Public pensions, normally the first to lead securities fraud cases, have been notably absent from the Apollo/Epstein stock drop litigation. That absence may reflect a deeper conflict: the same pensions that could sue Apollo for misleading disclosures are heavily invested in its private equity and private credit funds, where valuations remain opaque and untested.

In every major stock drop case, public pensions rush to the courthouse. This time, they haven’t—and that silence may be more revealing than any lawsuit. When your investment manager controls not just your stock portfolio but your private equity, your credit book, and your reported returns, suing becomes more than a legal decision—it becomes a threat to the entire system.”

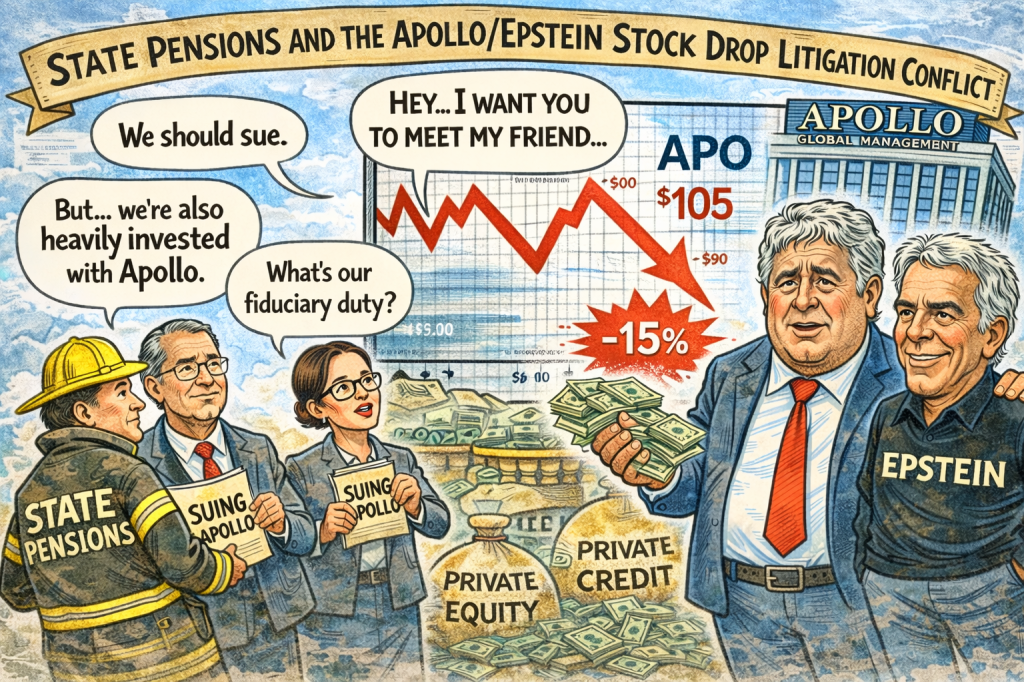

Public pensions. have the largest losses, the best lawyers, and a fiduciary duty to act.

From Enron to Wells Fargo to Boeing, state and union pension funds have led the charge—often becoming lead plaintiffs in billion-dollar securities cases.

So when Apollo Global Management lost billions in market value amid new disclosures tied to Jeffrey Epstein, the expectation was simple: Public pensions would sue. But so far, they haven’t. And that silence may tell you everything you need to know.

In 2019 and again in 2021, many institutional investors were told, in substance, that the Epstein problem at Apollo was largely personal to Leon Black and was being cleaned up. Almost all public pensions blindly accepted Apollos’ work. However, Epstein files released in February 2026 showed this to be a lie. Teacher Unions AFT & AAUP’s complaint to the SEC directly challenges that sanitized version, arguing that the public record now suggests a broader and deeper institutional relationship. https://www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf

Apollo is now facing a Classic Stock Drop Case with multiple securities lawsuits alleging: Misleading disclosures about its relationship with Epstein. Failure to fully inform investors about the scope of those ties. Material omissions that affected stock valuation https://www.bitget.com/amp/news/detail/12560605353269

This is standard Rule 10b-5 territory—the same legal framework used in nearly every major securities fraud case. The stock fell sharply following new reporting and disclosures.

Law firms quickly filed class actions. Everything about this case looks familiar—except one thing: The usual plaintiffs are missing.

Historically, public pensions dominate these cases: They step in because: They hold large positions. Courts prefer institutional investors as lead plaintiffs. They can drive litigation strategy. But in the Apollo/Epstein litigation: No major public pension has stepped forward.That is not normal. That is the story.

Apollo is not just another stock. A private equity manager. A private credit lender. A core counterparty to pension systems. Limited partners in Apollo private equity funds. Investors in Apollo private credit vehicles. They are clients, partners, and counterparties—not just shareholders.

More than 60 major US Public Pension plans NY,CA,OH,FL,TX etc. have $ multimillion exposure to Apollo Private Equity and Private Credit – See list at bottom https://commonsense401kproject.com/2026/03/23/divest-from-apollo-now-before-markets-courts-or-congress-force-it/

The risk to public pensions is valuation risk. Private equity and private credit are: Not marked to market valued internally or with lagged models. Litigation could expose overvaluation and conflicts leading to huge portfolio write downs, lower reported returns, and lower pension investment staff bonuses. These billions in hidden losses would be a huge political issue for state pensions.

Contrast Apollo with prior Epstein-related cases: Banks like Barclays faced investor lawsuits and public pensions were willing to engage. But Apollo is different. Because Apollo sits at the center of: Private credit, Private equity, and Pension return assumptions.

The biggest risk to pensions is not the stock drop. It is what discovery could reveal: Internal valuation practices, Private credit exposures, Conflicts between investor disclosures and internal knowledge.

In every major securities fraud case, public pensions rush to the courthouse. This time, they haven’t. And that silence is not accidental. When your investment manager controls your private equity, your credit book, and your reported returns, suing them is no longer just a fiduciary decision—it’s a systemic risk.”

The Epstein files raised questions about power and accountability. The Apollo lawsuits may answer a different question: Who is willing to act—and who is too exposed to speak?