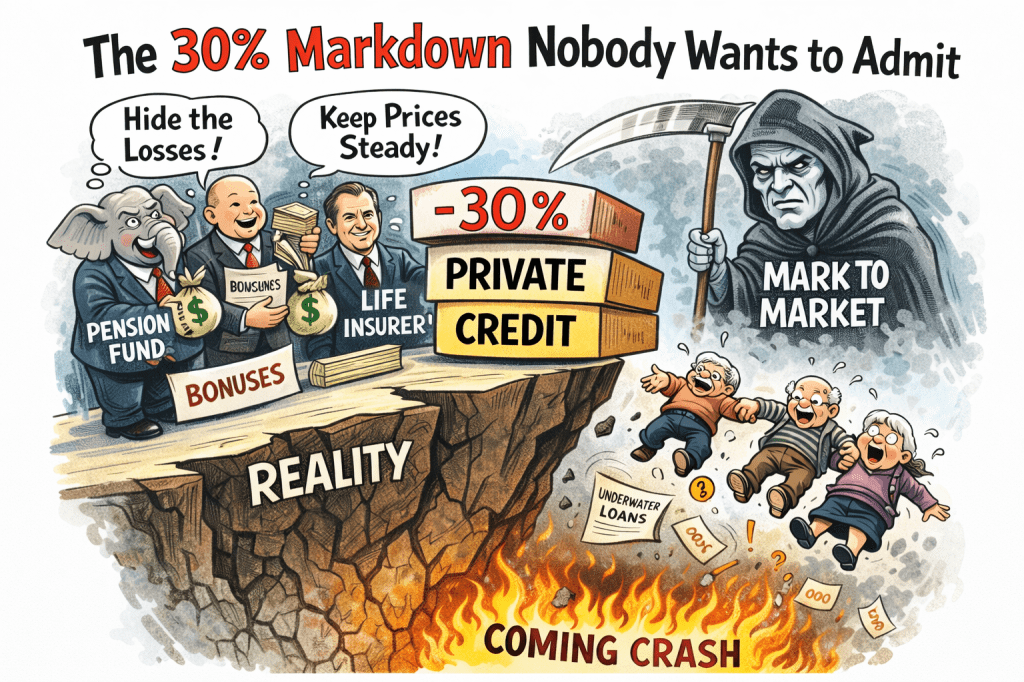

The private credit boom has been built on a simple premise: that loans held inside private funds are somehow safer, smoother, and more stable than those traded in public markets. Pension boards and insurance regulators have been told repeatedly that these assets produce steady income, modest volatility, and superior returns compared with traditional bonds. But the illusion of stability rests almost entirely on one thing — the ability of managers to avoid marking their portfolios to market. When assets do not trade, managers get to decide what they are worth.

Recent market signals suggest that if private credit were forced into real price discovery today, the markdown would be severe. Secondary market bids for private credit funds have appeared at roughly 65 cents on the dollar, implying discounts of about 35% to stated net asset value. That is not a theoretical model; it is what buyers are actually willing to pay for exposure to these portfolios right now. Even industry research has quietly acknowledged that private market assets often require discounts of 11–20% just to transact. The market is telling us something clear: the values reported by many funds likely exceed what investors could realize in a forced sale.

The reason those losses are not visible in public pension reports is simple. Most private credit assets are priced by internal models rather than markets. https://commonsense401kproject.com/2025/12/13/is-private-credit-performance-a-fraud/

Loans are marked quarterly using appraisal-style methodologies, comparable transactions, and manager estimates. Unless a borrower defaults outright, there is often no requirement to reflect the deterioration in market value that occurs as credit spreads widen or financing conditions worsen. In other words, a loan can lose a large portion of its economic value while the accounting value barely moves.

That is why defaults are such a misleading indicator of the true damage. Fitch reported recently that private credit defaults reached 9.2% in 2025, the highest level recorded. But defaults are only the visible failures — the tip of the iceberg. In most credit cycles the bulk of losses occur not because loans immediately default, but because their market value declines long before that point. When portfolios are not marked to market, those losses remain hidden until they can no longer be ignored.

Public pensions have powerful incentives to delay that moment. Large allocations to private credit and other alternative assets have been used to justify bonuses, consultant fees, and claims of superior performance. A sudden mark-to-market adjustment could expose years of overstated returns and raise uncomfortable questions about governance and oversight. Honest pricing could cause serious scandals around pay-to-play since most Private Credit vehicles are in secret no-bid contracts many offshore. The temptation to smooth valuations, delay recognition, and hope that markets recover is enormous.

Life insurers face a similar dilemma. The insurance industry now holds enormous volumes of private credit, particularly through structures associated with asset managers like Apollo and affiliated insurers such as Athene. For insurers, recognizing large valuation losses can trigger credit-rating pressure and regulatory scrutiny. As a result, there is strong incentive to rely on model-based valuations rather than market prices for as long as possible. In some cases the only external signal of rising risk may come from the derivatives market, where credit default swaps begin to price in deterioration long before accounting values change.

This dynamic creates a dangerous illusion. Reported values remain stable while economic values erode underneath them. When losses finally appear — often through defaults or forced sales — they arrive suddenly and in concentrated bursts. By that point the markdown reflects only the loans that have already collapsed, while the broader decline in portfolio value has been ignored for years.

If private credit portfolios were forced into true market pricing today, the evidence suggests the haircut could easily approach 30 percent or more across many strategies. That number is uncomfortable, but it aligns with what secondary buyers are already implying and with the discounts required to move private assets in stressed conditions. The danger is not simply the loss itself. It is the delayed recognition.

By postponing market pricing, pension systems and insurers risk transforming what could have been a gradual adjustment into a much larger reckoning later. The longer valuations remain detached from reality, the more dramatic the correction becomes when markets finally impose discipline.

The private credit boom promised stability. But stability created by accounting discretion rather than market pricing is not stability at all. It is simply a markdown waiting to happen — and the longer it is delayed, the larger it is likely to be.

Legal Appendix: When Private Credit Lies Meet ERISA

The growing exposure of retirement systems to private credit creates a legal risk that few pension sponsors appear to be acknowledging.

Private credit assets are typically not marked to market. Their valuations are often based on internal models or manager-supplied estimates rather than observable market prices. That creates the possibility that pension plans are carrying assets at inflated values.

If those valuations are overstated, the consequences extend far beyond investment performance.

They affect ERISA compliance and federal insurance premiums.

Defined benefit pension plans insured by the Pension Benefit Guaranty Corporation (PBGC) must pay annual variable-rate premiums based on underfunding levels. The stronger a plan’s funding ratio appears, the lower its PBGC premium.

But funding ratios depend directly on the reported value of plan assets.

If private credit assets are carried above their true economic value — for example, if the market would impose the kind of 20–30% markdowns increasingly discussed in credit markets — then pension funding ratios are overstated.

Overstated funding ratios mean lower PBGC premiums.

At that point the issue is no longer simply poor investment judgment.

It begins to resemble misrepresentation to a federal insurance program.

The legal exposure does not stop there.

Private credit risks are also surfacing in the annuity market that increasingly replaces pension plans. Pension Risk Transfer (PRT) annuities and fixed annuities in defined contribution plans do not mark liabilities to market either. But credit deterioration eventually reveals itself through two signals markets cannot hide:

- Credit rating downgrades, and

- Rising credit-default-swap (CDS) spreads, which reflect the market’s real-time assessment of insurer default risk.

When those signals emerge, plaintiffs will inevitably ask a simple question:

Did fiduciaries ignore market evidence that the underlying credit risk was deteriorating?

The Supreme Court’s pending Intel ERISA case may determine whether courts remain able to examine opaque investments like private credit at all. If the Court requires plaintiffs to produce perfect benchmarks before discovery, the practical effect will be to shield private-credit valuations from scrutiny — precisely because those assets lack transparent market pricing.

In other words, the Court may decide whether opacity becomes a legal defense.

If the market ultimately forces the 30% markdown in private credit that many analysts now expect, the legal consequences could cascade through the retirement system:

- overstated pension funding ratios,

- reduced PBGC premiums based on inflated assets, and

- annuity portfolios whose risk was hidden until credit spreads exploded.

When that happens, the question will not be whether losses occurred.

The question will be who knew the valuations were unrealistic — and who kept using them anyway.