The headlines are starting to catch up. Private credit is wobbling. Defaults are ticking up. Liquidity is tightening. Retail investors—particularly in interval funds and BDCs—are facing gates and delays.

But if you believe the media narrative, you would think this is primarily a retail-driven problem.

It’s not.

Retail is the visible edge of the iceberg, not the mass beneath it.

Follow the Real Money

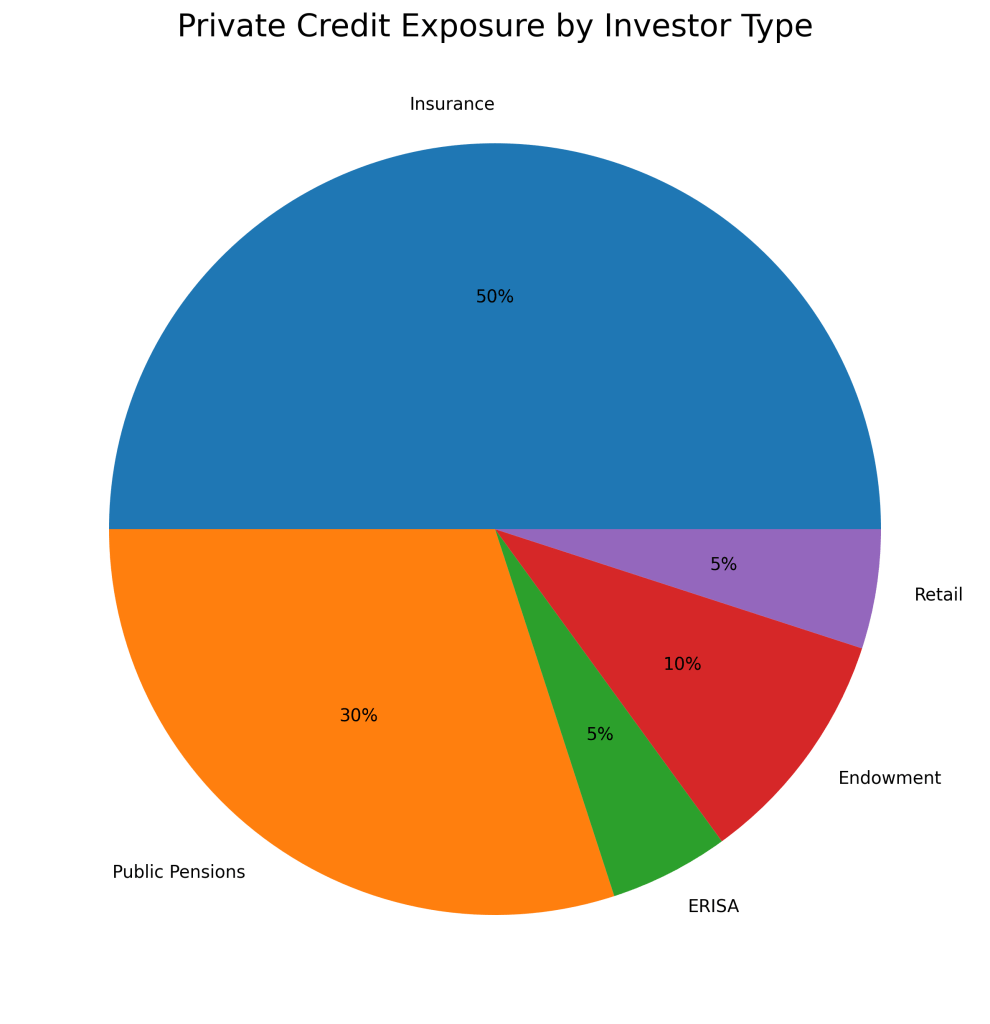

If we step back and look at where private credit actually sits in the U.S. financial system, a very different picture emerges:

- ~50% — Life Insurance Balance Sheets

- ~30% — Public Pensions

- ~5% — ERISA Plans / 401(k)s

- ~10% — Endowments & Foundations

- ~5% — Retail / Wealth Channels

Even if you debate the exact percentages, the conclusion is unavoidable:

Roughly 80% of private credit is held by institutions that have every incentive to avoid marking assets to market.

And that is why this “meltdown” is going to take time. https://commonsense401kproject.com/2026/03/07/private-credit-the-30-markdown-nobody-wants-to-admit/

The Incentive to Delay Reality

1. Life Insurers: The Epicenter of Risk

Life insurers—particularly those tied to private equity sponsors—are now the largest holders of private credit.

These assets sit inside:

- General accounts

- Fixed annuities

- Pension Risk Transfer (PRT) deals

The problem is simple:

- If insurers mark private credit down,

→ capital ratios fall

→ ratings agencies react

→ regulators demand more capital

And that triggers a cascade:

- Lower ratings → less annuity sales

- Higher capital requirements → lower profitability

- Potential liquidity stress

Annuity Litigation https://commonsense401kproject.com/2026/03/01/annuities-as-prohibited-transactions-in-retirement-plans/ https://commonsense401kproject.com/2026/01/23/fixed-annuities-are-the-dirty-secret-hiding-in-401k-and-403b-plans/

So what do insurers do?

They don’t mark to market unless they absolutely have to.

Instead:

- Assets are held at book value

- Internal models and private ratings dominate

- Loss recognition is delayed

2. Public Pensions: The Second Pillar of Denial

Public pensions are the second largest holders of private credit—and arguably the most politically sensitive.

Unlike insurers, their constraint isn’t regulatory capital.

It’s optics and incentives.

If public pensions mark private credit to market:

- Reported returns fall

- Funded status deteriorates

- Contribution pressure rises

And perhaps most importantly:

Performance bonuses disappear.

Many large public plans pay millions in incentive compensation tied to reported returns—returns that are increasingly influenced by illiquid, model-priced assets.

There is no appetite to unwind that system.

A Tenfold Shift Hidden in Plain Sight

Over the past 10–15 years, public pension exposure to private credit has exploded.

From:

- A niche allocation embedded in private equity

To:

- A core portfolio pillar

The growth is staggering:

Roughly 5x–10x increase in exposure—direct and indirect

And it accelerated in the post-2010 era of:

- Low interest rates

- Yield chasing

- “Alternative income” narratives

But unlike public bonds:

- These investments are often no-bid

- Illiquid

- Valued by models, not markets

The Fee Machine Behind It All

Private credit is not just about yield.

It is about fees.

Compared to traditional investment-grade bond management:

- Private credit can carry 5x–10x higher total fees

- Management fees

- Origination fees

- Structuring fees

- Monitoring fees

- Hidden spreads (especially in insurance wrappers)

These are not transparent, competitive markets.

They are often:

- Negotiated contracts

- With limited bidding

- And limited disclosure

The Political Economy Problem

Here’s where things get uncomfortable.

Since the Citizens United v. FEC decision:

- Political donations—especially at the state level—have become less transparent

- Financial firms have gained greater influence over public policy

At the same time:

- High-fee asset managers benefit disproportionately from:

- Pension allocations

- Insurance partnerships

- Alternative investment mandates

It is not unreasonable to ask:

Do higher-fee managers have stronger incentives—and greater ability—to influence allocation decisions than low-fee managers?

That question has barely been explored.

But it should be.

Because public pensions sit at the intersection of:

- finance

- politics

- opacity

Why This Won’t Unwind Quickly

The key players—insurers and pensions—share a common goal:

Delay recognition of losses as long as possible.

That means:

- No forced selling (unlike retail funds)

- Limited observable pricing

- Gradual, smoothed-down valuations

In other words:

This is not a mark-to-market crisis. It is a mark-to-model slow burn.

The Real Risk

The danger is not that private credit collapses overnight.

The danger is that:

- Losses accumulate silently

- Risk is mispriced for years

- And when recognition finally comes…

→ it hits the system all at once

Through:

- Insurance balance sheets

- Pension funding gaps

- Reduced retirement security

Final Thought

Retail investors may be the first to feel the pain.

But they are not the system.

The system is:

- Life insurers

- Public pensions

And both are structurally incentivized to pretend nothing is wrong.

That is why:

The private credit meltdown won’t be fast, visible, or orderly.

It will be slow.

It will be opaque.

And when it finally surfaces, it will be far larger than anyone currently admits.

———————————————————————————