Vivek Ramaswamy is now the Republican nominee for Ohio governor, and the pension conflict question has become much sharper.

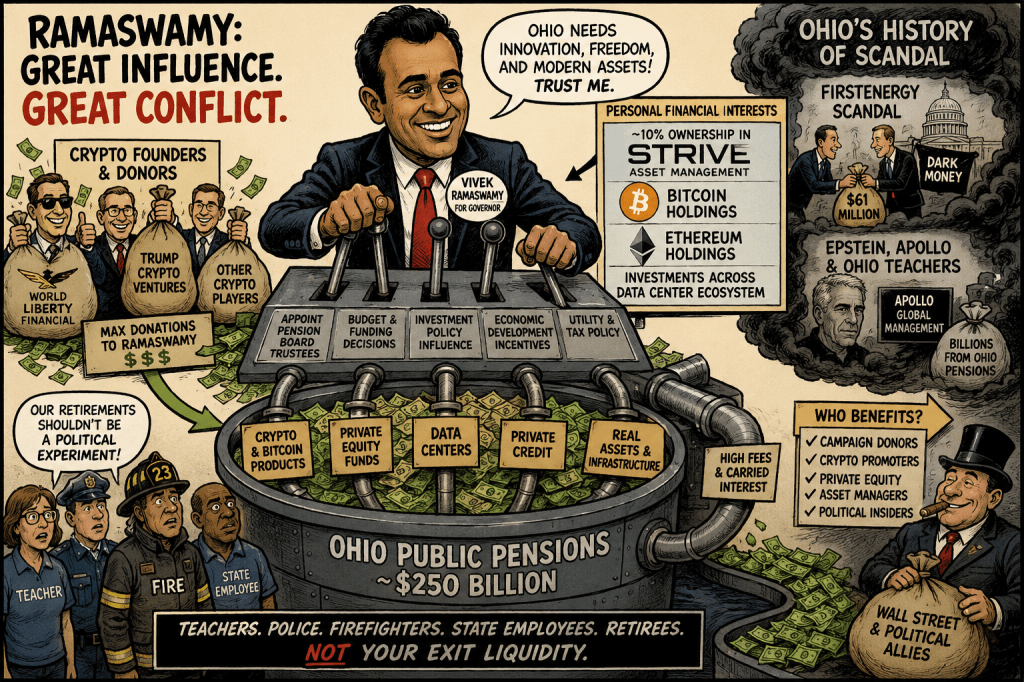

The issue is not simply that Ramaswamy likes Bitcoin. The issue is that he personally holds Bitcoin and Ethereum, retains roughly a 10% stake in Strive, and has supported Ohio House Bill 18, which would open the door for public funds and retirement systems to gain digital-asset exposure.

Recent reporting adds the campaign-money layer. TiffinOhio.net reported that founders of World Liberty Financial, the Trump-family-linked crypto venture, and related figures donated roughly $116,000 to Ramaswamy’s campaign in maximum-legal contributions clustered around primary day. The American Prospect, in partnership with CMD, separately reported that Ramaswamy was backing an Ohio crypto gamble while receiving millions from industry-linked donors.

This creates a classic public-pension conflict pattern: political power, donor money, personal financial exposure, and a proposed investment policy that could benefit the same ecosystem.

Ohio’s governor does not directly run the pension funds, but that is the wrong standard. CMD noted that Ohio’s five pension systems hold roughly a quarter-trillion dollars, and that the governor appoints an investment-expert trustee to each board. It also noted that the 2025 budget shifted the teachers’ pension board toward more government appointee control.

That is why my quote to CMD matters: the governor has “great influence” over state funds. With Ramaswamy, the concern is that influence could be used to normalize high-risk, politically connected investments—crypto, private equity, and other opaque products—inside public pension systems.

The Strive history is also relevant. Indiana’s public pension system contracted with Strive Advisory in 2022, with the contract capped at $150,000 and Ramaswamy reportedly eligible for $4,000 per hour for ad hoc work. That shows Strive was not merely a political brand. It was already seeking and receiving public-pension business.

The Missing Piece: Data Centers Connect Crypto, Private Equity, and Ohio Pensions

Perhaps the biggest conflict that has received the least attention is data centers.

Data centers are rapidly becoming the common denominator linking nearly every major financial interest surrounding Vivek Ramaswamy: private equity, private credit, artificial intelligence, cryptocurrency, electric utilities, real estate, and increasingly, public pension investments.

A recent report by Innovation Ohio concluded that Ramaswamy’s personal financial disclosure shows investments spanning virtually the entire Ohio data-center ecosystem, including semiconductor manufacturers, cloud computing companies, industrial real estate investment trusts (REITs), and cryptocurrency-related assets. The report argues that many of these holdings could benefit from state policies affecting tax incentives, utility regulation, infrastructure spending, and economic development.

For public pensions, this matters because data centers have become one of the fastest-growing investment themes within private equity and private credit.

According to recent S&P Global Market Intelligence data, private equity firms accounted for approximately 72% of all U.S. data-center investment during 2025, investing roughly $45.7 billion in the sector. Blackstone, Apollo, KKR, BlackRock, DigitalBridge and numerous other alternative asset managers are aggressively expanding their ownership of data centers and related infrastructure.

This is the same ecosystem that already receives billions of dollars from Ohio’s public pension systems.

Ohio pension funds have themselves been increasing allocations to data-center strategies. For example, the Ohio Police & Fire Pension Fund recently approved additional commitments specifically targeting data centers and digital infrastructure as part of its real-asset portfolio.

That creates a potentially significant overlap:

- Ramaswamy has financial exposure to companies throughout the data-center supply chain.

- His former company, Strive, has positioned itself to manage institutional investment assets while increasingly emphasizing Bitcoin-related investment products.

- Ohio public pension systems already invest heavily with many of the same private-equity firms financing and owning data-center infrastructure.

- As governor, Ramaswamy would influence appointments, economic-development incentives, utility policy, tax policy, and state investment priorities that could materially affect this industry.

The concern is not simply that data centers are profitable.

The concern is that public pension beneficiaries could unknowingly become financiers of an investment ecosystem in which political leaders, campaign donors, private-equity sponsors, crypto promoters, and asset managers all have overlapping financial interests.

Data centers have become the physical infrastructure supporting artificial intelligence, cloud computing, and cryptocurrency mining. They also represent one of the largest new destinations for private capital. In many cases, the same firms managing Ohio pension assets—Apollo, Blackstone, KKR, BlackRock infrastructure vehicles, DigitalBridge, and others—are simultaneously building, financing, lending to, or owning these facilities.

That is why the data-center issue cannot be separated from the crypto issue or the private-equity issue.

They are increasingly the same investment story.

Just as Ohio learned through Coingate that politically connected “alternative investments” can produce enormous conflicts of interest, today’s combination of crypto, private equity, artificial intelligence, and data centers presents a far larger and more sophisticated governance challenge.

Before Ohio taxpayers and pension beneficiaries are asked to finance this next investment boom, they deserve complete transparency regarding every financial interest, campaign

Ohio Has Been Here Before: From FirstEnergy to Epstein to Data Centers

Ohio does not suffer from a shortage of investment opportunities.

It suffers from a shortage of independent fiduciary oversight.

Ohio’s recent history should make every taxpayer cautious.

The FirstEnergy/House Bill 6 scandal demonstrated how campaign contributions, dark money organizations, political influence, and billions of dollars of public policy can become connected in ways that were largely invisible until federal investigators exposed the scheme. The scandal ultimately resulted in racketeering convictions and remains one of the largest public corruption cases in Ohio history.

Today the names are different.

Instead of electric utilities, the dominant interests are:

- cryptocurrency,

- artificial intelligence,

- data centers,

- private equity,

- private credit,

- and public pension assets.

But the governance questions are remarkably similar.

Ohio is becoming one of the nation’s largest data-center states. Billions of dollars in tax incentives, electric transmission upgrades, water infrastructure, and public policy decisions will determine who profits from that growth.

Those same data centers increasingly are owned or financed by the very private-equity firms that already manage billions for Ohio public pension systems.

Those same facilities support artificial intelligence and cryptocurrency mining.

Those same industries are major sources of political fundraising.

And now the leading candidate for governor has personal investments across much of that ecosystem while advocating policies favorable to digital assets.

That combination deserves far greater scrutiny than it has received.

The Epstein Lesson Should Not Be Forgotten

Earlier this year I wrote about another uncomfortable intersection between Ohio pensions and political influence: Apollo Global Management.

Apollo has managed billions of dollars for Ohio retirement systems while its former CEO, Leon Black, paid Jeffrey Epstein more than $150 million after Epstein’s 2008 conviction. Subsequent releases of Epstein-related materials renewed questions about Apollo’s governance and prompted calls by national teachers’ organizations for additional regulatory scrutiny.

My concern was never that pension beneficiaries’ money was invested with Jeffrey Epstein.

The concern was—and remains—that pension fiduciaries often ignore serious governance red flags whenever a politically connected Wall Street firm produces attractive marketing materials or promises higher returns.

That same governance failure is what allowed Ohio teachers to become deeply invested with Apollo despite years of controversy surrounding its leadership.

Today the governance question has expanded.

Instead of asking only whether Ohio pensions should invest with Apollo, we should ask whether public policy itself is becoming increasingly influenced by an interconnected financial network that includes:

- campaign contributors,

- crypto promoters,

- private-equity sponsors,

- data-center developers,

- institutional asset managers,

- and elected officials with financial interests in that same ecosystem.

The Common Thread Is Not Crypto—It Is Governance

Viewed separately, each issue appears manageable.

- Bitcoin.

- Data centers.

- Private equity.

- Artificial intelligence.

- Campaign contributions.

- Public pension investments.

Viewed together, however, they begin to resemble the same pattern Ohio has seen before.

FirstEnergy showed how concentrated financial interests can shape public policy through political influence.

The Apollo controversy demonstrated how pension fiduciaries can overlook governance concerns when large Wall Street firms are involved.

The emergence of crypto and data centers raises the possibility that these two patterns could merge into a new generation of conflicts.

Ohio should not wait for the next scandal before asking the obvious questions.

Public pensions exist to provide retirement security—not to become financing vehicles for politically connected investment ecosystems.

Ohio has seen this movie before. Coingate was not just about rare coins. It was about politically connected actors persuading public officials to put public money into exotic, hard-to-value assets. Today’s version may be Bitcoin, crypto-linked funds, or private-market products wrapped in “innovation” rhetoric. The structure is familiar.

House Bill 18 remains pending, but its introduced version would affect public-fund investment authority and would clarify that Ohio retirement boards are not prohibited from investing in qualifying exchange-traded products tied to digital assets. Even if the bill does not force pension boards to buy crypto, it changes the political and legal permission structure.

The fiduciary concern is simple:

Teachers, police, firefighters, public employees, and retirees should not become exit liquidity for campaign donors, political allies, or investment firms tied to the governor.

A real reform agenda would require:

- Full disclosure of Ramaswamy’s Strive ownership, crypto holdings, and related compensation.

- Recusal from any appointment, policy, or budget decision involving crypto, Strive, affiliated ETFs, or related public-fund investments.

- A statutory ban on public pension investments in crypto products promoted by campaign donors or governor-connected firms.

- Public release of all pension-related communications with Strive, crypto firms, private equity firms, and politically connected asset managers.

- Independent fiduciary review before any Ohio pension system invests in Bitcoin, crypto ETPs, or Strive-related products.

Ohio pensions already face enough risk from secrecy, alternative investments, and political interference. Ramaswamy’s campaign-money trail and Strive/crypto ties make the conflict too obvious to ignore.