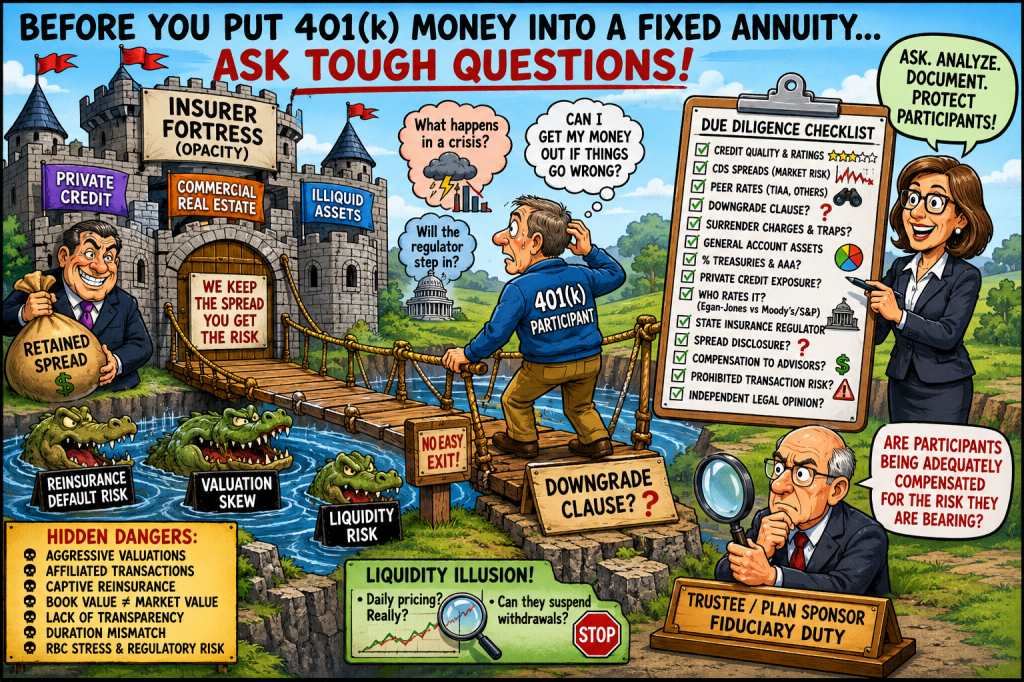

Consultant and Fiduciary Review Framework

Purpose

This checklist is intended to assist ERISA fiduciaries, consultants, investment committees, and plan sponsors in evaluating fixed annuity products offered within 401(k), 403(b), stable value, guaranteed income, or pension risk transfer structures.

The objective is to determine:

- whether the annuity provides adequate compensation for insurer credit and liquidity risk,

- whether the contract may involve prohibited transaction concerns,

- whether hidden spread compensation exists,

- and whether the product is prudent relative to available alternatives.

I. CREDIT QUALITY AND MARKET-BASED RISK REVIEW

A. Public Debt Yield Comparison

Questions

- What yield is the insurer currently paying on publicly traded senior notes?

- What spread over Treasuries does the market require?

- How does the annuity credited rate compare to:

- senior note yields,

- subordinated debt yields,

- institutional funding costs,

- and peer insurer bond spreads?

Key Analysis

If the insurer issues senior notes at 5.3% while crediting annuity holders only 3.0%, evaluate:

- retained spread,

- hidden compensation,

- and whether participants are undercompensated for insurer credit risk and illiquidity.

Documentation

- Current note prospectuses

- TRACE bond yields

- Bloomberg yields

- Treasury spread analysis

B. Credit Default Swaps (CDS)

Questions

- What is the insurer’s current 5-year CDS spread?

- Has CDS widened materially over:

- 1 year,

- 3 years,

- or since contract inception?

- Does the CDS market imply deterioration inconsistent with insurer ratings?

Key Analysis

CDS spreads may provide a more market-sensitive measure of insurer default risk than rating agencies.

Suggested Thresholds

- <50 bps = lower perceived risk

- 50–100 bps = moderate concern

100 bps = elevated concern

- Rapid widening = potential early warning signal

Documentation

- Bloomberg CDS data

- ICE/CMA pricing

- Historical spread charts

C. Ratings Review

Questions

- What are the:

- Moody’s,

- S&P,

- Fitch,

- AM Best ratings?

- Are ratings on:

- negative outlook,

- watchlist,

- or downgrade review?

- Have ratings agencies cited:

- commercial real estate,

- private credit,

- liquidity,

- or valuation risks?

Important

Ratings often lag actual market deterioration.

Documentation

- Ratings reports

- Outlook changes

- Recent downgrade history

II. CONTRACT STRUCTURE AND LIQUIDITY

A. Downgrade Clause

Critical Question

Does the annuity permit termination or liquidation upon:

- ratings downgrade,

- CDS widening,

- RBC deterioration,

- or insolvency concerns?

Questions

- Is there a downgrade trigger?

- At what level?

- BBB?

- BB?

- Can assets be moved without:

- surrender charges,

- market value adjustments,

- or penalties?

Key Analysis

Absence of downgrade rights may expose participants to trapped-credit risk.

B. Surrender and Exit Restrictions

Questions

- What are:

- surrender charges,

- book-to-market adjustments,

- waiting periods,

- transfer restrictions?

- Is liquidity daily, quarterly, annual?

- Can the insurer suspend withdrawals?

Key Analysis

Liquidity restrictions materially increase effective risk.

C. Market Value Transparency

Questions

- Is the contract carried:

- at book value,

- market value,

- or insurer discretion?

- Are underlying assets disclosed?

- Are marks independently verified?

III. COMPETITIVE RATE ANALYSIS

A. Peer Comparison

Questions

How does the credited rate compare to:

- TIAA Traditional,

- MassMutual,

- New York Life,

- Prudential,

- MetLife,

- synthetic stable value funds,

- Treasury securities,

- high-quality short/intermediate bond funds?

Key Analysis

A materially lower rate may imply:

- excessive retained spread,

- weak negotiation,

- or prohibited compensation structures.

B. Treasury and Risk-Free Comparison

Questions

- How does the annuity rate compare to:

- 2-year Treasury,

- 5-year Treasury,

- 10-year Treasury,

- money market yields?

Key Analysis

If annuity rates are below Treasury yields despite materially higher illiquidity and credit risk, fiduciary justification should be documented.

IV. GENERAL ACCOUNT ASSET QUALITY

A. Treasury / AAA Exposure

Questions

What percentage of General Account assets are invested in:

- U.S. Treasuries,

- Agencies,

- AAA securities,

- investment grade corporates,

- below-investment-grade assets,

- private credit,

- commercial real estate,

- CLOs,

- alternatives?

Key Analysis

Higher allocations to:

- private credit,

- CRE,

- structured products,

- or illiquid assets

increase annuity risk.

Suggested Review

Demand detailed NAIC Schedule D asset breakdowns.

B. Private Credit Exposure

Questions

- What percentage of the General Account is private credit?

- Is private credit:

- internally originated,

- affiliated,

- or third-party managed?

- Are assets level-3?

- Are marks independently validated?

Special Concern

Private equity-owned insurers may:

- use aggressive valuation methodologies,

- engage in affiliated transactions,

- or overstate NAV stability.

C. Who Rates the Private Credit?

Questions

Are underlying private credit securities rated by:

- Moody’s,

- S&P,

- Fitch,

- KBRA,

or instead by: - Egan-Jones,

- internal insurer models,

- or lesser-known agencies?

Key Analysis

Reliance on less rigorous or issuer-paid ratings may materially understate risk.

V. REGULATORY REVIEW

A. State Insurance Regulator

Questions

- Which state regulates the insurer?

- Is the regulator considered:

- strong,

- weak,

- industry-captured,

- or aggressive?

Particular Areas of Concern

- Iowa

- Bermuda-affiliated structures

- Captive reinsurance jurisdictions

Questions

- Does the insurer use:

- captives,

- offshore affiliates,

- reserve financing vehicles?

B. RBC and Statutory Capital

Questions

- Current RBC ratio?

- Trend over 5 years?

- Sensitivity to:

- CRE losses,

- private credit markdowns,

- downgrades?

Key Analysis

Strong RBC ratios may still depend on optimistic asset valuations.

VI. DISCLOSURE AND SPREAD COMPENSATION

A. Spread Disclosure

Questions

Does the insurer disclose:

- investment spread,

- net interest margin,

- retained spread,

- compensation from General Account investing?

Key Analysis

Failure to disclose spread economics may impair fiduciary evaluation.

B. Revenue Sharing and Compensation

Questions

Do:

- consultants,

- recordkeepers,

- advisors,

- brokers,

- or affiliates

receive direct or indirect compensation connected to the annuity?

Questions

- Shelf-space fees?

- Revenue sharing?

- Subtransfer agency fees?

- Proprietary product incentives?

VII. PROHIBITED TRANSACTION REVIEW

A. Legal Opinion Requirement

Required Question

Has independent ERISA counsel issued a written legal opinion explaining why:

- the annuity is not a prohibited transaction under ERISA §§406(a) and 406(b),

- insurer spread compensation is reasonable,

- and all compensation is fully disclosed?

Important Legal Issues

Evaluate:

- party-in-interest status,

- insurer compensation,

- affiliated transactions,

- proprietary products,

- General Account lending,

- and hidden spread retention.

Required Documentation

- Independent ERISA legal opinion

- PT exemption analysis

- Compensation disclosure memorandum

VIII. STRESS TESTING

A. Scenario Analysis

Stress Scenarios

- 30% private credit markdown

- CRE impairment

- downgrade to BBB

- downgrade below investment grade

- liquidity run

- widening CDS spreads

- reinsurance counterparty failure

Questions

- What happens to:

- participant liquidity,

- credited rates,

- insurer capital,

- surrender value,

- and contract termination rights?

IX. FIDUCIARY DOCUMENTATION

Committee Record Should Include

- Comparison to market bond yields

- Comparison to peer annuity products

- CDS analysis

- Liquidity analysis

- Downgrade clause analysis

- State regulator assessment

- Underlying asset quality review

- PT legal review

- Written rationale for prudence determination

X. CORE FIDUCIARY QUESTION

The central fiduciary issue is:

“Are participants being adequately compensated for:

- insurer credit risk,

- illiquidity,

- opacity,

- valuation uncertainty,

- and lack of marketability,

relative to available market alternatives?”

If not, fiduciaries should evaluate:

- whether the annuity is prudent,

- whether participants are subsidizing insurer spread profits,

- and whether the arrangement may involve prohibited transaction concerns.

https://commonsense401kproject.com/2026/03/11/tiaa-traditional-annuity-is-a-prohibited-transaction/ https://commonsense401kproject.com/2026/05/20/annuity-collapse-shows-why-insurers-are-a-growing-danger-in-401ks/