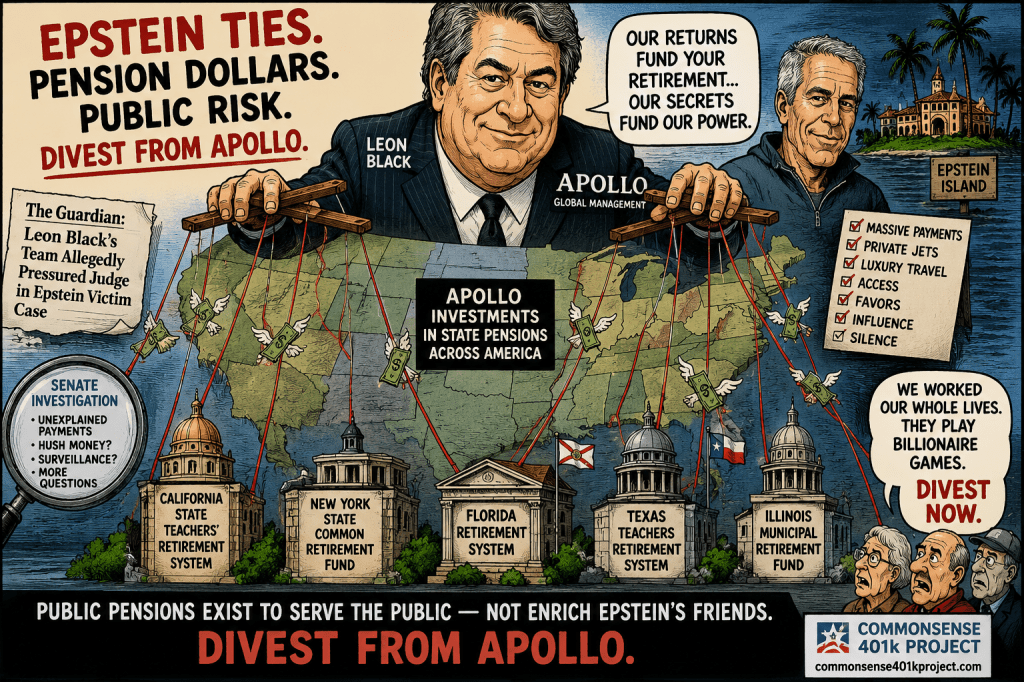

The case for public pensions to divest from Apollo Global Management because of its ties to Leon Black and Jeffrey Epstein just became substantially stronger.

For years, defenders of Apollo have argued that the Epstein controversy was old news. Black resigned as CEO in 2021. Apollo moved on. Investors should move on too.

But the new Guardian investigation published this week shows the scandal is not over. It is still evolving. New allegations, new reporting, new legal controversies, and new scrutiny continue to emerge years after Black supposedly separated himself from the firm. The article transforms this from a “historical reputational issue” into an ongoing governance and fiduciary problem for every pension system still invested with Apollo. https://www.theguardian.com/us-news/ng-interactive/2026/may/06/jeffrey-epstein-leon-black

The Guardian reports allegations that Black’s legal team privately communicated with a federal judge in connection with efforts to undermine an Epstein victim’s compensation award. Whether or not additional legal findings ultimately emerge, the significance for pension fiduciaries is obvious: the controversy surrounding Apollo’s founder is not fading away. It is expanding.

The issue is no longer simply that Black paid Epstein enormous sums after Epstein was already a convicted sex offender. The issue is that new layers of the story continue unfolding years later, creating continuing reputational, legal, and financial risks for institutional investors tied to Apollo.

That matters enormously for public pensions.

State pension systems routinely lecture corporations about governance, ethics, ESG, transparency, and reputational risk. Many have divested from tobacco, firearms, fossil fuels, Russia, Sudan, and private prisons. Yet these same pension systems continue allocating billions to Apollo while a growing stream of investigations, shareholder litigation, Senate inquiries, survivor allegations, and media exposés continue to surround the firm’s founding leadership.

At some point fiduciaries must explain why ESG principles apply to oil pipelines in Texas but apparently do not apply to relationships tied to Jeffrey Epstein.

The Guardian article also reinforces the credibility of Senator Ron Wyden and his ongoing investigation into Leon Black’s payments and relationships tied to Epstein. Wyden has already raised questions involving possible hush-money arrangements, surveillance activities, and unexplained financial flows connected to Epstein’s operations. https://www.finance.senate.gov/imo/media/doc/wyden_letter_to_doj-treasury-fbi_on_epsteinpdf.pdf

The complaint to the SEC from the AFT and AAUP on Apollo lying about Marc Rowan and more involved ties with Epstein is still outstanding. https://www.aft.org/sites/default/files/media/documents/2026/Letter_to_SEC_re_Apollo_Global_Management_February_17_2026.pdf

The Guardian investigation now adds another layer of scrutiny involving alleged legal pressure tactics and continuing litigation involving Epstein victims.

Public pensions can no longer dismiss this as a fringe activist concern or isolated media sensationalism. The concerns now involve:

- U.S. Senate investigations

- shareholder lawsuits

- SEC pressure from major unions

- continuing victim litigation

- repeated major-media investigations

- expanding reputational fallout

This becomes especially important because Apollo is not merely another Wall Street manager. Apollo is deeply embedded throughout the U.S. public pension system. Many pension systems have allocated billions into Apollo private equity, private credit, real estate, infrastructure, insurance-related products, and Athene-connected strategies. In many cases these same pension systems simultaneously proclaim commitments to governance oversight and stakeholder responsibility.

The contradiction is becoming impossible to ignore.

The financial implications are also growing. Apollo already faces stock-drop litigation connected to allegations that investors were not fully informed about Epstein-related risks. Continued investigations increase the possibility of additional litigation, regulatory scrutiny, fundraising pressure, and institutional backlash.

This is no longer simply an ethical issue. It is a material risk-management issue.

Institutional investors constantly claim that governance failures can create long-term financial damage. If pension systems truly believe that principle, then Apollo deserves heightened scrutiny. Governance risk is investment risk.

The Guardian story also undermines perhaps the most common defense used by Apollo supporters: that Leon Black is no longer CEO and therefore the issue is resolved.

That argument becomes weaker every month. Black remains inseparable from Apollo’s history, culture, and identity. Apollo’s rise was built under his leadership. The continuing revelations surrounding Epstein repeatedly pull Apollo back into the story regardless of formal titles or organizational charts.

The broader danger for pensions is that they are beginning to look selective and hypocritical in how they apply fiduciary standards. Pension systems aggressively police reputational risk when politically convenient, but appear far more tolerant when the investments involve elite private equity firms generating lucrative relationships, consultant fees, political access, and headline return numbers.

That double standard is becoming increasingly visible.

For pension trustees, the question is becoming straightforward:

How many more investigations, lawsuits, Senate inquiries, media exposés, and victim allegations must emerge before Apollo’s Epstein ties are finally considered a material fiduciary concern?

Because if this does not qualify as a governance red flag, it is difficult to imagine what possibly would.

List of Plans with Apollo Funds

Alaska Permanent Fund Apollo PE funds

Arizona PSPRS Apollo PE funds

California Public Employees’ Retirement System (CalPERS) Apollo Investment Fund VI and related vehicles

California State Teachers’ Retirement System (CalSTRS) Apollo Investment Funds VI, VII, IX, X; Hybrid Value II

Chicago Teachers Pension Fund 2024 performance confirms Apollo PE/PC as manager

Colorado PERA Apollo Investment Funds III,IV,V,VI, VII, Distresssed DIF

Colorado School Apollo Credit Opp III & DIF

Connecticut Retirement Plans & Trust Funds Apollo Investment Fund VIII

Florida State Board of Administration Apollo PE funds IV, V PC Accord V and VI

Georgia Teachers Retirement System

Idaho PERSI Apollo PE funds

Illinois Teachers Retirement System Apollo PE funds X

Illinois Municipal Apollo Credit Wilshire

Indiana Public Retirement System (INPRS) Apollo Origination Partnership

Iowa Public Employees Retirement System Apollo PE funds Wilshire

Kansas Public Employees Retirement System Apollo PE funds VIII,IX

Kentucky Teachers Apollo REIT & Apollo Stock

Los Angeles City Employees’ Retirement System (LACERS) Apollo PE funds VI

Los Angeles (CA) Water and Power has PE fund X

Louisiana Teachers’ Retirement System of Louisiana (TRSL), Apollo Credit, Natural Resources

Maryland State Retirement & Pension System ?PE funs

Massachusetts PRIM Apollo PE funds

Michigan RS Apollo Investment fund VIII, IX Hybrid Value Funds, Credit/ Opportunistic Credit

Minnesota State Board of Investment Apollo/Athene Dedicated Investment Program II

Mississippi PRS Apollo VIII IX Private Equity funds

Montana Board of Investments Stock holdings?

Nebraska Investment Council India Property Fund II LLC.

New Hampshire Retirement System Apollo PE funds

New Jersey Division of Investment: Stock holdings?

New Mexico State Investment Council Apollo PE VII, VIII PC

New York City Teachers’ Retirement System Apollo PE funds

New York City (NY) ERS PE $500mm 2013

New York City (NY) Police PE fund VI

New York State Apollo PE VIII

North Carolina Retirement Systems Apollo PE funds VI, VII

Ohio Highway Patrol SHPRS: Apollo PE funds

Ohio SERS: “Core Farmland Fund, LP Wilshire

Ohio State Teachers Retirement (STRS) PE Apollo S3 Equity Hybrid Solutions

Ohio Public OPERS Apollo PE funds, Oregon Public Employees Retirement Fund (OPERF), Apollo PE VI, VII, VIII, IX.

Oregon PER recently comitted $300mm to Apollo distressed debt fund as well as earlier funds like Apollo PE IX

Pennsylvania PSERS Apollo PE funds IV $620mm

Pennsylvania SERS Apollo PE funds VI- VIII

Rhode Island Retirement System Apollo PE VIII, IX

San Diego City Employees Retirement System Apollo PE funds

San Francisco (SFERS) San Francisco Employees’ Retirement System Apollo PE funds Wilshire

South Carolina RS $750mm

South Dakota Retirement System Apollo PE funds

Texas County & District PE fund X

Texas ERS Apollo Credit Strategies

Texas Municipal Fund VIII

Texas TRS Teachers’ Retirement Apollo PE funds

Tennessee Consolidated Retirement System Stock holdings?

San Francisco Employees’ Retirement System Apollo PE funds

San Diego City Employees’ Retirement System Apollo PE funds

University of Calfiornia PE VII, VIII Principal Wilshire

Virginia Retirement System Apollo PE funds

Washington State Investment Board (WSIB) Apollo S3 Equity & Hybrid

Australian Super Funds with Apollo – Hostplus, Care Super, Catholic Super-Equip Super. Micheal West/Cliona O’Dowd