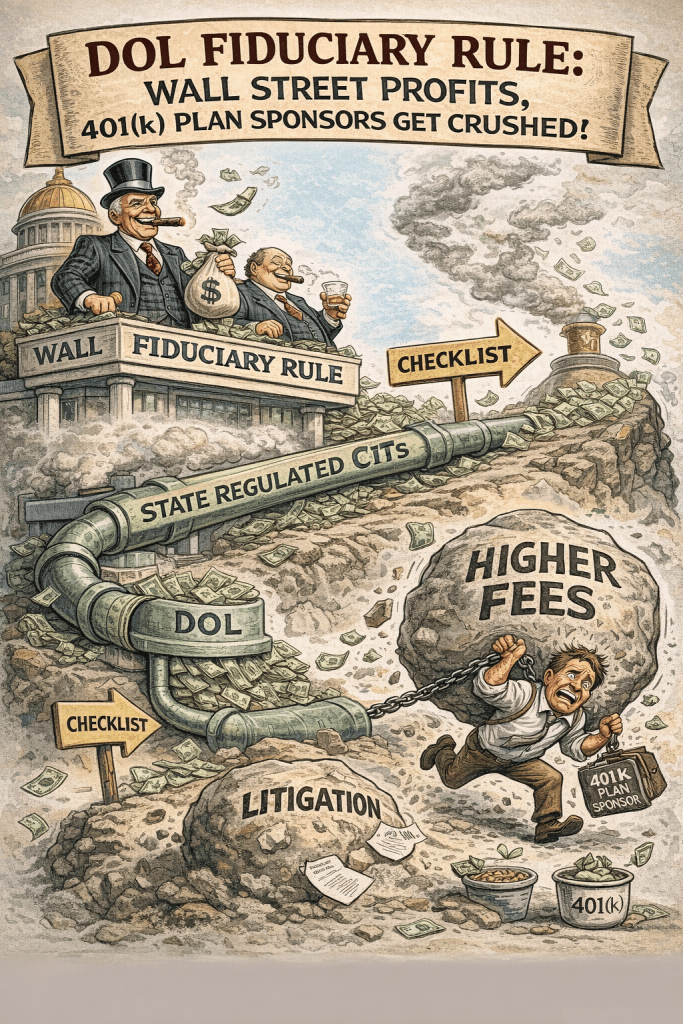

The Department of Labor is selling its new fiduciary rule as protection.

Protection from lawsuits.

Protection through process.

Protection via a checklist.

But strip away the language, and the reality is far more troubling:

👉 This rule is not about reducing litigation.

👉 It is about unlocking new revenue streams for Wall Street and the insurance industry—while leaving plan sponsors holding the liability.

The Bait: “Follow the Checklist, Reduce Your Risk”

The DOL’s message is simple:

If fiduciaries evaluate:

- fees

- performance

- liquidity

- complexity

- valuation

…then they will be protected.

But even under the rule itself, that protection is weak:

- It is not a true safe harbor

- It is only a rebuttable presumption

- Plaintiffs can still challenge the outcome

So what the DOL is really offering is not protection—it is procedural cover.

The Switch: Open the Door to High-Fee, Opaque Products

While promising protection, the rule simultaneously:

- Encourages alternative investments in 401(k)s

- Channels those investments into state-regulated CITs

- Facilitates inclusion of annuities and insurance products

These are not low-cost index funds.

These are:

- Private equity

- Private credit

- Insurance-wrapped products

- Spread-based annuities

👉 In other words: the highest-margin products in the entire financial system.

Why Wall Street and Insurers Win Immediately

This rule creates an immediate economic shift:

💰 More complexity = more fees

- Private markets → higher management fees

- CITs → less fee transparency

- Annuities → hidden spreads (often 100–300+ bps)

💰 Less transparency = less pricing pressure

- No SEC disclosure regime

- No daily pricing discipline

- No meaningful benchmarking

💰 Faster revenue recognition

- Fees and spreads are earned today

- Risks are borne later

Translation:

👉 Wall Street and insurers get paid now

👉 Participants take the risk later

👉 Plan sponsors absorb the liability when things go wrong

CITs: The Perfect Revenue Vehicle (and Litigation Time Bomb)

The rule effectively pushes plans into Collective Investment Trusts (CITs).

Why?

Because CITs allow:

- Mixing of public and private assets

- Limited disclosure

- State-level oversight instead of SEC regulation

And here’s what most fiduciaries—and participants—don’t realize:

👉 Many CITs are regulated at the state level (PA, NH, MD, etc.)

👉 That fact is often buried in fine print

👉 Underlying holdings are frequently undisclosed or poorly understood

That’s Not Just a Disclosure Problem—It’s a Legal Problem

Because once litigation begins, everything changes.

Discovery will ask:

- What regulator governs this CIT?

- What assets are inside it?

- Are any affiliates involved?

- How are values determined?

- What compensation is embedded?

And under Cunningham v. Cornell:

👉 If a party in interest is involved, the burden shifts

One Hidden Conflict Can Blow Up the Entire Structure

This is where the DOL’s rule becomes dangerous.

Inside these CIT-based target date funds, you may find:

- Affiliated private credit funds

- Insurance general account exposure

- Revenue-sharing arrangements

- Spread-based annuities

If any one of those components is found to be a prohibited transaction:

👉 The entire structure becomes subject to challenge

👉 Damages can follow

👉 Fiduciaries—not providers—are on the hook https://commonsense401kproject.com/2026/04/03/dol-401k-fiduciary-rule-enables-accounting-fraud/

The Real Risk Shift: From Providers to Plan Sponsors

Wall Street and insurers are insulated:

- They design the products

- They control the disclosures

- They collect the fees

But they are not fiduciaries.

Plan sponsors are.

So when things go wrong:

👉 It is not the product manufacturer that gets sued

👉 It is the plan committee

Morningstar Already Admits the Questions Aren’t Answered

Even industry observers acknowledge:

- Valuation concerns

- Fee opacity

- Liquidity risks

- Structural complexity

These are not technical issues.

These are the exact elements plaintiffs’ attorneys litigate. https://www.morningstar.com/alternative-investments/private-investments-401ks-we-still-have-questions

Bottom Line

The DOL claims this rule protects fiduciaries.

But the real structure is clear:

Wall Street and insurers:

- Gain new access to 401(k) assets

- Increase fees and spreads

- Face limited transparency requirements

Participants:

- Bear higher costs

- Take on opaque risks

- Lose visibility into their investments

Plan sponsors:

- Assume fiduciary responsibility

- Face increased litigation exposure

- Rely on a “checklist defense” that will not hold up

This rule isn’t a shield.

It’s a handoff:

👉 Profits go to Wall Street and insurance companies

👉 Risk goes to participants

👉 Liability stays with plan sponsors

And when the lawsuits come—as they will—

the checklist won’t save anyone.

🎯🎯🎯

Yahoo Mail: Search, Organize, Conquer

LikeLike