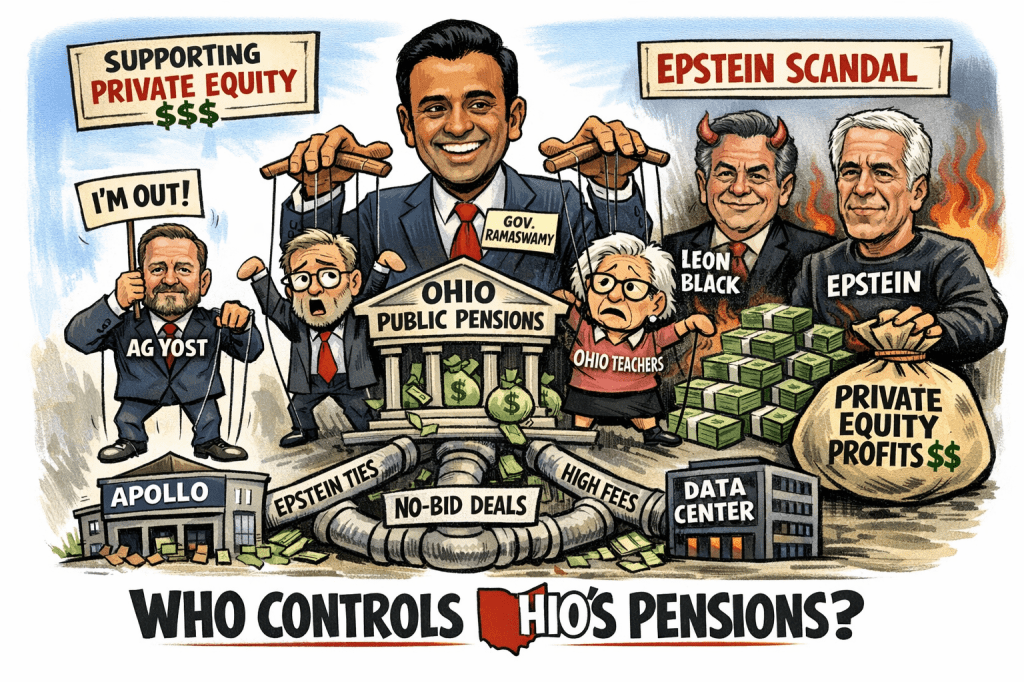

There is a growing effort across the country to scrutinize—and in some cases divest from—private equity firms entangled in conflicts, secrecy, and scandal. Nowhere is that pressure more justified than with Apollo Global Management, whose documented ties to Jeffrey Epstein and reliance on public pension capital have triggered renewed calls for accountability. https://commonsense401kproject.com/2026/03/10/jeffrey-epstein-funder-leon-blacks-apollo-bleeds-public-pensions-of-6-billion-a-year-through-secret-no-bid-contracts/ But in Ohio, that effort is likely to collide head-on with a potential governor whose financial roots and policy instincts are deeply aligned with the very system under scrutiny: Vivek Ramaswamy.

Ramaswamy is often marketed as a biotech entrepreneur, but the deeper story is one of private equity alignment. A significant portion of his wealth traces not to traditional operating businesses, but to data monetization platforms like Datavant, which was backed and scaled by New Mountain Capital. This is not incidental—it is emblematic. Datavant sits at the intersection of private equity, data extraction, and long-duration capital structures, the same ecosystem that increasingly dominates public pension portfolios.

That ecosystem depends heavily on state and local pension systems for capital. In Ohio, that includes both the Ohio Public Employees Retirement System and State Teachers Retirement System of Ohio—multi-billion-dollar funds that have allocated significant assets to private equity managers, including Apollo and its affiliated credit vehicles. As documented in prior analysis, these investments are often executed through opaque, no-bid contracts with layered fee structures that can exceed 500–600 basis points annually when fully loaded.

The political question is simple: would a Governor Ramaswamy support divestment from firms like Apollo in light of their Epstein ties, fee extraction, and governance concerns? The financial answer is far more revealing: it is highly unlikely.

Ramaswamy’s economic worldview is not merely tolerant of private equity—it is structurally dependent on it. His alignment extends beyond passive investment exposure into active policy advocacy. He has publicly supported the expansion of data center infrastructure—an asset class increasingly dominated by private equity and private credit vehicles, including those tied to Apollo. These data centers are not neutral infrastructure plays; they are fee-generating machines financed by the same pension capital that bears the downside risk.

This creates a reinforcing loop: public pensions allocate to private equity → private equity finances data centers and data platforms → political actors aligned with those interests promote further expansion → pension capital becomes even more dependent on the same opaque structures.

Ramaswamy’s involvement with Strive Asset Management adds yet another layer to this conflict. Strive positions itself as a challenger to ESG-driven investing, but in practice, it operates as a gatekeeper—advising and influencing pension allocations in Republican-controlled states such as Indiana. This is not a passive role. It places Strive—and by extension Ramaswamy—directly in the flow of pension capital decisions, including allocations to private equity managers.

In other words, the same individual who could oversee Ohio’s pension systems has already built a business model around influencing where those systems invest. That is not reform. That is vertical integration.

If Ohio’s pensions were to seriously consider divesting from Apollo or similar firms—whether due to Epstein-related governance concerns, hidden fee structures, or the growing risks in private credit—such a move would run directly counter to the financial architecture that underpins Ramaswamy’s own wealth and network. And that is before considering the broader systemic risk.

Private equity’s expansion into private credit, insurance balance sheets, and data infrastructure has created what can only be described as a shadow financial system—one that avoids mark-to-market discipline, obscures true fee levels, and concentrates risk in ways that are difficult for beneficiaries to see and even harder for fiduciaries to challenge. Ohio’s pensions are deeply embedded in this system.

A governor aligned with private equity is not going to unwind that exposure. He is far more likely to defend it. The result is a potential collision between fiduciary duty and political economy. Beneficiaries—teachers, public workers, retirees—have a right to demand transparency, competitive bidding, and independence from conflicted intermediaries. But those demands threaten a system that has become extraordinarily profitable for private equity firms and their political allies. The Apollo-Epstein controversy is not just a reputational issue. It is a stress test of whether public pension systems can act independently of the financial and political networks that influence them.

The Political Consolidation Behind Private Equity Power in Ohio

The political landscape in Ohio has already shifted in a way that reinforces—not challenges—the private equity status quo. When Dave Yost exited the 2026 gubernatorial race, it was not a neutral event. It effectively cleared the field for Vivek Ramaswamy, consolidating Republican political power behind a single candidate aligned with private equity interests. Yost’s withdrawal came immediately after the Ohio Republican Party endorsed Ramaswamy, turning what he described as a difficult path into a “vertical cliff” and eliminating meaningful intra-party opposition.

This matters for one reason: it removes one of the last potential institutional checks on how Ohio’s public pension capital is deployed. Because the stakes are not abstract. As documented in Epstein, Apollo, and Ohio Teachers’ Billions, https://commonsense401kproject.com/2026/02/23/epstein-apollo-and-ohio-teachers-billions/ Ohio’s largest pension systems—particularly State Teachers Retirement System of Ohio—have already committed billions to private equity structures tied to Apollo Global Management and its affiliates. These allocations are not passive index exposures. They are embedded in opaque, illiquid vehicles with limited transparency, no competitive bidding, and fee structures that can extract extraordinary value from beneficiaries over time.

The Epstein connection is not a historical footnote—it is a governance red flag. Apollo’s co-founder Leon Black was documented as having extensive financial ties to Jeffrey Epstein, raising serious questions about oversight, fiduciary judgment, and counterparty risk at the exact firms entrusted with public pension assets.

And yet, despite this, there has been no serious political push in Ohio to re-evaluate or unwind these relationships.

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Yost’s exit helps explain why. With the Republican field consolidated behind Ramaswamy—and with additional statewide officials and party infrastructure aligning in the same direction—the probability of a coordinated effort to investigate, much less divest from, Apollo or similar private equity firms drops dramatically.

Instead, what emerges is something far more concerning: political consolidation that mirrors financial concentration. Ohio’s pensions are already heavily allocated to private equity. Now the political leadership overseeing those pensions is converging around a candidate whose personal wealth, business ventures, and advisory networks are deeply intertwined with that same ecosystem. That is not a coincidence. It is alignment. And for beneficiaries—teachers, public employees, retirees—it raises a fundamental question: if both the capital and the political oversight are concentrated within the same private equity orbit, who exactly is left to challenge the system?

Ramaswamy will keep all the Apollo funds in Ohio

In Ohio, voters have a new option by voting for Amy Acton for Governor. Acton is more likely to support divestiture