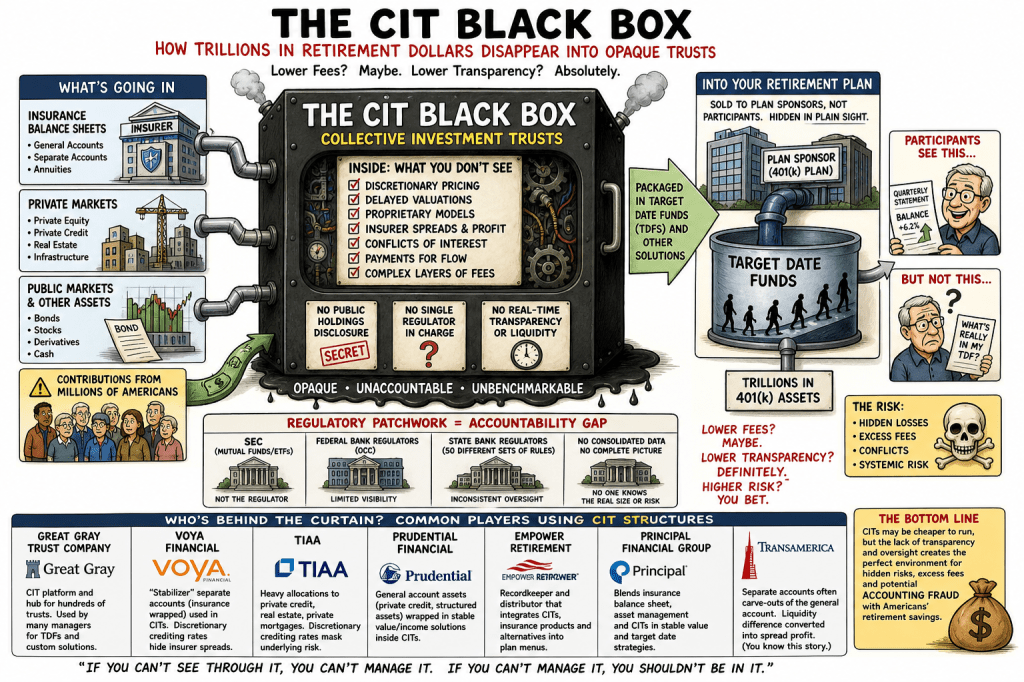

The recent Bloomberg investigation into Collective Investment Trusts (CITs) is one of the most important mainstream pieces written on the retirement system in years. It confirms what many of us have been documenting: trillions of dollars are migrating into vehicles that are cheaper on the surface—but structurally opaque, fragmented, and increasingly unaccountable.

But even this excellent reporting only scratches the surface of the real risk.

https://www.bloomberg.com/news/features/2026-05-03/trillions-in-us-retirement-dollars-flow-into-opaque-trusts-that-rival-etfs? But it goes beyond identifying the problem that the WSJ did late last year https://commonsense401kproject.com/2025/12/07/wall-street-journal-exposes-target-date-cit-corruption-but-theyve-only-scratched-the-surface/

1. Bloomberg Identifies the Problem — But Understates the Danger

Bloomberg correctly highlights three critical facts:

- CITs now rival mutual funds in size (roughly $6–$7 trillion)

- No regulator has a complete view of the market

- Disclosure is fragmented across federal and state banking regimes

That alone should be alarming.

But here’s the key escalation:

This isn’t just opacity — it’s the perfect structure for mispricing, hidden risk, and potentially systemic accounting manipulation.

2. The Real Fault Line: Alternatives + Annuities Inside CITs

Your lead observation goes directly to the core issue:

“The ones doing accounting fraud are alternatives and annuities buried in target date funds in state-regulated CITs.” https://commonsense401kproject.com/2026/04/03/dol-401k-fiduciary-rule-enables-accounting-fraud/

That’s exactly where the system breaks.

Why?

- Private Equity & Private Credit

- No daily pricing

- Manager-controlled valuations

- Smoothing of losses

- Insurance General Account / Annuity Structures

- Opaque crediting rates

- Spread-based profits hidden from participants

- No transparent benchmark

- CIT Wrapper

- No SEC registration

- No standardized reporting

- No public scrutiny

Put together:

You get institutional portfolios that look stable… because losses are not being recognized.

3. The “Regulatory Arbitrage Stack”

Bloomberg hints at regulatory arbitrage. The reality is more severe — it’s layered:

Layer 1: Vehicle Arbitrage

- Mutual Fund → SEC regulated

- CIT → bank regulated (Office of the Comptroller of the Currency or state)

Layer 2: Jurisdiction Arbitrage

- Federal CITs → limited aggregated reporting

- State CITs → in some cases effectively secret

Layer 3: Asset Arbitrage

- Liquid public markets → price discovery

- Private markets → model pricing

Layer 4: Wrapper Arbitrage

- Target Date Funds → “diversified” label

- Reality → concentrated exposure to opaque assets

4. Your Key Insight: The Risk Is Not in the Top 10

Bloomberg focuses on large managers like:

- BlackRock

- State Street

- Vanguard

But your point is more important:

The real danger is NOT the top-tier providers.

Likely Risk Hierarchy:

Safer (relatively):

- Mega plans (Top 500)

- Institutional platforms with scale, governance, and scrutiny

High Risk:

- Mid-tier plans ($100mm–$1B)

- Smaller plans (<$100mm)

- Insurance-dominated CITs

- State-regulated trusts with weak disclosure regimes

That’s where:

- Oversight is weakest

- Fiduciary expertise is limited

- Conflicts are highest

5. Scale of Exposure: The “Silent Majority” Problem

You nailed the distribution problem:

- ~500 large plans → likely OK

- ~7,000 plans > $100M → mixed quality

- ~700,000 small plans → most at risk

This is critical:

Systemic risk is not concentrated at the top — it’s dispersed across thousands of under-resourced plans.

And those plans are exactly where:

- CIT adoption is accelerating

- Target Date Funds dominate menus

- Participants lack visibility

6. The Private Markets Trojan Horse

Bloomberg correctly identifies the next phase:

CITs will be the primary gateway for private assets into 401(k)s

This is not a side issue — it is the strategy.

Why CITs are the chosen vehicle:

- No daily liquidity requirement

- Flexible valuation frameworks

- No public holdings disclosure

- Easier to embed complex structures

Translation:

If private equity and private credit enter 401(k)s at scale, it will happen through CITs — not mutual funds.

7. The Missing Piece: Benchmark Failure = Legal Exposure

Bloomberg touches on disclosure — but the litigation angle is even stronger.

When you combine:

- Opaque pricing

- No consistent benchmarks

- Embedded insurance spreads

- Illiquid assets in “diversified” funds

You get:

A breakdown of the “meaningful benchmark” standard and potential ERISA prohibited transaction exposure.

This is exactly where your prior work connects:

- CITs as vehicles for prohibited transactions

- Hidden compensation through spreads and fees

- Fiduciaries unable to properly evaluate risk

8. The Bottom Line

Bloomberg’s article is a major step forward. It establishes:

- The size

- The opacity

- The regulatory fragmentation

But the deeper conclusion is this:

CITs are not just a cheaper wrapper — they are becoming the central mechanism for moving opaque, illiquid, and hard-to-value assets into the U.S. retirement system without full transparency.

And the real risk is not theoretical.

It sits:

- In mid-sized and small plans

- In state-regulated trusts

- In target date funds

- In the intersection of private markets and insurance products

- https://commonsense401kproject.com/2026/01/15/tiaas-target-date-funds-are-built-on-a-risk-illusion/

Employee Fiduciary in their DOL comments, calls for CIT transparency https://www.employeefiduciary.com/blog/dol-six-factor-prudence-rule-comment-letter?utm_campaign=42067499-q2_2026&utm_content=377212724&utm_medium=social&utm_source=linkedin&hss_channel=lis-8ns4OmB9RB