Much has been written about retail investors getting trapped in private credit funds—gates, redemption limits, and liquidity mismatches at firms like Blackstone and Blue Owl.

But that narrative misses the real story.

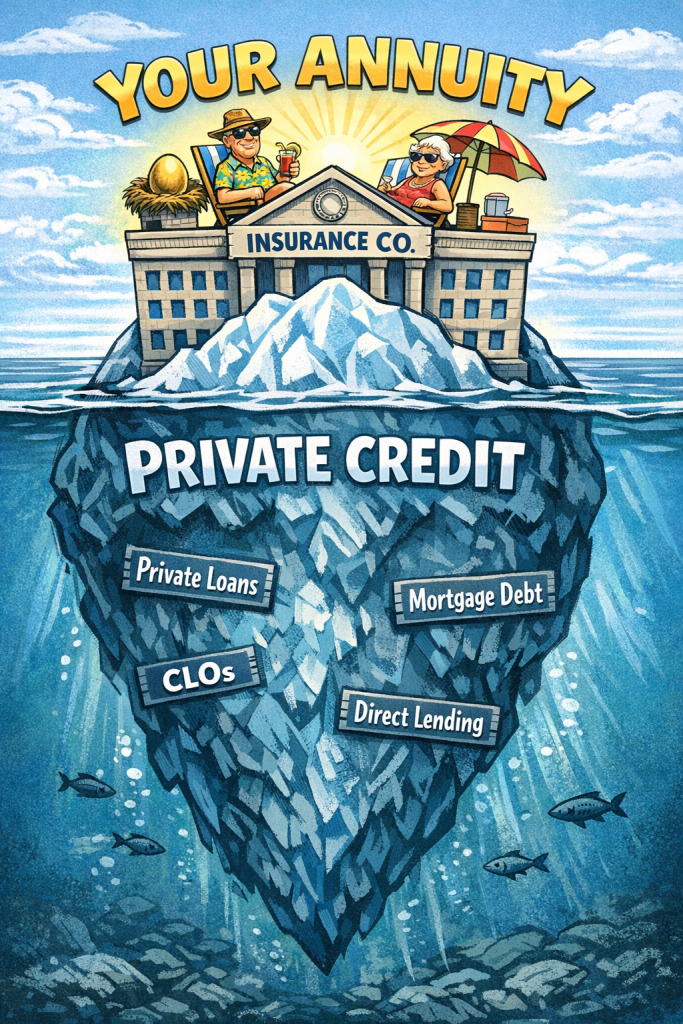

The largest exposure of individual investors to private credit is not in retail funds at all.

It is inside the annuities they already own.

And it’s not even close.

The Hidden Portfolio Behind Annuities

U.S. life insurers hold roughly $4.4 trillion in annuity reserves. That is the pool of money backing:

- Fixed annuities

- Indexed annuities

- Pension Risk Transfer (PRT) annuities

What backs those promises?

Not Treasuries. Not traditional investment-grade bonds.

Increasingly, it is private, illiquid credit:

- Private placements

- Direct lending

- CLO tranches and structured credit

- Commercial and residential mortgage loans

- Real estate debt

- Asset-backed private lending

Let’s be clear:

A mortgage loan originated and held by an insurer is economically indistinguishable from private credit.

It is:

- Privately negotiated

- Illiquid

- Not mark-to-market

- Often internally or privately rated

Calling it “mortgage lending” instead of “private credit” is a labeling exercise, not a risk distinction.

Do the Math—Even Conservatively

Public data shows:

- ~$849 billion in private placements

- ~$788 billion in mortgage loans

- ~$1.7 trillion in private bonds

Even if you take a conservative approach and only count:

👉 Private placements + mortgage loans = ~$1.6 trillion

Annuities represent roughly two-thirds of insurer liabilities.

That implies:

👉 Hundreds of billions to over $1 trillion of private/illiquid credit exposure backing annuity investors

And that is before fully counting structured credit and internally rated assets.

Retail Private Credit Is Smaller Than You Think

The products dominating headlines:

- Non-traded BDCs: ~$230 billion

- Credit interval funds: ~$120 billion

Total: ~$350 billion

That is what the media calls “retail private credit.”

Compare that to annuities:

👉 3x–5x larger exposure—minimum

👉 Far less transparent

👉 Far less understood by investors

The industry is focused on the storefront window.

The real risk sits in the warehouse.

Apollo, Athene, and the Industrialization of Private Credit in Annuities

No firm better illustrates this transformation than Apollo Global Management and its insurance affiliate Athene.

Apollo’s model is simple:

- Acquire or control an insurance balance sheet

- Use it as a permanent capital vehicle

- Allocate heavily to private credit, private mortgages, and structured assets

- Capture spread between portfolio yield and credited rate

Athene is not an outlier—it is the model.

This is the financialization of retirement savings:

- Annuities become funding vehicles

- Private credit becomes the asset base

- Spread becomes the profit engine

From a participant perspective:

👉 You think you own a “guaranteed product”

👉 You actually own exposure to a leveraged, opaque credit portfolio

This is particularly acute in:

- Pension Risk Transfers (PRTs)

- Fixed indexed annuities

- Stable value products backed by general accounts and most separate account products

Where credit risk, liquidity risk, and valuation risk are all concentrated in a single entity.

The Illusion of Safety

Retail private credit investors know they are taking risk.

Annuity investors are told they are avoiding it.

They hear:

- “Guaranteed”

- “Principal protection”

- “Stable value”

- “Lifetime income”

But in reality, they are exposed to:

- Illiquid credit portfolios

- Discretionary crediting rates

- Opaque valuation processes

- No meaningful benchmark

And most importantly:

👉 No way to measure the spread being extracted from them

The Regulatory Blind Spot

Regulators focus heavily on:

- Retail fund liquidity

- Redemption gates

- Investor suitability

But largely ignore:

👉 Private credit embedded in annuity balance sheets

Why?

Because annuities sit in the insurance regulatory regime, not the securities regime.

That means:

- No daily NAV

- Limited disclosure

- Heavy reliance on internal or private ratings

- Minimal transparency into underlying holdings

In short:

👉 More risk, less visibility

The Real Risk Isn’t Gates—It’s Mispricing

Retail private credit funds can gate investors.

Annuities do something more dangerous:

👉 They hide risk through smoothing

- Losses are delayed

- Valuations lag reality

- Crediting rates are discretionary

The investor never sees volatility.

Until it shows up as:

- Lower crediting rates

- Reduced benefits

- Or in extreme cases, solvency stress

The Bottom Line

The financial media is focused on the wrong problem.

Retail private credit funds are:

- Visible

- Controversial

- Relatively small

The real giant is hidden:

👉 The U.S. annuity market is the largest conduit of private credit exposure to individual investors

And it operates with:

- Less transparency

- Less accountability

- Less investor understanding

Mortgage loans, private placements, structured credit—it’s all the same story:

👉 Illiquid credit risk wrapped in the language of safety

Appendix: CDS Pricing and the Missing Downgrade Trigger

One of the most important—and completely ignored—tools for evaluating annuity risk is credit default swap (CDS) pricing.

CDS spreads provide a real-time, market-based measure of insurer credit risk.

Yet:

- Plan sponsors rarely review CDS levels

- Regulators do not require it

- Contracts almost never include downgrade protection mechanisms

This is a critical failure.

Why CDS Matters

For firms like Athene, CDS spreads reflect:

- Exposure to private credit

- Structured asset risk

- Liquidity concerns

- Market perception of solvency

When CDS spreads widen, the market is signaling:

👉 Rising default risk

But annuity investors see none of this.

The Missing Protection: Downgrade Triggers

In institutional markets, credit-sensitive contracts often include:

- Downgrade triggers

- Collateral posting requirements

- Termination rights

Annuities and PRT contracts typically include none of these.

That means:

👉 Participants are locked into a single-entity credit exposure

👉 With no exit mechanism as risk rises

Which is why I believe most Annuity contracts are ERISA prohibited transactions in retirement funds

What Should Be Required

At a minimum:

- CDS monitoring as part of fiduciary review

- Contractual downgrade triggers

- Transparency into general account asset allocation

- Benchmarking against market credit yields

Without these protections:

👉 Annuity investors are effectively uncompensated credit risk providers

Final Thought

If CDS spreads are rising…

If private credit exposure is growing…

If downgrade protections are absent…

Then the conclusion is unavoidable:

👉 Annuities are not eliminating risk—they are concentrating and concealing it