Tomorrow marks a quiet but potentially transformative development in the credit markets: the launch of the CDX Financials index, administered by S&P Global.

At first glance, this may look like just another derivatives benchmark. It isn’t. For those of us focused on ERISA fiduciary risk, annuity opacity, and prohibited transactions, this is a major step toward finally quantifying what insurers have long kept hidden.

What Is CDX Financials—and Why It Matters

6

The CDX Financials index is a standardized basket of credit default swaps (CDS) referencing major financial institutions—insurers, asset managers, and banks. It will trade daily, providing transparent, market-based pricing of credit risk.

Critically, the index includes names central to the retirement system:

- Apollo Global Management (via Athene / Apollo Debt Solutions)

- Lincoln National Corporation

- Prudential Financial

- American International Group

- MetLife

These are not abstract entities—they are the core counterparties behind fixed annuities, stable value products, and pension risk transfer (PRT) deals.

Why This Changes the Game for Annuities

For years, insurers have argued that:

- Credit risk is “long-term” and not mark-to-market

- Crediting rates are sufficient proxies for safety

- Benchmarks like money markets or Hueler are “good enough”

That framework collapses with daily CDS pricing.

CDS spreads provide a real-time, market-based measure of default risk. When spreads widen, the market is signaling:

“This insurer is becoming riskier—right now.”

That matters because:

- Fixed annuities are 100% exposed to a single insurer balance sheet

- PRT annuities replace PBGC protection with insurer credit risk

- Participants are not compensated for that risk transparently

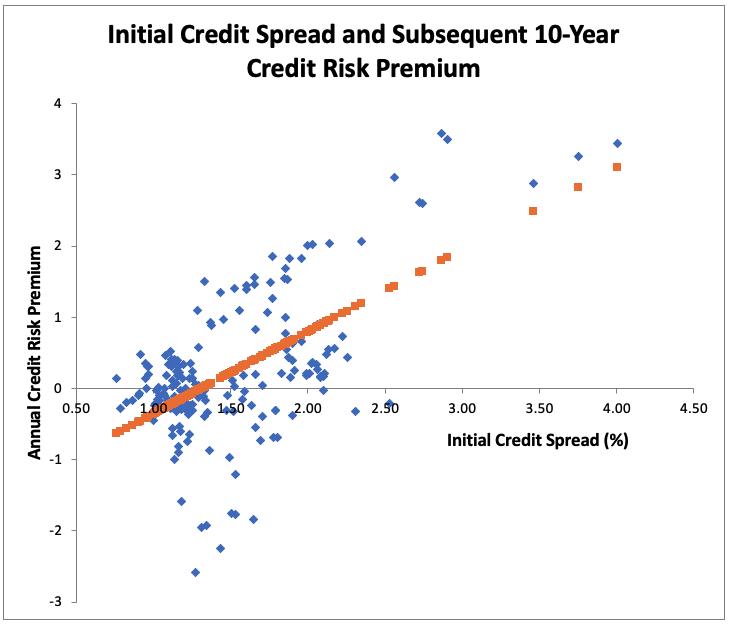

From Theory to Damages: A Litigation Breakthrough

5

You’ve already laid the groundwork in your CDS framework:

👉 https://commonsense401kproject.com/2025/10/29/annuity-risk-measured-by-credit-default-swaps-cds/

The CDX Financials index now enables something courts have struggled with:

A Clean Damages Framework

- Observe CDS spread for insurer (e.g., Athene, Prudential)

- Translate spread into implied credit risk premium

- Compare to participant credited rate

- Quantify under-compensation for risk

This directly supports:

- §404 prudence claims (failure to evaluate risk)

- §406 prohibited transaction claims (hidden spread extraction)

- Post-Cunningham v. Cornell burden shifting

In short:

CDS turns “opaque insurer discretion” into measurable economic harm.

Spillover Effect: Pricing the Unpriced

Even insurers not included in CDX will feel the impact.

Why?

- CDS markets are relative-value driven

- Traders will arbitrage spreads between index constituents and non-constituents

- This creates shadow pricing for the entire insurance sector

So even if a plan uses:

- A smaller insurer

- A separate account annuity

- A white-labeled stable value product

…it becomes increasingly difficult to argue:

“There is no observable market price for this risk.”

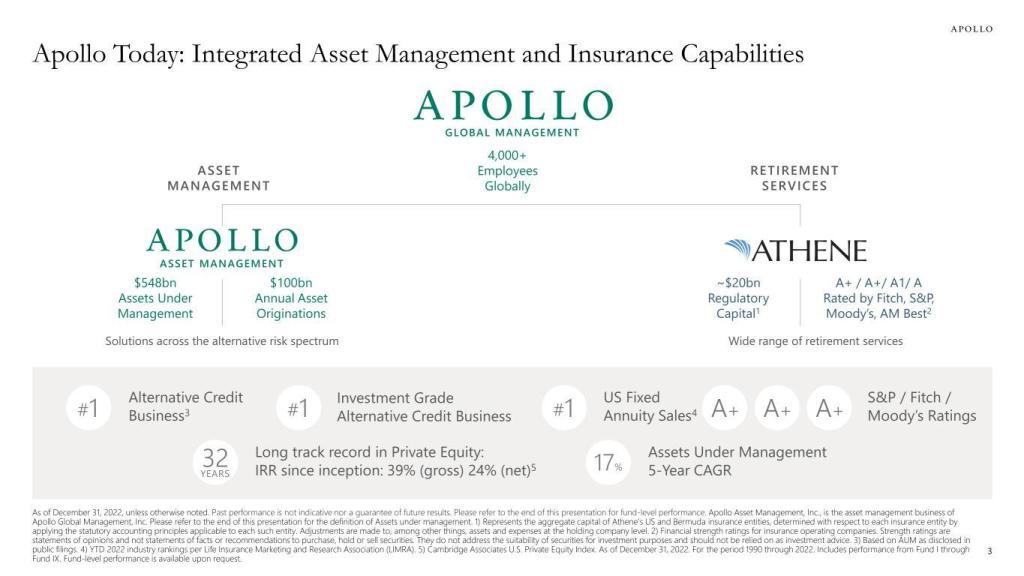

The Apollo / Athene Problem Comes Into Focus

7

This is where the implications become particularly acute.

Firms like Apollo Global Management have built insurance platforms (notably Athene Holding) that:

- Load general accounts with private credit and private mortgages

- Rely on internal or lightly regulated valuation frameworks

- Generate profits through spread capture, not disclosed fees

CDS pricing cuts through that opacity.

If Athene’s CDS widens while:

- Crediting rates stay flat

- Or lag peers

…it becomes powerful evidence that:

Participants are bearing increasing credit risk without compensation. https://commonsense401kproject.com/2026/03/26/apollos-garbage-dump-athene-loading-up-on-risk-endangers-retirees-in-prts-and-other-annuity-investors/

Implications for Fiduciaries—No More Excuses

With CDX Financials:

- Daily, independent credit pricing exists

- Comparable insurers are observable

- Risk-adjusted comparisons are feasible

Fiduciaries can no longer credibly claim:

- “We didn’t have a benchmark”

- “Risk was unobservable”

- “All insurers are roughly the same”

That argument was already weak. Now it’s gone.

What Comes Next

This is just the beginning.

Expect:

- Expert reports incorporating CDS curves and CDX spreads

- Discovery requests for insurer hedging and internal credit models

- Damages models tied to spread widening over time

- Increased scrutiny of:

- PRT annuities

- Stable value wrap providers

- Fixed annuity options in 401(k)s

Bottom Line

The launch of CDX Financials is not just a market event—it is a transparency event.

For decades, insurers have operated in a space where:

- Credit risk was hidden

- Spreads were undisclosed

- Benchmarks were manipulated or meaningless

Now, with daily CDS pricing:

The market is finally putting a price on the risk that participants were forced to bear in the dark.

And once risk is priced…

liability is not far behind.