Looking “Under the Hood” of CIT-Based Target Date Funds

Core Fiduciary Principle

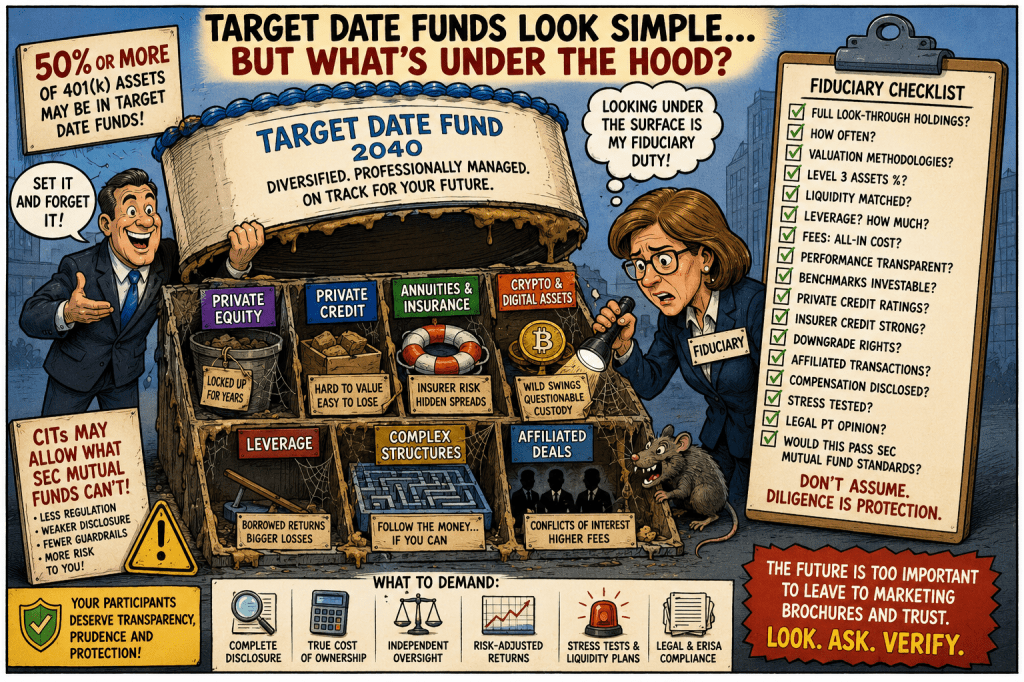

Target Date Funds (“TDFs”) frequently comprise 50% or more of total 401(k) assets and often serve as the plan’s Qualified Default Investment Alternative (“QDIA”).

CFA institute warns that the DOL pathway allowing alternatives needs stronger Guardrails especially around target date funds. https://blogs.cfainstitute.org/marketintegrity/2026/05/26/the-dol-pathway-for-private-assets-in-401ks-are-the-guardrails-strong-enough/

Accordingly, fiduciaries must evaluate:

- not only the Target Date Fund itself,

- but each underlying investment component individually.

Historically, most Target Date Funds operated within SEC-registered mutual funds, where:

- accounting standards,

- valuation rules,

- leverage restrictions,

- liquidity requirements,

- performance reporting,

- and fee disclosure obligations

provided meaningful investor protections.

However, increasingly, Target Date Funds are being moved into weakly regulated state-bank Collective Investment Trusts (“CITs”), where fiduciaries may encounter:

- hidden leverage,

- opaque valuation methodologies,

- affiliated transactions,

- undisclosed spread compensation,

- private credit,

- private equity,

- insurance products,

- crypto exposure,

- and other difficult-to-value assets

that historically were restricted, impractical, or prohibited within SEC mutual funds.

The fiduciary obligation therefore requires substantially enhanced due diligence.

I. TARGET DATE FUND STRUCTURE REVIEW

A. Vehicle Structure

Questions

- Is the TDF:

- SEC mutual fund,

- CIT,

- insurance separate account,

- managed account,

- or hybrid structure?

- Who regulates the structure?

- Is the CIT overseen by:

- OCC,

- state banking regulator,

- or trust company?

Key Concern

State-bank CITs may operate under materially weaker disclosure and transparency requirements than SEC mutual funds.

B. Underlying Holdings Transparency

Questions

- Are complete underlying holdings disclosed?

- How frequently?

- Daily?

- Quarterly?

- Annually?

- Is “look-through” transparency available for all underlying vehicles?

Red Flags

- “Proprietary confidential holdings”

- Delayed reporting

- Aggregated or vague asset descriptions

- Refusal to disclose private holdings

II. UNDERLYING ASSET CLASS REVIEW

A. Private Equity Exposure

Questions

- Does the TDF contain:

- private equity,

- venture capital,

- co-investments,

- secondary funds,

- continuation vehicles?

Required Due Diligence

- PME benchmarking

- IRR vs. time-weighted return comparison

- Fee layering analysis

- Capital call liquidity modeling

- Valuation methodology review

Key Questions

- Are valuations independently verified?

- Are assets Level 3?

- Are marks controlled by the manager?

- Are continuation funds used to avoid losses?

Red Flags

- Non-investable benchmarks

- IRR-only reporting

- Missing public market comparisons

- Hidden carried interest

- Subscription credit lines

B. Private Credit Exposure

Questions

- Does the TDF contain:

- direct lending,

- private debt,

- BDC exposure,

- CLOs,

- NAV loans,

- structured credit,

- mezzanine lending?

Required Due Diligence

- Default stress testing

- Recovery analysis

- Liquidity modeling

- Mark-to-market methodology review

Critical Questions

- Who rates the underlying private credit?

- Moody’s?

- S&P?

- Fitch?

- KBRA?

- internal models?

- Egan-Jones?

- Are ratings investment grade only because of weak methodologies?

Red Flags

- Level 3 pricing

- Internal marks

- Illiquid side pockets

- Affiliated originations

- Weak independent valuation

C. Annuity / Insurance Exposure

Questions

- Does the TDF contain:

- fixed annuities,

- guaranteed income products,

- synthetic wraps,

- insurance separate accounts,

- guaranteed minimum withdrawal products?

Required Due Diligence

- Insurer CDS spreads

- Credit ratings

- State insurance regulator review

- Downgrade clause analysis

- Spread compensation disclosure

- General Account asset review

Critical Questions

- Is there a downgrade termination clause?

- What percentage of General Account assets are:

- Treasuries,

- private credit,

- commercial real estate,

- structured products?

- Is the insurer privately owned by private equity?

Red Flags

- No liquidity rights

- Book-value-only accounting

- No mark-to-market transparency

- Captive reinsurance

- Hidden spread compensation

D. Crypto / Digital Asset Exposure

Questions

- Is there direct or indirect crypto exposure?

- Through:

- ETFs,

- venture funds,

- tokenized assets,

- miners,

- stablecoins,

- exchanges,

- private blockchain vehicles?

Required Due Diligence

- Custody review

- Valuation review

- Counterparty review

- Liquidity analysis

- Regulatory status review

Red Flags

- Offshore custodians

- Unregulated exchanges

- Token valuation opacity

- Leverage

- Staking arrangements

III. ACCOUNTING AND VALUATION REVIEW

A. Mark-to-Market Transparency

Questions

- Which assets are:

- Level 1,

- Level 2,

- Level 3?

- What percentage relies on:

- models,

- appraisals,

- manager discretion?

Key Concern

CITs may create “stale NAV” problems where risk is materially understated.

B. Performance Benchmarking

Questions

- Are benchmarks:

- investable,

- transparent,

- independently calculated?

Red Flags

- CPI-plus benchmarks

- Custom blended benchmarks

- Self-created benchmarks

- Non-public benchmark methodologies

Required Analysis

Compare:

- actual returns,

- volatility,

- drawdowns,

- Sharpe ratios,

against: - low-cost public index alternatives.

C. Smoothing and Return Manipulation

Questions

- Are valuations artificially smoothed?

- Does the TDF show unusually low volatility inconsistent with underlying risks?

Red Flags

- “Too smooth” performance

- Reduced reported volatility from appraisal-based assets

- Infrequent pricing

IV. LIQUIDITY AND REDEMPTION RISK

A. Liquidity Mismatch

Questions

Can daily participant liquidity be supported if:

- underlying assets are multi-year illiquid investments?

Key Concern

401(k) participants may have daily liquidity rights while underlying assets may require:

- years to liquidate,

- lockups,

- gates,

- or side pockets.

B. Suspension Rights

Questions

Can:

- withdrawals,

- transfers,

- exchanges,

- or redemptions

be suspended?

Red Flags

- Gate provisions

- Market stress restrictions

- Delayed NAV processing

V. FEES, SPREADS, AND CONFLICTS

A. Layered Fees

Questions

Are there:

- management fees,

- performance fees,

- carried interest,

- wrap fees,

- consulting fees,

- sub-advisory fees,

- recordkeeping revenue sharing?

Required Analysis

Calculate:

- total look-through cost,

- all indirect compensation,

- embedded spread compensation.

B. Proprietary Product Conflicts

Questions

Are underlying investments:

- proprietary,

- affiliated,

- revenue-sharing arrangements,

- or tied to recordkeeper compensation?

Red Flags

- Proprietary CITs

- Affiliated private funds

- Captive insurance products

- Shelf-space payments

VI. REGULATORY AND LEGAL REVIEW

A. SEC vs. CIT Protections

Questions

Which SEC protections are absent because the TDF operates as a CIT?

Important Areas

- Performance fee restrictions

- Liquidity rules

- Independent board oversight

- Valuation controls

- Public disclosure standards

B. ERISA Prohibited Transaction Analysis

Required Question

Has independent ERISA counsel issued a written legal opinion explaining:

- why the TDF structure does not involve prohibited transactions,

- why all compensation is reasonable,

- and why affiliated arrangements comply with ERISA §§406(a) and 406(b)?

Special Concern

Underlying:

- annuities,

- proprietary private credit,

- insurance products,

- and affiliated private funds

may create hidden party-in-interest conflicts.

VII. STRESS TESTING

Required Scenario Analysis

Stress Events

- 30% private credit markdown

- commercial real estate collapse

- insurer downgrade

- liquidity freeze

- crypto crash

- redemption run

- private equity write-downs

Questions

What happens to:

- participant balances,

- liquidity,

- transfer rights,

- NAV calculations,

- and fiduciary exposure?

VIII. CORE FIDUCIARY QUESTIONS

Fiduciaries Should Ask:

Transparency

- Can we fully explain every major underlying investment?

Liquidity

- Are participants promised daily liquidity backed by illiquid assets?

Valuation

- Are assets genuinely marked to market?

Compensation

- Is hidden spread or affiliated compensation present?

Benchmarking

- Are returns genuinely superior after all fees and risks?

Prudence

- Would these investments survive SEC mutual fund scrutiny?

IX. DOCUMENTATION REQUIREMENTS

Committee Files Should Include

- Full look-through holdings

- Asset class risk memoranda

- Independent valuation reviews

- Benchmark comparisons

- Liquidity stress tests

- Prohibited Transaction legal opinions

- Fee and spread analyses

- CDS and insurer reviews

- Regulatory assessments

X. CENTRAL FIDUCIARY WARNING

The movement of Target Date Funds from SEC mutual funds into opaque CIT structures may permit inclusion of:

- hidden leverage,

- private credit,

- private equity,

- annuities,

- crypto exposure,

- and difficult-to-value assets

that historically faced meaningful SEC constraints.

Because TDFs frequently represent the majority of participant retirement assets, fiduciaries must analyze each underlying component investment individually — not merely rely on the Target Date Fund label, branding, or consultant assurances.

The fiduciary duty is not to trust the surface level fund.

The fiduciary duty is to look through it.

Aronowitz points to fact it will be within a TDF as proof it will be OK, even if it loses money and was imprudent from the beginning. Posting a revised post on this tomorrow or Monday.

Yahoo Mail: Search, Organize, Conquer

LikeLike