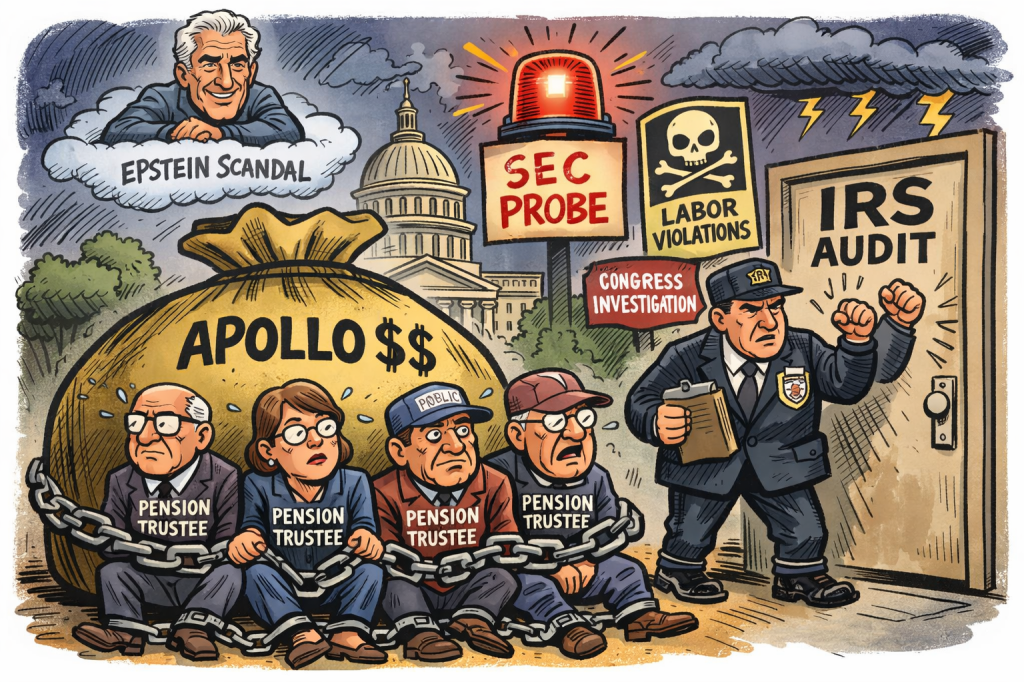

Public pension trustees still think the Apollo problem is reputational. It isn’t.

It has now become regulatory, legal, and financial—at the same time.

And the window to act voluntarily is closing fast. Since the February 1st Financial Times of London story dropped was soon followed by a SEC complaint by AFT and AAUP unions on February 12, and stock drop cases filed the next week after Apollo stock tanked over 35%, losing nearly $20 billion in value.

Apollo Is No Longer “Headline Risk”—It Is a Systemic Risk

For years, pensions were sold a carefully constructed narrative:

- Leon Black’s relationship with Jeffrey Epstein was “personal”

- the issue was contained

- governance had been “fixed”

That narrative is now unraveling.

The February 2026 complaint filed with the U.S. Securities and Exchange Commission by the American Federation of Teachers and American Association of University Professors alleges that Apollo’s disclosures may have been materially incomplete or misleading. https://www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf

In March the AFL-CIO filed another complaint echoing the Epstein concerns and adding some around labor violations of Apollo portfolio companies. https://aflcio.org/sites/default/files/2026-03/Letter%20to%20Apollo%20Global%20Management’s%20Lead%20Independent%20Director%20Gary%20Cohn%203.11.2026.pdf

AFL-CIO is an umbrella organization for a number of unions affiliated with public pensions including American Federation of State, County and Municipal Employees (AFSCME) American Federation of Teachers (AFT) International Association of Fire Fighters (IAFF) Service Employees International Union (SEIU) International Union of Police Associations (IUPA) https://aflcio.org/what-unions-do/social-economic-justice/corporate-accountability

The Apollo facts have become harder and harder for fiduciaries to wave away. In the February 17, 2026 SEC complaint from AFT and AAUP, the unions asked the Commission to investigate whether Apollo’s prior disclosures about its and its executives’ ties to Jeffrey Epstein painted an “inaccurate and incomplete picture.” Their letter pointed to newly released Epstein documents referring to Marc Rowan, including meetings at Apollo’s offices, breakfasts involving Rowan, Leon Black, and Epstein, discussions of donor-advised funds, tax matters, a possible Apollo inversion, and other business-related contacts. The letter concluded that the 2021 disclosures may have offered “an inaccurate depiction of the extent of Apollo’s ties with Jeffrey Epstein” and said the SEC should investigate whether the statements were materially false or misleading.

That matters enormously for pension fiduciaries. In 2019 and again in 2021, many institutional investors were told, in substance, that the Epstein problem at Apollo was largely personal to Leon Black and was being cleaned up. The new AFT-AAUP complaint directly challenges that sanitized version, arguing that the public record now suggests a broader and deeper institutional relationship. Whether the SEC ultimately agrees is not the point. The point is that pensions are on notice that the old comfort story may no longer hold. Once fiduciaries have credible notice that a manager may have mischaracterized material relationships, continuing to invest without a serious re-underwriting of the manager becomes its own governance failure.

Apollo co-founder Joshua Harris admitted at a 2013 meeting of the Philadelphia Board of Pensions that the firm’s capital base was overwhelmingly dependent on public retirement systems. Asked directly whether Apollo had many public pension investors, Harris responded bluntly that “almost all” of Apollo’s capital came from public funds, estimating that roughly 75% to 80% of Apollo’s capital was supplied by public pension plans. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

Apollo’s dependence on public retirement money means public fiduciaries cannot plausibly treat these governance issues as someone else’s problem. When the manager is deeply woven into pension portfolios, the pensions themselves inherit the governance burden. https://commonsense401kproject.com/2026/03/10/jeffrey-epstein-funder-leon-blacks-apollo-bleeds-public-pensions-of-6-billion-a-year-through-secret-no-bid-contracts/

The UN Human Rights Office is looking into Jeffrey Epstein’s files as a transnational “global criminal enterprise. Many US pensions have signed onto the UN Global Compact on Human Rights. Investment firms like Apollo have signed, which could lead to divestment. https://news.un.org/en/story/2026/02/1166980

This is no longer a contained issue. It is expanding across disclosure, governance, and labor fronts simultaneously.

Once fiduciaries are on notice that: disclosures may have been inaccurate, governance failures may be deeper than represented and Epstein-related ties may have been broader than disclosed the legal standard changes. Trustees no longer get to say: “We didn’t know.”

Congress Has Already Defined the Standard

In its February 2026 letter, the U.S. House Committee on Education and the Workforce warned that pensions risk losing their tax-favored status if they are not operating exclusively for beneficiaries. https://edworkforce.house.gov/uploadedfiles/02.12.26_calpers_loss_oversight_letter_will_instructions.pdf

Congress has already shown its hand. They aimed it at ESG specially the Environmental. But the logic doesn’t care about politics. Apply it to Apollo around Governance. Holding Apollo could endanger the IRS tax status of the plan.

Apollo’s stock collapse is not a side issue. It is confirmation. Between January and early March 2026, Apollo’s stock fell sharply wiping out tens of billions in market value.

That decline did three things at once:

1. Converted Governance Risk into Financial Loss

This is no longer theoretical.

Public pensions now hold:

- Apollo private equity and private credit (paying fees and likely hidden losses)

- Apollo stock (APO taking huge losses 2026)

- Apollo REIT (ARI -26% last 5 years)

They are simultaneously: clients and victims

2. Triggered Securities Litigation

This type of decline automatically triggers:

- stock-drop lawsuits

- securities fraud claims

- institutional investor recovery actions

This creates a direct fiduciary obligation: Pensions must evaluate whether to pursue recovery.

3. Exposed an Irreconcilable Conflict

Pensions now face a contradiction they cannot explain:

- suing Apollo (as shareholders)

- while allocating billions to Apollo (as clients)

Or worse:

- not suing at all—because of the conflicted relationship of Apollo secret no-bid contracts

That is the exact type of conflict regulators look for.

What They Cannot Do

They cannot:

- stay invested

- keep paying fees

- ignore the stock collapse

- ignore SEC complaints

- ignore labor violations

and claim they are acting solely in beneficiaries’ interest. That position is no longer credible.

The Clock Is Ticking for Pension Trustees

This is how these things unfold:

- Complaint filed (AFT/AAUP → SEC)

- Stock Drop Cases Filed

- Labor pressure escalates (AFL-CIO)

- Congress connects dots (oversight letters expand)

- Regulators follow

By the time enforcement arrives, it is too late. Apollo already had a long list of other Federal violations prior to Epstein. https://commonsense401kproject.com/2026/02/25/the-leon-black-culture-of-corruption-at-apollo-plans-should-divest/

Final Line

Apollo is no longer just a controversial manager. It is now a litigation event embedded inside every public pension portfolio.

Which leads to only one defensible conclusion: Divest now—while it is still a choice.

Because the next phase is not voluntary. It will be driven by courts,regulators or Congress

And by then, trustees will not be asked whether they acted. They will be asked: Why they didn’t.

List of Plans with Apollo Funds

Alaska Permanent Fund Apollo PE funds

Arizona PSPRS Apollo PE funds

California Public Employees’ Retirement System (CalPERS) Apollo Investment Fund VI and related vehicles

California State Teachers’ Retirement System (CalSTRS) Apollo Investment Funds VI, VII, IX, X; Hybrid Value II

Chicago Teachers Pension Fund 2024 performance confirms Apollo PE/PC as manager

Colorado PERA Apollo Investment Funds III,IV,V,VI, VII, Distresssed DIF

Colorado School Apollo Credit Opp III & DIF

Connecticut Retirement Plans & Trust Funds Apollo Investment Fund VIII

Florida State Board of Administration Apollo PE funds IV, V PC Accord V and VI

Georgia Teachers Retirement System

Idaho PERSI Apollo PE funds

Illinois Teachers Retirement System Apollo PE funds X

Illinois Municipal Apollo Credit Wilshire

Indiana Public Retirement System (INPRS) Apollo Origination Partnership

Iowa Public Employees Retirement System Apollo PE funds Wilshire

Kansas Public Employees Retirement System Apollo PE funds VIII,IX

Kentucky Teachers Apollo REIT & Apollo Stock

Los Angeles City Employees’ Retirement System (LACERS) Apollo PE funds VI

Los Angeles (CA) Water and Power has PE fund X

Louisiana Teachers’ Retirement System of Louisiana (TRSL), Apollo Credit, Natural Resources

Maryland State Retirement & Pension System ?PE funs

Massachusetts PRIM Apollo PE funds

Michigan RS Apollo Investment fund VIII, IX Hybrid Value Funds, Credit/ Opportunistic Credit

Minnesota State Board of Investment Apollo/Athene Dedicated Investment Program II

Mississippi PRS Apollo VIII IX Private Equity funds

Montana Board of Investments Stock holdings?

Nebraska Investment Council India Property Fund II LLC.

New Hampshire Retirement System Apollo PE funds

New Jersey Division of Investment: Stock holdings?

New Mexico State Investment Council Apollo PE VII, VIII PC

New York City Teachers’ Retirement System Apollo PE funds

New York City (NY) ERS PE $500mm 2013

New York City (NY) Police PE fund VI

New York State Apollo PE VIII

North Carolina Retirement Systems Apollo PE funds VI, VII

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Oregon PER recently comitted $300mm to Apollo distressed debt fund as well as earlier funds like Apollo PE IX

Pennsylvania PSERS Apollo PE funds IV $620mm

Pennsylvania SERS Apollo PE funds VI- VIII

Rhode Island Retirement System Apollo PE VIII, IX

San Diego City Employees Retirement System Apollo PE funds

San Francisco (SFERS) San Francisco Employees’ Retirement System Apollo PE funds Wilshire

South Carolina RS $750mm

South Dakota Retirement System Apollo PE funds

Texas County & District PE fund X

Texas ERS Apollo Credit Strategies

Texas Municipal Fund VIII

Texas TRS Teachers’ Retirement Apollo PE funds

Tennessee Consolidated Retirement System Stock holdings?

San Francisco Employees’ Retirement System Apollo PE funds

San Diego City Employees’ Retirement System Apollo PE funds

University of Calfiornia PE VII, VIII Principal Wilshire

Virginia Retirement System Apollo PE funds

Washington State Investment Board (WSIB) Apollo S3 Equity & Hybrid

–

Pennsylvania Stories from Joe DiStephano

https://www.inquirer.com/business/sers-psers-pensions-pennsylvania-apollo-torsella-20181220.html

https://www.inquirer.com/philly/blogs/inq-phillydeals/apollo-sixers-josh-harris-kushner-trump-pension-investments-psers-sers-philadelphia-20180302.html

In 2020 to big publicity PSERS ‘froze’ its Apollo investments

https://www.dailymail.co.uk/news/article-8865169/One-biggest-public-pension-funds-freezes-new-investments-Apollo-Global-Management.html

Wisconsin (SWIB) Apollo Credit

Appendix: Senator Wyden’s Findings on Apollo Founder Leon Black

In a March 20, 2026 letter, Senator Ron Wyden details extraordinary financial dealings between Apollo co-founder Leon Black and Jeffrey Epstein, including $170 million in payments between 2012 and 2017—amounts far exceeding what Black paid elite law firms for similar estate planning work. Wyden notes that, according to a U.S. Virgin Islands settlement, Epstein used money paid by Black to help fund his sex trafficking operations, raising serious questions about whether these payments were truly for legitimate services . The letter highlights newly unsealed Department of Justice records suggesting the arrangement “went well beyond” traditional tax or estate planning and may have involved undisclosed or improper purposes. https://www.finance.senate.gov/imo/media/doc/senator_wyden_letter_to_leon_black_redacted.pdf

Wyden further raises concerns about potential financial misconduct, including evidence that payments to Epstein may have been channeled through a questionable 501(c)(3) structure to maximize tax deductions, and that Black’s estate planning arrangements involved $141 million in overpayments tied to Apollo-related partnership interests. Additional records cited in the letter suggest Epstein may have acted as an intermediary for payments to women and was involved in activities far removed from legitimate advisory services. Taken together, the Senate Finance Committee’s findings underscore that the Apollo–Epstein relationship is not merely historical—it presents unresolved questions about financial integrity, governance, and compliance that remain directly relevant to fiduciaries evaluating continued investment exposure. https://www.finance.senate.gov/continuing-epstein-investigation-wyden-questions-leon-black-over-new-revelations-in-epstein-files-appearance-of-hush-money-payments-and-surveillance-of-women