Wall Street’s biggest sales pitch is simple:

Private Equity and Private Credit reduce risk through diversification.

That claim is not just misleading.

It is built on an accounting distortion that systematically understates risk and overstates diversification benefits.

And now, with the Department of Labor’s blessing, that same flawed model is being pushed into 401(k) Target Date Funds through opaque Collective Investment Trusts (CITs).

The Illusion: Lower Volatility, Lower Correlation, Better Portfolios

Every pension consultant presentation shows the same chart:

- Higher returns

- Lower volatility

- Lower correlation

A “free lunch.”

But that “free lunch” depends entirely on how the assets are valued—not what they actually are.

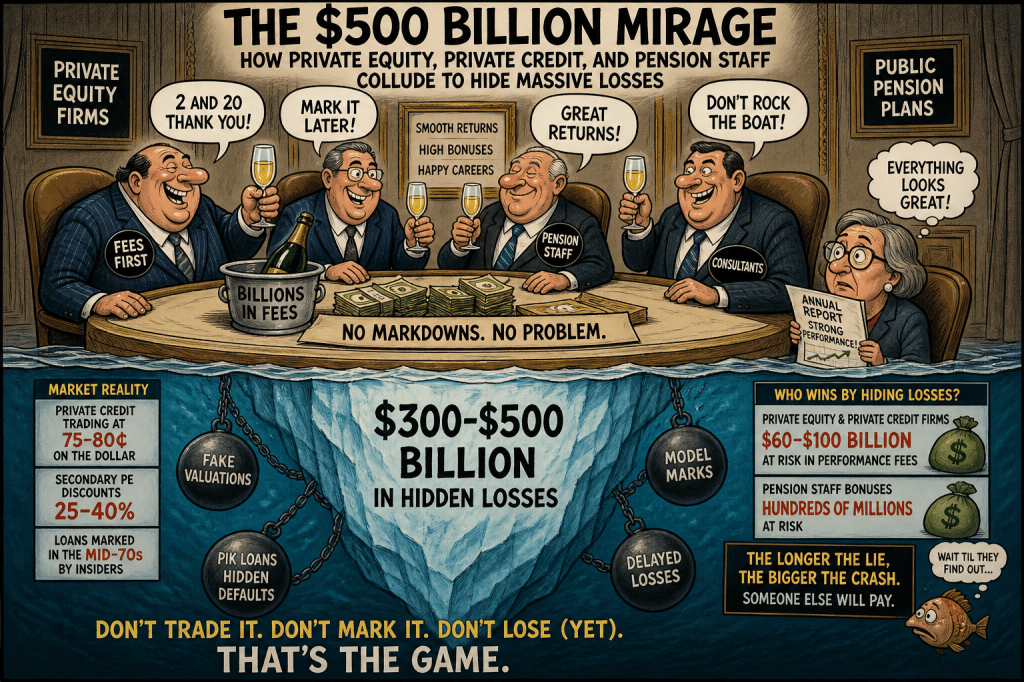

Volatility Is Not Lower — It Is Hidden

Private assets appear stable because they are not priced in real time.

- Public stocks → priced continuously

- Private equity → valued quarterly using models

- Private credit → priced internally

- Real assets → appraised with lag

This creates what academics call “volatility laundering.”

- Returns are artificially smoothed

- Risk is understated

- Drawdowns are delayed

As one analysis notes, smoothing can make volatility look ~10% when the true economic volatility is closer to 30%

Another study shows private equity valuations are updated infrequently and rely on assumptions, creating artificially smooth return patterns

This is not a small technical issue.

It is the foundation of the entire diversification narrative.

Correlation Is Also Fake

Risk models rely on correlation—how assets move relative to each other.

But when returns are smoothed:

- Price movements are delayed

- Volatility is dampened

- Correlation appears artificially low

Academic research confirms:

- Smoothing reduces measured correlation and beta

- Makes private assets appear less tied to public markets

- Overstates diversification benefits

When returns are “unsmoothed,” correlation rises and volatility increases significantly

Even real estate studies show appraisal-based pricing can create near-zero volatility and correlation that simply do not exist economically

The Model Breakdown: Garbage In, Garbage Out

Portfolio construction models—mean-variance optimization, Monte Carlo simulations—depend on:

- Standard deviation (volatility)

- Correlation

If both are artificially low:

👉 The model forces higher allocations to those assets

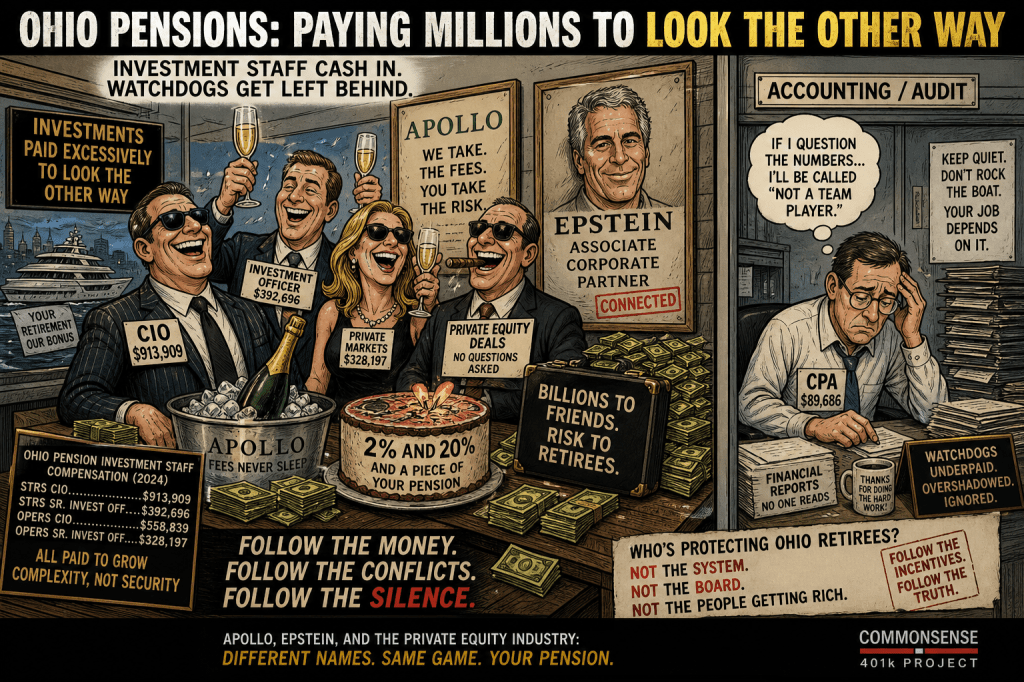

That is exactly what has happened:

- Public pensions now allocate 20%–40%+ to Private Equity and Private Credit

- Risk models “justify” it

- Consultants recommend it

- Staff bonuses depend on it

But the inputs are corrupted.

So the outputs are inevitable:

Systematic overallocation to mispriced, illiquid, opaque assets

This Is Not Diversification — It Is Delay

Private assets don’t avoid volatility.

They delay recognizing it.

Instead of:

- Immediate mark-to-market losses

You get:

- Slow, staged write-downs

- “Stable” performance… until it isn’t

As research shows, smoothing can reduce observed drawdowns from ~40% reality to ~12% reported levels

That is not diversification.

That is accounting deferral of losses.

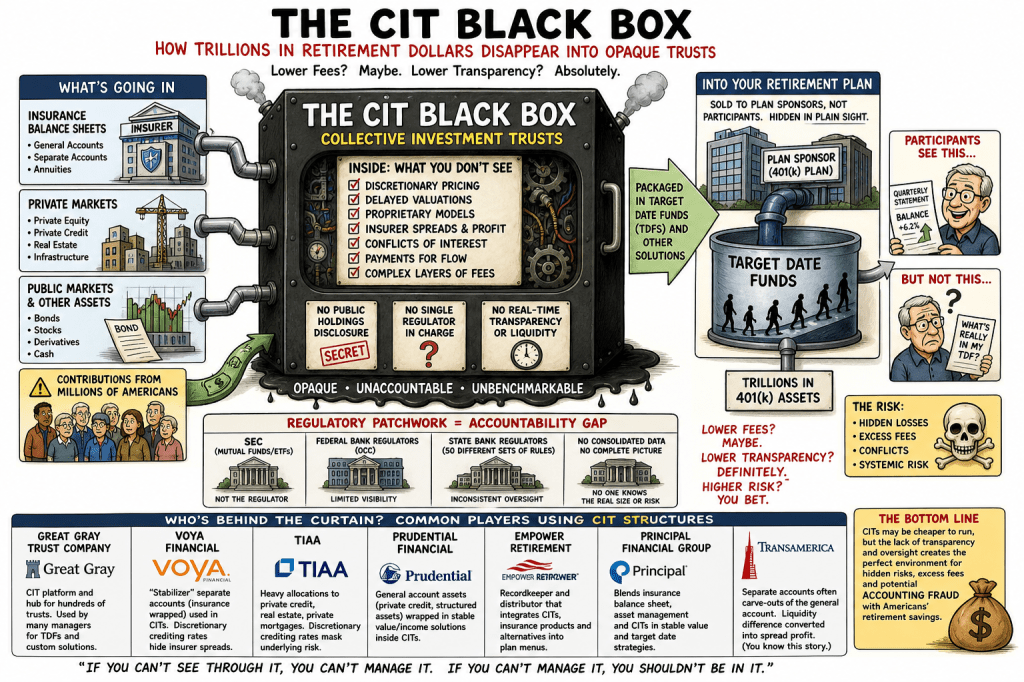

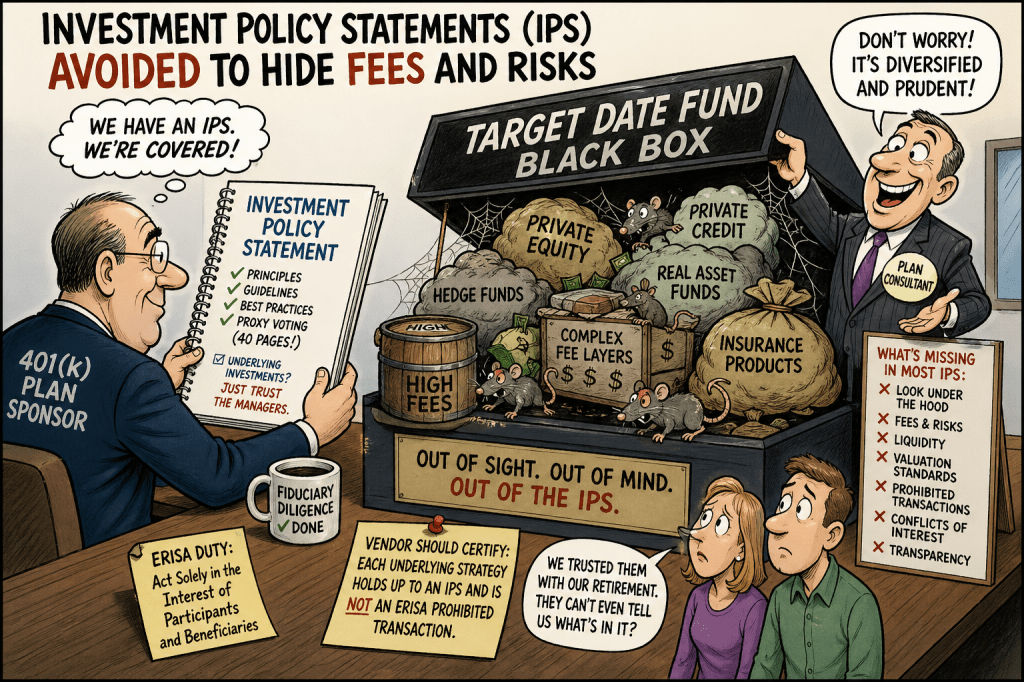

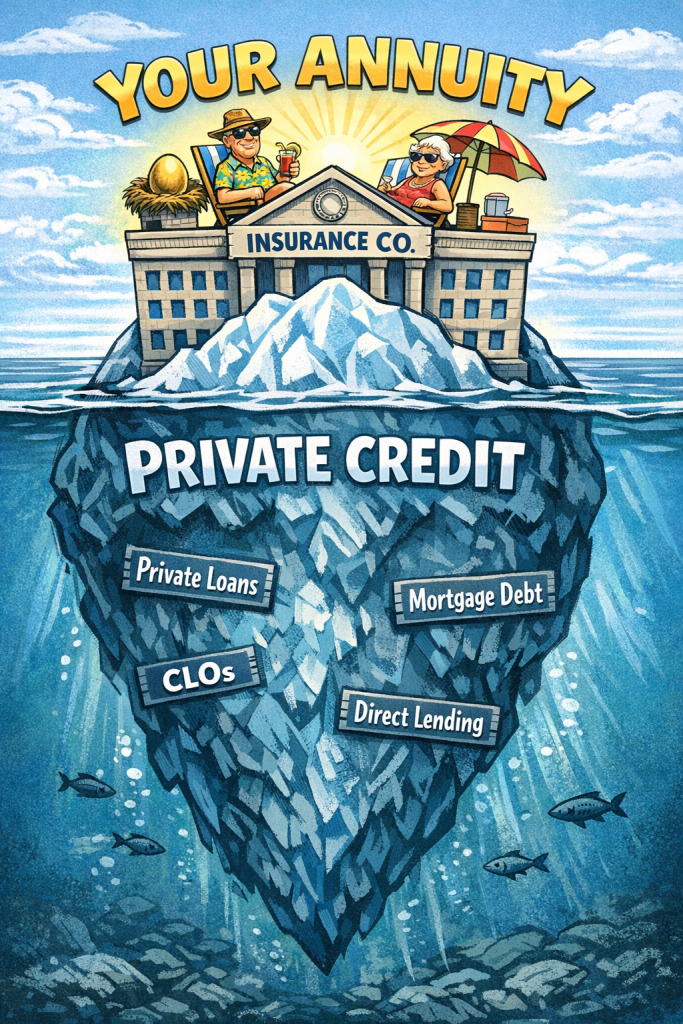

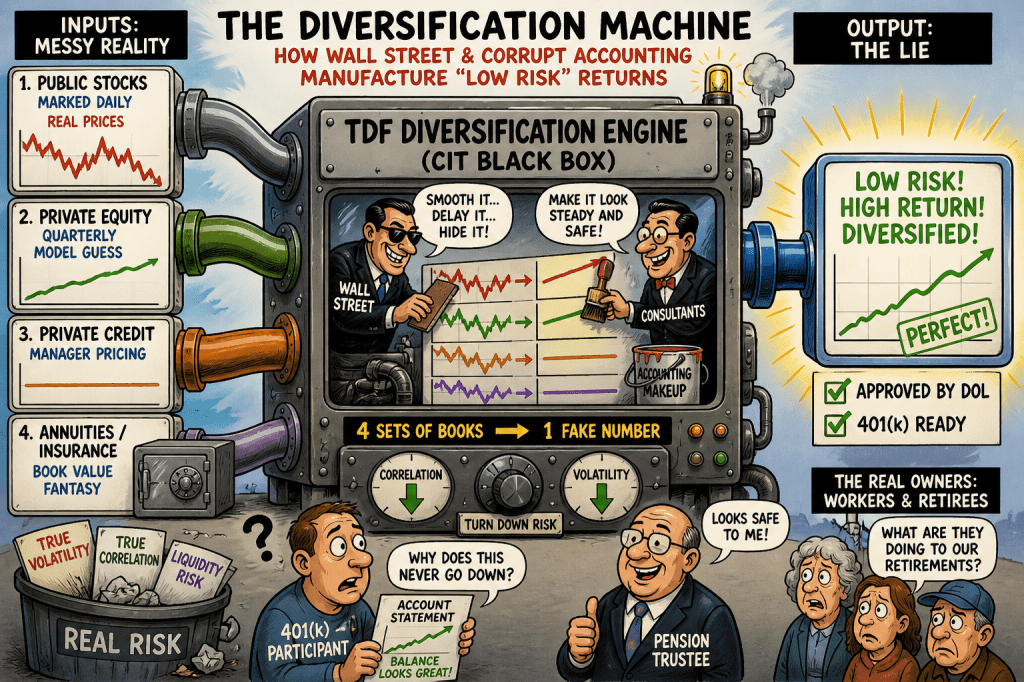

Enter the DOL: Bringing the Distortion into 401(k)s

Your prior work correctly identifies the next phase:

- The DOL rule enables these same assets in 401(k)s

- CITs allow mixing multiple accounting regimes

- Target Date Funds become the delivery vehicle

Inside a single TDF, you now have:

- Daily-priced public equities

- Quarterly private equity marks

- Model-based private credit

- Book-value annuities

Four incompatible accounting systems in one fund https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/

This is not diversification.

This is accounting chaos by design. https://commonsense401kproject.com/2026/04/03/dol-401k-fiduciary-rule-enables-accounting-fraud/

CITs: The Black Box That Makes It Possible

Unlike mutual funds, CITs:

- Avoid SEC transparency

- Operate under weak state regulation

- Allow hidden alternative exposures

- Enable discretionary valuation

They are the perfect container for:

- Private Equity

- Private Credit

- Annuities

- Structured products

And most importantly:

👉 They allow the accounting differences to remain hidden

Why This Is Dangerous in 401(k)s

Public pensions at least have:

- Investment staff

- Consultants

- Governance structures

401(k) participants have none of that.

They get:

- Defaulted into Target Date Funds

- With no visibility into underlying assets

- And no understanding of the risks

Yet those risks are:

- Higher leverage

- Lower liquidity

- Concentrated credit exposure

And critically:

👉 Mis-measured risk

The Endgame: When Smoothing Fails

This system works as long as:

- Markets rise

- Valuations are stable

- Liquidity holds

But when stress hits:

- Private valuations catch up

- Correlations spike toward 1

- Losses appear suddenly

And the “diversification” disappears overnight.

Bottom Line

Private Equity and Private Credit do not deliver diversification the way they are marketed.

They deliver:

- Artificially low volatility

- Artificially low correlation

- Artificially high allocations

All driven by accounting practices that smooth, delay, and obscure reality.

And now, through DOL policy and CIT structures, that same flawed model is being embedded into the core of the U.S. retirement system.

Call it what it is:

Diversification built on accounting fiction.