What Hospital Mergers, Legacy Insurance Products, and Weak Fiduciary Oversight Have in Common

By Christopher Tobe, CFA, CAIA

Ted Siedle and I have written extensively about billions of dollars trapped in aging private equity, venture capital, and real estate partnerships at CalPERS and other public pension systems. Those investments often survive long after their expected life, continuing to generate fees while producing little value. Ted has labled them “zombie funds” https://pensionwarriorsdwardsiedle.substack.com/p/zombie-fund-billions-at-calpers?

But after reviewing dozens of hospital retirement plans over the past several years—including roughly twenty ERISA litigation matters and more than fifty hospital Form 5500 filings—I have become convinced that hospitals have their own zombie problem.

The assets are different. The governance failure may be remarkably similar.

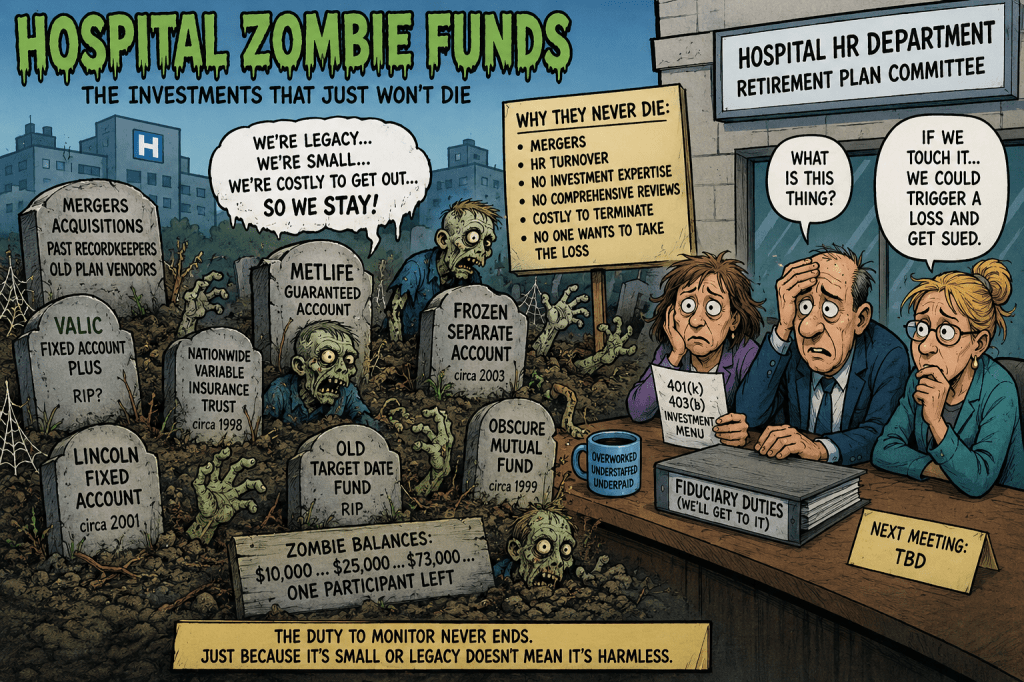

Hospital Zombie Funds

Instead of aging private equity partnerships, hospital 401(k) and 403(b) plans often contain dozens of tiny legacy investments:

- old VALIC insurance products

- Nationwide variable accounts

- Lincoln insurance contracts

- MetLife guaranteed accounts

- obsolete separate accounts

- forgotten mutual fund share classes

- legacy target-date funds

- investment options inherited through mergers decades ago

Many contain only a few thousand dollars.

Some have only one participant remaining.

Others have balances so small one wonders whether anyone has reviewed them in years.

These are what I call Hospital Zombie Funds.

A Retirement Plan Built Like an Archaeological Dig

Healthcare has experienced one of the largest merger waves in American history.

Every acquisition may bring:

- another 403(b)

- another 401(a)

- another insurance carrier

- another recordkeeper

- another consultant

- another investment committee

Few hospitals completely redesign the investment menu after every acquisition.

Instead, they often preserve legacy options to avoid disrupting participants.

Each merger adds another layer.

After twenty years, the investment menu resembles an archaeological excavation.

Every acquisition leaves artifacts.

Why Hospitals May Be Different

One observation from my work is that many hospital retirement plans appear to have less institutional investment infrastructure than large Fortune 500 companies.

Large corporations frequently have:

- treasury departments;

- dedicated pension professionals;

- experienced finance staffs;

- sophisticated fiduciary committees;

- long institutional memory.

Many hospitals instead rely heavily on:

- Human Resources;

- benefits administrators;

- volunteer committee members;

- outside consultants;

- recordkeepers.

Those functions often experience significant personnel turnover. As people leave, institutional knowledge can disappear with them. Successors inherit an investment lineup without necessarily understanding why certain legacy products remain.

This is an observation drawn from my experience across many healthcare plans rather than a universal conclusion, but it is a pattern that deserves closer study.

Insurance Products Create a Different Problem

Legacy mutual funds are generally straightforward to replace.

Insurance products frequently are not.

Many older fixed accounts and guaranteed contracts include provisions such as:

- surrender charges;

- market value adjustments (MVAs);

- book-value accounting;

- withdrawal restrictions;

- negotiated termination provisions.

These provisions vary by contract, but they can make replacing a legacy insurance product expensive.

Imagine a fiduciary committee learns that replacing an inherited insurance contract could immediately reduce participant account values because of contractual exit costs.

That creates a difficult choice.

Leave the contract in place and continue earning below-market crediting rates.

Or recognize a substantial immediate loss.

Few committees voluntarily choose the second option.

The Zombie Effect

This creates what might be called the Zombie Effect.

The investment survives not because anyone believes it is the best available option.

It survives because removing it has become politically, financially, or legally difficult.

Over time:

- committee members change;

- consultants change;

- recordkeepers change;

- memories fade.

Eventually no one remembers why the investment remains.

It simply stays.

The Public Pension Parallel

The governance dynamic resembles what Ted Siedle and I have documented in public pensions.

Public pension systems often hesitate to sell aging private equity or real estate partnerships because doing so requires recognizing losses or accepting discounts in the secondary market.

Hospital fiduciaries may face a comparable challenge when legacy insurance contracts carry meaningful exit costs.

Different assets.

Similar incentives.

Neither situation necessarily reflects bad faith.

Both may reflect governance systems that reward delaying difficult decisions.

The Duty to Monitor Never Ends

ERISA imposes a continuing duty to monitor plan investments.

That duty does not end after selecting an investment.

Nor does it disappear because an investment was inherited through a merger.

Every legacy option should periodically prompt basic questions:

- Why is this investment still here?

- How many participants remain invested?

- Is there a better alternative?

- What would it cost to replace?

- Has anyone recently analyzed those costs?

- Does the investment continue to serve participants’ best interests?

If no one can answer those questions, the plan may have a governance problem even if no single investment is independently imprudent.

Discovery Should Follow the Money

When litigation involves legacy insurance products, plaintiffs should seek discovery regarding:

- every insurance contract;

- every merger integration analysis;

- every recordkeeper conversion study;

- every surrender-value calculation;

- every market value adjustment analysis;

- every consultant recommendation concerning legacy contracts;

- every committee discussion about replacing insurance products;

- every analysis comparing the cost of exiting versus remaining.

Those documents may reveal whether fiduciaries actively evaluated legacy products—or simply allowed them to remain because changing them appeared difficult.

The real question is whether hospitals have allowed decades of mergers to create retirement plans filled with investments that no one meaningfully reviews anymore.

Just as public pensions accumulated billions in private equity zombie funds, hospital retirement plans may have accumulated a different generation of zombies—legacy insurance products and forgotten investment options that remain because they have become too complicated, too expensive, or simply too easy to ignore.

Well done, Chris! Significant mergers in the Atlanta area in recent years. Would not surprise me to related litigation as info comes out.

Yahoo Mail: Search, Organize, Conquer

LikeLike