The biggest issue missing from the Kentucky pension litigation isn’t standing. It’s transparency.

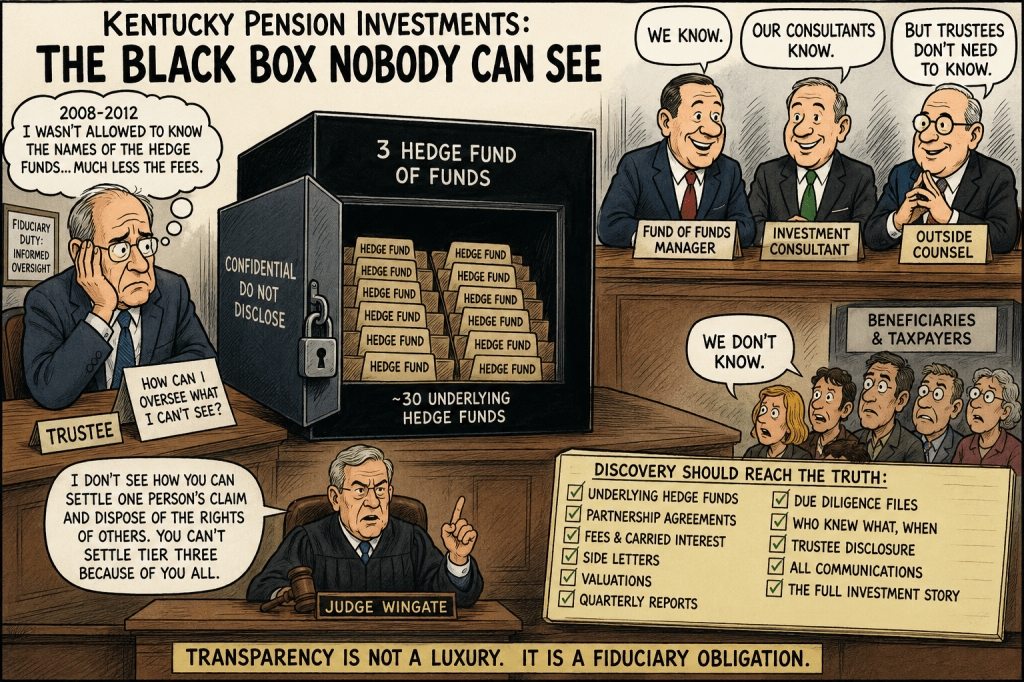

“From 2008 to 2012, while serving as a Kentucky Retirement Systems trustee, I was not allowed to know the names of the underlying hedge funds inside three hedge fund-of-funds managers. If I could not know what the pension owned, neither could taxpayers, beneficiaries, or outside experts. Fifteen years later, remarkably little has changed.”

I asked then and was denied and voted against Blackstone they are still keeping this secret.

After reading the transcript of the July 1, 2026 hearing before Franklin Circuit Judge Phillip Wingate, I was struck less by what was said than by what was never discussed.

For nearly 70 pages, attorneys debate standing, settlements, declaratory judgments, releases, and procedural authority.

Yet almost no one discusses the investments themselves.

That is remarkable considering the litigation ultimately concerns billions of dollars of pension assets entrusted to alternative investment managers.

As someone who served as a Kentucky Retirement Systems trustee from 2008 through 2012, I found the omission painfully familiar.

The Transcript Is About Procedure, Not Investments

Judge Wingate repeatedly tries to understand the procedural maze being placed before him.

At several points he questions why the parties appear to be attempting, through different legal vehicles, to accomplish essentially the same objective. He even comments that it sounds like “the same stuff” argued previously.

The discussion revolves around:

- standing

- settlement authority

- declaratory judgment

- releases

- jurisdiction

Those are important legal issues.

But there is a much larger issue sitting silently in the courtroom.

What exactly did Kentucky Retirement Systems own?

No one asks.

No one answers.

The Missing Layer

Most public discussion has centered on Blackstone.

But Blackstone was only one part of a much larger structure.

The pension system invested through three hedge fund-of-funds, which in turn invested in approximately thirty underlying hedge funds.

That second layer remains almost completely invisible.

Ironically, it was largely invisible even to trustees.

During my four years on the Board, I was never allowed to know the identities of the underlying hedge funds held inside these fund-of-funds structures.

Not only were the names withheld.

So were:

- underlying management fees

- incentive fees

- side letters

- liquidity restrictions

- partnership agreements

- operational due diligence reports

Even today, beneficiaries still cannot readily determine exactly what those fund-of-funds owned.

That should concern every taxpayer.

The Question Nobody Asked

Reading the transcript, one question kept coming to mind.

Who actually knew?

If trustees did not know the identities of the underlying hedge funds, then someone certainly did.

Was it:

- investment staff?

- outside consultants?

- fund-of-funds managers?

- outside counsel?

Discovery should answer that question.

Because governance depends upon information.

A fiduciary cannot supervise investments whose identity remains hidden.

Judge Wingate’s Questions Point Toward a Larger Problem

One of the more interesting moments occurs when Judge Wingate essentially says he does not understand how one person’s settlement can dispose of broader claims. Later he reminds counsel that “you can’t settle tier three because of you all.”

Although the judge is addressing procedural issues, his comments reflect a broader concern.

Who owns these claims?

Who has authority over them?

And perhaps most importantly:

Who gets to know the facts before they disappear inside a settlement?

Those observations become especially important if discovery has not yet reached the underlying investments.

Discovery Is Key

The transcript reveals an enormous amount of legal energy devoted to procedural questions.

But discovery should continue well beyond those issues.

If this case proceeds, discovery should include:

- every underlying hedge fund held through each fund-of-funds

- all subscription agreements

- partnership agreements

- side letters

- quarterly reports

- redemption notices

- valuation reports

- consultant due diligence files

- fee schedules

- communications discussing confidentiality

Without those documents, no one can fully evaluate whether fiduciary duties were satisfied.

Who selected each underlying hedge fund?

Who removed managers?

Who negotiated fees?

Who approved side letters?

Who monitored liquidity?

Who received valuation reports?

Which trustees, if any, were allowed to review those materials?

Those answers would tell us far more about Kentucky’s hedge fund governance than another procedural hearing ever could.

Transparency Is the Missing Remedy

Judge Wingate spends much of the hearing trying to determine who has authority to settle claims and what legal vehicle should govern those settlements.

Those questions matter.

But there is another remedy the court should not overlook.

Transparency.

Discovery is not merely a litigation tool.

It is one of the few mechanisms capable of opening a black box that has remained closed for nearly two decades.

Fifteen Years Later, We Still Don’t Know

As a former trustee, I find it astonishing that fifteen years after I left the Board, the central transparency problem appears largely unchanged.

Back then, trustees were expected to oversee billions of dollars invested through hedge fund-of-funds without being permitted to identify all of the underlying managers.

Today, the litigation risks ending with another procedural ruling before those underlying investments ever become public.

That would be a missed opportunity.

The real value of this litigation is not simply deciding who has standing.

It is finally allowing beneficiaries, taxpayers, and fiduciaries to see what they have been paying for all along.

The Kentucky pension litigation should not end with another debate over procedure.

It should end with discovery that opens the hedge fund black box.