The stable value industry’s own trade association inadvertently exposes the structural problem with general-account fixed annuities in retirement plans. I agree that these lawsuits against low-risk diversified synthetic-based stable value are baseless and harmful.

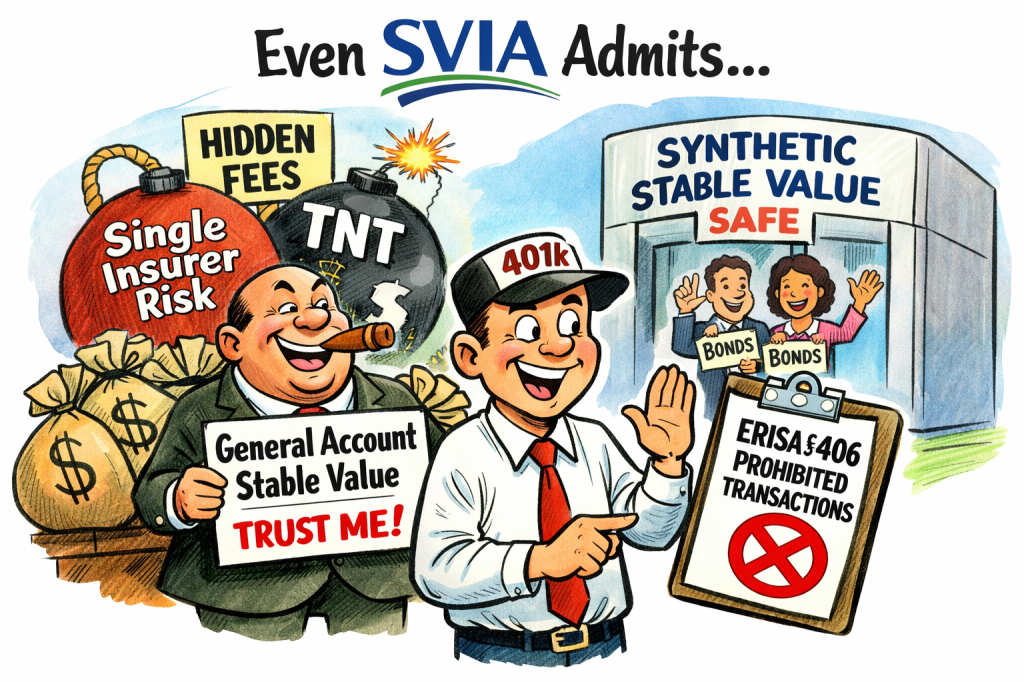

In recent amicus briefs filed in federal ERISA litigation, the Stable Value Investment Association (SVIA) explains that stable value products fall into several very different categories. Synthetic stable value products—individually managed accounts and pooled funds—hold the underlying bond portfolios directly for the benefit of the retirement plan. Insurance company products, by contrast, are issued and guaranteed by a single insurance company and backed by that insurer’s general account. https://www.stablevalue.org/svia-and-u-s-chamber-of-commerce-file-amicus-brief/

That seemingly technical distinction is the entire ballgame. In a synthetic stable value structure, the retirement plan owns the underlying assets—typically diversified portfolios of high-quality bonds—and insurance “wrap” providers merely guarantee book-value liquidity. The plan therefore, retains ownership of the portfolio and diversifies credit risk across many issuers.

In a general-account annuity, the plan owns nothing. The assets are commingled with the insurance company’s liabilities and participants become general creditors of the insurer. Their retirement security therefore, depends on the solvency of a single financial institution.

This difference is not subtle. It is a fundamental transformation of a retirement plan asset into an insurance company liability. The SVIA briefs also acknowledge another crucial difference: compensation structures. Synthetic stable value funds typically charge explicit, disclosed fees, while insurance company products often compensate themselves through an undisclosed “spread” between the insurer’s investment earnings and the crediting rate paid to participants.

That spread structure creates a classic ERISA prohibited transaction. Under ERISA §406, a fiduciary may not cause the plan to engage in a transaction that allows a service provider to receive undisclosed or excessive compensation from plan assets. Yet the spread in a general-account annuity is not negotiated as a transparent fee. Instead, the insurer keeps whatever investment earnings exceed the declared crediting rate, a figure that participants and fiduciaries often cannot observe or benchmark.

In other words, the insurance company is simultaneously:

- the issuer of the product,

- the manager of the assets,

- the counterparty to the contract, and

- the party determines its own compensation.

No independent market mechanism exists to test whether that spread is reasonable. The SVIA briefs further note that general-account products are “offered and guaranteed by a single insurance company.” That means participants bear concentrated exposure to one insurer’s credit risk, while the insurer captures the upside from investing the assets.

Synthetic stable value does the opposite. Credit risk is diversified across many bonds and multiple wrap providers, fees are disclosed, and the plan retains ownership of the portfolio.

In short:

| Structure | Asset Ownership | Credit Risk | Fees |

| Synthetic Stable Value | Plan trust owns bonds | Diversified | Explicit |

| General Account Annuity | Insurer owns assets | Single insurer | Hidden spread |

The insurance industry likes to present general-account products as “guaranteed.” But the guarantee is only as strong as the issuing insurer. History provides many reminders—from Executive Life to more recent insurance failures—that these guarantees are far from risk-free.

From a fiduciary perspective, the problem is not simply that general-account annuities carry more credit risk. The problem is that they combine opaque compensation, single-entity credit exposure, and self-dealing by the product issuer.

Those characteristics are precisely the types of conflicts ERISA’s prohibited-transaction rules were designed to prevent.

Synthetic stable value products demonstrate that another structure is possible—one where the plan retains ownership of the assets, fees are transparent, and risks are diversified.

Which raises the obvious question fiduciaries should be asking:

If a transparent, diversified structure exists, why place retirement assets into opaque general-account contracts where the insurer controls the assets, determines its own compensation, and concentrates credit risk in a single institution?

Under ERISA’s strict prohibited-transaction framework, that question may eventually have a simple answer. Because they never should have been there in the first place.

SVIA amicas JPMorgan July 2025, Baxter International July 2025 Hackensack Health August 2025