Why Jim Watkins’ Fiduciary Disclosure Theory May Be Even Stronger for Fixed Annuities and Pension Risk Transfer (PRT) Annuities

James Watkins’ latest article makes an important point that extends far beyond lifetime income annuities. https://fiduciaryinvestsense.com/2026/06/23/may-it-please-the-court-closing-argument-on-fiduciary-duty-of-disclosure-under-erisa-section-404a-and-section-783-of-the-restatement-third-of-trusts/

His central argument is simple:

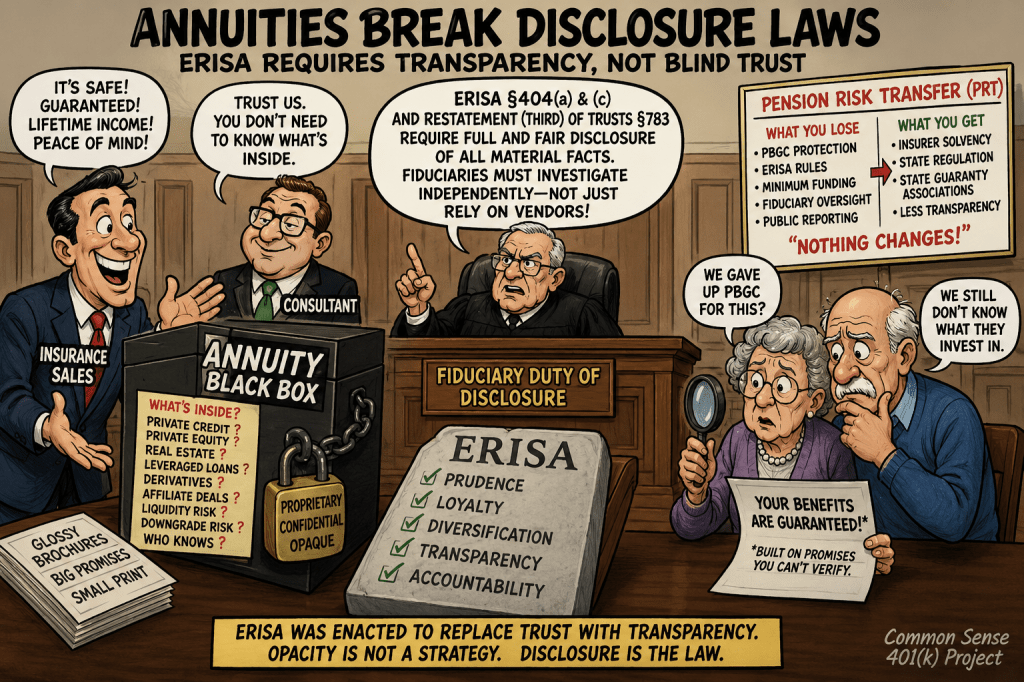

ERISA fiduciaries have an affirmative duty to conduct an independent investigation and disclose all material facts necessary for participants to make an informed decision under ERISA §§404(a) and 404(c), consistent with Section 783 of the Restatement (Third) of Trusts. A fiduciary cannot satisfy that duty by relying on opaque products or conflicted vendors.

I agree with that framework.

Where I part company with much of the retirement industry is that I believe the disclosure problem is far worse for fixed annuities and Pension Risk Transfer (PRT) annuities than it is for lifetime income products.

Those products are not merely difficult to understand.

They often make meaningful disclosure practically impossible.

ERISA Does Not Require Blind Trust

The insurance industry frequently argues that participants do not need to understand the insurer’s investment portfolio.

That argument turns ERISA upside down.

ERISA does not ask whether participants trust the insurer.

ERISA asks whether fiduciaries investigated the investment independently and disclosed the material facts necessary to make an informed decision.

Watkins correctly emphasizes that fiduciaries cannot simply rely on representations from product vendors or consultants with financial incentives. Courts have repeatedly described prudence as requiring an independent investigation rather than procedural box-checking.

If the fiduciary cannot independently verify the facts…

the fiduciary cannot honestly disclose them.

The Fixed Annuity Disclosure Problem

Fixed annuities are often marketed as “safe.”

Yet participants typically receive little or no disclosure regarding:

- actual composition of the insurer’s general account

- percentage invested in private credit

- percentage invested in private equity

- commercial real estate exposure

- leveraged loans

- derivative exposure

- affiliated investments

- securities lending

- liquidity risk

- downgrade risk

- surrender costs

- market value adjustment provisions

- conflicts created by affiliate asset managers

Participants are simply told:

“Your principal is guaranteed.”

That is marketing.

It is not meaningful fiduciary disclosure.

Lifetime Income Is Only the Beginning

My recent article described lifetime income products as the gateway drug for insurance products inside defined contribution plans.

Once fiduciaries become comfortable accepting opaque insurance accounting, the same logic naturally expands to:

- fixed annuities

- index annuities

- separate account annuities

- guaranteed lifetime withdrawal benefits

- collective investment trusts holding insurance contracts

The disclosure standards steadily decline.

Eventually, participants are expected to accept complex products based almost entirely on the insurer’s own representations.

That is precisely what ERISA was designed to prevent.

PRTs May Present the Biggest Disclosure Failure of All

The disclosure problem becomes even more severe in Pension Risk Transfers.

Participants are told:

“Nothing changes.”

In reality, almost everything changes.

The participant loses protection from:

- PBGC insurance

- ERISA funding rules

- minimum funding requirements

- fiduciary oversight

- trustee oversight

- public reporting

The participant instead becomes dependent upon:

- insurer solvency

- state insurance regulation

- state guaranty associations

- insurer investment decisions

Those are enormous changes.

Yet many retirees never receive a balanced explanation comparing those two systems.

Calling the transaction “de-risking” without explaining the risks transferred to retirees is itself arguably misleading.

Material Facts Are Often Missing

Watkins discusses ERISA’s requirement that participants receive sufficient information to make an informed decision.

Applying that principle to fixed annuities raises obvious questions.

Were participants told:

- that insurer portfolios increasingly contain private credit?

- that insurers frequently invest through affiliated asset managers?

- that portfolio risks can change dramatically after purchase?

- that investment guidelines often permit substantial discretion?

- that insurer ratings can change?

- that downgrade provisions may or may not exist?

- that surrender charges may prevent exiting?

- that participants cannot independently monitor portfolio quality?

If not…

how can the disclosure be considered complete?

PRT Participants Receive Even Less Information

Retirees transferred through Pension Risk Transfers frequently never receive meaningful disclosure regarding:

- insurer asset allocation

- private credit exposure

- affiliated investments

- investment guidelines

- liquidity management

- securities lending

- stress testing

- downgrade scenarios

- historical insurer failures

- differences between PBGC protection and state guaranty systems

Instead they receive reassuring marketing materials emphasizing guarantees.

Guarantees are important.

But guarantees themselves depend on the financial strength of the guarantor.

That relationship deserves explanation.

The General Account Is a Black Box

Unlike mutual funds or ETFs, insurer general accounts generally provide limited transparency into day-to-day holdings.

Participants therefore cannot independently determine whether the insurer has materially increased exposure to:

- private debt

- commercial real estate

- infrastructure lending

- leveraged finance

- affiliate transactions

The fiduciary often cannot either.

If neither participant nor fiduciary can independently verify portfolio risks, then meaningful disclosure becomes extraordinarily difficult.

That concern parallels Watkins’ broader observation that ERISA prudence requires objective investigation rather than reliance on opaque products.

Disclosure Is Not a Sales Brochure

Insurance marketing often emphasizes:

- guarantees

- lifetime income

- peace of mind

- certainty

ERISA requires something different.

It requires disclosure of material facts.

Material facts include both benefits and risks.

A disclosure document that highlights guarantees while omitting significant investment, liquidity, or counterparty risks may leave participants without the balanced information needed to make an informed decision.

Whether any particular disclosure is legally sufficient will depend on the specific facts, but fiduciaries should evaluate these materials carefully rather than assuming standard insurance brochures satisfy ERISA’s disclosure obligations.

The Litigation Risk Is Growing

Recent litigation increasingly focuses on process, transparency, conflicts of interest, and fiduciary investigation.

That trend creates additional exposure for sponsors offering insurance products inside retirement plans.

Future plaintiffs are unlikely to ask only:

“Was the product prudent?”

They may also ask:

- What independent investigation was performed?

- What information could the fiduciaries independently verify?

- What material facts were disclosed?

- What material facts were omitted?

- Could participants realistically understand the risks being transferred?

Those questions go directly to the fiduciary duties recognized under ERISA §404(a) and reflected in trust law principles discussed by Watkins.

Bottom Line

Jim Watkins’ article provides a useful framework for evaluating fiduciary disclosure obligations.

In my view, however, its implications extend well beyond lifetime income annuities.

Fixed annuities and Pension Risk Transfer annuities may present even greater disclosure challenges because participants are asked to rely on financial institutions whose risks cannot be independently verified through ordinary public disclosures.

ERISA was enacted to replace trust with transparency.

When participants cannot see the investments backing their retirement promises—and fiduciaries cannot independently verify or explain the material risks—courts may increasingly ask whether the disclosure obligations imposed by ERISA have truly been satisfied.