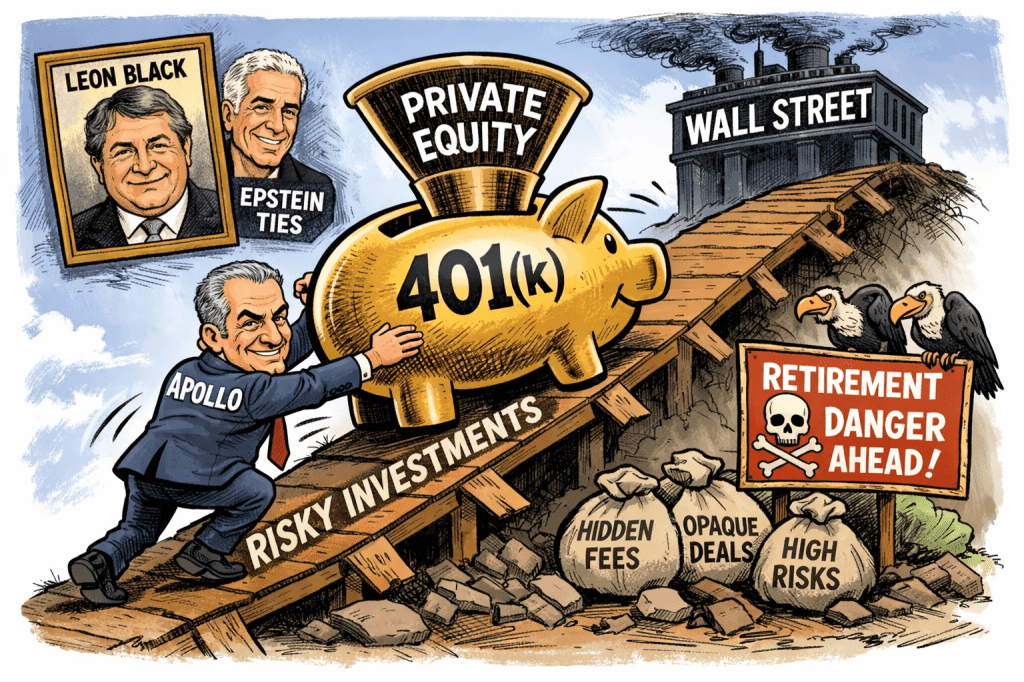

Wall Street never stops looking for a new pool of captive money. Now Apollo Global Management — the firm long shadowed by Jeffrey Epstein through co-founder Leon Black — is pushing to move deeper into America’s 401(k) system under CEO Marc Rowan. That push is no longer theoretical. Reuters reported in August 2025 that Rowan publicly welcomed an expected Trump administration move to channel more retirement assets into private markets, saying he believed the industry was “on the cusp” of serving the 401(k) and defined-contribution marketplace and that regulatory changes to make this easier were “common sense.”

The timing could hardly be more revealing. In February 2026, Apollo and Schroders announced a partnership that includes a collective investment trust for the U.S. defined-contribution market, targeted for launch in the second quarter of 2026. Schroders was recently purchased by TIAA division of Nuveen. Empower also set up deals with Apollo to put private assets into 401(k)s. Reuters and Apollo’s own announcement described the project as a retirement product blending public and private exposures for the defined-contribution channel. In other words, Apollo is not merely cheering from the sidelines. It is building the distribution pipe.

This is exactly the danger. Private equity has always depended on opacity, delayed pricing, layered fees, insider-friendly contracts, and benchmarks that can be manipulated or custom-built. Those features are a scandal in a public pension. In a retail 401(k), where workers are told they have daily liquidity and transparent account values, they become something worse: a structural mismatch between what participants are shown and what they actually own. Your March 6 piece makes that point directly — that private equity often survives in retirement plans only when buried inside more complex wrappers where participants cannot see the contracts, compensation, or valuation mechanics clearly.

That is why the political and regulatory backdrop matters so much. On August 7, 2025, the White House issued an executive order explicitly aimed at “democratizing access” to alternative assets in 401(k) plans and directed the Labor Department and SEC to facilitate that access. The Department of Labor then issued Advisory Opinion 2025-04A in September 2025, expanding the room for products housed in variable annuities, CITs, and pooled vehicles to qualify within QDIA-type structures. At the same time, SEC Commissioner Mark Uyeda gave a November 2025 speech urging broader access to private markets in defined-contribution plans. The direction of travel has been unmistakable: open the gates, soften the guardrails, and normalize illiquid, hard-to-price products in retirement plans built for ordinary workers.

But disclosure has not kept pace — not remotely. Your February 2026 comment letter to DOL laid out the core defect: participants often are not given full look-through holdings, underlying manager identities, layered fees, affiliate relationships, embedded insurance exposures, or even clarity about who regulates the product. As you wrote there, electronic delivery cannot solve a substantive transparency failure; it merely “accelerates opacity.” That criticism applies with even greater force to private-equity-laced CITs and hybrid retirement products.

The accounting problem is just as severe. In my “4 Sets of Books” piece, I noted that private assets inside 401(k)s are commonly valued using Level 3 inputs and often priced by managers or appraisers chosen by managers. That means the same firms collecting the richest fees are often closest to the marks participants are asked to trust. The more private assets migrate into 401(k) structures, the more retirement savers will be forced to rely on numbers that are neither market-clearing nor independently testable in real time.

And this is where Apollo’s own credibility problem becomes impossible to ignore. Just last week, Reuters reported that Apollo, Leon Black, and Marc Rowan were sued by shareholders who allege they concealed business ties to Jeffrey Epstein for years. Reuters also reported in February that Apollo publicly stated Rowan had no business or personal relationship with Epstein as scrutiny intensified. Whether Apollo ultimately prevails in that litigation is not the point here. The point is simpler and more devastating: one of the firms most aggressively seeking access to America’s retirement savings is simultaneously defending itself against allegations that it misled investors about its Epstein-related business ties. That is not a due diligence green flag. That is a fiduciary siren.

This is why Marc Rowan’s “common sense” line should be turned on its head. Common sense says that a private-equity giant born in secrecy, enriched by hidden fee structures, and still engulfed in Epstein-related fallout should not be handed a new franchise over workers’ nest eggs. Common sense says that 401(k)s are not venture-capital pools, not valuation laboratories, and not a bailout mechanism for an industry desperate for fresh retail capital as institutional investors push back on fees, illiquidity, and disappointing net returns. Common sense says that if a product cannot survive full fee transparency, clear legal accountability, independent valuation, and easy participant comprehension, it does not belong in a retirement plan.

Apollo’s campaign is not about democratizing finance. It is about democratizing extraction. The private-equity industry sees trillions sitting in 401(k)s and wants in. Marc Rowan is trying to lead that march. Fiduciaries, regulators, unions, and participants should say no — before workers discover too late that their retirement plan has become just another permanent-capital vehicle for Wall Street.

https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/https://commonsense401kproject.com/2026/03/10/jeffrey-epstein-funder-leon-blacks-apollo-bleeds-public-pensions-of-6-billion-a-year-through-secret-no-bid-contracts/