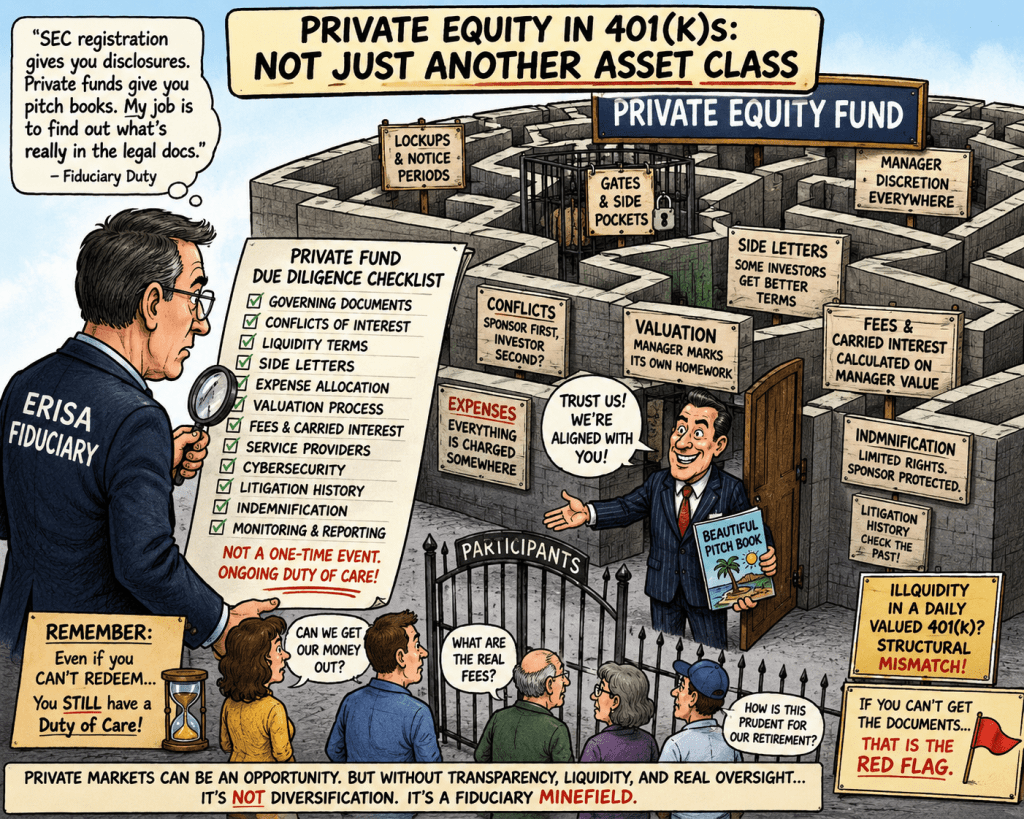

The new Kitces article by Richard Chen is framed as a practical due-diligence guide for RIAs reviewing private equity, private credit, hedge funds, venture, and real estate funds. But read in the 401(k)/403(b) context, it becomes something more important: an admission that private funds require a level of legal, operational, valuation, liquidity, conflict, side-letter, expense, and monitoring diligence that most participant-directed retirement plans are not equipped to perform. https://www.kitces.com/blog/private-equity-debt-fund-due-diligence-checklist-ria-fiduciary-governing-documents-operational/?

That is the key point. Chen does not write like a private-equity critic. He writes like a careful securities lawyer. Yet his checklist confirms my core argument: private markets are not simply “another asset class.” They are structurally different from mutual funds and public securities because the investor often lacks reliable pricing, daily liquidity, standardized disclosure, transparent fees, equal rights, and meaningful legal recourse.

This fits directly with my earlier critique of PwC’s private-equity-in-401(k)s paper. https://commonsense401kproject.com/2026/06/10/pwc-accidentally-says-the-quiet-part-out-loud-about-private-equity-in-401ks/ PwC emphasized “embedding” private markets inside defined contribution structures and estimated a massive fee opportunity for the industry. My response was that the real strategy is not participant choice, but default placement through TDFs, CITs, consultants, recordkeepers, and bundled fiduciary narratives.

Chen’s article strengthens that argument because he says fiduciaries cannot rely on sponsor pitch books or marketing materials. They must review governing documents, conflicts, gates, side pockets, side letters, expense allocation, indemnification, valuation procedures, service providers, cybersecurity, litigation history, and ongoing monitoring. That is not a minor administrative burden. That is a full legal and operational due-diligence regime.

The most important sentence for ERISA litigation is Chen’s warning that fiduciary diligence is not a one-time event. Even in closed-end illiquid funds, the inability to redeem “does not suspend the duty of care.” In fact, it intensifies monitoring obligations. That is devastating to the industry’s argument that private equity can be safely dropped into a TDF sleeve and forgotten for ten years.

Chen also highlights one of the central private-market fraud risks: valuation. Private fund sponsors often control or influence the values used to calculate management fees, carried interest, reported performance, and NAV. This matches my prior ERISA checklist: fiduciaries should not rely on IRR, custom benchmarks, stale marks, or manager-controlled accounting when deciding whether participants actually benefit.

The article is also useful on liquidity. Chen separates ordinary illiquidity from “very illiquid” structures: lockups, notice periods, fund-level gates, investor-level gates, side pockets, and suspension rights. In a daily-valued 401(k) system with loans, withdrawals, transfers, QDIA flows, and participant panic risk, that is not a feature. It is a structural mismatch.

The side-letter section may be especially important. Chen admits that different investors in the same fund may receive better fees, better reporting, better liquidity, co-investment rights, or most-favored-nation protections. That creates a simple ERISA question: how can a fiduciary prove participants received prudent, loyal, and comparable terms if other investors secretly received better ones?

The expense-allocation section also supports litigation. Chen notes that private funds may shift broken-deal costs, legal costs, regulatory expenses, travel, technology, insurance, placement-agent fees, and other overhead to investors. That directly supports the argument that private equity fee disclosure in DC plans is not merely incomplete — it may be fundamentally misleading.

The weakness in Chen’s piece is that it still treats private funds as suitable if the adviser checks enough boxes. For ERISA plans, that may be too forgiving. A retail RIA recommending a small allocation to a wealthy accredited investor is not the same as a plan fiduciary embedding opaque private assets inside default retirement vehicles for ordinary workers.

Chen/Kitches confirms that private equity in 401(k)s is a fiduciary minefield. If fiduciaries cannot obtain the LPAs, side letters, valuation files, expense allocations, liquidity terms, fee offsets, indemnification provisions, cyber controls, service-provider reports, litigation history, and ongoing monitoring records, they should not put private equity in participant-directed retirement plans. And if consultants, CIT providers, or managers refuse to provide those materials, that is not a diligence problem to be managed — it is the fiduciary red flag itself.

Why a checklist for a risk not required at all?Why go there at al.. That issue will be a primary focus of my AI series.

Yahoo Mail: Search, Organize, Conquer

LikeLike

Why a checklist for a product neither legally required and one fraught with obvious fiduciary issues. Why go their at all? #fiduciaryriskmitigation

Yahoo Mail: Search, Organize, Conquer

LikeLike