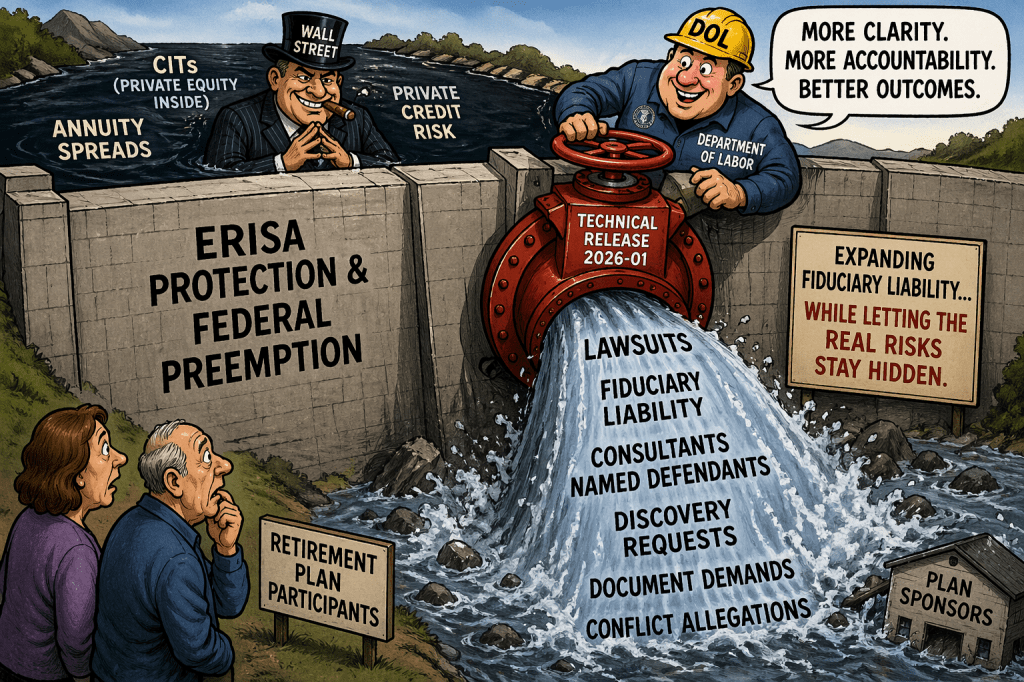

The U.S. Department of Labor’s latest guidance—Technical Release 2026-01—has been framed as a narrow clarification on proxy voting. https://www.dol.gov/agencies/ebsa/employers-and-advisers/guidance/technical-releases/26-01 That is not what it is.

It is something far more consequential:

- A major expansion of fiduciary status – mostly for consultants

- A political intervention into ESG and proxy voting

- And, most troubling, a quiet weakening of ERISA’s federal protections by deferring to weak state regulatory regimes on annuities and CIT’s

While it is great for Wall Street and the Insurance industry it is bad for participants and plans. Taken together, this release does not reduce litigation risk for plan sponsors. It guarantees more of it.

1. The Real Headline: Consultants Are Now Fiduciaries (Whether They Like It or Not)

The DOL makes one point unmistakably clear:

If you influence proxy voting, you are likely a fiduciary.

Under Employee Retirement Income Security Act of 1974, fiduciary status is functional—not based on titles or disclaimers. The DOL doubles down on that principle:

- Control over proxy voting = control over plan assets

- Advice on proxy voting for a fee = fiduciary investment advice

- Disclaimers “are not determinative”

This is not just about proxy advisory firms like ISS or Glass Lewis.

It directly implicates:

- Investment consultants designing proxy policies

- OCIO providers implementing governance frameworks

- Advisors influencing ESG or stewardship decisions

In practice, firms that have long operated in a gray zone—collecting fees while avoiding fiduciary responsibility—are now exposed. And with more consultants being secretly owned by Private Equity, the exposure increases.

And once you are a fiduciary, you are also a party in interest.

That is where the litigation begins.

2. The Political Overlay: ESG Is the Target, Not the Rule

The release is tied directly to executive branch policy and makes repeated references to:

- “Non-financial” considerations

- “Politically motivated” proxy voting

- The need to focus solely on risk-adjusted return

This is not neutral guidance. It is a federal attempt to reshape proxy behavior without formal rulemaking.

The practical effect:

- ESG-related proxy votes become legally risky

- Documentation burdens increase dramatically

- Plaintiffs’ attorneys gain a roadmap to challenge votes

Ironically, in trying to suppress ESG influence, the DOL has created a new litigation framework around proxy decision-making.

3. The Most Dangerous Move: Weakening ERISA Preemption

Buried in the release is a far more consequential shift—one that has nothing to do with proxy voting.

The DOL argues that certain state laws regulating proxy advice are not preempted by ERISA, because:

A prudent ERISA fiduciary would never engage in the conduct those laws regulate.

This sounds harmless. It is not.

It represents a fundamental change in ERISA preemption doctrine.

Traditional ERISA Preemption

For decades, ERISA has operated on a simple premise:

- Federal law governs employee benefit plans

- State laws that “relate to” plans are broadly preempted

- The goal is national uniformity and participant protection

DOL’s New Framework

The DOL now suggests:

- State laws can coexist with ERISA

- As long as fiduciaries theoretically avoid triggering them

This creates a dual system:

- Strict federal duties (on paper)

- Weak, fragmented state regulation (in practice)

4. Why This Matters: Annuities and CITs

This is where the release intersects directly with the biggest risks in the retirement system.

A. Annuities

Insurance products—especially general account annuities—are governed primarily by state law.

Those laws:

- Do not require full transparency of spreads

- Allow discretionary crediting rates

- Often obscure underlying asset risk (private credit, mortgages, etc.)

Under the DOL’s logic:

- ERISA fiduciaries should act prudently

- Therefore weak state regulation is “good enough”

This is a dangerous fiction.

It effectively allows:

- Hidden insurer profits

- Undisclosed credit risk

- Single-entity exposure fixed annuities masquerading as “stable value”

B. Collective Investment Trusts (CITs)

The same issue exists—arguably worse—with CITs.

Regulated by:

- State banking authorities (e.g., Pennsylvania, New Hampshire, Maryland)

- The Office of the Comptroller of the Currency in some cases

These structures:

- Avoid U.S. Securities and Exchange Commission disclosure requirements

- Frequently embed:

- Private equity

- Private credit

- Annuities and other Insurance products

Participants often have no idea what they own.

Again, the DOL’s position implies:

- ERISA fiduciaries should investigate these structures

- Therefore weak state oversight is acceptable

That is not regulation. That is abdication.

5. The Internal Contradiction: More Fiduciaries, Less Protection

This is the core problem.

The DOL is simultaneously:

Expanding fiduciary status

- More actors subject to ERISA

- More potential defendants

While weakening federal oversight

- Allowing state regimes to stand

- Accepting opacity in key investment structures

This creates the worst of both worlds:

- More liability

- Less transparency

6. Litigation Implications: A Plaintiff’s Roadmap

For those paying attention, this release is not a shield—it is a weapon.

It supports arguments that:

1. Consultants are fiduciaries

- Especially where they influence governance or structure

2. Advisory relationships trigger prohibited transaction scrutiny

- Fees + influence = conflicts

3. Discovery should expand

- Into proxy processes

- Into CIT underlying assets

- Into annuity crediting mechanisms

The logic aligns directly with Cunningham v. Cornell:

- Defendants bear the burden of proving exemptions

- Plaintiffs are entitled to discovery into hidden arrangements

7. The Bigger Picture: A Gift to Wall Street, Not Plan Sponsors

The DOL claims this guidance will reduce confusion and protect plans.

In reality, it does the opposite.

It:

- Expands fiduciary liability to more actors especially consultants

- Encourages reliance on opaque investment structures

- Preserves weak state regulatory frameworks

- Increases litigation exposure for plan sponsors

Meanwhile:

- Insurance companies continue to hide spreads

- Private equity remains embedded in CITs without disclosure

- Consultants collect fees while navigating newly expanded liability

Conclusion: More Risk, More Opacity, More Litigation

Technical Release 2026-01 is not a minor clarification.

It is a structural shift.

- It expands who can be sued

- While weakening the regulatory foundation meant to protect participants

And in doing so, it reinforces a troubling reality:

The modern retirement system is increasingly built on opaque structures, weak oversight, and conflicted intermediaries—with participants bearing the risk.