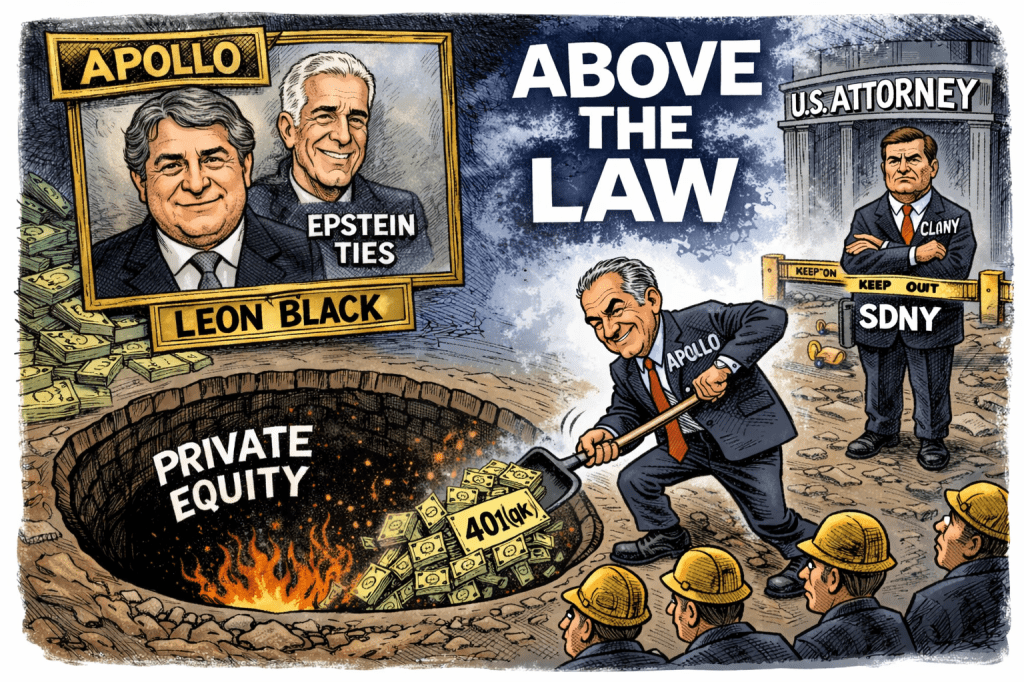

There are scandals on Wall Street. And then there is Apollo Global Management. Apollo was co-founded by Leon Black, the billionaire who paid convicted sex trafficker Jeffrey Epstein $158 million for mysterious “tax advice.” That relationship detonated into one of the ugliest scandals in modern finance and ultimately forced Black to step down as CEO. Yet despite that disgrace, Apollo remains deeply embedded in the American financial and political system. This is on top of a long history of scandals and violations with the SEC, EPA, and others.

Apollo CEO Marc Rowan is now leading the private-equity industry’s push to move trillions of dollars from 401(k) plans into opaque private assets. The sales pitch is dressed up in the language of “democratizing private markets.” But the reality is much simpler. Private equity needs fresh capital. Institutional investors are increasingly questioning fees, illiquidity, and performance. So Wall Street, led by Apollo, is now targeting the largest untouched pool of money in the country — American workers’ retirement savings.

And the political doors are wide open. Rowan has become one of the most influential financiers in Washington and was recently named to President Trump’s advisory structures related to Gaza reconstruction and governance. That alone should make people uncomfortable. But the deeper problem is the extraordinary web of influence surrounding Apollo and the agencies that are supposed to police it.

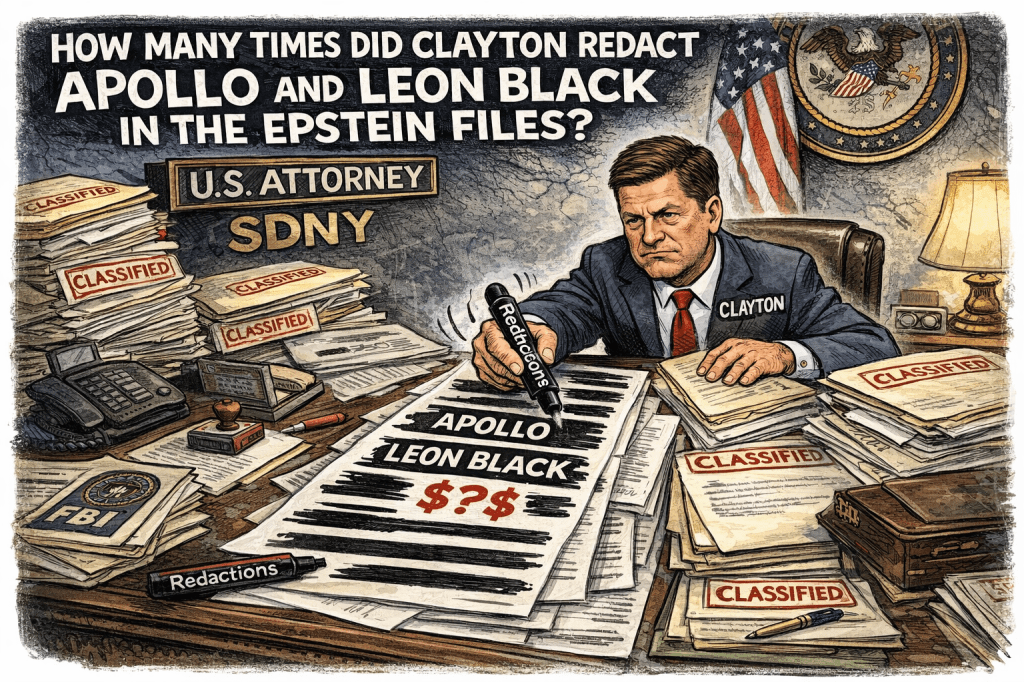

Consider the man now running the most powerful financial crime prosecutor’s office in the country. Jay Clayton, the U.S. Attorney for the Southern District of New York — the office that historically prosecutes Wall Street corruption — previously served as chairman of Apollo’s board. According to reporting by The Lever, Clayton still holds more than $1 million in Apollo investments.

What is worse, Attorney General Pam Bondi put Clayton in charge of the redactions of the Epstein files. My question is how many redactions did he make that involved Apollo and Leon Black? Pam Bondi has a long history with Apollo, hiring them to manage hundreds of millions for the Florida Retirement System when she was a trustee of that Pension.

Think about that for a moment. The top federal prosecutor in Manhattan has deep financial ties to a private-equity firm whose founder’s Epstein relationship remains the subject of lawsuits and investigations. The office that prosecuted Jeffrey Epstein now has a leader financially connected to the firm founded by Epstein’s most famous billionaire client. On top he was assigned by the US Attorney General to oversee redactions of millions of files, where he had numerous conflicts.

Meanwhile, the scandals keep coming. In February, Epstein file disclosure (maybe the one in a hundred Clayton missed) emails showing CEO Marc Rowan’s involvement with Epstein and that Epstein provided advice to Apollo, in contrast to SEC documents filed in 2021. In March 2026, Apollo, Leon Black, and Marc Rowan were sued by shareholders who alleged the firm had misled investors for years about its relationship with Epstein. The lawsuit claims Apollo’s filings falsely denied doing business with Epstein, even though he allegedly played a significant role in advising senior leadership.

Apollo has built a vast empire extracting fees from public pension funds through secretive, no-bid contracts, opaque valuation methods, and complex structures that hide the true cost of private equity and private credit. As much as 85% of their assets come from taxpayer funds. As documented in prior reporting, the firm’s fee machine likely drains billions of dollars annually from public retirement systems.

And now Apollo wants the next frontier. Your 401(k). The plan is straightforward. Private equity firms partner with asset managers to build collective investment trusts, target-date funds, and hybrid products that quietly insert private assets into retirement portfolios. Workers will be told they are receiving “diversification.” What they are actually receiving are illiquid assets priced by models, surrounded by multiple layers of fees, and wrapped in disclosures almost no participant can understand. It is a perfect system for Wall Street. Daily pricing in 401(k)s becomes fiction. Transparency disappears. Benchmarking becomes meaningless. And the fees — always the fees — continue flowing upward.

For decades, private equity thrived because public pensions provided patient capital with limited scrutiny. Now even those investors are asking questions about performance and fee extraction. So the industry is hunting for something better. Captive capital. A 401(k) participant cannot negotiate terms. They cannot demand transparency. They cannot fire the manager running the fund inside their target-date product.

If a firm was built by a billionaire who secretly paid Jeffrey Epstein $158 million… If that firm’s executives are currently being sued for allegedly concealing Epstein ties… If the nation’s top Wall Street prosecutor previously chaired that firm and still holds financial stakes in it…Why in the world would anyone allow that firm to manage workers’ retirement savings?

Public pensions should divest from Apollo. Regulators should scrutinize every contract the firm holds. And Congress should slam the door on the private-equity industry’s attempt to convert America’s 401(k) system into the next extraction machine.

Because if Apollo and the rest of the private-equity industry succeed, the Epstein scandal will end up being remembered not as the moment Wall Street cleaned house — but as the moment it realized it could get away with almost anything.

https://www.levernews.com/the-wall-street-prosecutor-with-a-portfolio-problem/

The Apollo / Epstein Files: Why Public Pensions Should Reopen the 2019 Divestment Debate