A new March 2026 academic study, Choosing Pension Fund Investment Consultants, may be one of the most important confirmations yet of what many critics of public pension investing have argued for years: investment consultants are not independent guardians of pension performance. They have increasingly become a distribution network for higher-fee alternative investments — especially private equity, private credit, hedge funds, and real assets — with little evidence that these strategies improve returns for pension beneficiaries.

The study by Aleksandar Andonov, Matteo Bonetti, and Irina Stefanescu systematically examines how consultants shape the investment behavior of U.S. public pensions. https://ssrn.com/abstract=4306217 Their findings strongly reinforce the concerns raised earlier in the Commonsense article, How America’s Largest Pension Consultants Became the Distribution Arm for Private Equity.

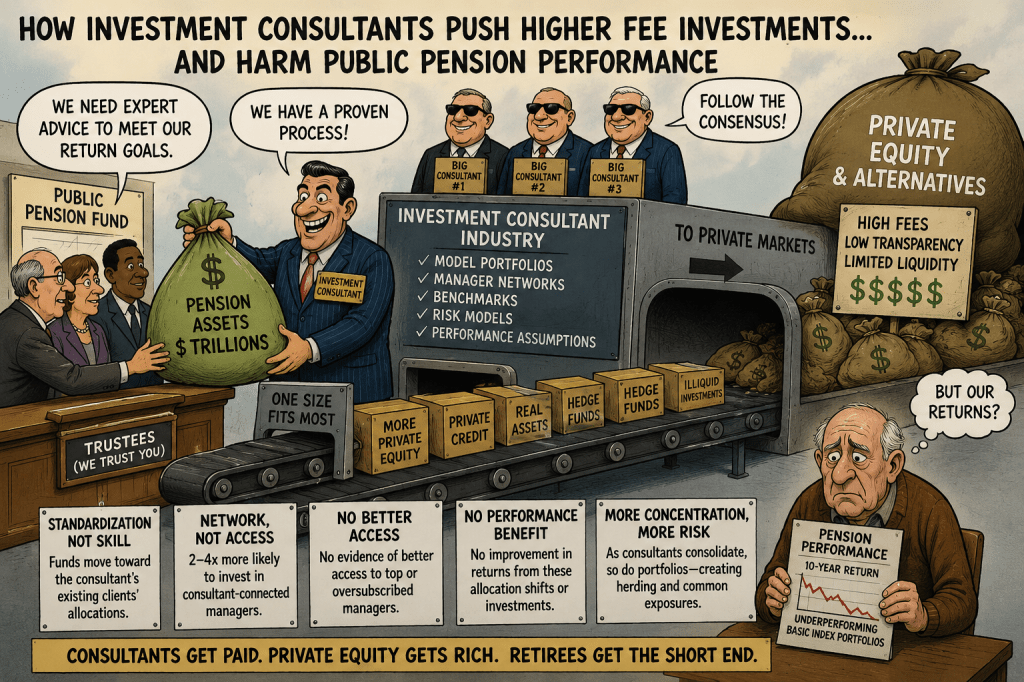

The core conclusion is devastating.

Consultants push pensions toward the same high-fee investments, often through the same networks of private fund managers, creating widespread portfolio convergence and systemic concentration risk — yet the study finds no meaningful evidence that these consultant-driven shifts improve performance.

The Consulting Industry Now Controls Public Pension Asset Allocation

According to the study, investment consultants advised approximately $19.5 trillion in pension assets as of 2024.

Over time, the consulting industry itself has become highly concentrated. By 2020, the top three consultants advised roughly half of all U.S. public pension assets.

That means a handful of firms increasingly determine:

- which asset classes pensions enter,

- which private equity firms receive commitments,

- which benchmarks are used,

- which “risk models” are accepted,

- and ultimately how trillions in retirement assets are deployed.

The study found that when pensions hire a new consultant, they rapidly begin to resemble the portfolios of the consultant’s other clients.

This is not independent fiduciary analysis.

It is industrialized standardization.

A pension fund in California, Iowa, Kentucky, or Texas increasingly receives variations of the same portfolio model:

- higher allocations to private equity,

- higher allocations to private credit,

- more “real assets,”

- lower transparency,

- more illiquid structures,

- and higher fees.

The authors specifically found that:

“Pension funds adjust their asset allocations toward the average portfolios of the consultant’s existing clients.”

That sounds less like fiduciary customization and more like franchise distribution.

The Private Equity Push

The study directly confirms that consultants have been central to the explosion of alternative investments in public pensions.

Public pension allocations to alternatives rose from roughly 10% to 30% during the study period.

At the same time, use of specialized private equity consultants surged.

Why?

The paper gives the answer plainly:

pensions hire specialized consultants specifically to scale up alternative investments.

Not because performance was proven superior.

Not because risk was lower.

Not because transparency improved.

But because pensions had target allocations to alternatives they wanted to fill.

The consultants became the machinery that helped force capital into private markets.

This mirrors precisely what critics have argued for years: consultants are compensated and incentivized inside an ecosystem dominated by private equity firms, private credit managers, real asset sponsors, and opaque benchmarking structures.

The “Access” Myth Falls Apart

One of the biggest defenses of private equity consultants has always been:

“We provide access to elite managers.”

The study directly tested this claim.

The researchers examined whether consultant-connected pensions gained access to:

- oversubscribed funds,

- later-stage top managers,

- co-investment opportunities,

- or otherwise capacity-constrained vehicles.

The answer:

almost no evidence.

Instead, consultants primarily steered pension money toward managers already within the consultant’s network.

The study found:

“A private fund is two to four times more likely to receive a commitment if it is connected to the consultant.”

That finding should alarm every public pension beneficiary in America.

Because it suggests the consultant business model is driven less by objective fiduciary analysis and more by network distribution dynamics.

In plain English:

the same consultants repeatedly funnel pension assets to the same private equity firms.

No Performance Benefit

The most important finding may be the simplest.

After all the complexity, opacity, illiquidity, and fees:

there was no measurable performance benefit.

The study found:

- no significant improvement in pension performance after consultant-driven allocation changes,

- no meaningful outperformance from specialized consultants selecting private funds,

- and no reliable evidence that consultant-advised private equity investments performed better than non-advised investments.

This is an extraordinary result considering the billions paid annually in:

- consulting fees,

- private equity management fees,

- carried interest,

- transaction fees,

- monitoring fees,

- fund-of-fund fees,

- and performance bonuses for pension staff tied to alternative benchmarks.

The consultants pushed pensions toward higher-cost structures without generating corresponding value.

Benchmark Engineering and the Illusion of Alpha

The study indirectly supports another growing criticism:

consultants help create benchmark systems that make private assets appear superior even when they are not.

Public pension boards often rely heavily on consultant-created assumptions:

- expected return forecasts,

- private equity volatility estimates,

- diversification assumptions,

- correlation matrices,

- and benchmark constructions.

But private equity and private credit valuations are not continuously marked to market like public securities.

That creates artificially low volatility and artificially high Sharpe ratios.

The result is an illusion of diversification and alpha generation.

Consultants then use these distorted statistics to justify even larger allocations to alternatives.

The cycle feeds itself:

- Consultants recommend higher alternatives.

- Alternatives use smoothed valuations.

- Smoothed valuations reduce apparent volatility.

- Lower volatility “proves” diversification.

- Consultants recommend even more alternatives.

Meanwhile, actual economic risk may be rising dramatically beneath the surface.

Consultants as Political Shields

The paper also highlights another important dynamic:

consultants serve as political protection for pension trustees.

Boards often lack investment expertise. Public trustees face political pressure and reputational risk. Hiring prestigious consultants allows boards to say:

“We relied on expert advice.”

But if the consultants themselves are embedded inside the private equity ecosystem, the entire fiduciary process becomes compromised.

The consultant becomes:

- the validator,

- the benchmark designer,

- the allocator,

- the gatekeeper,

- and effectively the distribution channel.

This creates a dangerous concentration of influence over public retirement assets.

The Real Damage

The real-world consequences are enormous.

Public pensions today often hold:

- 25% to 40% in alternatives,

- massive private credit exposure,

- illiquid real estate,

- infrastructure,

- leveraged buyouts,

- and opaque valuation-dependent investments.

At the same time:

- fees have exploded,

- liquidity risk has increased,

- transparency has collapsed,

- and benchmark accountability has deteriorated.

Yet many major public pensions have still underperformed simple passive public market portfolios over long periods.

The consulting industry helped engineer this transformation.

And according to this new academic evidence, they did so without delivering measurable value to pension beneficiaries.

The Bigger Question

The study ultimately raises a deeper fiduciary question:

If consultants systematically direct trillions toward higher-fee investments that:

- increase complexity,

- reduce transparency,

- create portfolio convergence,

- concentrate systemic risk,

- and fail to improve performance,

then whose interests are really being served?

Because increasingly, it appears the winners have been:

- private equity firms,

- private credit managers,

- alternative asset platforms,

- and the consultant industry itself.

Not retirees.

Andonov, Aleksandar and Bonetti, Matteo and Stefanescu, Irina, Choosing Pension Fund Investment Consultants (March 10, 2026). Available at SSRN: https://ssrn.com/abstract=4306217 or http://dx.doi.org/10.2139/ssrn.4306217