The collapse of PHL Variable Insurance Company should end the myth that annuities are somehow “safe” simply because they are wrapped in insurance company marketing language. What happened at PHL is not just an isolated insurance failure. It is a warning sign for the entire retirement system—especially for ERISA plans using annuities inside 401(k)s and Pension Risk Transfer (“PRT”) deals. Any ERISA plan with an Annuity without a downgrade clause is at high risk.

According to recent reporting with NBC https://www.nbcnews.com/news/us-news/paid-insurance-company-99000-generate-retirement-income-life-collapsed-rcna331934

PHL Variable—a private equity-owned insurer—collapsed after years of deterioration and is now heading toward liquidation, leaving many policyholders facing potentially massive losses above state guaranty limits.

The mainstream retirement industry keeps pretending annuities are equivalent to government-backed guarantees. They are not. They are unsecured obligations of highly leveraged insurance companies increasingly tied to private equity and private credit risk.

That distinction matters enormously under ERISA.

The PHL collapse exposes the fundamental fraud embedded in the modern annuity sales pitch to retirement plans. Participants are told they are buying “guaranteed income.” In reality, they are often buying concentrated exposure to a single insurer’s opaque balance sheet, private credit portfolio, derivatives exposure, and liquidity management strategy.

This is precisely why annuities in ERISA plans increasingly look like prohibited transactions.

The Department of Labor’s recent pro-annuity guidance ignores the central issue: the retirement system is being pushed toward products where the real risks are hidden inside insurance-company accounting structures that participants cannot evaluate. The underlying investments are often illiquid, privately valued, and shielded from normal SEC-style transparency. As discussed previously on Commonsense 401(k), many of these risks are amplified through state-regulated Collective Investment Trusts (“CITs”) and insurance separate accounts that avoid meaningful public disclosure.

PHL demonstrates what happens when the illusion breaks.

State guaranty associations that the annuity industry point to are a farce

https://commonsense401kproject.com/2025/06/24/state-guarantee-associations-behind-annuities-are-a-joke/ a typically capped around $250,000 for annuity present values have $0 balances so only designed for minimal at best coverage.

This becomes especially dangerous in Pension Risk Transfers which have 100% annuity coverage.

In a traditional defined benefit plan, retirees have protections through ERISA fiduciary duties and the Pension Benefit Guaranty Corporation. But once liabilities are dumped into an annuity structure through a PRT transaction, participants become exposed primarily to insurer solvency risk and limited guaranty association protections.

That is a massive downgrade in protection that the industry rarely discusses honestly.

The irony is staggering. Pension sponsors claim they are “de-risking” by shifting obligations to insurers. In reality, they may simply be replacing diversified pension funding structures with concentrated exposure to private equity-driven insurers increasingly loaded with private credit, commercial real estate, leveraged loans, and exotic structured assets.

The PHL collapse also destroys one of the central talking points used by annuity advocates: that insurance company failures are extremely rare and therefore not economically meaningful.

The modern insurance industry is not the same industry it was twenty years ago.

Private equity firms have aggressively moved into life insurance and annuity markets because retirement assets represent one of the largest pools of permanent capital in the world. Firms like Apollo Global Management transformed insurers such as Athene Holding into engines for gathering annuity assets and investing them into higher-risk private credit strategies. The economic model depends heavily on earning hidden spreads between what insurers make on investments and what they credit to retirees.

That creates an unavoidable conflict of interest.

The more risk the insurer takes internally, the larger the potential spread profits for shareholders and private equity sponsors. But retirees bear the ultimate solvency risk.

This is exactly why the PHL story should terrify fiduciaries considering annuity-heavy target-date funds or PRT transactions.

ERISA fiduciaries are supposed to act solely in participants’ interests. Yet many annuity arrangements involve opaque compensation, undisclosed spread profits, affiliated recordkeepers, proprietary CITs, and insurer-controlled valuation systems. Participants cannot independently evaluate the underlying risks because the accounting itself is often non-transparent.

The retirement industry calls this “innovation.”

A more accurate term may be “regulatory arbitrage.”

Even worse, the accounting structure of many insurance products can hide deteriorating asset values for years. As discussed previously in DOL 401(k) Fiduciary Rule Enables Accounting Fraud, private credit and insurance assets are often not marked to market in ways participants would recognize from mutual funds or public securities. This allows risk to accumulate quietly until a solvency event occurs.

That appears increasingly relevant in the PHL collapse.

The industry still insists annuities belong inside 401(k) default investments despite the fact that participants cannot meaningfully evaluate insurer balance sheets, CDS spreads, private credit concentrations, liquidity stress, or reinsurance chains.

Would any prudent fiduciary knowingly concentrate retirees into a single opaque private-credit vehicle with limited transparency, weak liquidity, and capped guaranty protection?

That is effectively what many annuity structures have become. Fixed annuities are in 2000 of the largest 8000 plans over $100 million in size and in bigger numbers in small plans. The new trend is to hide annuities into poorly state regulated CITs.

The PHL collapse should force courts, regulators, and fiduciaries to reconsider the entire legal framework surrounding annuities in ERISA plans. If these products expose participants to undisclosed insurer spread compensation, opaque accounting, affiliated-party conflicts, and substantial insolvency risk, then the prohibited transaction questions become unavoidable.

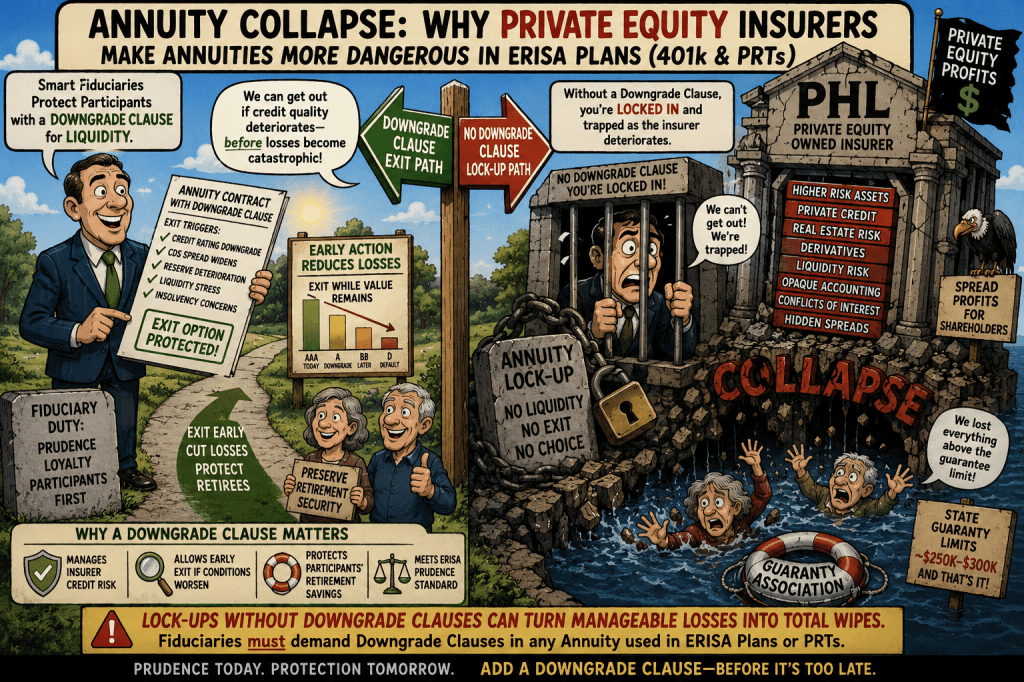

Even beyond the immediate losses, the PHL collapse exposes another major fiduciary failure in annuity structures used inside ERISA plans and Pension Risk Transfers: the lack of meaningful liquidity and downgrade protections. Any annuity used in a 401(k), stable value fund, or PRT transaction should contain a clear downgrade-triggered exit clause allowing fiduciaries to reduce or terminate exposure if the insurer’s credit quality materially deteriorates. That is standard risk management in many bond and derivative markets, yet retirement annuities are often structured as one-way lockups where participants remain trapped as the insurer weakens. Without downgrade clauses tied to credit ratings, CDS spreads, reserve deterioration, or liquidity stress, retirees can be forced to ride an insurer all the way into collapse. Fiduciaries should not be required to wait until losses approach 100% before acting. The ability to exit a deteriorating insurer early—while there is still market value left—is essential prudence under ERISA, particularly now that many annuity providers are deeply tied to private equity-driven private credit strategies.

The industry keeps calling annuities “guaranteed.”

PHL reminds us that the guarantee is only as strong as the insurer standing behind it.

https://commonsense401kproject.com/2026/03/26/apollos-garbage-dump-athene-loading-up-on-risk-endangers-retirees-in-prts-and-other-annuity-investors/ https://commonsense401kproject.com/2026/04/03/dol-401k-fiduciary-rule-enables-accounting-fraud/ https://commonsense401kproject.com/2026/03/01/annuities-as-prohibited-transactions-in-retirement-plans/