Kentucky is quietly becoming a new battleground in the national data center arms race It’s about tax breaks, hidden subsidies, and who is really paying the bill.

At the center of this push: state legislative leadership, electric utilities, and institutional capital—including public pensions chasing “infrastructure” returns.

The Legislative Playbook: Last-Minute Deals and Massive Subsidies

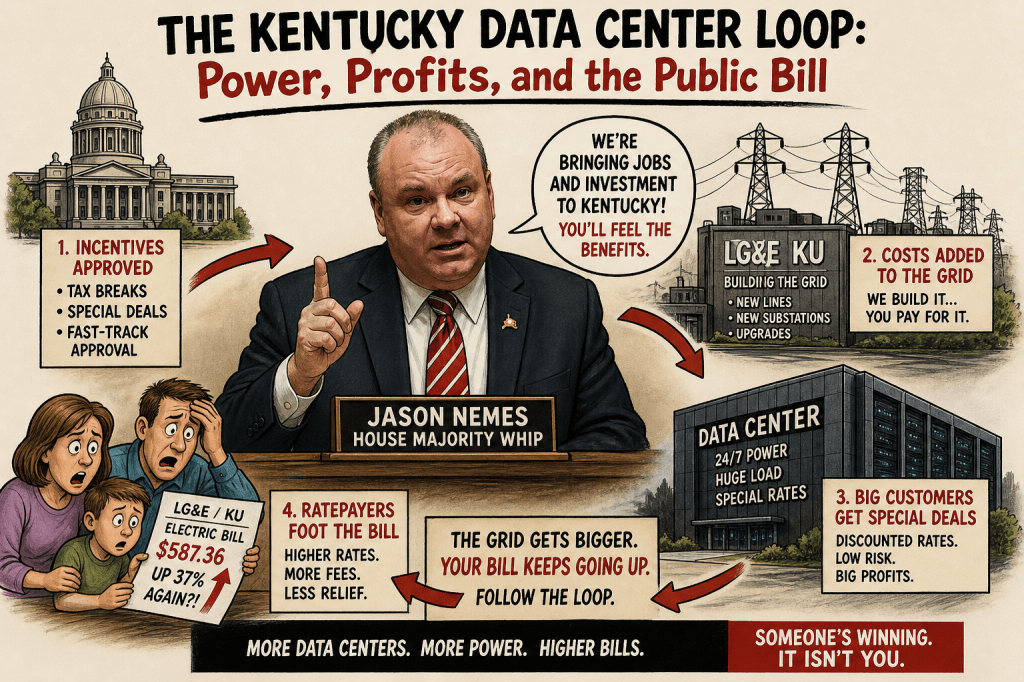

Start with Jason Nemes—House Majority Whip.

What happened in Kentucky is a textbook case of how major economic policy gets made:

- 2024–2025 bills (HB 8, HB 775) were initially unrelated to data centers

- Then—on the final day of the session—hundreds of pages were added

- Buried inside: sweeping data center tax breaks across all 120 counties

Even more striking:

- Sales tax exemptions on equipment can run 25–50 years

- Incentives mirror national trends where states compete in a race-to-the-bottom subsidy war

This isn’t normal policymaking. It’s legislative arbitrage—exactly the same playbook you’ve documented in private equity and annuities.

The Political Network: It’s Not Just Nemes

Nemes didn’t act alone. The push reflects coordinated leadership across Kentucky’s GOP supermajority:

- Robert Stivers

- Publicly pushed Kentucky to become a data center/AI hub

- David Osborne

- Represents areas targeted for data center siting

- Josh Bray & Steven Rudy

- Sponsors of enabling legislation

Even more revealing:

- Bills were shaped with input from utilities and corporate lobbyists

- Tech companies like Google and Meta lobbied to expand incentives

And at the federal level:

- Thomas Massie has warned that federal policy could strip local control over data center siting, enabling large-scale projects with minimal oversight

The Hidden Cost: Ratepayers and Communities

Kentucky lawmakers are now scrambling to deal with the consequences of what they passed:

- New bills aim to prevent data centers from shifting infrastructure costs onto ratepayers

- Concerns include:

- Massive electricity demand

- Water usage

- Grid upgrades paid by the public

This mirrors what’s happening nationally:

- Data centers are now a top-tier political issue across multiple states

- Voters are pushing back over utility costs and environmental impact

In Oldham County:

- A hyperscale project sparked local backlash and a moratorium

- Estimated:

- ~4,000 construction jobs

- But only ~176 permanent jobs

That’s the classic economic development tradeoff:

Huge subsidies → minimal employment → long-term infrastructure burden

The Real Driver: Electricity + Financial Engineering

Data centers don’t go where innovation is.

They go where:

- Power is cheap

- Regulation is weak

- Subsidies are large

- Land is available

Kentucky checks all four boxes.

But here’s the part most political coverage misses:

👉 Data centers are fundamentally an energy arbitrage trade

- Utilities build infrastructure

- States subsidize capital costs

- Operators lock in long-term power access

- Investors harvest stable, utility-like returns

Sound familiar?

It’s the same model as:

- Private credit

- Infrastructure funds

- Insurance general accounts

Where Pensions Come In

exposed through:

A. Infrastructure Funds

- Blackstone (digital infrastructure + data centers)

- Brookfield Asset Management

- Digital Realty

B. Private Equity / Private Credit

- Financing:

- Data center construction

- Power infrastructure

- Fiber networks

C. Real Estate (REITs and private vehicles)

- Hyperscale campuses treated as “core real estate”

The Kentucky Twist: Utilities + Politics + Pensions

Kentucky may be one of the clearest examples in the country of alignment between:

- Legislators → pass last-minute incentives

- Utilities (e.g., LG&E) → benefit from massive load growth

- Data center developers → lock in subsidized infrastructure

- Institutional investors (pensions) → supply capital

The result:

A closed-loop system where taxpayers subsidize infrastructure,

ratepayers fund expansion, and pensions book the returns.

“Kentucky didn’t just invite data centers—it rewrote the rules at the last minute to subsidize them.

The same public pensions chasing returns from these projects are the ones whose participants will pay higher utility bills to support them.

That’s financial engineering—funded by the public, for the benefit of private capital.”

- The Teachers’ Retirement System of the State of Kentucky

committed $100 million directly into a data center fund (TA Digital)

Both major Kentucky systems—TRS and KPPA—have long-standing relationships with:

- Blackstone Inc.

- KKR & Co.

- Private equity firms including Blackstone and KKR are aggressively investing in data center infrastructure globally

- KKR alone has committed billions to data center platforms (e.g., Global Technical Realty)

Blackstone:Owns and finances hyperscale data center platforms globally

Kentucky teachers’ pensions are already investing directly in data centers, while state legislators are subsidizing those same projects.

At the same time, Kentucky’s other pension system is deeply tied to Blackstone and KKR—two of the largest global owners of data centers.

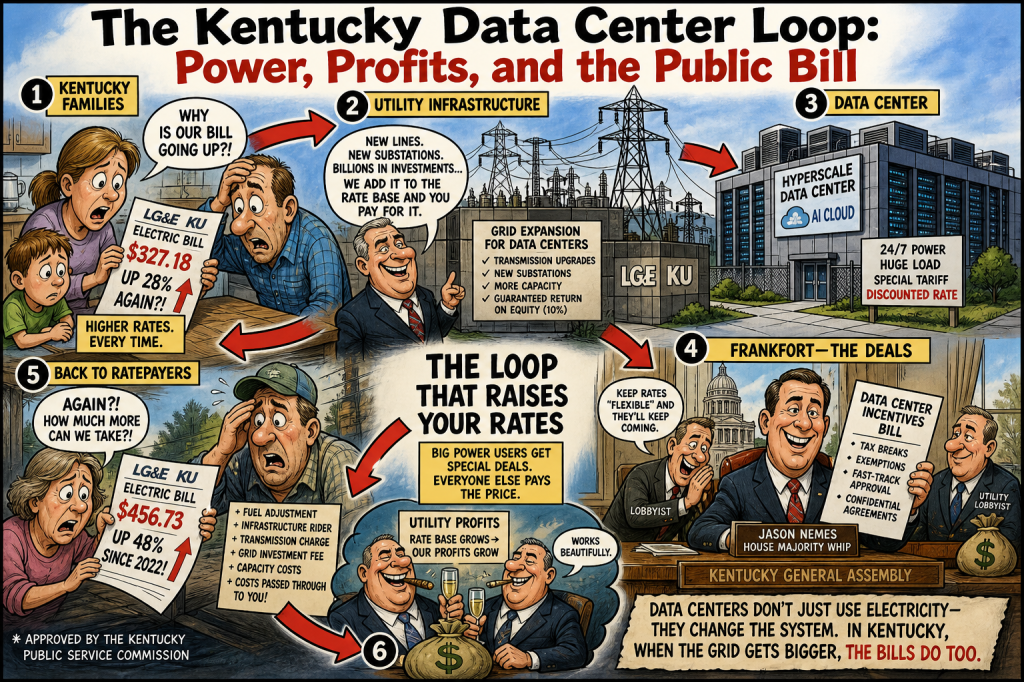

How Data Centers Can Raise Utility Prices in Kentucky (LG&E & KU)

1. The Basic Reality: Data Centers Are Massive, Continuous Power Loads

A single hyperscale campus can demand 100–400+ megawatts—comparable to a small city.

Unlike factories, this demand is:

- 24/7 (no off-peak relief)

- Highly concentrated geographically

- Growing rapidly with AI workloads

That forces utilities like Louisville Gas and Electric and Kentucky Utilities to build dedicated infrastructure, often on tight timelines.

2. The Cost Stack: What Has to Be Built

To serve one large data center cluster, LG&E/KU may need:

- New high-voltage transmission lines

- New substations

- Transformer capacity upgrades

- Grid reinforcement across regions

- In some cases: new generation capacity

These are multi-hundred-million to multi-billion dollar investments.

3. The Critical Issue: Who Pays for That Infrastructure?

Utilities recover costs through regulated rate structures approved by the Kentucky Public Service Commission.

In theory:

- The data center should pay for its incremental costs

In practice:

- Costs often get socialized across all customers

This happens through:

A. Rate Base Expansion

- Infrastructure is added to the utility’s “rate base”

- Utilities earn a guaranteed return (e.g., 9–10%)

- That return is collected from all ratepayers

👉 Translation:

Even if a data center is the reason for the build, everyone pays

B. Demand Risk Shifting

If a data center:

- Delays construction

- Scales back

- Or exits

The infrastructure remains—and:

Residential and small business customers absorb the stranded costs

C. Special Contracts & Discounts

To attract data centers, states often allow:

- Discounted electricity rates

- Tax exemptions on energy use

- Long-term fixed pricing deals

Result:

Revenue shortfalls are made up elsewhere in the rate structure

6. The Hidden Driver: Load Growth Sounds Good—But Isn’t Always

Utilities often argue:

“Large customers help spread fixed costs and lower rates”

That can be true only if:

- The data center pays full cost

- Demand is stable

- Infrastructure is efficiently utilized

But with hyperscale centers:

- Buildouts are lumpy and oversized

- Timing mismatches create unused capacity

- AI demand is uncertain and cyclical

👉 Result: Overbuild risk → higher rates

7. National Evidence (What’s Happening Elsewhere)

Across multiple states:

- Data center demand is driving rate cases and price increases

- Regulators are beginning to push back on:

- Cost shifting

- Special tariffs

- Subsidized infrastructure

Kentucky is now entering that same phase—with legislation already being discussed to protect ratepayers from these costs.

“Data centers don’t just consume electricity—they reshape the entire cost structure of the grid.

In Kentucky, utilities build billions in infrastructure to serve a handful of hyperscale customers, and those costs don’t stay isolated—they flow through the rate base to every household and small business.