Last updated 3/9/26

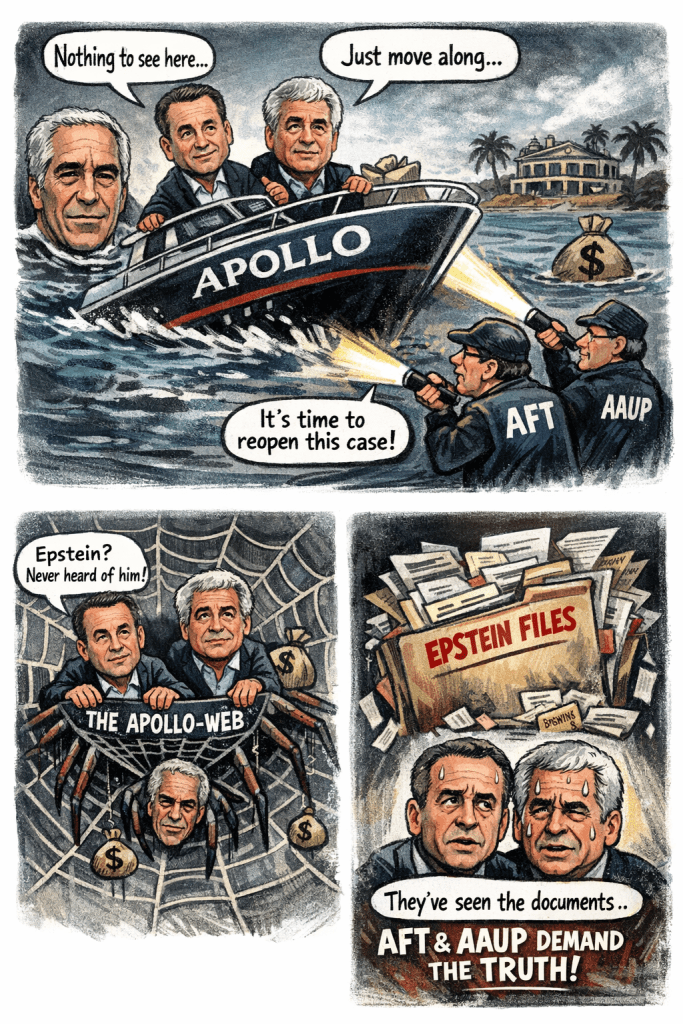

In 2019, when Jeffrey Epstein was arrested, and the first public scrutiny fell on Leon Black — co-founder of private capital giant Apollo Global Management — many public pension funds faced a simple choice: do we continue investing with a firm deeply connected, even if indirectly, to a convicted sex offender? Almost all chose not to divest. Funds asked questions. One major plan paused new commitments. But nearly all maintained existing exposures. At the time, the narrative trustees were given — both publicly and privately — was this: by CEO Marc Rowan

Leon Black’s relationship with Epstein was personal, isolated, and unrelated to Apollo’s business. Apollo itself had never done business with Epstein. This lie was exposed first in the Financial Times article https://www.ft.com/content/092d9e44-ec17-4da7-8b58-e43bf09113ab and then in Bloomberg https://www.bloomberg.com/news/features/2026-02-13/the-leon-black-files-epstein-was-a-fixer-for-billionaire-s-deepest-secrets?, additional color on Rowan on political fallout at https://www.thekomisarscoop.com/2026/02/the-board-of-peace-already-has-a-corruption-problem/ The AFT and AAUP’s letter to the SEC further highlights this deception. https://www.aft.org/press-release/aft-aaup-demand-sec-probe-over-apollo-execs-epstein-contacts Major pensions CalSTRS and Connecticut have started questioning Apollo over Jeffrey Epstein ties, as reported in Pensions & Investments on 2/24/26. https://www.pionline.com/asset-management/pi-apollo-jeffery-epstein-calpers-calstrs-marc-rowan-leon-black/ A securities lawsuit was filed 3/2/26 about Apollo, Marc Rowan, and Leon Black lying on the extent of their involvement with Jeffrey Epstein https://www.reuters.com/sustainability/boards-policy-regulation/apollo-leon-black-sued-allegedly-concealing-epstein-business-ties-shareholders-2026-03-03/ Another lawsuit dropped on 3/2/26 claims that Leon Black and Jeffrey Epstein colluded to attack accusers https://nypost.com/2026/03/02/us-news/leon-black-colluded-with-jeffery-epstein-to-attack-accusers/

That representation, backed by a commissioned Dechert LLP review released in 2021, https://www.apollo.com/insights-news/pressreleases/2021/01/apollo-global-management-announces-conclusion-and-release-of-independent-review-211549270 was enough to calm many boardrooms. But the public record today — rich with subsequent reporting, legal filings, government investigations, and newly released DOJ emails — shows that premise was deeply flawed, if not false.

What Naked Capitalism and Other Sources Showed Back in 2019–2023

In July 2023, finance observers at Naked Capitalism laid out what was already obvious from the early media coverage of the Black–Epstein ties:

Leon Black had paid Epstein eye-popping sums — tens of millions of dollars annually — for “tax advice” despite Epstein having no recognized tax credentials, and there was legitimate skepticism about whether that amounted to anything more than paying for influence or access. The Senate Finance Committee was openly probing the arrangement as emblematic of how super-wealthy elites use opaque tax structures to avoid taxes altogether.

The commentariat also noted that many pensions did not act even when the story broke — that file shows PSERS froze new commitments and other investors expressed concerns, but most limited partners simply let the issue fade. Reuters wrote how Leon Black downplayed his relationship with Epstein and denied no Apollo connections https://www.reuters.com/business/finance/apollo-seeks-tame-investor-concerns-over-ceos-ties-epstein-2020-10-21/https://www.reuters.com/world/asia-pacific/apollo-ceo-black-says-he-regrets-ties-epstein-denies-any-wrongdoing-2020-10-13/

Naked Capitalism was blunt: paying $158 million to someone unlicensed for tax or estate planning — and doing so without a formal fee agreement — was not only “unseemly” but abnormal even by private-markets standards.

What the Government and Press Have Disclosed in early 2026

Appendix: The “No Relationship” Defense Is Structurally Implausible

Marc Rowan’s spokesperson now asserts that neither Rowan nor anyone else at Apollo (excluding Leon Black) had a business or personal relationship with Jeffrey Epstein. That defense hinges on a narrow semantic distinction — as if sporadic communications, returned calls, arranged meetings, and interactions involving Apollo personnel somehow do not constitute a “relationship.” But governance does not turn on wordplay. If Epstein was fielding calls from Rowan, arranging in-person meetings, communicating with Apollo colleagues, and inserting himself into matters touching corporate staff and financial structures, then the claim of “no relationship” becomes structurally implausible. At minimum, it reflects contact and operational interface during a period when Epstein was simultaneously serving as Black’s fixer across financial, reputational, and legal risk domains. For public pension fiduciaries evaluating counterparty governance, the relevant question is not whether Rowan socialized with Epstein. It is whether senior leadership had interactions with, access to, or reliance upon an individual later revealed to be deeply embedded in sensitive matters involving the firm’s co-founder. If the answer is yes — even episodically — then the categorical “no relationship” defense collapses under its own weight.

The Financial Times’ 2026 Emails Dump

In early 2026, a tranche of Department of Justice emails released as part of the Epstein files showed that Apollo’s leadership may have mischaracterized key facts:

- Epstein was not just a personal advisor to Leon Black — he was given internal financial documents from Apollo executives, including current CEO Marc Rowan, and was involved in discussions over firm tax arrangements.

- Epstein requested and reviewed sensitive tax receivable agreement figures and potential tax strategies for Apollo’s internal transactions, contradicting earlier Apollo statements that no business was conducted with Epstein.

- Emails indicate that not just Black, but Rowan and co-founder Josh Harris, were earmarked as needing to sign off on Epstein-connected plans — placing them squarely inside matters previously described as personal affairs.

That’s a seismic shift: the firm’s public defense was personal dealings only; the record now shows Epstein engaged in substantive discussions over corporate and tax strategy involving multiple senior executives. https://www.ft.com/content/092d9e44-ec17-4da7-8b58-e43bf09113ab

The following contacts, contained in the letter, are just a small portion of the hundreds of documents in the Epstein files that refer to Marc Rowan, Leon Black and Apollo. Epstein was first convicted of sex crimes in June 2008. From https://www.aft.org/press-release/aft-aaup-demand-sec-probe-over-apollo-execs-epstein-contacts

- Rowan and Epstein apparently met for the first time on Sept. 3, 2013, at Apollo’s offices.

- Rowan and Epstein met on the morning of Sept. 8, 2013.

- Rowan and Black had breakfast with Epstein on Oct. 22, 2013.

- Black instructed Rowan to call Epstein regarding “donor advised funds” in January 2014.

- Rowan met Epstein for breakfast on Jan. 6, 2016.

- Rowan met with Epstein at his New York City mansion on Jan. 14, 2016. It is likely at this meeting they discussed what Epstein described as involving “Athene, Montauk Rothschild. Planes boats etc.”

- Epstein inquired about the costs and specifications of a plane that Rowan was selling in January 2016.

- In February 2016, Rowan and Epstein discussed working with Edmond de Rothschild to finance an Apollo inversion. Epstein appears to have been the conduit for the introduction to the bank.

- Rowan appears to have sought Epstein’s advice on Apollo calculations for a tax receivable agreement on March 4, 2016.

- Epstein introduced Nicholas Ribis, an executive with Trump’s resort empire, to Rowan in March 2016. Ribis appears to have tried to get himself appointed as examiner in the bankruptcy of Caesars Entertainment Inc.

- In September 2016, Apollo’s Brad Wechsler asked Apollo staff to keep Epstein cc’d on materials related to tax matters for family offices of the three Apollo founders, including Rowan, for his “substantive expertise.”

The February 17, 2026 letter to the SEC from the American Federation of Teachers and the American Association of University Professors dramatically undercuts the premise on which many public pensions declined to divest in 2019. www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf The letter details newly released Justice Department documents showing that Marc Rowan and Joshua Harris met repeatedly with Jeffrey Epstein between 2013 and 2016, discussed matters involving Athene and potential Apollo transactions, sought Epstein’s advice on tax receivable agreements, and even involved him in introductions related to financing and bankruptcy proceedings

These disclosures stand in direct tension with Apollo’s January 25, 2021 Form 8-K https://www.sec.gov/Archives/edgar/data/1411494/000119312521016405/d118102d8k.htm and accompanying Dechert report, which asserted that Leon Black “never promoted Mr. Epstein’s services to other Apollo senior executives” and that neither Harris nor Rowan hired or consulted Epstein on personal matters. The AFT letter states plainly that the DOJ files suggest those statements were “misleading” and that investor communications currently give an “inaccurate and incomplete picture” of Apollo’s ties to Epstein . For public pension fiduciaries, this is no longer merely a reputational issue—it is a disclosure integrity issue. If the representations that underpinned the 2019 decision not to divest are now credibly challenged by federal document releases, trustees have a renewed duty to re-examine whether continued exposure to Apollo satisfies their obligations of prudence, candor, and risk oversight. The Financial Times published a paywall piece on the AFT letter on 2/17/26 https://www.ft.com/content/9f96ca88-2cee-4ca1-a076-58cf3440ac55

The “No Relationship” Defense Collapses Under Documentary Evidence

In 2019, public pension trustees were assured that Jeffrey Epstein’s relationship was personal to Leon Black, contained, historical, and irrelevant to Apollo’s institutional governance. Marc Rowan and Apollo representatives emphasized that no broader operational or business integration existed. That narrative is now irreconcilable with the documentary record.

The newly released Justice Department files, detailed in Bloomberg’s February 13, 2026 investigation, show Epstein operating not as a passive estate planner but as a “stealthy do-it-all fixer” deeply embedded in financial structuring, asset leverage, tax positioning, corporate entities, and sensitive personal matters involving Apollo’s co-founder

Why This Matters to Public Pensions

Joshua Harris one of the 3 original Apollo founders with Leon Black and Marc Rowan was asked this question at a Philadelphia Pension meeting. She asked Mr. Harris if Apollo had a lot of public pension plan investors. He said that, almost all of the capital received by Apollo was from Public Funds; he estimated approximately 75% to 80% of Apollo’s capital was from Public Pension Plans. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

1. Pension Boards Relied on a False Premise

In 2019–2021, trustees were told:

- Apollo had no corporate relationship with Epstein

- Black’s payments were personal and non-business-related

- Nothing in Apollo’s governance or operations was implicated

- That representation was material to trustees’ fiduciary judgments — especially for those whose due diligence pointed to reputational risk, governance risk, and long-term fund performance.

Today’s evidence suggests that the premise trustees used to decline divestment was incorrect.

That’s not just a reputational wrinkle — it’s a fiduciary risk oversight failure.

2. The Naked Capitalism Frame Was Right About the Real Question

Back in 2019, commentators questioned the real value of Epstein’s services and whether the arrangement was something other than benign advice. Naked Capitalism suggested: Paying someone like Epstein $158 million, without a professional fee agreement or credentials, was implausible outside of influence, access, or other undisclosed benefits — especially when vetted tax professionals could have done similar work for a fraction of that fee. That same skepticism now resonates with the newer evidence showing Apollo executives shared sensitive tax-related information with Epstein — something that goes well beyond “advice.” https://www.nakedcapitalism.com/2023/07/former-apollo-chief-leon-black-has-more-jeffrey-epstein-splaining-to-do-with-tax-evasion-alleged-rape-of-autistic-16-year-old.html

The Broader Governance Pattern Pensions Should Recognize

This episode fits a much larger pattern — one these same pensions have repeatedly confronted in private markets: When you ask managers for transparency on governance concerns, the first answer is usually a controlled narrative.

Only later, often under external pressure or legal document release, does a more complex, less flattering story emerge. This is the same dynamic you’ve documented in retirement investment analytics — where private-market disclosures are often opaque until forced into daylight.

The Fiduciary Question Trustees Must Now Ask

Not: Should we feel bad about Apollo’s historic transgressions? But: Did we make our 2019 divestment decision based on facts that were materially incorrect? If so, should we revisit that decision now?

And if Apollo’s prior disclosures were materially inaccurate:Did trustees receive updates that corrected the record at the time? Did pensions perform iterative due diligence as new facts emerged? Did funds that continued to invest explain how they evaluated the governance impact? Should pension committees reopen investment decisions in light of new evidence?

These are not political questions. They are fiduciary ones.

What Pension Fiduciaries Should Do Now

In light of the newly revealed evidence and other reporting:

1. Request Apollo to explain, in writing, the extent of Epstein’s involvement in firm matters now shown after 2019 facts. Trustees should demand transparent, verifiable responses from Apollo on: What documents were shared with Epstein . Who in Apollo communicated with Epstein . What strategic matters Epstein was consulted about. Whether Apollo’s prior statements to investors continue to be accurate 2. Re-evaluate all Apollo commitments against fiduciary standards This should include: Governance risk assessments, Reputational risk analyses, Operational due diligence, Cost/benefit of continuing exposure vs. risk mitigation 3. Consider divestment, or exit strategies where appropriate Funds that maintain significant exposure should periodically reassess whether continued involvement aligns with prudent investor standards — especially when the manager’s transparency has been called into question.

Conclusion: This Is Not Ancient History

What happened with Apollo in 2019 was not settled history. Too many trustees accepted an incomplete — and now demonstrably inaccurate — narrative. The Naked Capitalism critique back then was more than snark; it was fundamentally right about the depth and implications of the relationships at play. Pensions can no longer rely on the original premise they were given. It’s time to ask: Should we continue to invest with a manager whose senior leadership repeatedly mischaracterized material governance facts to public investors? That is the commonsense fiduciary question of 2026.

Sources-

https://www.truehoop.com/p/when-josh-harris-and-jeffrey-epstein https://www.thedp.com/article/2026/02/penn-marc-rowan-jeffrey-epstein-files-emails https://www.haaretz.com/us-news/2026-02-04/ty-article/.premium/pro-trump-billionaire-on-gaza-board-of-peace-linked-to-jeffrey-epstein-in-new-doj-files/0000019c-2887-db08-abdd-6b8ffaff0000 https://www.inquirer.com/news/marc-rowan-plane-epstein-penn-20260130.html

United States public pensions (confirmed in public sources)

Connecticut $111mm Apollo Fund VIII chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://portal.ct.gov/-/media/ott/pdfs/2018cifcafr.pdf

Rhode Island invests $100s of millions in Apollo Investment fund VIII, IX Apollo Hybrid Value Funds

Massachusetts PRIM / PRIT Fund ACFR lists “Apollo Management (New York, NY)” in its manager listing.

New Hampshire Retirement System public investment materials include “Apollo Global Management, Inc.” in the manager list.

(Separately, industry coverage reports NHRS approved a commitment to an Apollo fund.)

New York City Teachers’ Retirement System (TRS of the City of New York) — Reuters reported NYC pension commitments to Apollo and mentions TRS NYC’s specific commitments to Apollo funds. PE Hub

New York State Aug 2013: Apollo Investment Fund VIII, L.P. — $400 million commitment (NYSCRF report).

(Report dated 2015-08): Apollo Natural Resources II, L.P. — $400 million commitment (NYSCRF report).

Dec 2021: Apollo Impact Mission Fund — $150 million commitment (Monthly Transaction Report; also states Apollo is an “existing relationship” and notes “no placement agents”).

Dec 2022: Apollo Investment Fund X, L.P. — $350 million commitment (Monthly Transaction Report).

Mar 2023: Apollo Excelsior PE Co-Invest, L.P. — $350 million commitment (Monthly Transaction Report).

Pennsylvania PSERS (Public School Employees’ Retirement System of PA) — PSERS board resolution for Apollo Investment Fund IX notes prior PSERS commitments to multiple Apollo partnerships and states PSERS had committed $620m to Apollo-managed partnerships since 2012 (as of that 2017 resolution).

Pennsylvania SERS maintained exposure to flagship buyout funds during Apollo Fund VI–VIII cycles.

California CalPERS (CA Public Employees’ Retirement System) — identified in SEC filings as one of Apollo’s “Strategic Investors.” Huge Holdings in billions

California CalSTRS (CA State Teachers’ Retirement System) — CalSTRS’ own Private Equity Portfolio Performance table lists multiple Apollo vehicles (e.g., Apollo Investment Fund IX; Apollo Hybrid Value Fund II; Apollo Investment Fund X) with commitments shown.

Los Angeles City Employees’ Retirement System (LACERS) — LACERS performance update document references Apollo Investment Fund VI (example of an Apollo commitment appearing in a LACERS consultant report).

Oregon PERS invests $millions in invests $100s of millions in Apollo Investment fund VI, VII, VIII, IX Private Equity

Washington State Investment Board Apollos S3 Equity & Hybrid Solutions Fund https://www.dakota.com/resources/blog/consultant-led-private-equity-allocations-from-q4-2025?utm_source=chatgpt.com

New Mexico SIC → Apollo credit fund: $100M 2007 NMERB PE: Apollo Investment Fund VII (2008), $40M. Apollo Investment Fund VIII (2013, $50M.

Idaho (PERSI – Public Employee Retirement System of Idaho)

PERSI’s private-equity performance/holdings reports explicitly list multiple Apollo funds (e.g., Apollo Investment Fund IX and others).

Montana (Montana Board of Investments)

Montana BOI’s published holdings include “APOLLO ASSET MANAGEMENT INC” as a listed holding (public equities holdings file).

South Dakota (South Dakota Retirement System / SD Investment Council)

SDRS CAFR includes “Apollo” in the roster of investment managers under the State of South Dakota Investment Council.

Colorado (Colorado PERA)

Colorado PERA’s “Private Equity Holdings” list includes multiple Apollo funds (e.g., Apollo Investment Fund III/IV/V/VI/VII and Apollo Distressed Investment Fund (DIF)).

Arizona (PSPRS – Public Safety Personnel Retirement System of Arizona)

PSPRS ACFR shows Apollo exposures in alternatives, including entries like “APOLLO INVESTMENT FUND VII” and “PSPRS-APOLLO EUR NPL.”

San Francisco (SFERS)

The AFT/PitchBook compilation table shows San Francisco Employees’ Retirement System with an Apollo column entry (commitment exposure summary).

(SFERS’ own PE update memo also references “Apollo” in the context of a “public PE basket,” though that’s not the same as confirming a direct Apollo mandate.)

San Diego (San Diego City Employees’ Retirement System)

The same AFT/PitchBook table lists San Diego City Employees’ Retirement System with an Apollo column entry (commitment exposure summary).

Florida State Board of Administration (Florida SBA) — Florida SBA performance report lists multiple Apollo private equity funds (e.g., Apollo Investment Fund IV, V) with commitment amounts; separate reporting also describes commitments to Apollo credit funds. Apollo Accord Fund V and VI LP

Virginia Retirement System (VRS) — reported commitments to Apollo vehicles (e.g., $50m in 2020 and $250m commitment reported in 2022).

Teachers’ Retirement System of Texas (TRS Texas) — reported as a major investor/LP in Apollo funds (e.g., Reuters/industry coverage of Apollo funds; PERE notes TRS Texas as a major investor in Apollo Investment Fund VIII).

Teachers’ Retirement System of Louisiana (TRSL) — reported commitments to Apollo strategies (e.g., Apollo Natural Resources fund commitments, plus later credit commitments).

South Carolina Apollo reference 2011 PE INT.

Mississippi has held Apollo VIII IX Private Equity funds

North Carolina (state retirement system / treasurer investment reporting)

North Carolina’s FY2009 Annual Investment Report lists Apollo private equity vehicles in its private equity holdings, including “Apollo Investment Fund VI” and “Apollo Investment Fund VII.”

Kentucky (Teachers’ Retirement System of the State of Kentucky) A TRS-KY Quarterly Investment Update shows holdings that include “APOLLO COMMERCIAL REAL ESTAT” and “APOLLO GLOBAL MANAGEMENT INC” (multiple line items).

Ohio State Teachers Retirement (STRS) $600mm in Apollo Private Equity Partnerships Apollo S3 Equity and Hybrid Solutions Fund I Apollo Global Management (APO)

OPERS: Holds Apollo Global Management (APO) equity

(.

Ohio SERS: Apollo Global Management , “Core Farmland Fund, LP

—

Ohio Highway Patrol SHPRS: “Apollo Investment Fund” appears as a line item in ORSC report snippets (with dollar amounts shown

TRS Illinois makes $200mm to Apollo Investment Fund X Oct.22 PE Int

Connecticut $111mm Apollo Fund VIII chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://portal.ct.gov/-/media/ott/pdfs/2018cifcafr.pdf

Iowa hiring of Apollo Strategic Origination Partners (Dakota.com), Apollos Insurance Company, and Athene is domiciled in Iowa

Indiana Added $180mm 2024 https://www.dakota.com/fundraising-news/indiana-prs-invest-180m-to-private-equity-private-credit-hire-international-equity-manager https://www.alternativeswatch.com/2022/05/19/indiana-public-employees-retirement-system-inprs-alternative-investments/ Apollo $150mm Origination Partnership Private Credit

Kansas Public Employees Retirement Systems has $100s of millions in Apollo Investment fund VIII, IX

Michigan invests $100s of millions in Apollo Investment fund VIII, IX Apollo Hybrid Value Funds, Apollo Credit/ Opportunistic Credit

U. of Michigan $30mm Apollos Structured Credit Recovery of Investments.

Nebraska Investment Council refers to Apollo as a Council Manager Partner via the India Property Fund II LLC.

Wisconsin (SWIB) — credible press/database mentions, not a clean public SWIB PDF hit I found industry-investment reporting stating Wisconsin’s SWIB has committed to Apollo-managed funds (example: an Apollo credit fund).

Minnesota SBI – March 21, 2025 SBI meeting packet contains a reference to “Apollo/Athene Dedicated Investment Program II,

Canada (confirmed)

- CPP Investments (Canada Pension Plan Investment Board / CPPIB) — CPPIB’s own press release states it made a US$150m commitment to an Apollo private equity fund (older but directly documented).

- Ontario Teachers’ Pension Plan (OTPP) — documented deal with Apollo-affiliated funds (CareerBuilder acquisition) showing direct co-investment/transaction participation alongside Apollo funds.

UK public pensions (confirmed)

- London Pensions Fund Authority (LPFA) — industry pension press reports LPFA selecting Apollo (manager selection / mandate).

- Cumbria Local Government Pension Scheme (LGPS) — a published LGPS alternatives holdings spreadsheet includes an “APOLLO MULTI-CREDIT FUND” line item.

Singapore fund. Australian Super Funds – Hostplus, Care Super, Catholic Super, Equip Super

Public Pensions Have Known About Apollo’s Governance Problems for Over a Decade, and Epstein’s ties for 7 Years

As early as 2015, Apollo’s name was entangled in one of the most notorious public pension corruption scandals in the country — the CalPERS pay-to-play case. Former CalPERS CEO Fred Buenrostro was sentenced to prison after pleading guilty to bribery charges connected to placement agent Alfred Villalobos. Villalobos, a former CalPERS board member turned placement agent who helped private equity firms win business, committed suicide before serving his sentence. The scandal exposed how politically connected intermediaries steered pension capital to private equity managers, including Apollo. Despite the corruption scandal, Apollo continued to receive pension allocations. (See: Los Angeles Times coverage of Villalobos’ death and the broader CalPERS scandal.) https://www.latimes.com/business/la-fi-villalobos-suicide-20150115-story.html

In 2016, the Securities and Exchange Commission fined Apollo Global Management $52.7 million for failing to adequately disclose accelerated monitoring fees and other conflicts of interest to investors. The SEC found that Apollo misled fund investors regarding fee practices. The penalty was widely reported as one of the largest of its kind at the time. https://www.sec.gov/newsroom/press-releases/2016-165

During Indiana’s 2016 Senate race, the National Republican Senatorial Committee ran attack ads referencing that fine, “Hoosier teachers, police and firefighters trusted Bayh’s firm (Apollo). But while he made millions, his firm misled retirees and received the largest fine in SEC history,” https://www.nrsc.org/press-releases/confirmed-evan-bayhs-firm-defrauded-hoosier-retirees-2016-10-13/ Since then Indiana Republican Governors have continued to invest pension assets with Apollo.

Then came 2019 and the renewed scrutiny of Leon Black’s payments to Jeffrey Epstein. In 2021, Apollo disclosed through SEC filings and a Dechert investigation report that Black had paid Epstein approximately $158 million for “legitimate professional services.” The Dechert letter stated Apollo itself “did no business with Mr. Epstein” and that no other Apollo employee engaged Epstein’s services. https://www.sec.gov/Archives/edgar/data/1411494/000119312521016405/d118102d8k.htm SEC Dechert Letter

But in 2026, the AFT and AAUP formally urged the SEC to investigate Apollo’s 2021 disclosures, citing newly released Epstein files and alleging that investor communications may present an “inaccurate and incomplete picture.” That escalation signals that pension stakeholders believe the 2021 explanations may not fully resolve disclosure concerns. https://www.aft.org/press-release/aft-aaup-demand-sec-probe-over-apollo-execs-epstein-contacts

Regulatory issues have continued. In 2025, the SEC ordered Apollo to pay $8.5 million for recordkeeping violations, further reinforcing that disclosure and compliance lapses are not isolated historical artifacts but recurring governance concerns.

In 2022 Apollo hired outgoing Connecticut Treasurer Shawn Wooden to get more public business https://www.ai-cio.com/news/former-connecticut-treasurer-named-chief-public-pension-strategist-at-apollo-global-management/

Donald Huffines is running for Texas Comptroller which sits on the board of the $60 billion Texas Permanent School Funds which holds $millions with Leon Black’s Apollo.https://tx.localnews.com/texas-permanent-school-fund-corp-raises-position-in-apollo-commercial-real-estate-finance/ Huffines secretly bought the Epstein Zorro Ranch.

Apollo, via its debt control of Gannett, controls the main state media in many of the markets, especially state capitols of the above Public Pension Plans, like the Columbus Dispatch, Cincinnati Enquier and 12 other smaller Ohio papers. Tallahassee Democrat, Jacksonville Times Unon and 15 other Florida papers. Springfield State Journal, Peoria Journal Star, Rockford Register Star, and 10 other Illinois papers. Austin American-Statesman El Paso Times, and 6 other Texas papers. Indianapolis Star, Des Moines Register, Topeka Capital-Journal, Lansing State Journal, Jackson Clarion-Ledger, The Providence Journal

I point out California Media conflicts some Apollo at https://commonsense401kproject.com/2025/11/08/why-private-equity-sees-katie-porter-as-a-strategic-threat-as-california-governor/

UN Human Rights Office looking into Jeffrey Epstein files pointing to a transnational “global criminal enterprise Many US pensions have signed onto the UN Global Compact on Human Rights. Investment firms like Apollo have signed as well and this could increase their risk of divestment https://news.un.org/en/story/2026/02/1166980

https://www.unpri.org/supporters LACERS Vermont Minnesota City of Chicago, ILL Treasurer, State of HI, Seatle SCERS , San Francisco, NYC Teachers, Ontario Teachers, Maryland, CALSTRS, Connecticut, CALPERS (since 27 April 2006)

Apollo Global Management 14 October 2020 https://www.unpri.org/supporters