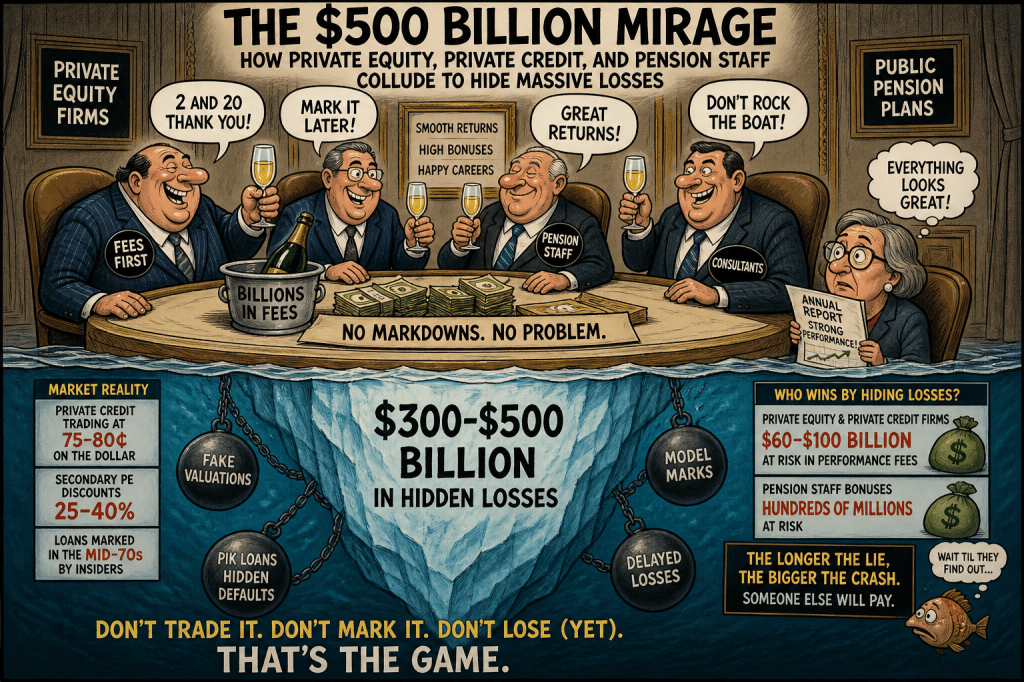

There is a simple reason you are not hearing about massive losses in public pensions right now:

Because no one involved gets paid if the truth comes out.

Behind the polished annual reports and carefully engineered benchmarks sits what may be the largest coordinated financial misrepresentation in modern pension history—hundreds of billions in unrecognized losses in Private Equity and Private Credit.

The Market Has Already Spoken—Pensions Are Ignoring It

6

In recent weeks, real pricing has started to leak out:

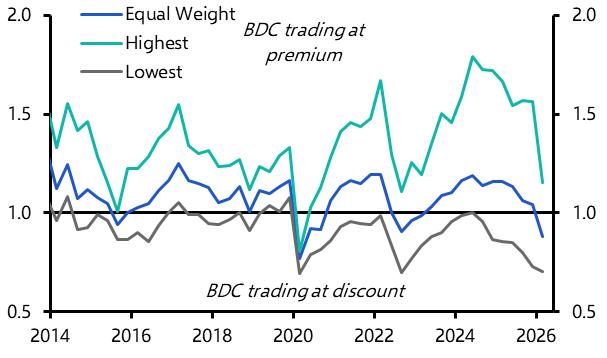

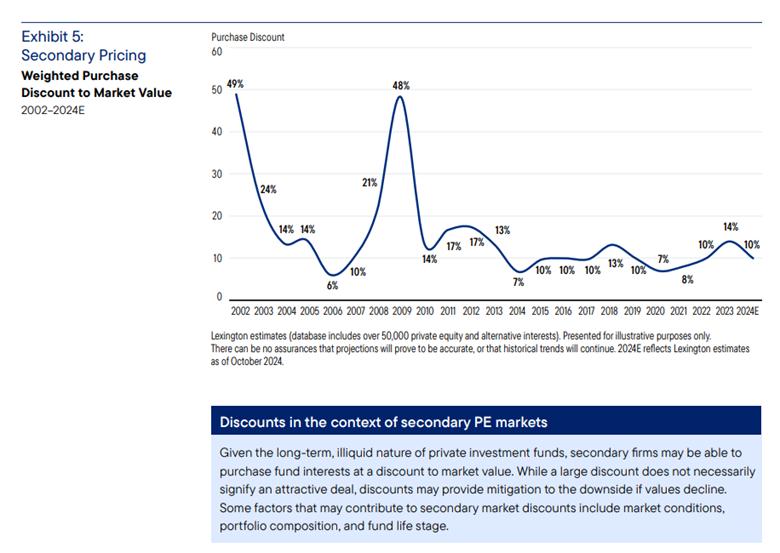

- Publicly traded private credit funds are trading at ~75–80 cents on the dollar

- Secondary markets for private equity show material discounts

- Even insiders have acknowledged loans in weaker portfolios marked in the mid-70s

That is market pricing.

Yet public pension reports still show:

- Private credit: ~95–100 cents

- Private equity: flat or positive returns

This is not a timing issue.

This is a valuation regime designed to avoid reality.

The Scale of the Problem: $300–$500 Billion in Hidden Losses

Start with a simple framework:

- U.S. public pensions: ≈ $6 trillion

- Allocation to Private Equity + Private Credit: ~20–25%

- Total exposure: ≈ $1.2–$1.5 trillion

Now apply observable market discounts:

| Asset | Exposure | Realistic Discount | Implied Loss |

| Private Credit | ~$400B | 20–30% | $80B–$120B |

| Private Equity | ~$900B | 25–40% | $225B–$360B |

Total hidden losses: $300B to $500B

And that is a conservative estimate.

Why These Losses Are Not Being Recognized

Because the system is built to delay loss recognition.

Private assets are:

- Level 3 (model-based) valuations

- Marked by the same firms that earn fees from them

- Rarely subjected to real transactions

This allows:

- Smoothing of returns

- Lagging write-downs by years

- Artificial “outperformance” vs public markets

In other words:

If you don’t trade it, you don’t have to price it. https://commonsense401kproject.com/2026/04/08/why-the-private-credit-meltdown-may-take-a-while/

The Incentive Structure: Everyone Gets Paid to Pretend

This is where the story moves from negligence to something far more troubling.

Private Equity and Private Credit Firms (2 and 20)

- Fees are based on reported NAV and performance

- Lower valuations = lower fees

If assets were marked honestly:

- Performance fees would fall dramatically

Estimated impact:

- $60 billion to $100 billion in lost performance fees by PE firms

Pension Staff

- Bonuses tied to reported returns

- “Outperformance” often based on non-investable benchmarks

If losses were recognized:

- Bonuses collapse

- Career narratives collapse

Estimated impact:

- Hundreds of millions in staff compensation

That is currently way above private market levels. https://commonsense401kproject.com/2026/05/02/ohio-strs-investment-staff-paid-excessively-to-look-the-other-way/

I also believe that since Citizens United the Private Equity industry has found a way to enrich state level officials via dark money that appoint and control pension board members as evidenced by huge increase in Private Equity in secret no-bid contracts.

The Quiet Alignment of Interests

This is not a conspiracy in the traditional sense.

It is something more durable:

A perfectly aligned incentive system

| Group | Incentive |

| Private Equity | Keep valuations high |

| Private Credit | Avoid defaults/write-downs |

| Pension Staff | Preserve performance and bonuses |

| Consultants | Captured by staff some even owned by PE |

No one benefits from recognizing losses.

So losses are not recognized. https://commonsense401kproject.com/2025/12/11/how-americas-largest-pension-consultants-became-the-distribution-arm-for-private-equity/

The “Artificial Alpha” Machine

This is how the illusion works:

- Private assets are not marked to market

- Benchmarks are lagged or custom-built

- Reported returns appear stable

- Bonuses and fees are paid

- Losses are deferred into the future

This creates what can only be described as:

Manufactured outperformance

State Pension staff and Private Equity/Credit are tied in numerous ways. For example with Jeffrey Epstein linked Apollo they stick with them through scandals https://commonsense401kproject.com/2026/04/17/apollo-divestment-case-for-jeffrey-epstein-ties-stronger-after-wyden-letter/ and will refuse to file stock drop claims. https://commonsense401kproject.com/2026/04/11/state-pensions-notably-absent-from-apollo-stock-drop-cases/

Public assets in Private Equity and Private Credit funds allow them to put up to 25% of the fund in ERISA assets without ERISA level transparency and disclosures, hiding billions in fees for 401k and other private sector pension assets.

The Dangerous Endgame

The risk is not just accounting.

It is liquidity.

If pensions ever need to:

- Rebalance

- Pay benefits during stress

- Or sell assets

They will discover:

- The market price is far below reported value

- Losses materialize instantly

This is how a slow-motion accounting problem becomes a sudden funding crisis.

The Parallel to 2008—But Worse

In 2008:

- Banks marked assets too slowly

- Losses eventually forced into the open

Today:

- Pensions don’t face daily liquidity pressure

- Losses can remain hidden much longer

Which means:

The eventual adjustment could be larger.

The Bottom Line

Public market signals are clear.

Private market accounting is not.

Between the two sits a gap of:

$300 billion to $500 billion in unrecognized pension losses

And behind that gap sits:

- $60–$100 billion in private equity and private credit fees

- Hundreds of millions in pension staff bonuses

All dependent on one thing:

Not marking assets to reality.

Final Thought

This is not just a valuation issue.

It is a fiduciary issue.

Because when losses are hidden:

- Participants are misled

- Risks are understated

- Decisions are distorted

And eventually—

Someone else pays the price.