actually benefits private-equity firms more than ordinary workers?

They conclude that retail investors receive:

higher fees,

greater complexity,

more opaque investments,

uncertain valuations,

weaker liquidity,

while private-equity firms receive billions of dollars of new permanent capital precisely when institutional fundraising has slowed.

One of the strongest sections explains why private equity suddenly wants retirement money.

The industry is facing:

weak fundraising,

fewer exits,

excess portfolio companies,

higher interest rates,

reduced institutional allocations.

That is exactly when the industry begins talking about “democratization.”

Clayton and de Fontenay correctly observe the irony.

Retail investors are being invited into private equity at what may be one of the most difficult periods the industry has experienced in years.

That reinforces our earlier observation that Wall Street is seeking a new captive source of assets—not necessarily because those assets will earn superior returns, but because the industry needs fresh capital.

The Performance Debate Has Finally Gone Mainstream

One of the most encouraging developments is that respected legal scholars are now openly questioning what once seemed untouchable:

Does private equity actually outperform?

The authors review the academic literature and conclude that the evidence is far from settled. After adjusting for leverage, risk, fees, and methodology, many studies show little or no persistent outperformance, while any historical advantage appears to be shrinking as more capital floods the asset class.

Readers of The Great Performance Fraud will recognize this argument immediately. https://commonsense401kproject.com/2026/07/26/the-great-performance-fraud/ Our concern has never been merely whether returns are high. Our concern has been whether the reported returns are comparable to public-market investments at all.

They Confirm the Diversification Illusion

One of our longest-running themes has been that private equity appears less volatile largely because it is not continuously marked to market.

Clayton and de Fontenay make essentially the same point.

The apparent low correlation with public markets may simply reflect valuation smoothing rather than lower underlying economic risk. Comparing private-equity volatility with publicly traded securities can therefore create a misleading picture of diversification.

The professors observe that consultants specializing in private markets have structural incentives to recommend private-market investments because their businesses depend upon those markets continuing to grow. They also warn that performance data and benchmarks in private markets are susceptible to manipulation, making consultant recommendations especially difficult to evaluate independently.

That mirrors years of our reporting on consultant conflicts involving alternative investments.

Taken together, three independent critiques now point in the same direction:

NYU Stern questions whether the DOL proposal protects participants or primarily shields the private-equity industry.

BYU and Duke challenge the economic assumptions underlying the entire “democratization” narrative and explain why the proposal could increase costs and risks while weakening fiduciary accountability.

The CommonSense 401(k) Project has argued for years that opaque valuations, hidden fees, conflicted advice, and weakened disclosure standards are fundamentally inconsistent with ERISA’s participant-first principles.

These perspectives are not identical, and they differ in emphasis and legal theory.

But they converge on one central message:

The burden of proof belongs to those seeking to transform the American retirement system—not to those asking that ERISA continue to demand transparency, independent valuation, meaningful fee disclosure, prudent fiduciary oversight, and accountability before exposing millions of workers’ retirement savings to increasingly opaque private-market products.

That is a debate worth having. And thanks to the work of Professors Clayton and de Fontenay, it is now being advanced with rigorous scholarship rather than marketing slogans.

Their article, “The Labor Department’s Proposed 401(k) Rule Protects Private Equity, Not Retirees,” deserves to become required reading for every ERISA fiduciary, consultant, plaintiff attorney, trustee, and member of Congress evaluating the proposal.

For years, I have argued in CommonSense 401(k) Project that the movement to place private equity, private credit, insurance products, and other opaque investments into America’s retirement system has nothing to do with helping retirees, but to enrich Wall Street.

The NYU paper reaches many of the same concerns from an independent academic perspective.

They Ask the Right Question

The debate has often been framed incorrectly. Private-equity advocates ask:

“Should participants have access to private markets?” NYU instead asks:

“Who is this rule really protecting?” That distinction changes everything.

The Department of Labor describes the proposal as creating a neutral framework for fiduciaries evaluating alternative investments. Yet one of its central features is reducing litigation exposure for plan fiduciaries who follow prescribed procedures when selecting investments. Private Equity industry supporters argue this encourages innovation; consumer advocates contend it shifts legal protection toward fiduciaries and asset managers rather than participants by blocking transparency.

That concern has been at the center of nearly every article we have written on this issue.

Safe Harbors Are Not Investment Standards

One of the biggest problems with the proposed rule is philosophical.

ERISA was enacted to protect workers.

The proposed regulation instead spends enormous effort explaining how fiduciaries can protect themselves from litigation. It’s hidden objective seems to be hiding high fee high risk products to enrich Wall Street.

Instead, this DOL proposal appears willing to accept investments with:

subjective valuations,

limited liquidity,

non-standard performance reporting,

complex fee structures, and

benchmark methodologies unavailable in public markets.

That represents a lowering—not a raising—of investment standards.

The Missing Piece: Performance Integrity

The NYU article focuses heavily on fiduciary protection.

But there is an even deeper issue.

Private equity is unlike virtually every traditional investment offered inside 401(k) plans because performance itself often depends upon manager-generated valuations rather than continuously observable market prices.

The answer is simple. Greater opacity creates greater opportunities to capture fees that would be difficult to sustain in highly transparent mutual funds.

Private equity adds another layer:

management fees,

carried interest,

transaction fees,

monitoring fees,

portfolio-company expenses,

financing costs,

valuation discretion.

Participants frequently see only a fraction of the total economic cost.

The Department’s proposal asks fiduciaries to consider fees.

But unless those fees are fully observable, measuring them becomes extraordinarily difficult.

Transparency cannot be optional. Private Equity contracts will be buried in poor state regulated CIT’s, which will then be buried in another layer of poor state regulated CITs in a Target Date Fund.

Many of these questions remain difficult—even for sophisticated institutional investors.

Expecting ordinary 401(k) fiduciaries to answer them consistently is unrealistic. Current structures of non-transparent state CITs will make it impossible for fiduciaries to do this level of due diligence

The Business Model Depends Upon Information Gaps

One of our most controversial articles argued that much of private equity’s competitive advantage comes not from superior investment skill but from information asymmetry.

The combination includes:

limited transparency,

proprietary benchmarks,

subjective pricing,

confidential agreements,

limited disclosure,

complicated organizational structures.

Whether one agrees with that conclusion or not, it highlights why transparency matters.

Markets work best when participants can compare investments using common standards.

As a Trustee of a $20 billion plan I was not allowed to look at the Private Equity contracts. Staff knew if I did I would point out the hidden fees and clauses which violated state fiduciary laws.

Michael Goldhaber at NYU Stern deserves credit for reframing the debate.

Rather than asking whether private equity can enter 401(k) plans, they ask whether the Department of Labor’s proposal adequately protects the people ERISA was enacted to serve.

That is exactly the right question.

Our answer remains that participant protection requires more than procedural safe harbors. It requires investment standards built on transparent valuation, comparable performance measurement, complete fee disclosure, independent benchmarking, meaningful liquidity, and enforceable fiduciary accountability.

Until those standards exist, opening America’s retirement system to increasingly opaque private-market products risks protecting the industry’s expansion more effectively than the retirement security of the workers whose savings finance it.

The Department of Labor’s proposed rule assumes that fiduciaries can prudently evaluate private equity before placing it inside America’s retirement plans.

That assumption falls apart the moment one asks a simple question:

How many ERISA fiduciaries—or their attorneys—will actually be allowed to read the underlying private equity contracts?

As a Trustee of a $20billion Retirement fund, I was not allowed to see the underlying Private Equity Contracts.

In many modern target-date structures, the answer may effectively be none.

The private equity fund sits inside another investment vehicle.

That vehicle sits inside a state-regulated Collective Investment Trust (CIT).

That CIT is then buried inside another state-regulated target-date CIT.

The plan sponsor never contracts directly with Apollo, KKR, Carlyle, or Blackstone.

Instead, it owns units of a CIT that owns another CIT that owns a limited partnership.

By the time an ERISA fiduciary reaches the actual governing contract, the legal rights may already have disappeared.

The Missing Documents

The attached review of Apollo, Carlyle, and KKR partnership agreements demonstrates why these contracts matter.

They commonly give the General Partner:

unilateral valuation authority,

broad indemnification,

confidentiality protections,

authority to conduct parallel investment activities,

extensive conflict protections,

limited fiduciary liability.

The architecture is remarkably consistent.

Authority.

Valuation.

Indemnification.

Confidentiality.

Oversight comes later—if at all.

That alone should concern every ERISA attorney.

The 25 Percent Test

Many private equity funds contain provisions allowing substantial portions of the partnership to consist of non-ERISA investors.

Practitioners commonly refer to this as the “25 percent test” under the Department of Labor’s plan asset regulation, where benefit plan investor participation below certain thresholds can mean the underlying assets are not treated as ERISA plan assets.

If 80%, 90%, or 95% of investors are non-ERISA capital, the governing agreement may legitimately be written primarily for non-ERISA investors. Or to shield Private Equity from ERISA liability

The contract may permit provisions that would never appear inside an ERISA trust.

What Would a Good ERISA Lawyer Say?

Imagine handing an experienced ERISA attorney—not a securities lawyer—the actual limited partnership agreement.

The attorney reads provisions providing:

manager-controlled valuations;

broad exculpation clauses;

confidentiality restrictions;

affiliated transactions;

parallel funds;

limited fiduciary remedies.

Many attorneys would likely advise their client that these provisions deserve careful scrutiny under ERISA’s duties of prudence and loyalty before committing plan assets. Whether particular provisions violate ERISA would depend on the facts and legal analysis, but the contractual allocation of authority itself raises obvious fiduciary questions.

Unfortunately, most attorneys may never receive the documents.

The Intel Problem

That is why the Supreme Court’s decision in the Intel litigation matters so much.

the central issue extends beyond pleading standards.

It is about whether plaintiff attorneys can obtain the information necessary to determine whether fiduciaries actually acted prudently.

Without discovery:

the contracts remain hidden;

the side letters remain hidden;

the valuation procedures remain hidden;

the conflicts remain hidden.

If the governing documents cannot be examined, meaningful fiduciary review becomes extraordinarily difficult.

The Perfect Shield

The Department of Labor proposes allowing private equity inside target-date funds.

State banking regulators oversee the CIT.

The private equity manager invokes contractual confidentiality.

The plan sponsor receives only summary information.

Participants receive even less.

The plaintiff’s attorney cannot obtain the governing documents until after years of litigation—if ever.

Every layer adds another barrier to transparency.

Every layer makes fiduciary review more difficult.

Every layer weakens ERISA’s promise of accountability.

ERISA Was Never Intended to Operate Blindfolded

ERISA is built on informed fiduciary judgment.

That judgment becomes impossible when the governing documents cannot be examined.

If fiduciaries cannot read the contracts…

If participants cannot read the contracts…

If regulators rarely review the contracts…

If plaintiff attorneys cannot obtain the contracts…

…then the Department of Labor is asking fiduciaries to certify prudence based largely on trust.

That is not the ERISA Congress enacted.

It is an invitation to substitute opacity for diligence.

Before private equity is allowed inside America’s retirement plans, the Department of Labor should answer one basic question:

Will every ERISA fiduciary, every participant, and every plaintiff’s attorney have meaningful access to the governing contracts before retirement assets are committed?

If the answer is no, then the rule risks protecting secrecy as much as it protects investment flexibility.

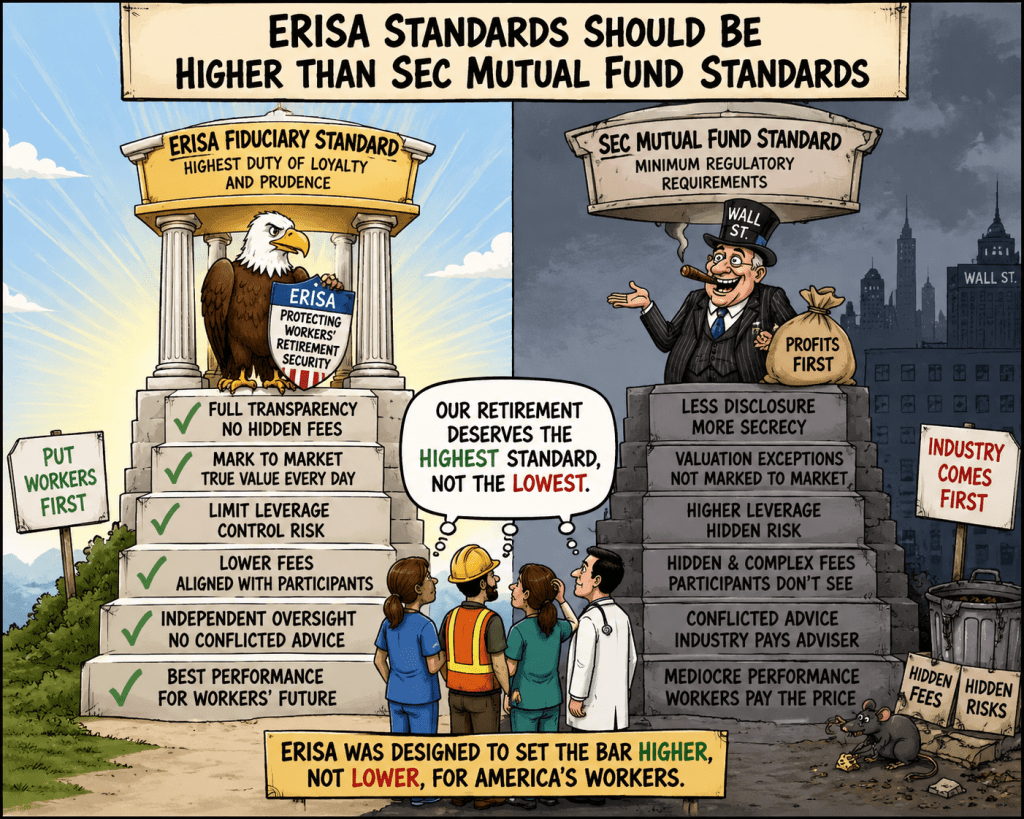

That should mean ERISA investments are held to standards at least as strong as those governing SEC-registered mutual funds. In reality, Wall Street, private-equity firms, insurers, consultants, and asset managers are pushing for the opposite. They want retirement plans to admit investments that could not meet the accounting, valuation, liquidity, fee, and performance standards ordinarily expected of a mutual fund.

They especially want to place those investments inside target-date funds, where millions of participants will receive them automatically through a qualified default investment alternative without understanding what they own. The emerging target-date fund could contain: – private equity valued by the private-equity manager; – private credit valued by the lender that originated the loan; – cryptocurrency subject to extreme price volatility and custody risks; – fixed annuities valued according to insurer contract terms; – lifetime-income products whose true economic cost is obscured by actuarial assumptions; – collective investment trusts with less public disclosure than mutual funds; and – publicly traded stocks and bonds valued at observable market prices. All these assets would then be combined into one fund, assigned one net asset value, compared with one benchmark, and advertised using one performance number. That is not a higher fiduciary standard. It is an invitation to accounting chaos. https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/

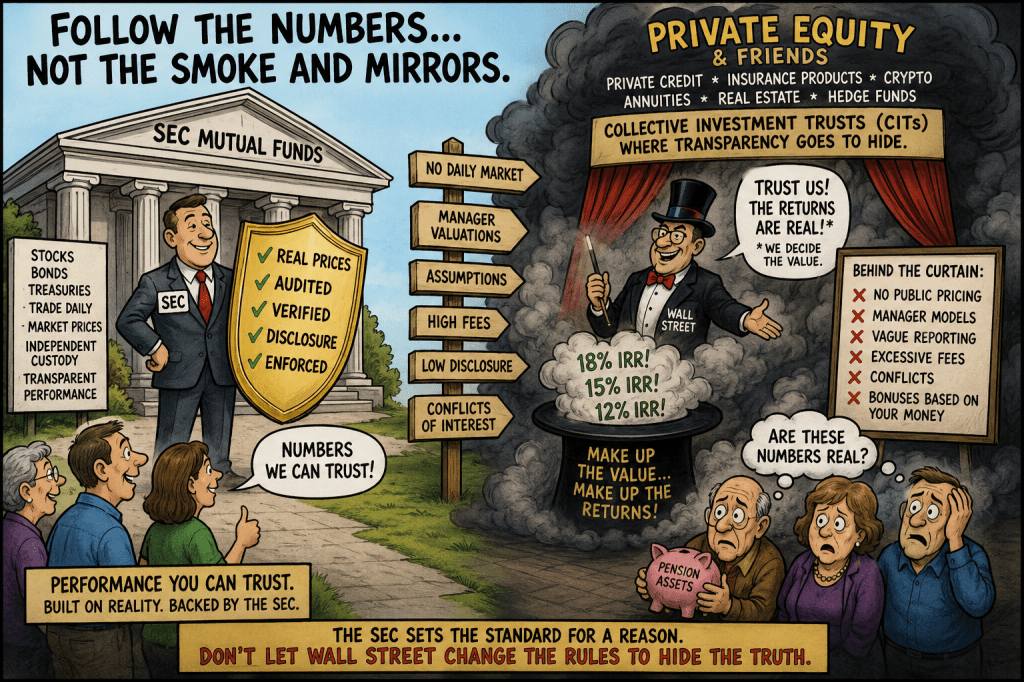

The Mutual-Fund Standard Begins With Market Value An SEC-registered mutual fund normally values publicly traded securities using current market quotations. When reliable quotations are not readily available, the fund must use a formal fair-value process. The valuation must be conducted in good faith, subject to documented procedures, risk assessment, methodology testing, pricing-service oversight, recordkeeping, and board supervision. The objective is to estimate what an asset could reasonably be sold for in an orderly transaction between market participants.

That does not mean mutual-fund valuation is perfect. Thinly traded bonds, complex derivatives, and unusual securities can still involve judgment. But the process begins with the correct economic question: What is this investment worth today? The proposed ERISA approach increasingly begins with a different question: What number can the manager or insurer report without recognizing the current loss? That distinction is fundamental. A market-based system recognizes that values rise and fall. A manager-controlled system often allows losses to be delayed, smoothed, modeled away, hidden in assumptions, or shifted into future crediting rates and withdrawal restrictions.

SEC Exceptions Are Narrow, Not General Permission to Ignore Markets The investment industry may point to limited SEC accounting exceptions, such as the treatment of certain money-market funds, to argue that market pricing is not always required. But those exceptions prove the rule rather than undermine it. Money-market accounting accommodations were designed for narrowly constrained portfolios of short-term, highly liquid instruments. They are accompanied by detailed requirements governing maturity, liquidity, diversification, credit quality, stress testing, oversight, and disclosure. The theory is that amortized cost can remain close to current market value when the assets are short term and relatively stable. Even then, the SEC has repeatedly tightened money-market rules when experience showed that stable accounting could conceal real risks.

A narrow rule for short-term liquid instruments cannot reasonably justify carrying a ten-year private loan at par. It cannot justify allowing a private-equity sponsor to determine the reported value of a company it owns. It cannot justify treating an insurer’s contractual promise as though it were equivalent to cash. It cannot justify hiding complex lifetime-income guarantees inside a target-date fund. And it cannot justify using stale or manager-created valuations to report lower volatility and higher apparent risk-adjusted returns. ## Private Equity Marks Its Own Homework Private-equity funds generally do not have daily market prices.

The private-equity manager controls the investment, receives management fees, may receive carried interest tied to performance, and plays a central role in determining the reported value of the portfolio company. That creates an unavoidable conflict. The manager benefits when reported values are higher. Higher values can produce better performance rankings, additional fundraising, larger bonuses, more carried interest, and favorable comparisons with public markets. Valuation committees, outside consultants, and auditors may review the process, but they ordinarily do not create an actual market transaction. An audited estimate remains an estimate. The fact that an accounting firm reviewed a manager’s assumptions does not mean the asset could be sold for the reported price. Private-equity funds frequently rely on: – comparable-company multiples; – projected earnings; – adjusted earnings before interest, taxes, depreciation, and amortization; – discounted cash-flow models; – prior financing rounds; – manager-selected peers; – acquisition-cost anchors; and – assumptions about future exits. Each assumption creates discretion. A small change in the selected earnings figure, valuation multiple, discount rate, or projected exit date can materially change the reported value. Public stocks receive prices from actual buyers and sellers. Private equity receives a model from the firm being paid to manage it. Those numbers should not be treated as equivalent.

Private Credit Has the Same Conflict Private credit is often marketed as safer and less volatile than public bonds. Much of that apparent stability comes from accounting manipulation. A publicly traded bond can fall immediately when interest rates rise, credit spreads widen, the borrower deteriorates, or investors demand more compensation for risk. A private loan may remain near par because the lender or affiliated manager continues to value it near par. The economic risk may have increased dramatically even though the reported price barely moves. A private-credit manager may originate the loan, collect origination and management fees, negotiate amendments, waive covenants, extend maturities, capitalize unpaid interest, and determine whether the borrower should be treated as impaired. The same manager can then report the loan’s value. That is not market discipline. It is lender-controlled accounting. The lack of visible volatility does not prove the lack of risk. It may merely prove the lack of trading. Private credit can appear to diversify a target-date fund because its values move slowly compared with public markets. But slowly reported values are not the same as stable economic values. Mixing private credit with public bonds can manufacture the appearance of lower correlation, lower volatility, and superior downside protection. That is a fraudulent accounting diversification, not investment diversification.

Fixed Annuities Are Accounting Promises, Not Transparent Portfolios A fixed annuity is frequently described as safe because the participant’s account balance does not fluctuate like a mutual fund. But the visible account value is a contractual figure, not necessarily the current economic value of the contract. The participant usually does not own the insurer’s underlying bonds, mortgages, structured securities, private loans, real estate debt, or affiliated investments. The insurer owns those assets. The participant owns a promise from the insurer. The insurer controls: – the asset allocation; – the amount of private credit; – the use of affiliated investments; – the crediting rate; – the retained spread; – the reserve assumptions; – the surrender rules; – the transfer restrictions; – the market-value adjustment; – the payment schedule; and – much of the information available to the plan fiduciary. A contract may show a value of $100 even though an economically equivalent market sale, surrender, or replacement would produce substantially less. The loss has not disappeared. It may be embedded in: – a below-market crediting rate; – surrender charges; – installment-payment provisions; – withdrawal restrictions; – employer-initiated-event clauses; – a market-value adjustment; – illiquidity; – or the insurer’s retained spread. Reporting the contract at $100 does not establish that it is worth $100.

Lifetime Annuities Are Even Harder to Measure Lifetime-income products create additional valuation problems. The apparent value of a lifetime annuity depends on assumptions involving: – interest rates; – mortality; – longevity; – insurer expenses; – insurer profit margins; – adverse selection; – lapse behavior; – optional benefits; – inflation; – guarantee periods; – beneficiary provisions; and – insurer credit risk. Two annuities can promise similar monthly payments while having materially different economic values because of differences in insurer strength, contract terms, liquidity, downgrade protections, state guaranty-association exposure, mortality assumptions, and embedded fees. The participant often cannot transfer or resell the annuity. Once purchased, the transaction may be irreversible. That makes the initial valuation and fiduciary review more important, not less. Yet insurers rarely disclose the full economic spread between: – the assets supporting the annuity; – the expected cost of benefit payments; – the value of participant guarantees; – the insurer’s expenses; – the insurer’s capital charge; and – the insurer’s expected profit. The monthly payment is presented as the product. The undisclosed spread is the price.

Target-Date Funds Turn Incompatible Valuation Systems Into One Number A target-date fund containing public securities, private equity, private credit, crypto, fixed annuities, and lifetime-income contracts could combine several incompatible accounting systems. Public stocks may be valued at closing market prices. Public bonds may be valued through observable market transactions or pricing services. Private equity may be valued quarterly using manager models. Private credit may be held near par despite deteriorating secondary-market conditions. Crypto may trade continuously across fragmented exchanges. Fixed annuities may be reported using contract values. Lifetime-income guarantees may be valued through actuarial models that are largely invisible to participants. The target-date fund then blends all of these into one reported return. The result looks mathematically precise. It may be economically meaningless. A participant could be shown a return of 7.42%, but that number may combine: – actual market gains; – unrecognized private-asset losses; – stale quarterly values; – insurer-declared crediting rates; – modeled annuity values; – delayed impairments; – accrued but unpaid interest; – and benchmark assumptions selected by the manager. No ordinary investor could reconstruct the calculation. Many plan fiduciaries could not reconstruct it either.

Smoothing Can Manufacture Superior Performance Private assets and insurance contracts tend to report smoother returns than publicly traded securities. That smoothness is often presented as evidence of lower risk. But an investment can appear less volatile simply because it is valued less frequently or because losses are recognized more slowly. Suppose public markets decline by 20%. The public holdings inside a target-date fund recognize the decline immediately. The private-equity sleeve may use a valuation from months earlier or a model that reflects only part of the decline. The private-credit sleeve may remain near par despite widening credit spreads. The fixed-annuity sleeve may continue reporting contract value. The lifetime-income sleeve may be valued under assumptions that change only periodically. The target-date fund will appear to fall less than a fully market-valued portfolio. That does not prove that it suffered less economic damage. It may merely mean that less of the damage was reported. This accounting lag can improve apparent: – downside capture; – volatility; – Sharpe ratios; – maximum drawdowns; – correlations; – diversification; – and benchmark-relative performance. The fund may therefore look safer precisely because its least transparent assets are not being measured on the same basis as its public assets. ## Benchmarks Become Misleading A benchmark is meaningful only when the investment and benchmark are measured on comparable terms. A public-stock index is marked to market. A public-bond index is marked to market. A target-date fund containing private assets and insurance contracts may not be. If the benchmark recognizes losses immediately while the fund delays them, the fund can report artificial outperformance. Private-equity managers also frequently use internal rates of return, while public-market benchmarks generally use time-weighted returns. Private credit may be compared with public bonds even though the private loans are not marked with the same frequency or market sensitivity. Annuity crediting rates may be compared with bond-fund returns even though the annuity return omits the current market value of the underlying insurance promise. These comparisons mix different accounting rules, different liquidity, different timing, and different risk. The resulting excess return may be nothing more than excess discretion.

Target-Date Funds Eliminate Participant Consent Participants already have difficulty understanding target-date funds composed of conventional stocks and bonds. Once private equity, private credit, crypto, and annuities are added, meaningful understanding becomes nearly impossible. Participants may not know: – which private-equity funds are included; – which companies those funds own; – how those companies are valued; – what private loans are held; – whether the loans are impaired; – how much crypto exposure exists; – which exchange or custodian is used; – which insurer issued the annuity; – what assets support the insurance promise; – what surrender restrictions apply; – how much the insurer retains as a spread; – or what happens if the target-date manager removes or replaces the investment. The participant sees one fund name. The participant receives one fact sheet. The participant is shown one performance number. The complexity is hidden inside the package. That is especially troubling because target-date funds are commonly used as default investments. Participants may be placed into them because they made no investment election. Silence is being treated as consent to private equity, private credit, crypto, and insurance products. That is not informed choice. ## Complexity Makes Fiduciary Monitoring Weaker ERISA fiduciaries are required to act prudently and solely in the interest of participants. But complexity often weakens fiduciary oversight. A plan committee may rely on: – the target-date manager; – the recordkeeper; – the investment consultant; – the insurer; – the private-equity sponsor; – the private-credit manager; – the valuation firm; – and the auditor. Each adviser reviews only part of the structure. No one may accept responsibility for the combined economic result. The consultant may say the valuations came from the manager. The manager may say they followed industry standards. The auditor may say it tested compliance with accounting procedures rather than determining actual market value. The insurer may say the crediting rate complied with the contract. The fiduciary committee may then claim it relied on experts. That is how responsibility disappears. The more opaque the target-date fund becomes, the easier it is for every adviser to point to someone else.

Fees Become Almost Impossible to Identify Mutual funds disclose expense ratios. That disclosure may be incomplete in some respects, but it provides a common starting point. A target-date fund containing private assets and annuities can have multiple layers of compensation that do not appear clearly in the headline fee. Private equity may charge: – management fees; – carried interest; – transaction fees; – monitoring fees; – portfolio-company fees; – financing fees; – and expenses charged through underlying entities. Private credit may charge: – management fees; – origination fees; – amendment fees; – structuring fees; – prepayment fees; – servicing fees; – and performance compensation. Crypto may involve: – custody fees; – trading spreads; – fund expenses; – staking arrangements; – and exchange costs. Annuities may impose: – insurer spreads; – mortality and expense charges; – administrative expenses; – surrender charges; – market-value adjustments; – distribution compensation; – and embedded profits that are not described as fees. The target-date fund may then charge another management fee on top of all the underlying costs. A participant may see a reported expense ratio that captures only a fraction of the true economic cost. ## ERISA Standards Should Be Stronger ERISA should not permit an investment to receive weaker accounting, valuation, liquidity, or disclosure treatment merely because it is placed inside a retirement plan. At a minimum, any target-date fund containing private equity, private credit, crypto, fixed annuities, or lifetime-income products should be required to provide the following. ### Current Economic Value Every investment should disclose a reasonable estimate of current realizable value. Historical cost, contract value, manager net asset value, actuarial value, and declared account value should not substitute for an estimate of what the investment is economically worth today.

Separate Reporting by Valuation Method Performance should be broken out according to whether assets are: – exchange traded; – priced through observable market data; – valued by an independent third party; – valued by the investment manager; – carried at contract value; – valued through actuarial assumptions; – or valued using stale information. A single blended return should not conceal fundamentally different valuation systems. ### Comparable Benchmarks Private assets should not be permitted to claim outperformance against public indexes unless the comparison adjusts for valuation lag, leverage, liquidity, fees, and methodology. Annuity crediting rates should not be compared with market-valued bond returns without recognizing the economic value of the contract and the insurer spread.

Full Look-Through Fee Disclosure Plans should disclose every material layer of fees, spreads, carried interest, insurance profits, transaction costs, affiliate payments, and underlying fund expenses. Calling compensation a spread does not make it free. ### Liquidity and Exit Disclosure Participants and fiduciaries should know: – whether an asset can be sold; – who can buy it; – how long a sale could take; – what discount may be required; – whether withdrawals can be suspended; – whether the insurer can pay in installments; – whether the manager can restrict redemptions; – and whether the reported value differs materially from likely exit value.

Independent Valuation A manager should not have primary authority to value the same assets on which its fees and performance compensation depend. Material private assets should be valued using truly independent processes, with disclosure of disagreements between the manager, independent valuer, auditor, and secondary-market evidence. ### No Accounting Blending Target-date funds should not be allowed to combine market-priced assets, manager-priced assets, contract-valued insurance products, and actuarially valued guarantees into one performance number without detailed reconciliation. The participant should be able to see how much of the reported return came from actual market prices and how much came from models, assumptions, smoothing, and manager judgment.

Mutual-Fund Eligibility Should Be the Floor The retirement industry has often treated ERISA plans as a laboratory for products that could not gain acceptance in ordinary mutual funds. That principle should be reversed. A useful starting rule would be: > If an investment cannot meet the valuation, liquidity, fee, accounting, and disclosure standards expected of an SEC-registered mutual fund, it should face a presumption against inclusion in an ERISA target-date fund. That does not mean every retirement investment must literally be organized as a mutual fund. It means the mutual-fund standard should be the regulatory floor, not the ceiling. A product should not qualify for weaker oversight merely because it is held through: – a collective investment trust; – an insurance company separate account; – an insurance company general account; – a private partnership; – a limited liability company; – a pooled employer plan; – or a target-date fund. Changing the legal wrapper does not change the economic risk.

Target-Date Funds Should Be Simpler Than Individual Choice Menus A target-date fund is supposed to simplify retirement investing. Adding private equity, private credit, crypto, and annuities does the opposite. The participant is no longer buying a diversified portfolio of transparent stocks and bonds. The participant is buying a chain of trusts, partnerships, contracts, guarantees, valuation models, fee arrangements, and withdrawal restrictions. A participant could never independently reproduce or evaluate the portfolio. That should be viewed as a fiduciary defect, not an innovation. Complex products may generate higher fees for Wall Street, but they do not necessarily generate better retirement outcomes. ## The Real Purpose Is Distribution Private-equity firms want access to the enormous defined-contribution market. Private-credit managers need new buyers as the market expands. Crypto firms want retirement-plan legitimacy and a stable source of inflows. Insurers want annuities embedded into defaults because most participants will never actively choose them. Target-date funds provide the ideal distribution mechanism. Once an asset is embedded in a default fund, the provider no longer needs to persuade each participant. The provider needs only to persuade: – the target-date manager; – the recordkeeper; – the consultant; – the insurer; – the plan sponsor; – or a regulator. One institutional decision can direct billions of dollars into products that participants may not understand and never affirmatively selected. The complexity benefits the seller. The opacity protects the fees. The accounting smooths the performance. The target-date wrapper delivers the customers. ## The Fiduciary Rule Should Be Simple Workers should not receive lower investment protections because their money is held inside an ERISA plan. They should receive higher protections. ERISA target-date funds should therefore be required to meet standards stronger than those governing ordinary mutual funds, including: – current and independently supportable valuations; – complete fee and spread disclosure; – market-based performance reporting; – comparable benchmarks; – daily or clearly disclosed liquidity; – transparent ownership; – visible counterparty exposure; – and understandable participant communications. Private equity, private credit, crypto, fixed annuities, and lifetime-income products should not receive a regulatory shortcut simply because Wall Street places them inside a target-date fund. The governing principle should be: > **If the investment cannot withstand mutual-fund-level scrutiny, it should not be hidden inside the default retirement investment of an American worker.

Target-date funds should protect participants from complexity. They should not be used to conceal it. :::

Addendum: Collective Investment Trusts Should Not Become the Regulatory Escape Hatch

The movement away from SEC-registered mutual funds and toward Collective Investment Trusts (“CITs”) is often marketed as a way to reduce expenses. It has for some Vanguard and Fidelity funds.

Increasingly, however, CITs are becoming something far different—a regulatory escape hatch through which Wall Street can introduce products that would face far greater scrutiny inside an SEC mutual fund.

Originally, CITs were simple institutional pooled trusts investing primarily in publicly traded stocks and bonds. They generally mirrored mutual funds while avoiding certain retail regulatory costs.

That model is changing rapidly.

Today’s target-date CITs increasingly provide a convenient structure for investments that are difficult to value, difficult to benchmark, difficult to monitor, and difficult for participants to understand.

Unlike SEC mutual funds, CITs generally:

are not registered under the Investment Company Act of 1940;

do not issue SEC prospectuses;

are not subject to the same shareholder reporting requirements;

often disclose far less portfolio information;

frequently provide less detailed fee disclosure;

may rely upon confidential trust documents unavailable to participants; and

often disclose holdings only quarterly or even less frequently.

None of those characteristics necessarily make a CIT imprudent.

But they become dangerous when combined with opaque investments.

Lower Disclosure Encourages Higher Risk

The SEC mutual-fund framework developed over decades around one central principle:

Investors should know what they own.

The current movement toward state-regulated CITs increasingly produces the opposite result.

Participants frequently cannot determine:

the underlying private-equity partnerships;

the private-credit funds;

leverage employed by underlying managers;

insurance contracts;

affiliated transactions;

valuation methodologies;

secondary-market pricing;

carried interest;

performance fees;

insurer spreads; or

other embedded compensation.

Instead, participants receive a target-date fund fact sheet showing only a single allocation and a single performance number.

The complexity disappears from view.

The risk does not.

Hidden Leverage Creates Hidden Risk

Leverage magnifies both gains and losses.

Public mutual funds generally disclose leverage in financial statements and regulatory filings.

Private markets frequently embed leverage at multiple levels simultaneously.

A target-date CIT can unknowingly expose participants to:

leverage at the portfolio company;

leverage inside private-equity funds;

subscription credit facilities;

leverage inside private-credit vehicles;

leverage employed by real estate funds;

leverage inside infrastructure investments;

derivative exposure;

securities financing transactions; and

leverage employed by insurance companies supporting annuity guarantees.

A participant reviewing a target-date fact sheet rarely sees this aggregate exposure.

The participant may believe the fund owns a diversified portfolio.

In reality, portions of that portfolio may already be highly leveraged before the target-date manager even purchases them.

The result is leverage stacked upon leverage.

Hidden Fees Are Just as Dangerous

The migration from mutual funds to CITs has also weakened fee transparency.

Mutual funds generally report a readily identifiable expense ratio.

CITs increasingly layer compensation throughout the investment structure.

Participants may indirectly pay:

target-date management fees;

underlying CIT management fees;

private-equity management fees;

carried interest;

monitoring fees;

transaction fees;

consulting fees;

placement-agent compensation;

insurance spreads;

affiliate profits;

servicing fees;

administration fees;

financing costs; and

portfolio-company expenses.

Many of these costs never appear in the participant’s stated expense ratio.

Instead, they reduce investment returns invisibly.

From an economic standpoint, a hidden spread deducted before returns are credited is no different than an explicit fee deducted afterward.

ERISA should recognize both as plan expenses requiring full fiduciary review.

Lower Standards Should Never Follow a Different Legal Structure

Changing an investment’s legal wrapper should not reduce fiduciary protections.

Yet that is precisely the direction the industry is moving.

Assets that may not fit comfortably inside an SEC mutual fund increasingly migrate into:

Collective Investment Trusts;

insurance separate accounts;

insurance general accounts;

private partnerships;

private funds;

limited liability companies; and

other exempt investment vehicles.

Each step away from SEC regulation generally reduces public transparency.

Participants know less.

Fiduciaries often know less.

Regulators receive less standardized information.

Meanwhile, investment complexity increases.

That is the opposite of what ERISA should encourage.

The Burden Should Increase—Not Decrease

The more opaque an investment becomes, the greater the fiduciary obligation should be.

Instead, today’s regulatory structure often produces the opposite result.

The least transparent investments frequently receive:

the weakest disclosure;

the weakest valuation standards;

the weakest performance comparisons;

the weakest fee transparency;

the weakest liquidity disclosure; and

the weakest participant understanding.

That inversion of regulatory priorities makes no sense.

The burden of proof should rest with the product sponsor.

If a private-market investment, insurance product, or highly leveraged strategy cannot satisfy disclosure and valuation standards comparable to those governing SEC mutual funds, it should not be admitted into an ERISA target-date fund simply because it has been placed inside a Collective Investment Trust.

We did not discuss stock picking, interest rates, or the latest hot investment strategy. Instead, we discussed something far more fundamental:

Can investors even trust the performance numbers they are being shown?

That question should be at the center of every fiduciary discussion in America.

For decades, the investment industry has quietly relied on one enormous advantage that most investors never think about.

SEC-registered mutual funds operate under real performance standards.

Most alternative investments do not.

As I explained during the interview, performance measurement is not simply calculating a percentage return. Performance depends upon accounting standards, valuation standards, fee disclosure standards, and regulatory enforcement. Those are exactly the areas where private equity, private credit, insurance products, and many state regulated Collective Investment Trusts (CITs) begin to diverge sharply from SEC-regulated mutual funds.

Mutual Funds Have Something Wall Street Hates

The SEC spent decades building an ecosystem where investment performance is tied to verifiable market values and sound accounting principles.

Mutual funds generally own securities that trade every day. Stocks trade. Treasuries trade. Corporate bonds trade. Market prices exist.

The system is not perfect. But investors know the numbers come from actual market prices—not from managers deciding what they think their investments are worth.

That is why SEC mutual funds have become the gold standard for investment performance.

Private Equity Begins With a Different Assumption

Private equity starts with an entirely different premise.

Most portfolio companies do not trade.

No daily market exists.

Managers determine valuations using internal models.

Consultants and plans blindly accept those valuations.

Auditors verify only whether the methodology was followed—not whether the valuation reflects what an outside buyer would actually pay.

Those internally generated values then become the foundation for:

reported returns

IRRs

manager rankings

consultant recommendations

executive bonuses

performance fees

The entire chain depends on valuations that often cannot be independently observed.

That does not mean every valuation is fraudulent. But it does mean the reported performance is much more dependent on judgment than the performance of publicly traded securities.

Oxford Is Asking the Same Questions

Oxford Professor Ludovic Phalippou has spent years examining private equity performance reporting.

His recent work argues that many headline returns substantially overstate the economic returns ultimately received by investors. Using different but economically grounded measures, he concludes that some of the industry’s largest firms produced returns roughly half of widely promoted figures. https://ludovicphalippou.substack.com/p/big-boys-returns

When changing the measurement system can cut reported returns in half, fiduciaries should ask whether they fully understand what those numbers represent.

SEC Mutual Funds Prevent Many of These Problems

There is a reason the SEC generally does not permit traditional private equity funds inside ordinary registered mutual funds.

The regulatory framework for registered funds emphasizes liquidity, valuation, disclosure, diversification, and pricing requirements that are difficult for many traditional private-market investments to satisfy.

The practical effect is simple.

Most retirement investors holding mutual funds receive performance based largely on observable market prices.

Once fiduciaries move into private markets, valuations increasingly depend upon manager estimates.

That difference matters.

Why the Industry Is Moving Toward State CITs

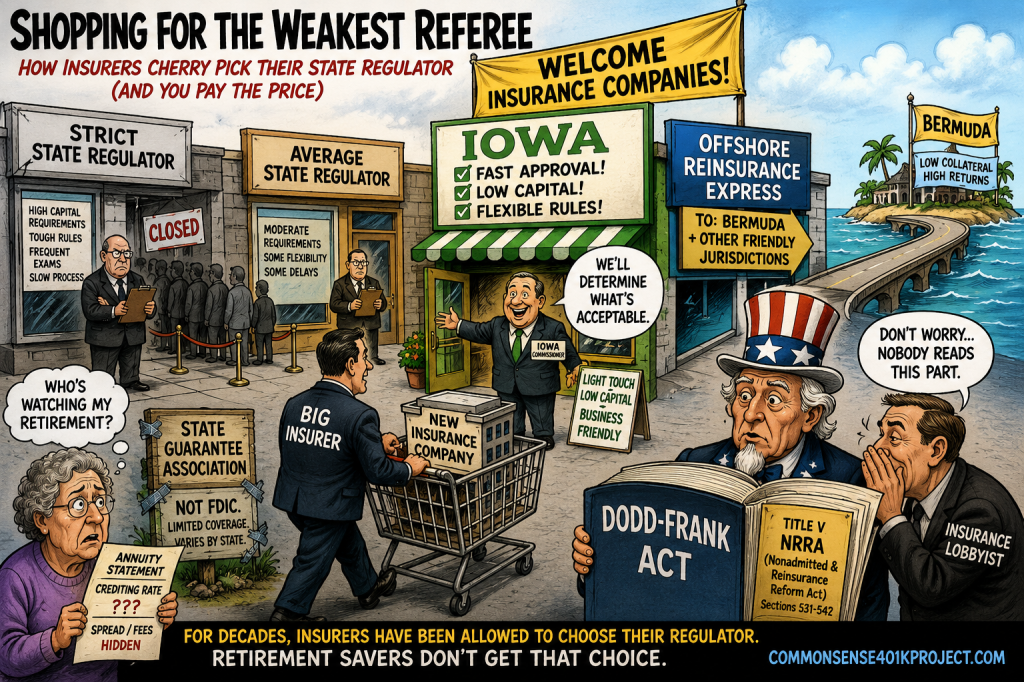

Federal regulation, like the SEC and the OCC regulated CITs tend to have solid rules and staff with some knowledge of the rules. Private Equity has gone the route of Annuities pick the weakest state regulator of 50. These then become state banking commissioners instead of state insurance commissioners. https://commonsense401kproject.com/2026/07/21/annuities-cherry-pick-the-weakest-state-regulator/ But the same principles apply little or no rules and a small unknowledgeable staff who do not know or care what type of assets go into their CITs much less understand performance or valuation issues.

Collective Investment Trusts (CITs) have become the preferred delivery mechanism for investments that would be difficult—or impossible—to package inside a traditional mutual fund.

When combined with private equity, private credit, insurance contracts, and other difficult-to-value assets, the result is a retirement marketplace where participants receive far less information than they would receive in a comparable SEC mutual fund.

In my view, this migration deserves much greater scrutiny because it reduces transparency precisely where independent verification is most difficult.

Ohio STRS Shows Why Standards Matter

The Ohio STRS controversy demonstrates why performance methodology matters.

State Pensions are not covered by Federal Pension Standards ERISA, so the state essentially makes it up its own rules so very difficult to prove any violations of law.

Performance standards influence real money.

Bonuses.

Manager selection.

Consultant evaluations.

Public confidence.

If performance calculations can materially change outcomes, fiduciaries should understand precisely how those calculations are produced.

GIPS Is Helpful—but Not Enough

Many plans and consultants point to CFA Institute’s Global Investment Performance Standards (GIPS).

GIPS has unquestionably improved consistency in performance reporting.

But GIPS is fundamentally a reporting framework.

It does not itself verify private valuations or enforce compliance in the way a regulator does.

The investment industry increasingly portrays SEC mutual funds as outdated while marketing private equity, private credit, insurance products, and opaque Collective Investment Trusts as the future of retirement investing.

I see it differently. The greatest strength of SEC mutual funds is not simply low cost. It is trust.

Their performance is built on transparent accounting, market pricing, standardized disclosure, and decades of regulatory oversight.

When retirement assets migrate into vehicles where valuations become increasingly subjective, fiduciaries should recognize that they are also leaving behind the strongest performance framework investors have ever had.

Performance is only meaningful if investors can trust how it was measured.

And that may be the biggest investment issue almost nobody is discussing today.

This article expands on themes discussed in my recent interview with Jeffrey Snyder of the Broadcast Retirement Network regarding SEC mutual fund standards, private-market performance measurement, and fiduciary responsibility. The interview emphasized the importance of looking “under the hood” of reported investment returns rather than relying solely on headline performance figures. Full transcript of interview at https://www.thestreet.com/retirement/sec-mutual-funds-the-performance-standard-you-can-actually-trust

Appendix: Why Traditional Private Equity Performance Measures Overstate Skill

A CFA Framework for Understanding the Performance Illusion

One of the recurring defenses offered by the private equity industry is that its performance has been “proven” by decades of academic research using Public Market Equivalent (PME), IRR, TVPI, and similar metrics.

Unfortunately, those measures are far less objective than they appear.

Many of the industry’s favorite performance statistics systematically overstate manager skill because they fail to properly adjust for risk.

The issue is remarkably similar to evaluating a hedge fund using Treasury bills as the benchmark. If the benchmark understates the risk being taken, ordinary leverage begins to masquerade as investment genius.

The Hidden Assumption Inside PME

Most institutional investors have heard of Kaplan-Schoar PME.

It has become one of the industry’s standard methods for comparing private equity against public markets.

What relatively few trustees understand is that the methodology effectively assumes a market beta of approximately 1.0.

Buyout funds, however, generally operate with substantially more leverage than ordinary public companies.

Story demonstrates that once buyout leverage is properly recognized, the effective beta is closer to 1.2–1.4 rather than 1.0.

That seemingly small difference has enormous consequences.

If the benchmark assumes too little risk, then leverage itself is incorrectly recorded as manager skill.

Leverage Is Not Alpha

Imagine two investors.

One buys a diversified public equity portfolio.

The other borrows heavily and buys essentially the same companies.

If both produce higher returns because one employed leverage, few would call that investment genius.

Yet that is effectively what happens in many traditional private equity performance comparisons.

The leverage premium becomes “alpha.”

Once benchmarks are adjusted for comparable leverage and style exposure, most of the apparent excess return disappears.

The Benchmark Matters

Another weakness is benchmark selection.

Many studies compare buyout funds against broad indices such as the S&P 500.

But buyout targets tend to resemble smaller, value-oriented companies.

A more appropriate benchmark is therefore a leveraged small-cap value portfolio rather than a large-cap index.

Once that comparison is made, the excess performance largely vanishes.

This finding is consistent with work by Ludovic Phalippou, Erik Stafford, L’Her and others, who conclude that much of buyout performance can be replicated using inexpensive public securities combined with leverage.

Direct Alpha Tells a Different Story

Traditional presentations often emphasize IRRs and multiples because they look impressive.

Data shows that Direct Alpha—a metric designed to compare private equity against a properly risk-matched benchmark—often produces dramatically different conclusions.

His worked example is revealing:

Compared with the S&P 500:

Direct Alpha = +0.96%

Compared with a style-matched benchmark:

Direct Alpha ≈ 0.10%

Compared with a properly risk-adjusted leveraged benchmark:

Direct Alpha = –0.34%

Nothing about the fund changed.

Only the benchmark changed.

The apparent “alpha” disappeared.

Why This Matters for Public Pension Bonuses

This has enormous implications for public pension systems.

Many pension staffs receive bonuses for outperforming benchmark portfolios.

But if the benchmark fails to recognize the additional leverage and systematic risk embedded in private equity, then employees may be rewarded simply for taking more risk—not for producing genuine investment skill.

That is exactly the concern raised repeatedly in this article.

The accounting methodology itself can manufacture alpha where none actually exists.

ERISA Should Demand Better

For ERISA fiduciaries, the implications are even more significant.

ERISA has never rewarded managers merely for increasing risk.

The prudent fiduciary standard has always required evaluating returns relative to the risks undertaken.

If private equity benchmarks ignore leverage, ignore style effects, or otherwise understate risk, then fiduciaries may be relying on performance measures that systematically exaggerate investment success.

A prudent fiduciary should insist on:

Risk-adjusted benchmarks.

Transparent leverage assumptions.

Comparable public-market alternatives.

Direct Alpha or equivalent risk-adjusted measures.

Independent verification rather than marketing presentations.

The Bigger Picture

This article has argued that much of private equity’s reported superiority rests on accounting conventions rather than economic reality.

This technical framework reaches much the same conclusion through an entirely different route.

His work does not argue that every private equity investment underperforms.

Rather, it demonstrates that once leverage, size, value, and systematic risk are properly priced, the industry’s long-claimed “persistent alpha” becomes difficult to find.

That is precisely why pension trustees, ERISA fiduciaries, auditors, and regulators should stop asking whether private equity beat the S&P 500.

They should instead ask the much harder—and much more important—question:

Did it beat a public portfolio carrying the same risks?

If the answer is no, then billions of dollars of performance fees, carried interest, staff bonuses, and public narratives about private equity “outperformance” deserve to be reconsidered.

The Risky Insurance paper provides an important independent confirmation of the argument Thomas Lambert and I made in our March 2026 Journal of Economic Issues article, “‘Safe’ Annuity Retirement Products and Possible Future U.S. Retirement Risks, Threats, and Shortfalls.” https://doi.org/10.1080/00213624.2026.2613361

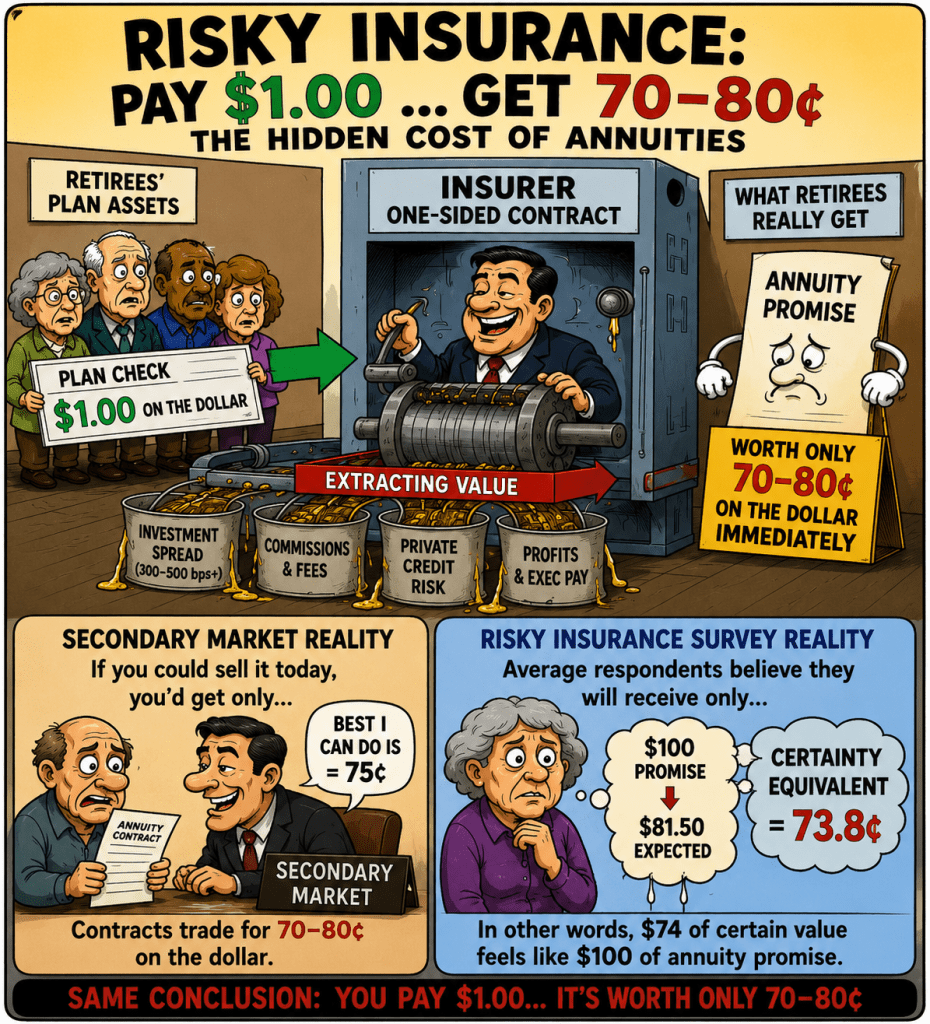

Our paper argues that an annuity’s reported book value is not the same thing as its economic value. An insurer may report a contract at 100 cents on the dollar because the customer is not permitted to demand the underlying assets, sell the contract freely, or force the insurer to mark the obligation to market. But when actual buyers are asked what they would pay for the contract—or when consumers are asked what certain payment they would accept in exchange for the insurer’s uncertain promise—the value can fall toward 70 to 80 cents on the dollar.

The new NBER paper makes that argument much harder to dismiss.

Three Different Roads Lead to Roughly the Same 70-to-80-Cent Valuation

There are now at least three distinct ways to observe the economic discount hidden beneath annuity book-value accounting.

Valuation method

Indicated economic value

Consumers’ expected annuity payout in the NBER survey

81.5 cents per promised dollar

Consumers’ annuity certainty equivalent

73.8 cents per promised dollar

Secondary-market pricing cited in Lambert–Tobe

Often approximately 80 cents per contract dollar

Current stressed private-credit exits and tender prices

Frequently 70–85 cents per reported NAV

These are not identical measurements and should not be mechanically treated as interchangeable. But they point in the same direction: a contractual or accounting value of $1 may conceal an economic value closer to $0.70–$0.80 once liquidity, uncertainty, credit risk, contract restrictions, and the cost of immediate exit are recognized.

Our Paper Already Identified the Annuity’s 20% Liquidity Discount

Lambert and Tobe noted that annuities do not generally price or mark to market each day. An annuity holder who wants liquidity must often accept a substantial secondary-market discount. We specifically cited secondary-market firms that commonly pay approximately 80% of contractual value, meaning a person could purchase an annuity and face an immediate 20% economic loss if forced to sell it.

That was not merely an observation about retail hardship. It exposed the central accounting deception:

The insurance company reports the annuity at book value because the contract prevents the policyholder from discovering its market value.

A mutual fund normally shows the participant the market value of its assets every day. A publicly traded bond is marked to the price at which investors are willing to buy and sell it. An annuity instead reports the insurer’s contractual promise, usually without showing what an independent buyer would pay for that promise.

Illiquidity does not eliminate market risk. It conceals it.

Our paper also explained why this problem becomes more severe after a downgrade. A bond manager can sell a deteriorating security when it falls below the portfolio’s required credit standard. Most annuity holders cannot sell the issuing insurer’s promise without surrender charges, market-value adjustments, contractual restrictions, or a deep secondary-market discount. The holder therefore may be forced to ride the insurer down toward default.

The NBER Paper Independently Values the Risky Annuity at 74 Cents

The NBER authors reach a strikingly similar result through an entirely different method.

Survey respondents expected to receive, on average, only 81.5% of the annuity payments they had been promised. They also indicated that a completely certain payment of only 73.8% of the promised benefit would make them economically indifferent to retaining the risky insurance contract. The difference produces an implied annuity risk premium of about 7.7 percentage points.

The 73.8-cent figure is not a quoted secondary-market price. It is a consumer certainty equivalent. It reflects the amount of certain value respondents were willing to accept instead of bearing:

insurer default risk;

partial-payment risk;

claims and contract disputes;

delay risk;

procedural complexity;

and uncertainty about future performance.

Yet it lands almost precisely in the range suggested by actual illiquid-market discounts.

That convergence matters. Consumers may not know the insurer’s portfolio, spread, capital formula, offshore reinsurance arrangements, or private-credit exposure. But collectively they appear to value the promise as though it were a deeply discounted, illiquid credit instrument—not cash and certainly not a Treasury obligation.

Private Credit Creates a Second Hidden Mark-to-Market Discount

The connection becomes more troubling because life insurers increasingly hold private credit and other illiquid debt.

The precise percentage depends heavily on how “private credit” is defined. Current estimates range from approximately 20% of insurers’ fixed-income holdings under narrower definitions to roughly 35% or more of balance-sheet exposure under broader definitions. One 2026 estimate placed life and annuity insurers’ private-credit exposure at approximately 46% of total debt holdings. Therefore, it is reasonable to say that some insurers—and especially certain private-equity-affiliated insurers—have something approaching half of their debt portfolio exposed to private or illiquid credit, but it would be too broad to say every insurer is 50% private credit.

Our paper anticipated this development. We documented that private-equity-influenced insurers were moving into private asset-backed securities, private placements, leveraged credit, commercial real estate, and other difficult-to-value investments. We also explained that the regulatory system allows many of these assets to be carried using modeled values and favorable NAIC designations rather than observable market prices.

The market is now beginning to test those modeled values.

Recent offers for interests in nontraded private-credit vehicles have reportedly been made at discounts of 15% to 30% from reported NAV—equivalent to approximately 70 to 85 cents on the accounting dollar. Earlier surveys of private-credit secondary transactions showed average pricing around 85 cents on the dollar, while publicly traded private-credit vehicles have also traded at material discounts to stated NAV.

This produces a potential double-opacity structure:

The insurer carries private loans near modeled or reported value, even when a prompt secondary sale might produce only 70 to 85 cents.

The insurer then issues an annuity contract backed by that portfolio and reports the policyholder’s claim at 100 cents, even though the annuity itself may be saleable only at a substantial discount.

The participant sees neither markdown because both sides of the insurer’s balance sheet are insulated from ordinary market pricing.

The Annuity Is a Leveraged Claim on Assets That May Themselves Be Overstated

An annuity is not direct ownership of the insurer’s bonds, mortgages, CLOs, private loans, or affiliated investments. It is a general unsecured claim against the insurance company.

That means the annuity owner is structurally behind the insurer’s entire asset-selection process. The owner bears the consequences of:

private-credit markdowns;

defaults and restructurings;

valuation errors;

affiliate transactions;

leverage within borrowers;

leverage within private-credit funds;

reinsurance leverage;

and the insurer’s own capital structure.

The Financial Stability Board warned in 2026 that private credit can contain leverage at multiple levels: the portfolio company, fund, sponsor, investor-financing, and insurance-company levels. It also highlighted opacity, interconnectedness, liquidity mismatch, and the difficulty regulators face in detecting concentrated risk.

Thus, the annuity contract is not simply backed by a diversified portfolio of safe loans. It may be a single-entity promise backed in substantial part by private obligations that cannot be readily sold at their stated values.

A Simple Illustration

Assume an insurer reports $100 of assets supporting an annuity obligation:

Insurer assets

Book value

Possible prompt-sale value

Private and illiquid credit, 50%

$50

$35–$42.50

Public and more liquid assets, 50%

$50

$47.50–$50

Total

$100

$82.50–$92.50

This simple illustration does not establish an individual insurer’s actual liquidation value. Not every private loan would sell for 70 cents, and a forced liquidation may be either better or worse depending on credit quality, duration, transfer restrictions, and market conditions.

But the illustration shows how quickly reported surplus can disappear.

If the insurer has $100 in stated assets and $95 in policyholder and other liabilities, it appears to have $5 of capital. If those assets would produce only $85 in a stressed market sale, the insurer is not merely short of its reported capital. It may be economically insolvent by $10.

The annuity holder’s 100-cent promise would then depend on:

continued book-value accounting;

time to maturity;

borrowers’ ability to refinance;

regulatory forbearance;

affiliated support;

reinsurance recoveries;

guaranty-association capacity;

or a public rescue.

This is why a small percentage decline in insurer assets can create a much larger percentage loss in insurer capital.

The 70-to-80-Cent Range Is a Market Signal, Not Yet a Universal Appraisal

The strongest defensible formulation is not that every annuity is presently worth 70 cents. That would require insurer-specific analysis of:

underlying asset composition;

actual secondary bids;

liability duration;

surrender rights;

ratings;

CDS and bond spreads;

capital and surplus;

reinsurance;

guaranty-association treatment;

and contract provisions.

The stronger and more accurate statement is:

Multiple independent valuation methods suggest that many insurance promises marketed and accounted for at 100 cents on the dollar may have economic values closer to 70–80 cents when marked for liquidity, risk, and certainty.

That is more than a rhetorical claim. It now rests on:

actual annuity secondary-market discounts identified in Lambert–Tobe;

the NBER paper’s 73.8-cent annuity certainty equivalent;

consumers’ expectation of receiving only 81.5% of promised annuity benefits;

current private-credit secondary prices and tenders at material discounts to reported NAV;

and evidence that insurers have accumulated substantial private and illiquid credit exposure.

This Also Helps Explain the Hidden 300-to-500-Basis-Point Spread

The insurer earns a large spread partly because the customer is not receiving a liquid, market-priced security.

The insurer takes in $1 of participant money, invests it in assets that may offer elevated yields because they are illiquid, opaque, leveraged, affiliated, or risky, and then credits the participant a much lower rate. Lambert and Tobe explain that the spread equals the insurer’s general-account return minus the rate paid to participants—and that most insurers do not disclose either the complete portfolio economics or the resulting spread.

The insurer may therefore be compensated several times:

a private-credit liquidity premium;

a credit-risk premium;

an origination or affiliate fee;

an asset-management fee;

the retained difference between asset yield and participant crediting rate;

and surrender or liquidity restrictions imposed on the customer.

Yet the annuity holder receives the least liquid claim in the structure.

That is the fundamental asymmetry:

The insurer collects the liquidity premium, but the participant bears the illiquidity.

If private credit yields 9% or 10%, the insurer credits the participant 3% or 4%, and an immediate market sale of the contract produces only 70 to 80 cents, the annuity is not functioning like a low-cost safe investment. It is functioning like a high-spread, illiquid loan from the participant to the insurer.

The Book-Value Illusion

The industry’s defense is that the insurer does not need to sell the assets today. It can hold the private loans to maturity, collect principal and interest, and use the proceeds to meet annuity payments over decades.

That defense assumes away the very risks at issue:

loans may default;

borrowers may need refinancing;

recoveries may be delayed;

private valuations may be stale;

annuity liabilities may accelerate;

collateral calls may occur;

policyholders may seek liquidity;

reinsurance counterparties may weaken;

and regulators may discover that reported capital was overstated.

“Hold to maturity” is not a guarantee of par recovery. It is an accounting and liquidity strategy that works only if the underlying credits ultimately perform and the insurer remains able to fund its liabilities in the meantime.

Our paper described annuities as single-entity, illiquid credit exposures rather than genuinely diversified safe investments. The NBER paper now shows that ordinary consumers appear to reach a similar conclusion when asked to value the promise. They discount it to approximately 74 cents of certainty.

The Strongest Conclusion

Lambert and Tobe argued that annuities are reported at artificial book values, shielded from daily market pricing, and backed increasingly by illiquid assets that may themselves be difficult to value. The new NBER findings provide independent household-level evidence of the same economic reality.

Consumers do not value a dollar of promised annuity payment as a dollar of safe wealth. They value it at approximately:

81.5 cents after allowing for expected nonpayment; and

73.8 cents after also pricing the uncertainty surrounding that payment.

At the same time, the private-credit assets increasingly supporting those promises may trade at 70 to 85 cents when an actual seller requires liquidity.

The central problem is therefore not merely that insurers hold risky assets. It is that the entire structure is designed to avoid the moment when either the assets or the liabilities must reveal a market price.

The private loan is carried at a modeled dollar. The annuity is carried at a contractual dollar. But when either one must be converted to cash, the market may say it is worth only 70 or 80 cents.

That gap is not harmless accounting noise. It is the hidden risk reserve that insurers have transferred to annuitants while retaining the spread, commissions, and profits for themselves.

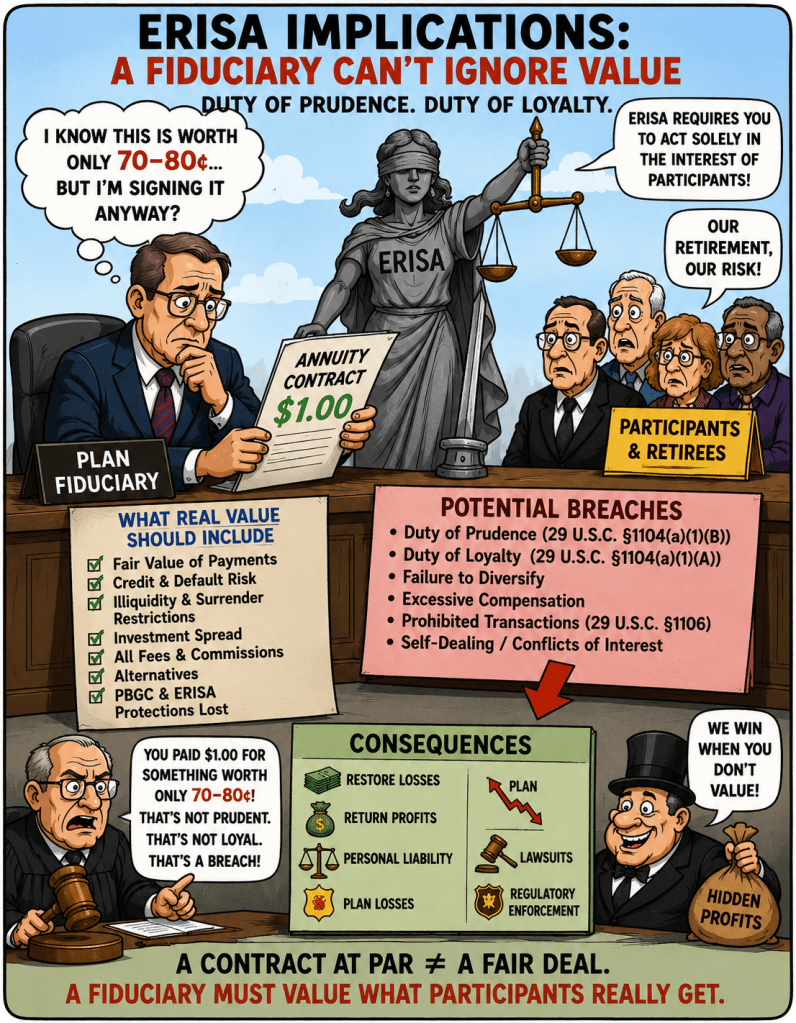

The ERISA Problem With Buying a $0.70 Annuity for $1.00

An ERISA fiduciary would ordinarily never knowingly use $100 of plan assets to purchase an investment that becomes worth only $70 or $80 the moment the transaction closes. Calling the investment an “annuity,” recording it at book value, or preventing the participant from selling it does not eliminate the economic loss. It merely prevents the loss from appearing on a daily account statement.

That principle applies in two related settings:

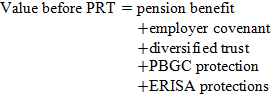

a defined contribution plan purchasing or retaining a fixed annuity; and

a defined benefit plan purchasing a lifetime annuity in a pension risk transfer.

The legal details differ, especially because the decision to terminate or de-risk a pension plan may be a settlor decision. But the actual selection, pricing, and purchase of the annuity remain fiduciary acts. The Department of Labor expressly distinguishes the sponsor’s business decision to conduct a PRT from the fiduciary implementation of that decision.

The Immediate Loss Is Not Hypothetical

Our March 2026 Journal of Economic Issues paper explains that annuity contracts generally are not marked to market and often cannot be redeemed after an insurer downgrade. Where secondary markets exist, an owner needing immediate liquidity may receive only approximately 80 cents on the contractual dollar. The contract’s lack of daily pricing does not make the loss disappear; it conceals the amount that an independent buyer would actually pay.

The NBER Risky Insurance paper approaches the same issue from the purchaser’s perspective. Survey respondents expected an annuity to deliver only approximately 81.5% of its promised benefits, and their average certainty equivalent was approximately 73.8% of the promised amount. In other words, the average respondent regarded about $74 of certain value as equivalent to a nominal $100 insurance promise.

Neither number is necessarily a formal fair-value appraisal of every annuity. A secondary-market discount may include illiquidity, transaction costs, adverse selection, surrender provisions, and the buyer’s required profit. The certainty equivalent includes perceived nonpayment risk and risk aversion. But a fiduciary cannot simply ignore these measurements when they repeatedly indicate that a supposedly $100 asset has a market or certainty value of only $70 to $80.

1. Duty of Prudence: A Fiduciary Must Examine Economic Value, Not Merely Contractual Face Value

ERISA requires fiduciaries to act with the care, skill, prudence, and diligence that a knowledgeable person would use under the circumstances then prevailing. It also requires diversification to minimize the risk of large losses unless nondiversification is clearly prudent.

The key phrase is “under the circumstances then prevailing.” A fiduciary cannot knowingly purchase an annuity at $100 while disregarding evidence available at the time that:

the contract could be resold for only $70 to $80;

the participant cannot exit after an insurer downgrade;

the insurer’s assets include large amounts of illiquid or modeled private credit;

the insurer retains a substantial undisclosed investment spread;

materially safer or more liquid alternatives are available;

and the contract transfers the participant from a diversified ERISA plan into a single-insurer credit exposure.

The Supreme Court has emphasized that fiduciaries must conduct their own independent evaluation of investments. Participant choice does not excuse an imprudent investment option, and a fiduciary has a continuing obligation to monitor investments and remove imprudent ones.

A fixed annuity therefore cannot be defended merely by saying:

“Participants voluntarily selected it.”

Nor can a PRT annuity be defended merely by saying:

“The sponsor had the right to terminate the pension plan.”

The sponsor may have the right to decide whether to terminate or de-risk. The fiduciary must still prudently determine how plan assets are used to carry it out.

2. The Fiduciary Must Determine What the Plan Actually Receives for Its $100