Annuities are Prohibited

Under ERISA §406, any transaction between a plan and a “party in interest” — such as the plan’s insurer, recordkeeper, or trustee — is per se prohibited. That includes the purchase or maintenance of a fixed annuity contract from an insurer that profits from spreads, affiliated services, or undisclosed compensation.

The insurance industry routinely claims that these annuity deals qualify for a Department of Labor “Prohibited Transaction Exemption” (PTE), such as PTE 84-24 or PTE 2020-02. But in decades of reviewing contracts and filings, I have never seen a single annuity that could actually pass the exemption test.

Each PTE requires that:

- Compensation be reasonable and disclosed;

- The transaction be in the best interest of participants; and

- No misleading statements be made.

Annuities fail on all three. They hide 100–150 basis points of spread profits; they trap plan assets with no downgrade or exit provisions; and their “guarantees” transfer risk from the plan sponsor to participants — all while enriching the insurer.

Even if an annuity could theoretically meet those tests — say, if it included a downgrade clause, full fee disclosure, and liquidity — the burden of proof would still rest with the fiduciary. The Second Circuit’s 2025 decision in Cunningham v. Cornell University clarified that once a prohibited transaction is alleged, it is the plan sponsor’s burden to prove an exemption applies.

In practical terms:

- Every fixed annuity is a prohibited transaction by default.

- The plan fiduciary must prove — not assume — that an exemption is valid.

- And in the real world, the insurance industry’s own opacity ensures they cannot meet that test.

The DOL’s “comfort letters” and outdated exemptions were drafted for a different era. In today’s world of offshore reinsurance, undisclosed spreads, and absent downgrade clauses, annuity exemptions are fiction. Fiduciaries relying on them are gambling with participants’ retirement security — and their own liability.

Appendix November 25, 2025

In the current 4 ongoing cases of fixed annuities as Prohibited Transactions filed since Cunningham V. Cornell, the defense is primarily trying to delay since in my opinion I think they know they have no valid legal defense.

Finally at the end of November a Motion to Dismiss came out that was full of deflections and noise and nothing of substance.

In the entire 27-page Motion to dismiss brief, plan:

❌ Never invokes §408

❌ Never claims PTE 84-24 applies

❌ Never claims §408(b)(2) applies

❌ Never argues the annuity contract is exempt under any DOL rule

❌ Never argues Annuities spread is “reasonable compensation”

❌ Never claims the plan assets are not being used for the insurer’s benefit

❌ Never argues the fiduciaries obtained “no less favorable terms than arms-length”

NOTHING

ERISA clearly says:

✔ Any transaction with any party-in-interest involving plan assets is prohibited.

✔ Any indirect compensation is prohibited.

✔ Any fiduciary self-dealing is prohibited.

Plan does not dispute ANY of these elements.

Thus:

There is no legally valid exemption defense anywhere in the MTD. Everything is noise. There appears to be no real defense for Fixed annuities as Prohibited Transactions

Appendix 1 : Single-Entity Credit Risk, Diversification, and the Illusory Safety of Annuities

A. Single-Entity Credit Risk and the Core Fiduciary Principle of Diversification

One of the most fundamental principles of fiduciary investing—embedded in ERISA §404(a)(1)(C)—is diversification. The purpose of diversification is not to enhance returns, but to eliminate uncompensated risk, particularly the risk that outcomes hinge on the solvency or behavior of a single counterparty. Courts, regulators, and modern portfolio theory all recognize that avoidable single-entity risk is presumptively imprudent unless justified by extraordinary countervailing benefits.

Insurance annuities offered in 401(k) plans violate this principle at their core. Whether structured as general-account fixed annuities, group annuity contracts or,pension risk transfer annuities. or insurance-wrapped collective investment trusts, these products expose participants to concentrated credit risk in a single life insurer. The participant’s principal and credited interest are not diversified across a portfolio of issuers; they are contingent on the ongoing solvency, capital management, reinsurance strategy, and asset allocation decisions of one institution.

By contrast, virtually every alternative capital-preservation vehicle available to ERISA fiduciaries—mutual funds, pooled stable-value funds, diversified bond funds—spreads credit exposure across dozens or hundreds of issuers and multiple guarantors. The elimination of single-issuer dependency is precisely the risk control diversification is meant to achieve.

The persistence of annuities in 401(k) plans therefore represents a stark departure from baseline fiduciary norms.

B. Why Annuities Are Structurally Inconsistent with ERISA Diversification Standards

ERISA does not require fiduciaries to eliminate all risk, but it does require them to eliminate unnecessary and uncompensated risk. Single-entity credit exposure in annuities is both.

From a risk-return perspective, annuities offer no unique benefit that requires concentrating credit exposure in one insurer:

- They do not provide higher expected returns than diversified alternatives.

- They do not provide superior liquidity.

- They do not provide inflation protection.

- They do not provide diversification benefits relative to other plan assets.

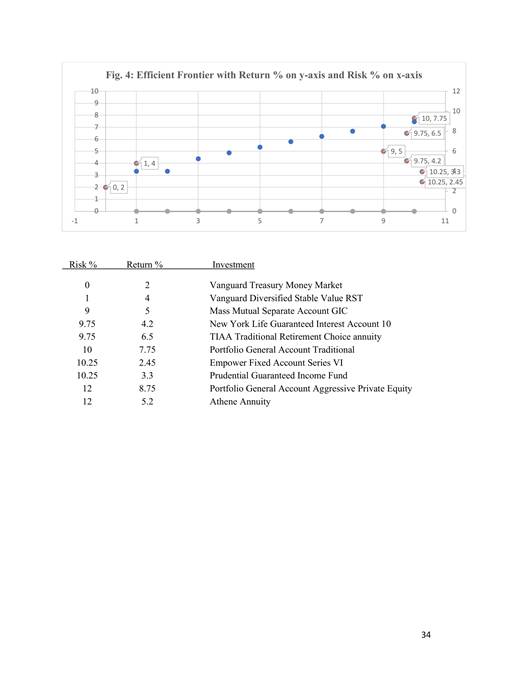

Indeed, as shown in prior work on the stable-value efficient frontier, single-insurer annuities typically lie below the efficient frontier—offering lower returns at higher risk than pooled stable-value products. When a fiduciary selects a product that increases credit risk while simultaneously reducing expected return, the decision cannot be reconciled with prudence.

The industry’s response—that insurers are “highly rated” or “heavily regulated”—misses the fiduciary point. Diversification is not optional merely because a counterparty is perceived as safe. Enron, Lehman Brothers, AIG, and Silicon Valley Bank were all highly rated until they were not. ERISA fiduciaries are not permitted to gamble participant assets on the continued health of a single institution when diversification is readily available.

C. Downgrade Provisions: The Risk Control That Annuities Systematically Avoid

One of the most telling features of annuity contracts used in retirement plans is the absence of meaningful downgrade provisions. In sophisticated fixed-income investing, downgrade triggers are standard risk-management tools. They allow an investor to:

- Terminate exposure if a counterparty’s credit deteriorates,

- Demand collateral or restructuring,

- Reallocate assets before losses become irreversible.

In the annuity context, downgrade provisions would allow a plan fiduciary to exit or mitigate exposure if the insurer’s credit profile weakens—precisely the moment when participant assets are most at risk.

Yet most annuity contracts offered in 401(k) plans either:

- Contain no downgrade trigger, or

- Include downgrade language so weak or discretionary as to be meaningless, or

- Impose punitive market-value adjustments that deter fiduciaries from exercising exit rights.

This omission is not accidental. Downgrade provisions reduce insurer profitability by constraining asset allocation, limiting leverage, and curtailing the ability to extract spread income from riskier assets. As a result, insurers systematically resist contract terms that would allow fiduciaries to respond rationally to credit deterioration.

From a fiduciary perspective, this is indefensible. A product that locks participants into a deteriorating credit exposure—while preventing fiduciaries from acting—is fundamentally inconsistent with prudence and loyalty.

D. Credit Default Swaps: The Risk Metric the Industry Does Not Want Fiduciaries to See

Credit default swaps (CDS) provide a market-based, continuously updated measure of default risk. Unlike credit ratings, CDS prices respond in real time to changes in asset quality, leverage, liquidity, and systemic stress. For sophisticated investors, CDS spreads are a primary tool for monitoring counterparty risk.

As demonstrated in prior analysis, CDS markets often price life insurers as meaningfully riskier than their ratings suggest. In some cases, CDS-implied default probabilities are an order of magnitude higher than what fiduciaries would infer from insurer marketing materials or statutory filings.

Yet CDS information is almost never disclosed or discussed in the annuity selection process. Insurers do not reference CDS spreads in participant disclosures, and plan fiduciaries are rarely encouraged—by consultants, recordkeepers, or insurers themselves—to examine them.

The reason is straightforward: acknowledging CDS-implied risk would undermine the core sales narrative of annuities as “safe” and “guaranteed.” Moreover, if fiduciaries explicitly recognized this risk, they would be compelled either to diversify away from single-insurer exposure or to demand risk-mitigating features that reduce insurer profitability.

Thus, the industry’s silence on CDS is not a neutral omission; it is a structural feature of a business model dependent on opacity.

E. Why the Suppression of Risk Controls Matters Under ERISA §406

The systematic avoidance of diversification, downgrade protections, and market-based credit risk metrics has direct implications under ERISA’s prohibited-transaction rules.

Annuities are per se transactions with a party in interest. To be lawful, they must qualify for an exemption. But exemptions require that compensation be reasonable and that transactions be in participants’ best interests.

A product that:

- Concentrates risk in a single counterparty,

- Prevents fiduciaries from responding to credit deterioration,

- Suppresses widely accepted risk metrics,

- And delivers inferior risk-adjusted returns,

cannot plausibly be described as “reasonable” or “in the best interests” of participants.

Moreover, the insurer’s resistance to downgrade provisions and risk transparency reveals the economic conflict at the heart of the annuity model: participant safety and insurer profitability move in opposite directions. ERISA does not permit fiduciaries to subordinate participant protection to a service provider’s profit margins.

F. Fiduciary Implications

Once single-entity credit risk is properly framed, the fiduciary implications become unavoidable:

- Diversification is not optional under ERISA; annuities violate it by design.

- Risk-mitigation tools exist (downgrade provisions, CDS monitoring, diversification), but are deliberately excluded from annuity contracts.

- The exclusion benefits insurers financially, not participants.

- Failure to address these risks cannot be cured by disclosure alone, because participants cannot diversify away insurer credit risk within the product.

Accordingly, annuities in 401(k) plans are not merely risky—they are structurally misaligned with ERISA’s fiduciary architecture. This misalignment supports the conclusion that, absent radical redesign, annuities should be treated as prohibited transactions rather than permissible investment options.

Appendix 2: Relevant Case Law — Disselkamp and SeaWorld in Support of ERISA Claims

I. Disselkamp v. Norton Healthcare, No. 3:18-CV-00048-GNS (W.D. Ky. Aug. 2, 2019)

Statement of the Rule (Share-Class Analogy):

In Disselkamp, the Western District of Kentucky held that a plan fiduciary’s choice of a higher-cost mutual fund share class when an identical lower-cost alternative was available states a claim under ERISA §404 even without alleging poor market performance, because the harm arises from the pricing decision itself:

“A fiduciary’s selection of an economically equivalent investment option with a materially higher cost constitutes a fiduciary breach when a lower-cost alternative was available.” (quoting Disselkamp, denial of motion to dismiss) — Disselkamp (cited throughout opinion).

Damages Framework:

The court emphasized that the continuing cost differential is the damage:

“The harm here is not cured by later monitoring or disclosure; rather, the excess costs persist and compound over the life of the investment.” — Disselkamp (see damages discussion).

Relevance to Annuities:

Fixed annuity contracts are priced through crediting rates, functionally analogous to a mutual fund’s expense ratio. A fiduciary’s selection of an annuity with a permanently lower crediting rate when superior alternatives were available mirrors the share-class violation in Disselkamp:

- Crediting rate differentials = economic cost differentials;

- Rate differentials compound over time, not corrected by later action;

- Lock-in provisions (withdrawal limits, market value adjustments) make annuity damages even more severe than share-class damages.

Accordingly, Disselkamp provides a template for quantifying damages in annuity cases by comparing actual credited rates to hypothetical prudent alternatives.

II. Coppel v. SeaWorld Parks & Entertainment, Inc. (D. Md.) — the SeaWorld Order

Statement of the Rule (Stable Value/Annuity Pricing):

The United States District Court for the District of Maryland denied a motion to dismiss ERISA claims challenging the inclusion and retention of certain stable value and annuity-like products in SeaWorld’s plan. The court held that:

“Plaintiffs have alleged sufficient facts to support plausible claims that Defendants breached their fiduciary duties by selecting and retaining products with inferior pricing and structural constraints when superior alternatives were available.” — SeaWorld Order, cited in Coppel v. SeaWorld Parks & Entertainment (denying motion to dismiss).

The SeaWorld Order rejected arguments that:

- Claims were mere performance disputes;

- Disclosure or custom immunized fiduciary conduct;

- Plaintiffs needed precise benchmarking at the pleading stage.

Instead, the court analogized low crediting rates and restrictive features to imprudent pricing decisions.

Relevance to Annuities:

The court’s reasoning confirms that ERISA fiduciary claims can proceed where:

- A product offers inferior economic terms (e.g., low crediting rates);

- Prudent available alternatives with superior economic terms existed;

- The fiduciary process was inadequate; and

- Retention itself can constitute a continuing breach.

This mirrors Disselkamp’s analysis and expands it to non-mutual-fund products, including stable value and annuity products.

III. Integrated Legal Implications for Annuities

A. Pricing Decisions Are Fiduciary Decisions

Both Disselkamp and SeaWorld confirm that selecting an investment with inferior pricing — regardless of labels or industry practice — is a fiduciary decision that must be evaluated under ERISA §404:

- Disselkamp: Higher cost share classes → fiduciary breach.

- SeaWorld: Low crediting rates and restrictive product design → plausible fiduciary breach.

For annuities, the key pricing metric is the crediting rate, not net performance.

B. Damages Are Measureable from the Point of Selection

The court in Disselkamp recognized that damages arise from the pricing decision itself, not from subsequent market movements. This endorses a compounding model where:

Damages = (Comparator rate − Actual credited rate) × Account balance × Time, compounded.

SeaWorld confirms that priced differences alone can anchor plausible claims, making it easier to allege damages at the pleading stage.

C. Disclosure and Custom Do Not Immunize Imprudent Pricing

SeaWorld specifically rejected the notion that broad industry practice or disclosure cures fiduciary breaches:

Exposure to risk and inferior pricing “cannot be justified solely by disclosure or industry acceptance.” — SeaWorld Order (quotation paraphrased).

This supports your point that DOL exemptions do not work simply because insurers disclose spread mechanics or participants sign forms.

D. Prohibited Transaction Implications

Once a pricing decision is shown to be a fiduciary breach under §404 logic, it also supports a strong §406 prohibited transaction claim:

- The insurer is a party in interest;

- The retained spread is compensation;

- A low crediting rate relative to available alternatives demonstrates unreasonable compensation;

- Compounding losses illustrate continuing harm.

After Cunningham v. Cornell, defendants must prove exemption applicability. Disselkamp and SeaWorld provide legal support for the proposition that pricing decisions with structural pricing differentials are not cured by disclosure alone.

IV. Conclusion

Disselkamp and SeaWorld provide two complementary legal frameworks:

- Disselkamp offers a damages model and analogical reasoning for pricing decisions as fiduciary breaches.

- SeaWorld confirms that similar theories are viable for non-mutual-fund products like fixed annuities and stable value funds.

Together, they reinforce the proposition that:

- Low crediting rates in annuities are actionable under ERISA fiduciary standards;

- Pricing differentials can be quantified as ongoing, compounding harms;

- Disclosure or industry practice does not insulate fiduciaries from liability; and

- Prohibited transaction theory is bolstered when pricing decisions confer unreasonable compensation on parties in interest.

This legal support strengthens both liability and damages allegations in annuity litigation arising from the structures discussed in Annuities Are a Prohibited Transaction — DOL Exemptions Do Not Work.

This Appendix to Great Grey CIT stable value fund discloses major issues with the underlying Empower General Account Fixed Annuity . https://greatgray.com/wp-content/uploads/2025/05/0.08-Stable-Value-Funds-2024-Final.pdf It also states the credited rate process is “discretionary and proprietary.” This is a direct admission that the plan’s return is not the transparent output of a portfolio—it’s the output of an insurer’s internal pricing decision, i.e., classic general-account spread mechanics.

Appendix 3: Why Prudent Sponsors Will Never Offer Annuities and Why All Annuities Should Be Treated as Prohibited Transactions

A recent analysis by James W. Watkins, III (J.D., CFP Emeritus®) further reinforces the central themes of this blog — that annuities, whether marketed as lifetime income solutions or stable investment options in 401(k) plans, raise fundamental fiduciary, ethical, and legal problems for plan sponsors and participants alike. While this blog has focused on ERISA fiduciary violations and CFA ethical standards, Watkins’s 3×3 analysis adds another dimension: the economic, risk, and transparency failures inherent in annuity products that make them unsuitable — and arguably impossible to prudently offer — within qualified retirement plans. The Prudent Investment Fiduciary Rules https://fiduciaryinvestsense.com/2026/01/04/upon-further-review-the-3-x-3-analysis-that-shows-why-prudent-plan-sponsors-will-never-offer-annuities-within-their-plan/

1. Plan Sponsors Have No Legal Duty to Offer Annuities — Only Legal Risks

Watkins points out that neither ERISA nor any other law requires plan sponsors to offer annuities within defined contribution plans. Unlike traditional investment options such as mutual funds, annuity inclusion is purely elective, with no statutory directive for fiduciaries to provide them as a “choice” for participants. Thus, any decision to include annuity products is voluntary and must be justified under ERISA’s stringent fiduciary standards of prudence and loyalty — a burden few if any annuity products can satisfy. The Prudent Investment Fiduciary Rules

2. Plain Arithmetic Shows Annuities Favor Issuers, Not Participants

A core feature of Watkins’s analysis is that even simple breakeven calculations — factoring in interest crediting rates, mortality assumptions, and present value — generally show that the odds of a typical participant breaking even on an annuity are low. Where the expected value of payouts is less than the underlying contract value for most participants, annuities shift economic risk to participants while concentrating profits with issuers. This economic asymmetry is a stark conflict with ERISA’s requirement that fiduciary decisions “must be made solely in the interest of plan participants and beneficiaries” — not in the financial interest of an annuity provider. The Prudent Investment Fiduciary Rules

3. Lack of Transparency and Comparative Analysis Makes Prudence Impossible

Watkins underscores a problem this blog has highlighted repeatedly: annuities lack the transparency and standard disclosures necessary for a prudent fiduciary evaluation. Unlike mutual funds or exchange-traded products subject to SEC registration and mandated disclosures, annuity contracts do not present investors with reliable, comparable data on fees, crediting methodologies, embedded compensation, or counterparty credit risk. This opacity precludes a plan fiduciary from performing the “complete and accurate information” analysis required by ERISA §404(a)(1)(B). The Prudent Investment Fiduciary Rules

4. Annuities Concentrate Risk Contrary to ERISA’s Diversification Standard

By concentrating participant assets in a single insurer’s general account, annuities expose plans to single-entity credit risk, illiquidity, and counterparty failure risk — all antithetical to diversification principles under ERISA §404(a)(1)(C). This concentration risk is compounded by the fact that annuity crediting rates and the insurer’s asset mix are often opaque to fiduciaries. This structural risk profile contrasts sharply with diversified mutual funds that spread exposure across many securities and are transparently priced. The CommonSense 401k Project

5. Watkins’s Analysis Supports a Prohibited Transaction Framework

When placed alongside Supreme Court and DOL logic on prohibited transactions — particularly after Cunningham v. Cornell — Watkins’s points strengthen the argument that annuities functionally fail the standards that might otherwise justify a prohibited transaction exemption. Annuities typically involve:

- Parties in interest: The insurer, often a recordkeeper affiliate or plan service provider, is economically tied to the plan or consultant.

- Indirect compensation: Issuers and intermediaries benefit from spreads, crediting margins, and embedded fees not disclosed as plan expenses.

- Lack of neutrality: The structure embeds conflicts of interest that tilt economics toward the provider rather than the plan.

Taken together, they satisfy the text and spirit of §406(a) — where a fiduciary or party in interest receives a benefit from plan assets that ERISA intended to prohibit. Because annuity products rarely meet neutral-pricing, arm’s length standards, their inclusion in plans should be treated as a prohibited transaction unless a clear exemption applies. The CommonSense 401k Project

Conclusion: Watkins Reinforces the Prohibited Transaction Thesis

The Watkins 3×3 analysis does more than critique annuity suitability; it highlights the economic mechanics and fiduciary risks that make annuities incompatible with ERISA’s core duties. Combined with the CFA-standards analysis and the legal framework discussed in this blog, the evidence now suggests that all annuities offered inside 401(k) and 403(b) plans merit scrutiny not just as poor investment choices, but as prohibited transactions that create unrecoverable economic harm and conflict with statutory fiduciary obligations.

This reinforces the need for:

- Plan fiduciaries to avoid annuity products absent extraordinary justification.

- Regulators and courts to treat annuity inclusion as inherently conflicted under ERISA.

- Plaintiffs and practitioners to bring claims that reflect these structural economic realities.