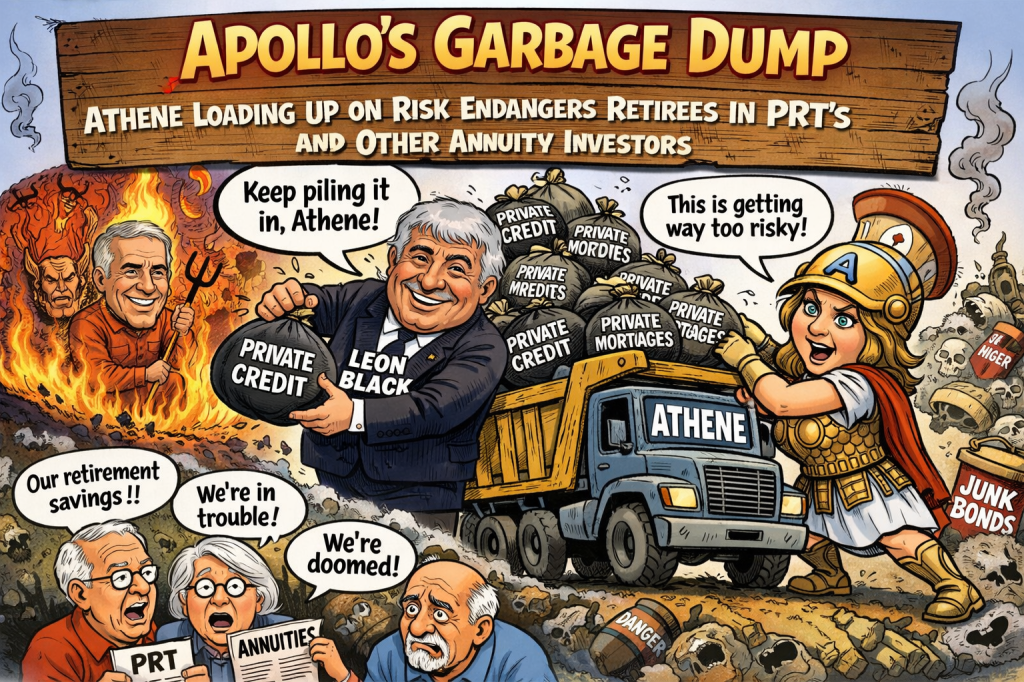

Apollo wants you to believe Athene is the safest part of the machine. The reality is the opposite. Apollo’s Private Credit and Private Mortgages many worth 70 cents on the dollar can hide their losses on the Athene balance sheet. If those loans are mispriced—or deteriorate—Athene absorbs the damage. https://commonsense401kproject.com/2026/03/24/the-401k-private-credit-lie-98-of-the-risk-is-already-there-hidden-inside-annuities/

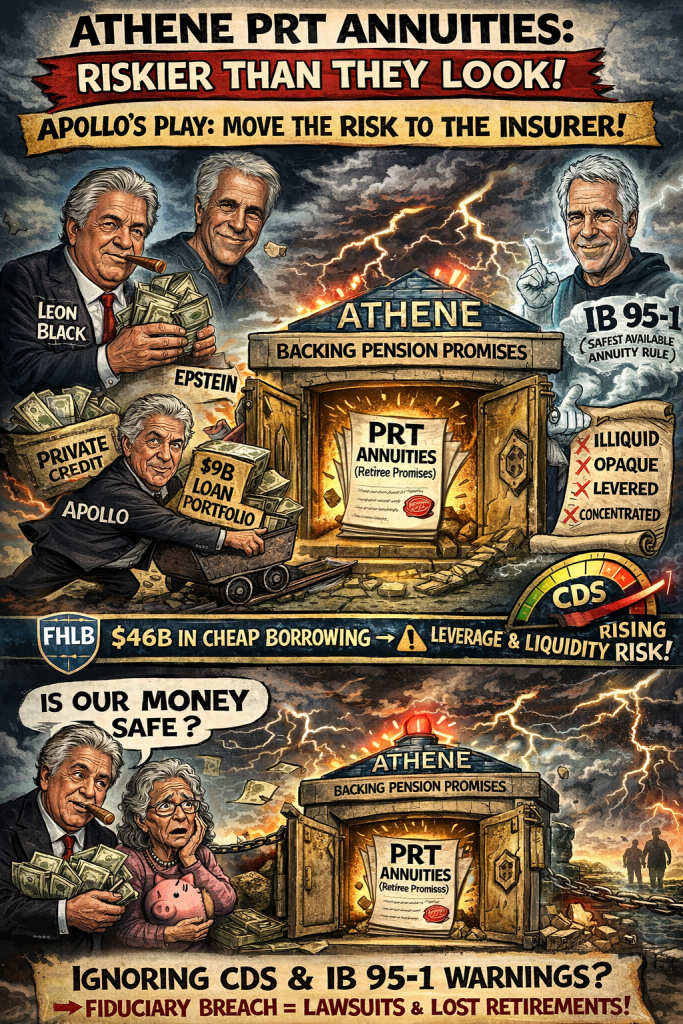

The latest transaction—shifting a $9 billion commercial real estate loan portfolio into Athene—is being sold as a “balance sheet upgrade.” https://www.ainvest.com/news/athene-9b-fhlb-liquidity-edge-clashes-regulatory-overhang-2603/ In plain English, Apollo is moving risk out of a public vehicle and into the insurance company and hiding the losses.

Athene relies on weak regulation from the Iowa Insurance Commissioner that never marks to market their losses in Private Credit and Private Mortgages. https://www.msn.com/en-us/money/markets/how-keeping-private-credit-safe-became-iowa-s-problem/ar-AA1Z40s8

Athene relies on the Federal Home Loan Bank Des Moines for cheap Leverage with access to a credit line of over $46 billion. Athene is borrowing against its balance sheet to fund higher-yielding private credit and real estate assets. That is not liquidity. That is spread-driven leverage built on government-supported funding. https://retirementincomejournal.com/article/annuity-issuers-atm-the-fhlbs/ https://www.bloomberg.com/news/articles/2026-03-25/apollo-s-insurance-arm-vaults-to-second-biggest-fhlb-borrower?

Apollo originates private credit, Athene and public pensions buy it https://commonsense401kproject.com/2026/03/23/divest-from-apollo-now-before-markets-courts-or-congress-force-it/ Spread flows back to Apollo. Apollo is counting on weak regulators not forcing mark to market on Athene, and public pensions afraid of the political fallout from losses and excessive fees they were hiding from taxpayers.

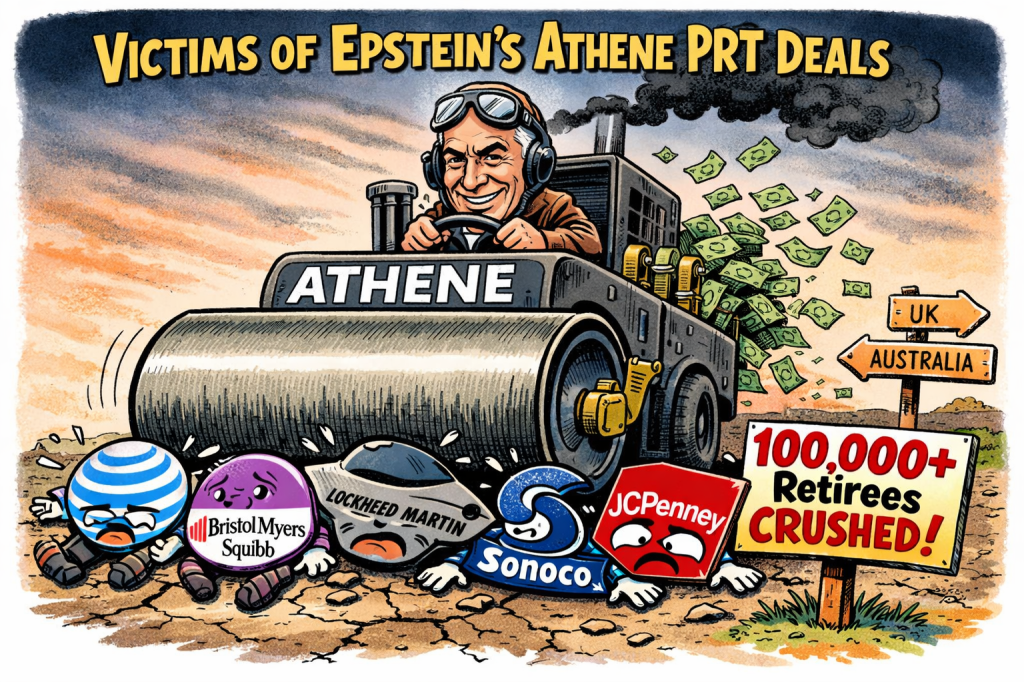

Worse is that many Corporate pensions replaced PBGC insured diversified portfolios with an Athene Pension Risk Transfer (PRT) Annuity. https://commonsense401kproject.com/2026/02/25/jeffrey-epsteins-pension-destruction-engine-athene/ The Trump DOL has tried to help Apollo by swaying Athene PRT Court Cases. https://commonsense401kproject.com/2026/01/11/dols-prt-annuity-amicus-brief-dismantling-erisa/

PRT annuities depend on one thing: The long-term financial strength of the insurer. But now that insurer Athene is: Increasing leverage via FHLB, Absorbing large real estate loan portfolios, Exposed to private credit stress, and Operating under prior regulatory violations

Plan Fiduciaries when choosing a PRT annuity under IB 95-1 must evaluate: The financial strength of the insurer, The quality and diversification of assets, The insurer’s ability to make future payments, The structure of the transaction ie Does it have a Downgrade Clause or not https://commonsense401kproject.com/2026/01/09/retirement-plans-must-demand-downgrade-provisions-for-any-annuity/

Athene PRT’s do not meet these requirements. While some courts have protected Apollo by blocking transparency https://commonsense401kproject.com/2025/11/06/prts-why-courts-keep-ignoring-the-dangers-of-pension-risk-transfer-annuities-and-why-these-cases-must-be-appealed/ I am hopeful these cases will be appealed.

Athene paid a $45 million penalty for improper PRT activity in April 2020, after an investigation found its pension risk transfer (PRT) business had solicited and placed group annuity contracts with an unlicensed subsidiary. The Department of Financial Services cited violations of New York Insurance Law, noting the subsidiary had entered into 14 large-scale pension risk transfer transactions involving thousands of New York policyholders. https://www.dfs.ny.gov/reports_and_publications/press_releases/pr202004132

The American Federation of Teachers and the American Association of University Professors filed a complaint letter to the SEC on Apollo that specifically mentions Athene.

https://www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf Specifically that “Rowan met with Epstein at his New York City mansion on Jan. 14, 2016.6 It is likely at this meeting that they discussed what Epstein described as involving “Athene, Montauk Rothschild. Planes boats etc.”

SEC complaint footnote refers to a specific Epstein file

https://www.justice.gov/epstein/files/DataSet%209/EFTA00305994.pdf In an email on April 15, 2015 from Jeffrey Epstein to Melanie Spinella and Redacted (possibly Leon Black of Apollo).

I believe your decision re only paying 20m has frankly, left me felling quite uneasy, colors my view about the Athene or Rothschild transaction. ……Athene,income, capital,foreign, exit, corporate, insurance regs, out and inbound issues, basis, appropriate discount rates. ? …….We can talk about Rowen request re Athene, complex 2 billion in taxes on transaction. ?

Rowen refers to Apollo CEO Marc Rowen who previously filed an SEC report in which he claimed no contact with Epstein or his involvement with Apollo issues like Athene.

Rising CDS spreads (market signaling higher credit risk) Renewed scrutiny from Epstein-related disclosures and Ongoing litigation risk at Apollo and the conclusion becomes unavoidable: The risk profile of Athene-backed annuities is increasing—not decreasing.

Apollo says Athene’s access to cheap government-backed FHLB funding makes annuities safer. In reality, it allows them to load more risk onto the balance sheet that retirees depend on. The $9 billion commercial real estate loan transfer isn’t a sign of strength. It’s a signal that the risks of private credit and real estate are being quietly shifted into the very entity that is supposed to guarantee pension benefits.