Investment Policy Statements (IPS) are often described as a cornerstone of fiduciary prudence. Consultants, recordkeepers, and industry “experts” routinely recommend them. Yet in the 401(k) world, IPS documents are frequently weak, superficial, or conspicuously absent.

That is not an accident. I suspect some many attorneys and consultants recommend that you do not have them at all to avoid accountability and liability.

Despite their importance, an IPS is not explicitly required under ERISA. That loophole has become a strategic escape hatch. Plan sponsors can claim adherence to fiduciary best practices while avoiding the discipline, transparency, and accountability that a robust IPS would impose.

The Illusion of Compliance

The industry line goes something like this:

“An IPS is a best practice, but not legally required.”

Translation: we’ll give you one if you ask—but don’t expect it to actually constrain anything.

In practice, most 401(k) plans fall into one of three categories:

- No IPS at all – especially in small and mid-sized plans

- Template IPS documents – boilerplate language, largely meaningless

- Superficial IPS frameworks – broad principles, no enforceable standards

Only the largest “mega plans” tend to have detailed IPS documents—and even those often fail where it matters most.

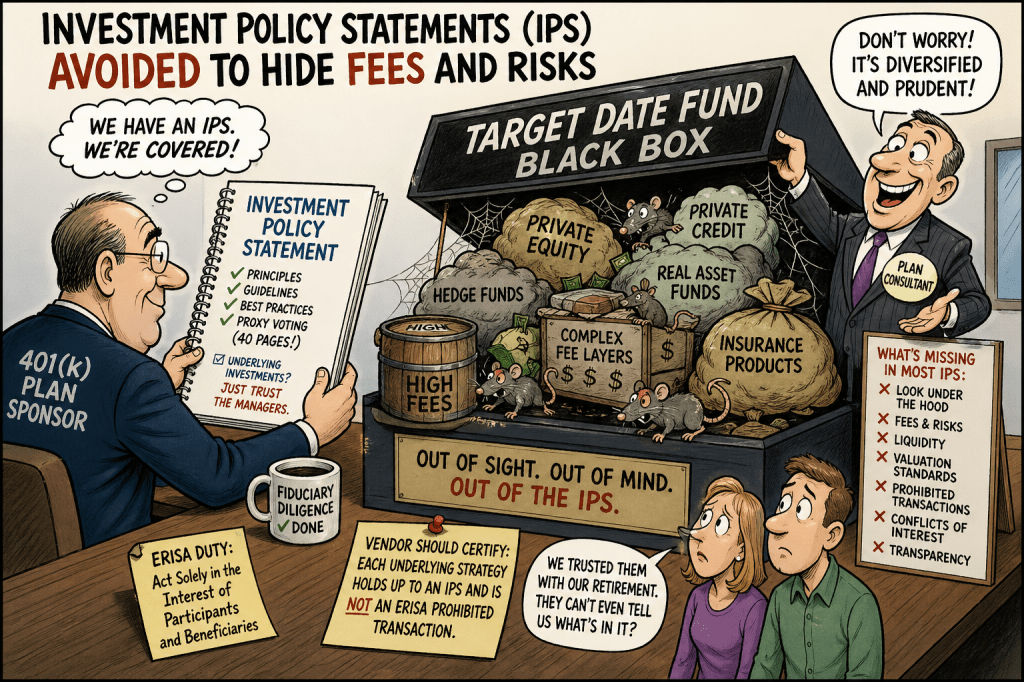

Target Date Funds: The Black Box Problem

Today, target date funds (TDFs) dominate the 401(k) landscape, accounting for more than 50% of assets in many plans. They are marketed as diversified, professionally managed, and prudent.

But here’s the problem:

Most IPS documents do not look under the hood of target date funds.

Instead, they treat TDFs as a single “qualified default investment alternative” (QDIA) and stop there.

That is a massive blind spot.

A proper IPS should require that:

- Each underlying strategy within a TDF should be evaluated independently

- Each component is assessed for fees, liquidity, valuation, and conflicts

- Each investment complies with ERISA prohibited transaction rules

- Structure review if not a SEC-registered mutual fund, but a weak state-regulated CIT

Instead, what we see is the opposite:

- Private equity is embedded in TDFs with no disclosure standards

- Private credit exposures with opaque valuation

- Insurance products (annuities) are buried inside structures

- Fee layers that cannot be reconciled from participant disclosures

A weak IPS doesn’t just fail to detect these issues—it actively conceals them. This coincides with the legal theory of meaningful benchmarks, which is used to block transparency. https://commonsense401kproject.com/2026/01/20/why-the-meaningful-benchmark-standard-is-a-judicial-illusion-built-for-wall-street/

The Missing Standard: Prohibited Transactions

One of the most glaring omissions in most IPS documents is any meaningful discussion of ERISA prohibited transactions.

This is where the rubber meets the road.

If an investment:

- Involves a party in interest

- Includes undisclosed compensation (revenue sharing, spreads, shelf fees)

- Relies on opaque valuation or self-dealing

…it may violate ERISA’s core fiduciary rules.

Yet IPS documents almost never require vendors to certify that:

“Each underlying investment strategy is not an ERISA prohibited transaction.”

Why not?

Because forcing that statement would expose the economic reality of many products—particularly:

- General account and Separate Account annuities

- Private market vehicles embedded in CITs and TDFs

- Hidden strategies like Crypto

CALPERS: A Case Study in IPS Failure

In our 288-page report on CALPERS, we made a deliberate decision:

We did not even discuss the IPS.

Why?

Because it was effectively useless.

The document devoted roughly 40 pages to proxy voting—a topic with minimal financial impact on returns—while offering only superficial treatment of:

- Private equity

- Private credit

- Valuation methodology

Even worse, the IPS simply deferred to a separate “valuation policy.”

And that valuation policy? A rubber stamp.

It essentially states that CALPERS relies on manager-provided valuations—the very entities with the strongest incentive to overstate performance.

In other words:

- No independent pricing

- No market discipline

- No enforceable standards

Calling this a “policy” is generous. It is closer to a delegation of responsibility without oversight.

Why Weak IPS Documents Persist

The absence of meaningful IPS enforcement is not a coincidence. It serves multiple stakeholders:

1. Plan Sponsors

Avoid liability by maintaining plausible deniability:

- Our consultants said we did not need an IPS

- “We followed our IPS”

- Even if the IPS says nothing meaningful

2. Consultants

Preserve flexibility:

- No constraints on recommending high-fee or conflicted products

- No accountability for underlying structures

3. Recordkeepers and Vendors

Maintain opacity:

- Hide revenue streams (spreads, kickbacks, platform fees)

- Bundle products that would fail scrutiny individually

4. Asset Managers

Avoid scrutiny of:

- Private market valuations

- Illiquid investments

- Complex fee structures

A real IPS would disrupt all of this.

What a Real IPS Should Do

A legitimate Investment Policy Statement should:

- Drill into underlying holdings, not just superficial products like Target Date

- Require transparent, market-based valuation standards

- Explicitly prohibit undisclosed compensation structures

- Mandate analysis of liquidity and credit risk

- Require certification of ERISA compliance at the strategy level

- Establish benchmarking based on investable alternatives

Most importantly, it should be enforceable.

Without enforcement, an IPS is just a document—useful for optics, useless for protection.

The Bottom Line

Investment Policy Statements in the 401(k) world are often presented as evidence of fiduciary discipline.

In reality, they frequently function as:

A shield for fiduciaries—and a blindfold for participants.

As target date funds continue to absorb the majority of retirement assets, the failure to scrutinize what lies beneath them becomes more dangerous.

A weak IPS doesn’t just fail to protect participants.

It enables the high risks and hidden costs that ERISA was designed to prevent.

Until IPS documents require real transparency—down to the underlying investments and their economic structure—the system will continue to operate in the shadows.

And that, more than anything, explains why so many in the industry prefer them weak—or not at all.