Updated 3/22/26

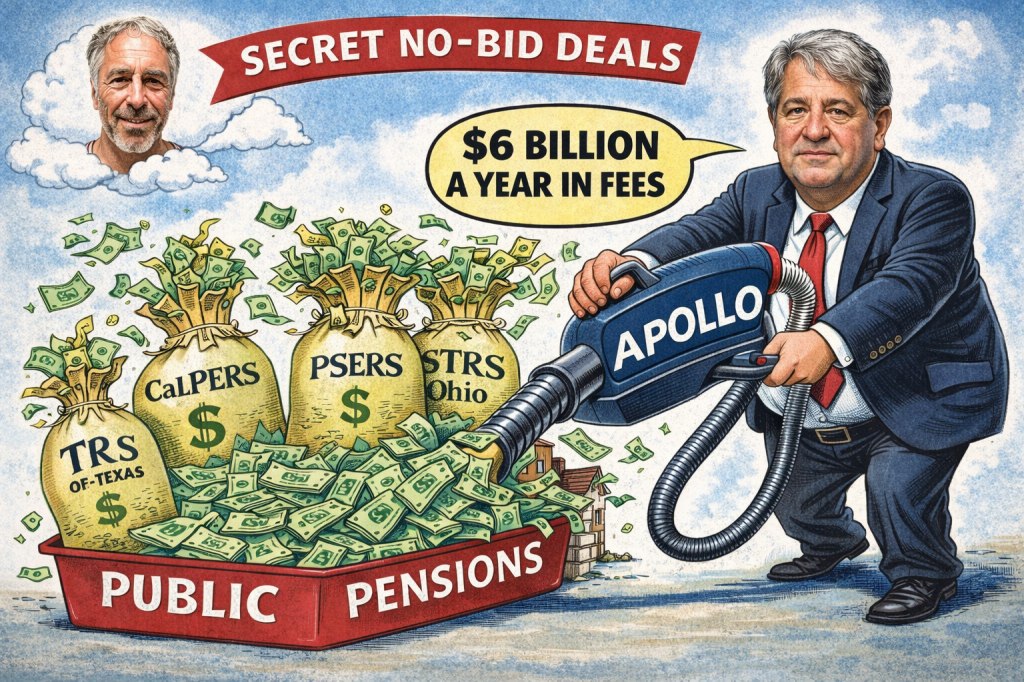

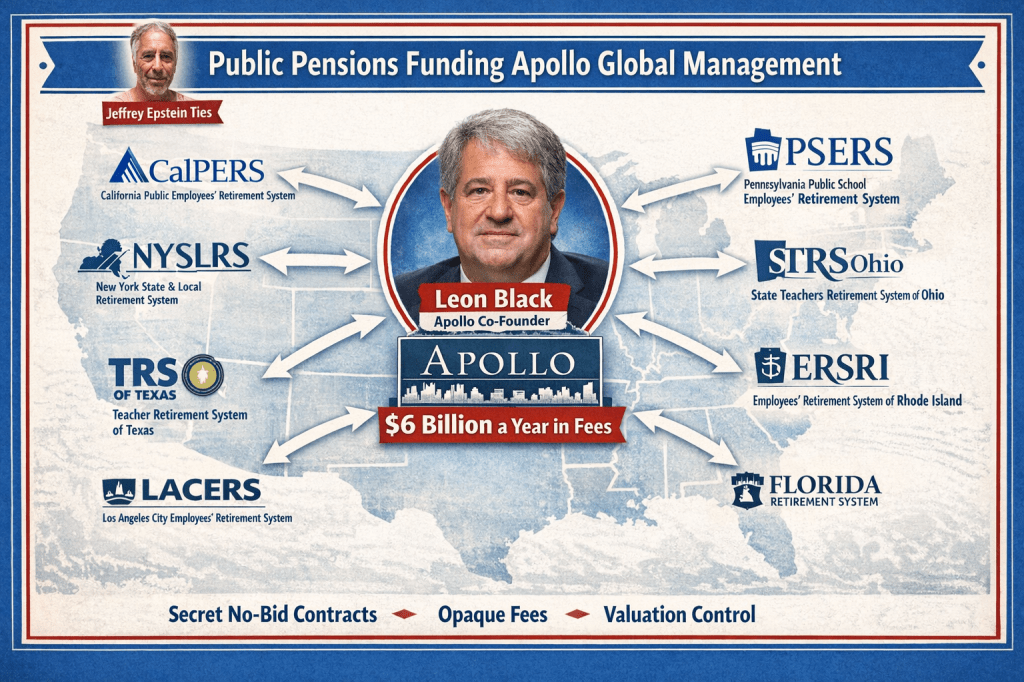

Public pensions across the United States may be paying as much as $6 billion a year to Apollo Global Management through a web of secret private equity and private credit contracts that most beneficiaries, taxpayers, and often even trustees themselves are never allowed to see. That estimate is not pulled out of thin air. It comes from combining two facts the industry would rather not discuss at the same time.

First, Apollo co-founder Joshua Harris admitted at a 2013 meeting of the Philadelphia Board of Pensions that the firm’s capital base was overwhelmingly dependent on public retirement systems. Asked directly whether Apollo had many public pension investors, Harris responded bluntly that “almost all” of Apollo’s capital came from public funds, estimating that roughly 75% to 80% of Apollo’s capital was supplied by public pension plans. https://www.phila.gov/pensions/PDF/IM_03_28_13_Investment_Minutes.pdf

Second, academic research by Oxford finance professor Ludovic Phalippou has repeatedly estimated that the true economic cost of private equity—including management fees, carried interest, transaction fees, monitoring fees, and portfolio-company charges—can reach 600 basis points annually, or roughly 6% of invested capital.

If public pension plans collectively have roughly $100 billion invested with Apollo, applying Phalippou’s cost estimate produces a staggering result: roughly $6 billion per year flowing from public retirement systems to one private equity firm. Even if the estimate is imprecise, the order of magnitude is the point. These are not marginal fees. They represent a massive transfer of retirement wealth from teachers, firefighters, public employees, and ultimately taxpayers to Wall Street managers operating under contracts that remain hidden from the public whose money is at stake.

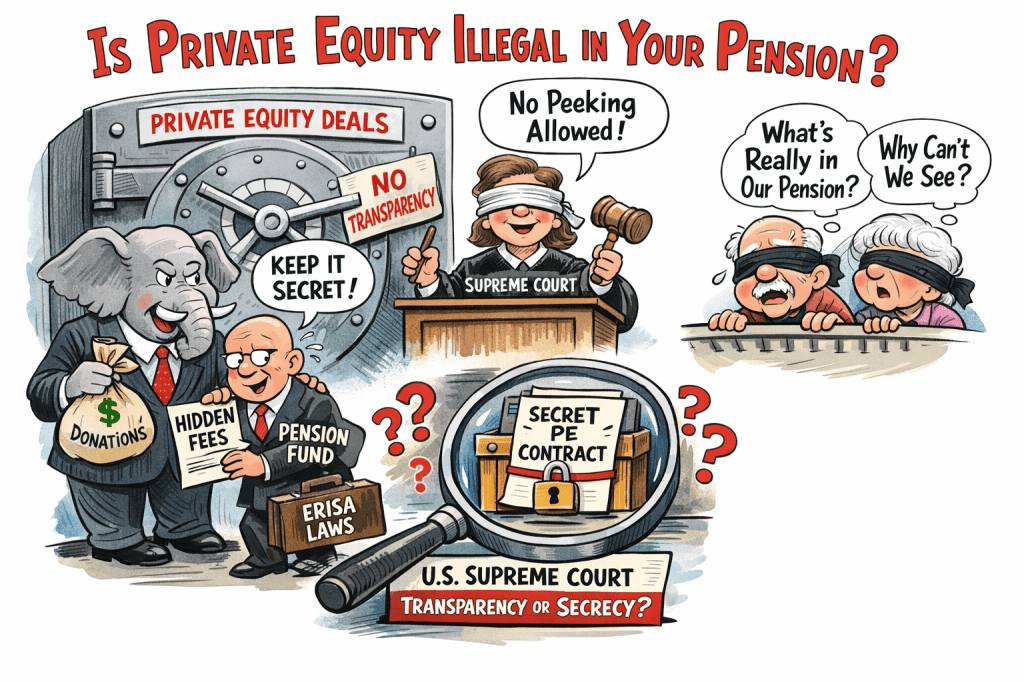

And those contracts raise serious legal questions. During my time as a trustee of the Kentucky Retirement Systems, I repeatedly asked to see the private equity partnership agreements governing these investments. Like many trustees across the country, I was told they were confidential. Trustees responsible for billions of dollars of public pension assets were effectively asked to approve investments whose governing legal documents could not be publicly disclosed.

Only through a rare discovery process during a federal investigation was I able to obtain a number of these contracts. In 2014 I provided eleven of them to Naked Capitalism’s trove archive, and around the same time, the Pennsylvania pension system accidentally disclosed twelve private equity agreements, including the Apollo Investment Fund VIII Limited Partnership Agreement. https://trove.nakedcapitalism.com/LPAs/verified-as-LPAs/Apollo_Investment_Fund_VIII_LPA_S1.pdf The industry response was immediate: the documents were quickly pulled down after Apollo became aware of the disclosure. Fortunately, the files were captured during a brief window and preserved.

Those documents revealed what public pension beneficiaries are normally forbidden to see.The Apollo contract shows a structure that places enormous power in the hands of the general partner while sharply limiting oversight by investors. Valuation authority rests largely with the manager itself. Broad indemnification provisions protect the firm from liability except in cases of extreme misconduct. The agreement allows Apollo to operate parallel vehicles and affiliated funds while maintaining discretion over allocations across them. So called Advisory boards exist but are mostly boondoggles to wine and dine pension staff so they keep their secrets. https://www.bloomberg.com/authors/AR2mdR8I6A4/neil-weinberg

In other words, the manager holds the authority, the protections, and the conflicts—while the pension system holds the capital and the risk. I believe this would be found to be illegal in many states. This structure is not accidental. It is precisely why the contracts must remain secret. Public pension funds are not private investors deploying personal wealth. They are public trust funds, governed by state constitutions, fiduciary statutes, and procurement rules designed to protect taxpayer resources. Trustees of these systems have a duty to act solely in the interest of beneficiaries and to manage funds prudently and transparently.

Yet private equity allocations frequently bypass the procurement safeguards that apply to almost every other form of public spending. Instead of competitive bidding or documented market comparisons, staff and consultants typically recommend a specific private equity fund and negotiate privately with the manager. The board is then presented with a take-it-or-leave-it opportunity framed as a limited investment window.

In effect, multi-billion-dollar investment mandates are awarded through secret no-bid contracts.

In any other context involving public funds—construction projects, infrastructure contracts, or technology procurement—such arrangements would immediately trigger investigations into favoritism or corruption. But in the world of private equity, this process has become routine.

The secrecy itself may conflict with state open-records laws and fiduciary obligations. Pension assets are public trust funds, and fiduciaries generally cannot bind those assets under contracts that prohibit disclosure of the governing terms. Yet private equity partnership agreements routinely contain confidentiality provisions preventing the public from seeing fee structures, conflict provisions, valuation policies, and indemnification clauses.

When beneficiaries cannot see the contracts governing their retirement money, meaningful accountability disappears.

The valuation provisions in these contracts are particularly troubling. Private equity managers typically retain substantial control over how portfolio assets are valued. Those valuations determine reported performance, and performance determines both carried interest and the ability to raise new funds. When the same party that profits from strong valuations also controls the valuation process, the conflict of interest is obvious.

Under traditional fiduciary law, trustees are expected to maintain independent oversight over the valuation of trust assets. Delegating that authority to a counterparty whose compensation depends on the outcome would normally raise serious red flags. Yet in private equity, that structure has become standard practice.

Broad indemnification provisions compound the problem. Many LPAs shield the general partner from liability except in cases of extreme misconduct, limiting investors’ ability to pursue claims even if negligent decisions damage the fund. Public pension trustees generally cannot waive legal protections on behalf of beneficiaries in this way without careful justification.

Taken together, the secrecy, valuation control, indemnification protections, and absence of competitive procurement raise the possibility that many private equity contracts are inconsistent with the fiduciary duties imposed on public pension trustees under state law. But even if the legal issues were ignored, another problem looms.

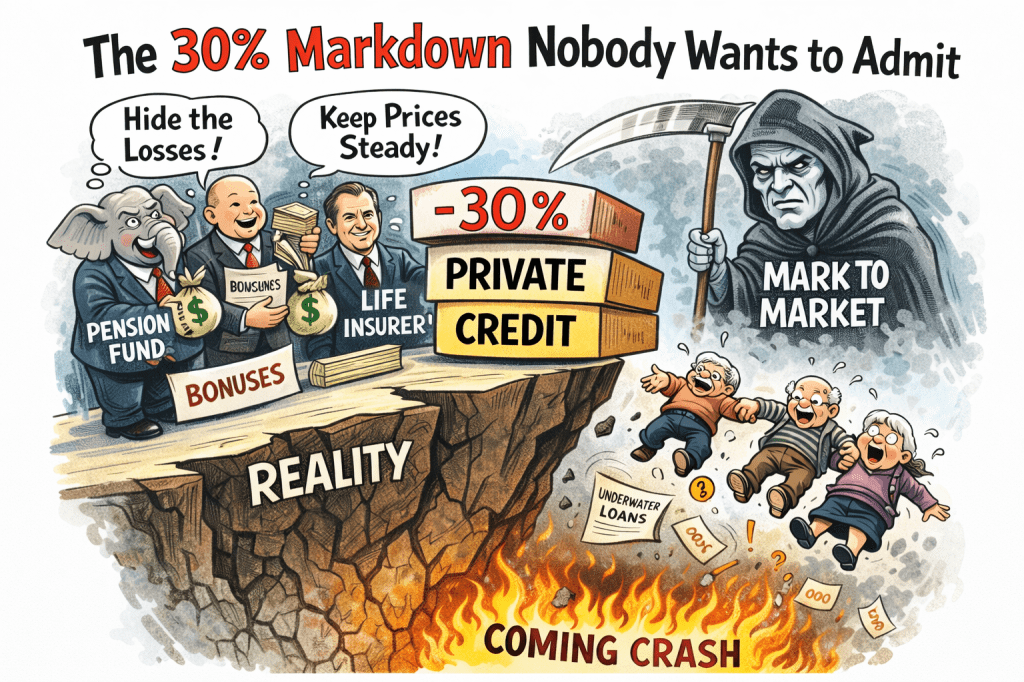

Public pension funds appear increasingly reluctant to confront the true value of their private equity and private credit portfolios. As markets tighten and private credit defaults rise, there is growing evidence that many assets may be significantly overvalued. If these holdings were forced into the open market today, they might clear at 70 cents on the dollar or less, revealing billions in hidden losses.

The consequences of acknowledging those losses would be enormous. Funding ratios would decline. Consultants’ performance claims would collapse. And pension staff—many earning $300,000 or more annually with bonuses tied to reported investment performance—could see compensation sharply reduced or even face clawbacks. The incentives to delay recognition of those losses are therefore powerful.

Many pension trustees are appointed by political officials. Those officials operate in a post-Citizens United political environment where private financial firms, including Apollo and their executives, can legally contribute vast sums to political organizations and super PACs secretly. Whether or not such contributions influence pension investment decisions, the appearance of conflict is impossible to ignore.

Apollo, via its debt control of Gannett, controls the main state media in many of the markets, especially state capitols of the below-mentioned Public Pension Plans, like the Columbus Dispatch, Tallahassee Democrat, Springfield (IL) State Journal, Austin American-Statesman. Indianapolis Star, Des Moines Register, Topeka Capital-Journal, Lansing State Journal, Jackson Clarion-Ledger, The Providence Journal.

The Epstein Apollo corruption machine is still operating strongly in Ohio, with the Attorney General going after Trustees trying to provide transparency around private equity, which would have exposed Apollo. https://commonsense401kproject.com/2026/02/23/epstein-apollo-and-ohio-teachers-billions/

Apollo was founded by Leon Black, whose relationship with convicted sex trafficker Jeffrey Epstein ultimately forced Black to step down as CEO after it was revealed that he had paid Epstein more than $150 million for financial services. This caused serious divestiture talks in 2019 and 2020 that CEO Marc Rowan calmed by saying Epstein’s involvement was limited to Leon Black personally and that it was for tax advice. New Epstein files released in February 2026 document that Rowan was lying and that his and Apollos’ involvement with Epstein was extensive. The Teachers Unions AFT and AAUP have filed a complaint with the SEC and a civil class action has been filed against Apollo for lying about its Epstein involvement. www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf

and covered on CNN https://www.cnn.com/2026/02/21/business/apollo-epstein-wall-street?

AFL-CIO going after Epstein linked Apollo on workers rights violations

Apollo has long history of fines from SEC and other Federal Agencies https://commonsense401kproject.com/2026/02/25/the-leon-black-culture-of-corruption-at-apollo-plans-should-divest/

Divest from Apollo.

Not because private equity is inherently illegitimate, and not because every Apollo investment has failed. But because fiduciaries cannot responsibly commit public retirement assets to opaque, no-bid contracts that place enormous power in the hands of private managers while denying transparency to the public whose money is at stake. Apollos recent issues around Epstein strain their credibility as a manager of public funds. https://commonsense401kproject.com/2026/02/05/the-apollo-epstein-files-why-public-pensions-should-reopen-the-2019-divestment-debate/

The longer pensions remain entangled in this system, the greater the risk that hidden losses, undisclosed conflicts, and legal challenges will eventually surface. When that day comes, retirees and taxpayers will ask a very simple question:

Why did no one act sooner?

A partial list of over 58 pensions that hold Apollo is below.

Alaska Permanent Fund Apollo PE funds

Arizona PSPRS Apollo PE funds

California Public Employees’ Retirement System (CalPERS) Apollo Investment Fund VI and related vehicles

California State Teachers’ Retirement System (CalSTRS) Apollo Investment Funds VI, VII, IX, X; Hybrid Value II

Chicago Teachers Pension Fund 2024 performance confirms Apollo PE/PC as manager

Colorado PERA Apollo Investment Funds III,IV,V,VI, VII, Distresssed DIF

Colorado School Apollo Credit Opp III & DIF

Connecticut Retirement Plans & Trust Funds Apollo Investment Fund VIII

Florida State Board of Administration Apollo PE funds IV, V PC Accord V and VI

Georgia Teachers Retirement System

Idaho PERSI Apollo PE funds

Illinois Teachers Retirement System Apollo PE funds X

Illinois Municipal Apollo Credit Wilshire

Indiana Public Retirement System (INPRS) Apollo Origination Partnership

Iowa Public Employees Retirement System Apollo PE funds Wilshire

Kansas Public Employees Retirement System Apollo PE funds VIII,IX

Kentucky Teachers Apollo REIT & Apollo Stock

Los Angeles City Employees’ Retirement System (LACERS) Apollo PE funds VI

Los Angeles (CA) Water and Power has PE fund X

Louisiana Teachers’ Retirement System of Louisiana (TRSL), Apollo Credit, Natural Resources

Maryland State Retirement & Pension System ?PE funs

Massachusetts PRIM Apollo PE funds

Michigan RS Apollo Investment fund VIII, IX Hybrid Value Funds, Credit/ Opportunistic Credit

Minnesota State Board of Investment Apollo/Athene Dedicated Investment Program II

Mississippi PRS Apollo VIII IX Private Equity funds

Montana Board of Investments Stock holdings?

Nebraska Investment Council India Property Fund II LLC.

New Hampshire Retirement System Apollo PE funds

New Jersey Division of Investment: Stock holdings?

New Mexico State Investment Council Apollo PE VII, VIII PC

New York City Teachers’ Retirement System Apollo PE funds

New York City (NY) ERS PE $500mm 2013

New York City (NY) Police PE fund VI

New York State Apollo PE VIII

North Carolina Retirement Systems Apollo PE funds VI, VII

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Oregon PER recently comitted $300mm to Apollo distressed debt fund as well as earlier funds like Apollo PE IX

Pennsylvania PSERS Apollo PE funds IV $620mm

Pennsylvania SERS Apollo PE funds VI- VIII

Rhode Island Retirement System Apollo PE VIII, IX

San Diego City Employees Retirement System Apollo PE funds

San Francisco (SFERS) San Francisco Employees’ Retirement System Apollo PE funds Wilshire

South Carolina RS $750mm

South Dakota Retirement System Apollo PE funds

Texas County & District PE fund X

Texas ERS Apollo Credit Strategies

Texas Municipal Fund VIII

Texas TRS Teachers’ Retirement Apollo PE funds

Tennessee Consolidated Retirement System Stock holdings?

San Francisco Employees’ Retirement System Apollo PE funds

San Diego City Employees’ Retirement System Apollo PE funds

University of Calfiornia PE VII, VIII Principal Wilshire

Virginia Retirement System Apollo PE funds

Washington State Investment Board (WSIB) Apollo S3 Equity & Hybrid

Wisconsin (SWIB) Apollo Credit

Apollo also involved in data centers https://commonsense401kproject.com/2026/03/09/why-public-pensions-should-divest-from-apollo-data-centers/

AG Bondi puts Apollo xChair in charge of Epstein file Redactions – How many files with Apollo and disgraced founder Leon Black did he redact? https://commonsense401kproject.com/2026/03/12/jeffrey-epstein-funder-leon-blacks-apollo-still-thinks-they-are-above-the-law/