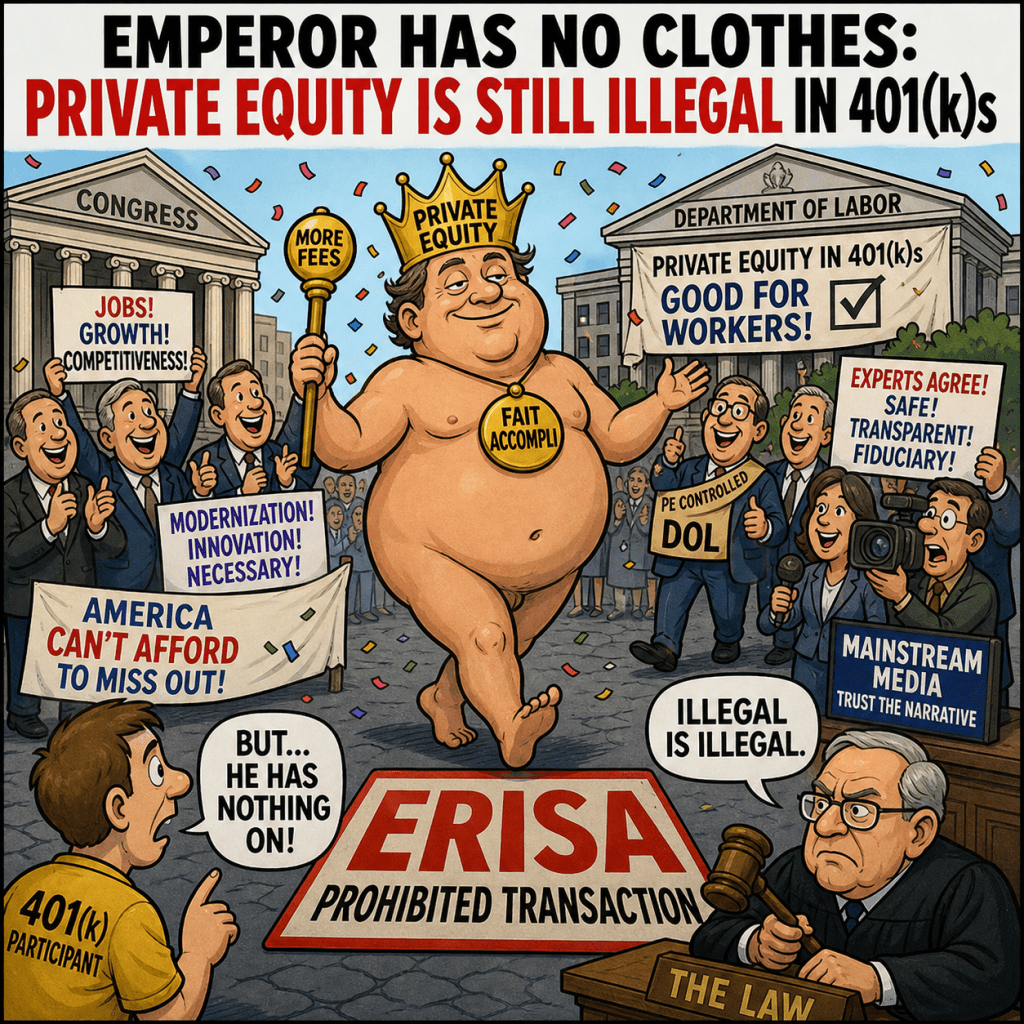

There is a simple truth the retirement industry does not want plan sponsors, participants, or courts to confront:

Despite all the hype we hear from the Private Equity-controlled Department of Labor, PE-controlled Congress, and the PE-controlled or influenced media, that this is a done deal and coming

Private Equity in 401(k) plans is illegal in many cases under ERISA’s prohibited transaction rules.

Not “risky.”

Not “complex.”

Illegal.

And yet it is rapidly being inserted into target date funds, Collective Investment Trusts (CITs), and so-called “diversified” portfolios.

How?

Through secrecy, accounting manipulation, and regulatory arbitrage. https://commonsense401kproject.com/2026/03/06/is-private-equity-illegal-in-your-pension/

1. The Core Legal Problem: ERISA Prohibited Transactions

ERISA is not vague on this.

It prohibits transactions between a plan and a party in interest unless strict exemptions apply. Private equity structures routinely violate this framework:

- Undisclosed fee layers (2 and 20, monitoring fees, transaction fees)

- Revenue sharing and cross-payments

- Affiliated service providers (recordkeepers, consultants, PE sponsors)

- Self-dealing through vertically integrated platforms

As laid out in your prior piece “Private Equity as an ERISA Prohibited Transaction”, once fully disclosed, many of these arrangements would fail fiduciary scrutiny immediately. https://commonsense401kproject.com/2025/10/27/private-equity-as-an-erisa-prohibited-transaction/

That is precisely why full disclosure never happens.

2. The Secrecy Model: If You Can’t See It, You Can’t Challenge It

The industry’s entire defense rests on one premise:

Participants and fiduciaries are never given the information needed to evaluate legality.

This issue is front and center in the Supreme Court’s pending case involving Intel Corporation.

As you’ve written:

- The case is not really about benchmarking

- It is about access to information

If participants cannot see:

- Private equity contracts

- Fee arrangements

- Valuation methodologies

- Side letters

Then ERISA enforcement collapses.

You cannot challenge what you cannot see.

3. The CIT Black Box: Regulatory Arbitrage in Action

Private equity cannot survive inside SEC-registered mutual funds because:

- Daily valuation is required

- Full fee disclosure is required

- Liquidity standards apply

So the industry created an end-run:

State-Regulated Collective Investment Trusts (CITs)

These vehicles:

- Avoid SEC oversight under the Investment Company Act of 1940

- Operate under weak state banking regulation

- Allow mixed accounting standards in a single portfolio

- Provide minimal transparency to participants

As highlighted in your “CIT Black Box” piece: https://commonsense401kproject.com/2026/05/04/the-cit-black-box-bloomberg-gets-it-right-but-the-real-risk-is-even-bigger/

CITs can combine assets priced under four different accounting regimes.

This is not diversification.

It is accounting manipulation.

4. The 25% Rule: The Legal Loophole That Isn’t

The industry often hides behind the so-called “25% test”:

- If less than 25% of a fund is “plan assets,”

- ERISA protections can be diluted or avoided

This rule was never intended to:

- Shield opaque private equity structures

- Enable hidden fee extraction

- Allow fiduciaries to bypass disclosure

Yet in practice, it is used to:

Convert ERISA-protected assets into unregulated capital pools

This is not compliance.

It is regulatory arbitrage. Industry relies on captured Public pensions to fill the 75% non-ERISA potions

5. Even Trustees Can’t See the Contracts

In one of the most telling real-world examples:

- I, as A Kentucky pension trustee of a $20 billion state plan, was denied access to private equity contracts

They did this because I would have shown that the contracts violated state fiduciary laws which are much weaker than ERISA

6. The Diversification Lie

Private equity’s biggest selling point is also its biggest fraud:

“It improves diversification.”

This claim is built on corrupted inputs:

- Artificially smoothed returns

- Manager-reported valuations

- Suppressed volatility

- Lagged pricing

As detailed in your diversification analysis:

- Correlation appears low because pricing is manipulated

- Risk appears low because losses are delayed or hidden

In reality:

- Private equity and private credit are often highly correlated to public markets

- But with worse liquidity, higher fees, and delayed losses

This leads to systematic overallocation in:

- Public pensions

- Target date funds

- 401(k) plans

- https://commonsense401kproject.com/2026/05/04/the-diversification-lie-how-private-equity-and-private-credit-use-corrupt-accounting-to-hijack-pension-and-401k-allocations/

7. The DOL’s Role: Enabler, Not Enforcer

Recent Department of Labor actions—particularly guidance and proposed rules—have:

- Opened the door to private equity in 401(k)s

- Deferred to weaker regulatory frameworks

- Avoided meaningful disclosure requirements

As you’ve argued: https://commonsense401kproject.com/2026/04/04/the-dols-fiduciary-rule-is-really-a-gift-to-wall-street-and-a-trap-for-plan-sponsors/

The DOL fiduciary rule has become a gift to Wall Street and a trap for plan sponsors.

Plan sponsors are being told:

- “It’s allowed”

- “It’s diversified”

- “It’s prudent”

But when litigation comes, they will face:

- Strict ERISA liability

- Without having ever seen the full picture themselves

The DOL has never enforced prohibited transactions with annuities, so basically, the 700 thousand plans under $100 million in assets, are out of luck and will become victims.

The largest 8000 plans, those over $100 million in assets, will be attracting the litigation. The largest 800 plans or so will probably avoid private equity in plans, as they have avoided annuities because of the litigation risk. The media’s focus on the top 1/10th of 1% of plans will probably help this stay under cover.

8. Why This Fails ERISA – Plain and Simple

Private equity in 401(k)s often violates:

1. Duty of Loyalty

Hidden fees and conflicts benefit managers, not participants.

2. Duty of Prudence

Opaque, illiquid, and unpriceable assets cannot be prudently evaluated.

3. Prohibited Transaction Rules

Undisclosed compensation and affiliated dealings trigger violations.

4. Disclosure Requirements

Participants are denied material information.

9. The Bottom Line

Private equity in 401(k)s survives not because it is legal—

But because:

- Contracts are hidden

- Fees are obscured

- Risks are mispriced

- Regulators look away

- Courts are denied the evidence

And most importantly:

Participants are kept in the dark.

10. The Coming Reckoning

If courts—starting with the Supreme Court of the United States—force disclosure:

- Private equity structures will be exposed

- Prohibited transaction claims will follow

- Fiduciary defenses will collapse

At that point, the question will no longer be:

“Is private equity appropriate in a 401(k)?”

It will be:

How was this ever allowed in the first place?

Private Equity in 401(k)s is not a gray area.

It is a black box built to avoid the law.

And once the box is opened—

The entire structure falls apart.