The new paper from PwC on private markets in defined contribution plans is one of the more revealing industry documents to emerge in years. Not because it exposes the dangers of private equity in 401(k)s — although it acknowledges many of them — but because it openly frames the issue from the industry’s perspective: distribution, scalability, and fee expansion. https://www.pwc.com/us/en/industries/financial-services/library/private-markets-401k-defined-contribution.html

PwC writes:

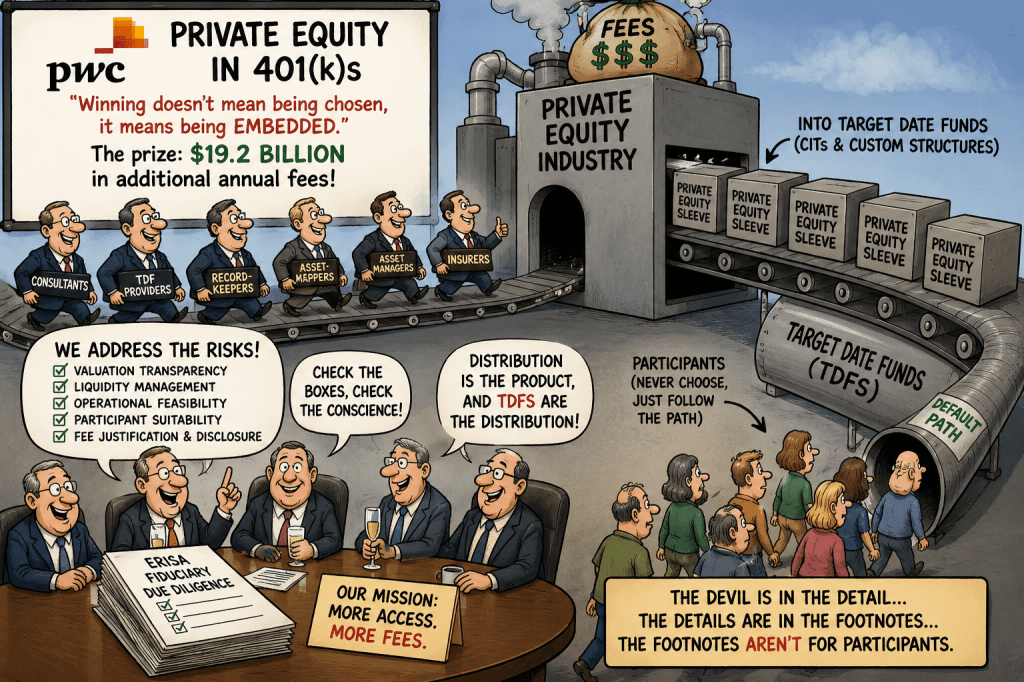

“Yet it’s worth remembering that in DC, winning doesn’t mean being chosen, it means being embedded. And the prize is meaningful, perhaps as much as $19.2 billion in additional annual fees across the industry.”

That sentence should be read carefully by every fiduciary, regulator, and participant in America.

The private equity industry understands something that consultants, target-date fund providers, insurers, and asset managers have spent years engineering: once an investment product is embedded inside a default structure, especially a target-date fund (TDF), participant inertia does the rest.

As I have written before: they repeat

“Distribution is the product, and TDFs are the distribution.”

The industry does not need participants to affirmatively choose private equity. It only needs consultants and recordkeepers to quietly place it inside weak state regulated CIT-based target-date structures where participants never see the underlying risks, valuation assumptions, liquidity constraints, or fee layers.

PwC’s framework identifies five standards for consultant-driven access to DC plans:

- Valuation transparency and discipline

- Participant and plan-level liquidity

- Operational feasibility

- Participant experience, risk mitigation, and suitability

- Fee justification and disclosure

At first glance, these sound reasonable. In reality, they largely function as a consultant comfort checklist designed to reassure fiduciaries while preserving the underlying opacity that makes private markets profitable in the first place.

The problem is not that the industry ignores the risks. The problem is that the industry acknowledges the risks while redefining them as manageable operational issues rather than structural fiduciary defects.

1. “Valuation Transparency” Without Real Market Transparency

PwC discusses valuation governance and discipline as though the issue is simply creating better procedures around marks.

But the real problem is that private equity valuations are fundamentally non-market valuations.

Unlike mutual funds or public securities, most private assets are not priced daily through actual market transactions. They are model-based, manager-controlled, consultant-mediated valuations that frequently rely on stale marks, internal assumptions, appraisal smoothing, and self-selected comparables.

The entire diversification story behind private equity depends heavily on these accounting conventions.

If private equity were marked continuously to observable market liquidity events, much of the “low volatility” narrative would collapse.

This is why the industry fights so hard to keep private assets inside structures exempt from normal securities transparency standards — especially state-regulated CITs and insurance products.

The issue is not merely whether valuations exist. The issue is whether participants can trust them.

2. Liquidity Risk Is Not a Side Issue — It Is the Core Issue

PwC correctly identifies liquidity as a central challenge. But it understates how dangerous this becomes inside participant-directed retirement plans.

401(k) plans are fundamentally daily-liquidity systems:

- daily trading

- daily participant transfers

- daily loans

- daily hardship withdrawals

- daily distributions

Private equity is fundamentally the opposite:

- long lockups

- uncertain exit timing

- manager-controlled realization schedules

- secondary market discounts during stress periods

The industry solution is to place only a “small sleeve” of private equity inside diversified TDFs and surround it with liquid public assets.

But this does not eliminate liquidity risk. It simply transfers liquidity pressure onto the liquid portion of the portfolio during stress events.

That structure works until participants panic, markets fall, or sponsors face large-scale withdrawals.

At that point, fiduciaries discover that liquidity engineering is not the same thing as actual liquidity.

3. Operational Feasibility Is About Consultant Infrastructure, Not Participant Protection

PwC frames operational feasibility as an administrative challenge:

- valuation systems

- transfer restrictions

- daily NAV calculations

- recordkeeper coordination

But the deeper reality is that the operational structure exists primarily to make illiquid assets appear compatible with a daily-priced participant-directed system.

The entire architecture is designed to normalize something that does not naturally fit inside ERISA DC plans.

This is where consultants become essential gatekeepers.

The consultant’s role is increasingly not independent fiduciary oversight. It is engineering pathways that allow higher-fee alternative products to gain access to retirement plan assets while maintaining legal defensibility.

That is why consultant-controlled CITs and custom TDF structures have become so important to the industry.

4. “Participant Experience” Is Often Just Risk Camouflage

PwC discusses participant suitability and risk mitigation, but the actual industry strategy is often volatility smoothing through accounting and structure.

Participants are far less likely to object to private equity exposure if:

- valuations move slowly,

- losses are delayed,

- Benchmark comparisons are customized,

- liquidity stress is hidden,

- fee layers are buried inside bundled structures.

This creates the appearance of stability precisely because the assets are not continuously market-priced.

In many ways, the modern private-market TDF structure resembles the same “stable until suddenly unstable” dynamic that historically appeared in:

- insurance general accounts,

- synthetic yield products,

- structured credit vehicles,

- and certain stable value structures before periods of market stress.

5. Fee Disclosure Still Avoids the Real Economics

PwC mentions fee justification and disclosure, but the paper still largely avoids the most important issue:

the economics of the entire ecosystem.

Private equity fees are not limited to a simple “2 and 20” discussion anymore.

The fee stack increasingly includes:

- private equity manager fees,

- carried interest,

- secondary transaction costs,

- consultant fees,

- OCIO overlays,

- valuation vendors,

- CIT structures,

- recordkeeper revenue sharing,

- custom TDF fees,

- and insurance wrappers.

This is why the industry’s obsession with DC access is so intense.

Even a small allocation inside massive retirement systems creates extraordinary recurring fee streams.

PwC’s own estimate of $19.2 billion in additional annual industry fees may actually understate the long-term economic opportunity.

The Real Goal Is Embedding, Not Selection

The most honest sentence in the PwC paper is the recognition that success in defined contribution plans comes from becoming embedded.

That is exactly correct.

Participants rarely affirmatively choose complex illiquid products.

Instead, the industry seeks:

- default structures,

- consultant-approved models,

- CIT wrappers,

- custom glidepaths,

- and bundled fiduciary narratives that make the exposure effectively invisible.

The future battle over private equity in 401(k)s will not primarily be fought over performance.

It will be fought over:

- transparency,

- accounting standards,

- liquidity truthfulness,

- prohibited transactions,

- consultant conflicts,

- and whether fiduciaries can legally place opaque, self-priced, high-fee structures into participant-directed retirement plans.

The devil is not in the headline promises.

The devil is in the accounting, the liquidity assumptions, and the distribution structure.

And PwC’s paper unintentionally confirms exactly that.

https://commonsense401kproject.com/2026/06/07/erisa-private-equity-fiduciary-due-diligence-checklist/