Wall Street keeps telling regulators, lawmakers, and plan sponsors that private credit in 401(k) plans is coming. That is the distraction. Private credit is not coming. It is already here. And not in the place anyone is debating.

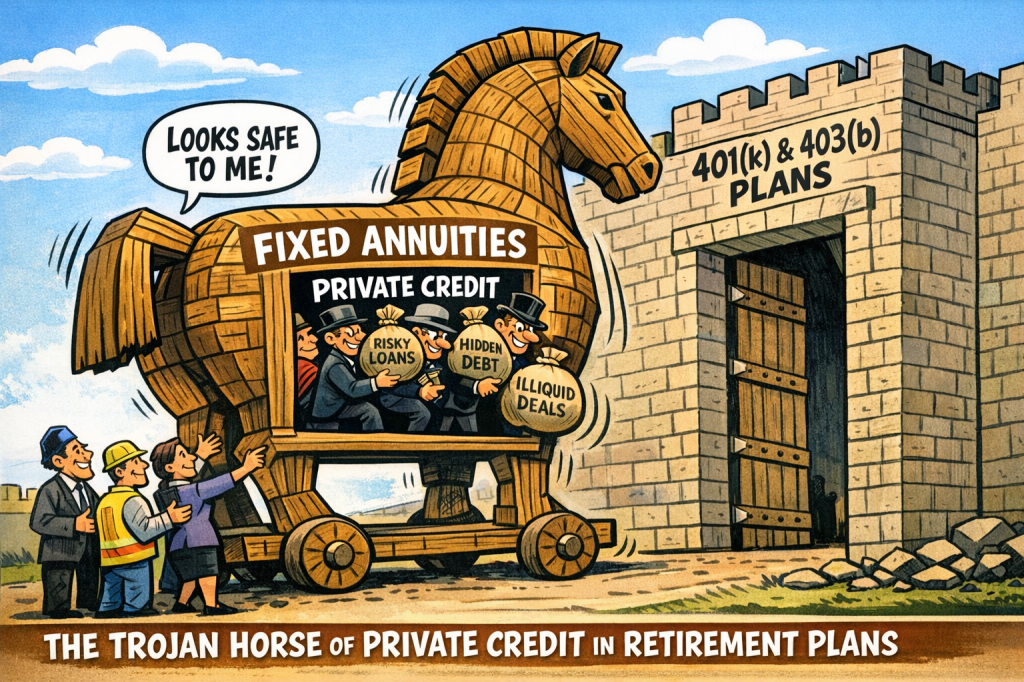

Roughly 98% of all private credit exposure inside 401(k) and 403(b) plans already sits inside one product: fixed annuities—buried inside insurance company general accounts where participants cannot see it, price it, or escape it. Of the 9000 401(k) and 403(b) plans with over $100 million in assets, over 3500 hold fixed annuities. For the over 700 thousand plans, probably half hold fixed annuities https://commonsense401kproject.com/2026/01/23/fixed-annuities-are-the-dirty-secret-hiding-in-401k-and-403b-plans/

The real scandal is not future allocations to private markets.

It is the massive, undisclosed private credit exposure already embedded in the system today.

The Misdirection: Target Date Funds with “Future” Private Credit, and Lifetime Annuities

The current policy debate focuses on whether private equity or private credit should be allowed inside target date funds. There is also a huge push for Lifetime Income Annuities

But today:

- Actual direct private credit exposure inside target date funds is minimal to negligible

- Lifetime income annuity adoption remains tiny with very low balances

- Most participants have no direct allocation at all

This is not where the risk is. This is narrative management. Some bait and switch pushing lifetime annuities, knowing that any rules encouraging them will make it easier to retain fixed annuities.

Where the Risk Actually Is: Fixed Annuities

As documented in, fixed annuities are the dominant hidden channel for private credit exposure in retirement plans. Issued by companies like Empower, Lincoln, TIAA, Prudential, Principal, Transamerica, MetLife, NYLife, and MassMutual. https://commonsense401kproject.com/2026/03/11/tiaa-traditional-annuity-is-a-prohibited-transaction/

Inside general account-backed fixed annuities:

- Assets are not participant-directed

- Portfolios are not transparently disclosed

- Credit quality is often self-rated or privately rated

- Valuations are not mark-to-market

And most importantly:

- These portfolios are heavily concentrated in private credit and private mortgages

Participants think they own a “safe”, stable product.

What they actually own is a black-box private credit fund wrapped in an insurance contract.

Insurance Companies = Private Credit Warehouses

Insurance company general accounts have quietly become some of the largest holders of private credit in the world. https://commonsense401kproject.com/2025/10/28/offshore-private-credit-creates-erisa-prohibited-transaction-risks-for-life-insurance-products-new-evidence-from-bis/

The structure works like this:

- Plans hand assets to the insurer

- The insurer invests heavily in illiquid private loans

- The insurer credits participants a smoothed, opaque rate

- The spread—often 100–200+ basis points—is retained

The participant bears:

- Credit risk

- Liquidity risk

- Valuation opacity

The insurer keeps:

- The upside

- The pricing control

- The information advantage

This is not a stable value product. It is a leveraged credit transformation machine with no transparency.

Synthetic Stable Value Solid

Synthetic Funds like Fidelity MIPS and Vanguard RST, and products from T.Rowe Price, Galliard, Invesco, are transparent diversified and do not contain private credit.

In the early 2000s, JPMorgan stable value hid a 15% sleave in private credit in their synthetic product, much like currently people are planning on hiding it in Target Date Funds. However, in the 2008 crisis, this private credit blew up, and a number of lawsuits followed. https://www.investmentnews.com/regulation-legal-compliance/jp-morgan-settles-lawsuit-on-alleged-fiduciary-breach-in-stable-value-funds/72643

Separate Accounts: The Illusion of Safety

Some defenders argue that separate account annuities are safer because assets are “segregated.”

But the reality is more dangerous:

- Investment guidelines are often broad or discretionary

- Insurers can swap out high-quality assets over time

- Replacement assets can include private credit or structured exposures

- Participants have no visibility into those changes

What begins as a conservative portfolio can quietly become something very different.

This is not transparency. https://commonsense401kproject.com/2025/07/28/the-great-annuity-mirage-how-separate-accounts-continue-to-mislead/ It is controlled opacity.

The “Guarantee” Myth

The final line of defense is always the same:

“Annuities are protected by state guarantee associations.”

That protection is largely illusory.

State guarantee associations:

- Are not pre-funded at meaningful levels

- Are dependent on assessments of other insurers during stress

- Have coverage caps

- Have never been tested against systemic private credit losses

They are not the FDIC. https://commonsense401kproject.com/2025/06/24/state-guarantee-associations-behind-annuities-are-a-joke/

They are a patchwork backstop for isolated failures—not a shield against industry-wide risk.

Calling this protection is like calling a fire extinguisher a sprinkler system.

They are not regulated by the SEC since fixed annuities are not allowed in SEC registered mutual funds. They are regulated by State Insurance Commissioners which is why the Wall Street Journal just called the Insurance commissioner of Iowa the biggest US regulator of Private Credit https://www.msn.com/en-us/money/markets/how-keeping-private-credit-safe-became-iowa-s-problem/ar-AA1Z40s8

Why the 98% Number Matters

If you step back, the structure becomes clear:

- Direct private credit in 401(k)s: minimal

- Private credit in annuity general accounts: massive

- Transparency: none

- Pricing: controlled by the insurer

- Benchmarking: impossible

So when policymakers debate “whether to allow private credit in retirement plans,” they are debating the wrong question.

The correct question is:

Why is nearly all of the existing private credit exposure hidden inside products that avoid ERISA transparency altogether?

The Legal Problem: A Prohibited Transaction Hiding in Plain Sight

Under ERISA, this structure raises unavoidable issues:

- The insurer is a party in interest

- The insurer controls pricing, valuation, and crediting rates

- The insurer profits from undisclosed spreads

- The participant bears undisclosed risk

That is the textbook definition of a conflicted transaction.

And under the framework reinforced by Cunningham v. Cornell:

- The burden shifts to the defendant

- Exemptions must be proven

- Compensation must be reasonable and transparent

Hidden private credit exposure inside opaque annuity structures fails that test. https://commonsense401kproject.com/2026/03/11/stable-value-industry-admits-synthetic-funds-are-safer-and-why-that-makes-general-account-annuities-a-prohibited-transaction/

Conclusion: The Risk Is Not Coming—It’s Already Embedded

The retirement industry wants regulators focused on the future:

- Private credit in target date funds

- Innovation

- Access

But the real story is already written:

- Private credit is already dominant inside retirement plans

- It is concentrated in the least transparent structures

- It is priced by conflicted parties

- And it is invisible to participants

This is not a debate about whether private credit belongs in 401(k)s.

It is a reckoning with the fact that it already dominates them, just hidden where no one is supposed to look.