Chris Tobe, CFA, CAIA Submitted 100-word Comment to DOL

https://www.regulations.gov/document/EBSA-2026-0166-0001

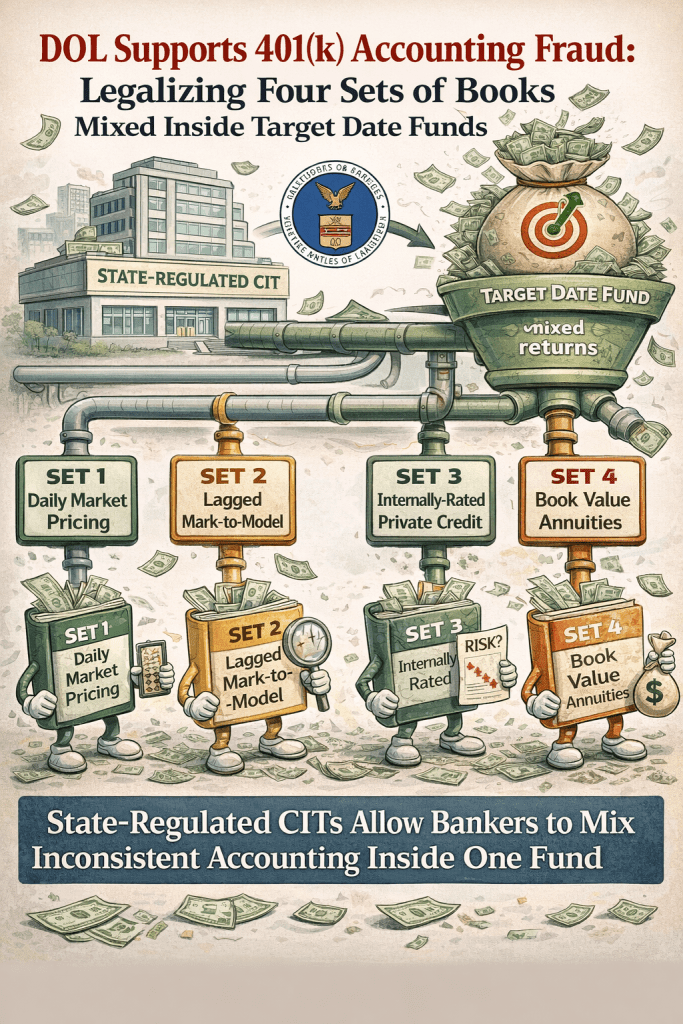

The Department’s proposed rule effectively legitimizes opaque investment structures in 401(k)s that obscure true economic value and risk and violate basic accounting standards. By encouraging use of Private Equity, Private Credit, Crypto, and Annuities (with underlying private credit)—particularly through state-regulated collective investment trusts (CITs)—the rule permits commingling of assets subject to inconsistent valuation regimes, including book value, mark-to-model, smoothed returns, and market pricing. This creates multiple “sets of books” within a single target date fund, undermining ERISA’s core fiduciary duty of prudence and transparency. This proposal invites systemic mispricing, conflicts of interest, and prohibited transactions.

The Department of Labor’s latest proposed rule—“Fiduciary Duties in Selecting Designated Investment Alternatives”—is being pitched as modernization. In reality, it is a sweeping regulatory green light for what can only be described as 401(k) accounting chaos.

At its core, the rule explicitly encourages fiduciaries to include “alternative assets” in defined contribution plans, including target date funds, which comprise over 50% of 401k assets. But what the Department fails to acknowledge—because it cannot defend—is that these assets are not governed by a single, consistent accounting framework.

Instead, the rule enables a structure where multiple incompatible valuation systems coexist inside a single fund:

- Public equities → daily market pricing

- Private equity → lagged, mark-to-model valuations

- Private credit → internally rated, often non-observable pricing

- Annuities → book value with discretionary crediting rates

This is not diversification. This is four sets of books in one product. https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/

The CIT Loophole: Where Transparency Goes to Die

The rule’s most dangerous feature is not what it says—but where it pushes assets.

The Department knows full well that SEC-registered mutual funds cannot accommodate this level of accounting inconsistency. So instead, the rule effectively channels these investments into state-regulated Collective Investment Trusts (CITs).

CITs:

- Are not subject to SEC transparency standards

- Do not require full fee or underlying asset disclosure

- Allow commingling with insurance products and private markets

- Operate under OCC/state banking rules that lack ERISA-level protections

This is the perfect regulatory arbitrage vehicle.

And the DOL knows it.

The Annuity Protection Scheme (Hidden in Plain Sight)

The rule repeatedly claims to be “asset-neutral.” That is demonstrably false.

Buried within the proposal is a clear signal: annuities are to be protected and expanded, not scrutinized.

The Department:

- Explicitly contemplates lifetime income products within QDIAs

- Emphasizes fiduciary discretion over objective pricing benchmarks

- Avoids any requirement to disclose insurer general account yields

This is critical. Because fixed annuities are not fee-based products—they are spread-based products.

That spread:

- Is undisclosed

- Is variable across plans

- Can exceed 200–300 basis points

Represents direct compensation to a party in interest https://commonsense401kproject.com/2026/01/23/fixed-annuities-are-the-dirty-secret-hiding-in-401k-and-403b-plans/

Under any honest application of ERISA §406 and the Supreme Court’s decision in Cunningham v. Cornell, this structure raises clear prohibited transaction concerns.

Yet instead of addressing that conflict, the DOL is building a regulatory shield around it.

“Alternative Assets” = Already Embedded Risk

The industry narrative is that alternatives are new to 401(k)s.

That is false.

As documented extensively, private credit, real estate debt, and illiquid assets are already embedded—primarily inside annuities.

This rule does not introduce alternatives. It:

- Expands them

- Obscures them

- Legitimizes their lack of transparency

And critically, it allows them to be wrapped inside CITs where participants cannot see the underlying risks. https://commonsense401kproject.com/2026/03/24/the-401k-private-credit-lie-98-of-the-risk-is-already-there-hidden-inside-annuities/

The Legal Problem: ERISA Requires Prudence, Not Plausibility

The Department attempts to create a “safe harbor” based on process—suggesting that if fiduciaries follow a checklist, they are protected.

But ERISA is not a checklist statute.

It requires:

- Prudence (objective, risk-based analysis)

- Loyalty (no conflicts of interest)

- Transparency (participants understand what they own)

You cannot meet those standards when:

- Valuations are inconsistent

- Risks are hidden in insurance balance sheets

- Compensation is embedded in undisclosed spreads

This is not prudence. It is plausible deniability codified into regulation.

The Bottom Line

The DOL’s proposed rule does three things:

- Legalizes multi-layered accounting opacity inside 401(k)s

- Funnels assets into lightly regulated CIT structures

- Protects annuity providers and their undisclosed spread profits

This is not reform.

It is a coordinated rollback of fiduciary accountability.

And if finalized, it will mark the moment when the Department of Labor stopped protecting retirement savers—and started protecting the financial products that extract from them.

—————————————————————-

Appendix A

Accounting and Valuation Failures in Private Market Assets and Their Conflict with ERISA Fiduciary Standards

I. Overview

Modern defined contribution plans increasingly incorporate private equity, private credit, and annuity-based investments—often through collective investment trusts (“CITs”) and target date funds. These instruments rely on heterogeneous and incompatible accounting regimes, including:

- Level 1 fair value (observable market prices)

- Level 3 fair value (model-based valuations)

- Net Asset Value (“NAV”) practical expedients

- Book value accounting (insurance general account products)

The coexistence of these regimes within a single investment vehicle produces non-comparable, non-verifiable, and potentially misleading valuations, undermining ERISA’s fiduciary requirements of prudence and loyalty.

II. Private Market Accounting Is Inherently Subjective and Unreliable

A. Level 3 Fair Value Relies on Manager Discretion

Under ASC 820 Fair Value Measurement and IFRS 13 Fair Value Measurement, private equity and private credit investments are typically classified as Level 3 assets, meaning:

- No observable market inputs exist

- Valuations depend on internal models

- Significant managerial judgment is required

Accounting academics have repeatedly warned that such valuations lack reliability and comparability.¹

The Institute of Chartered Accountants in England and Wales notes that fair value for illiquid assets is “controversial” due to its reliance on subjective estimates and managerial discretion, particularly for Level 3 inputs.²

Similarly, academic research finds that private equity valuation requires “significant preparer discretion,” with outcomes highly sensitive to assumptions rather than market evidence.³

B. Valuation “Stickiness” and Opportunistic Smoothing

Empirical accounting research demonstrates that private asset valuations are not merely subjective—they are systematically biased.

Recent literature finds that Level 3 valuations exhibit “stickiness,” meaning:

- Losses are delayed

- Volatility is artificially suppressed

- Reported returns are smoothed over time

This creates what researchers describe as **“opportunistic valuation behavior.”**⁴

Such smoothing directly conflicts with the requirement that fiduciaries evaluate investments based on current and accurate economic value, rather than lagged or managed figures.

III. NAV-Based Accounting Creates Circular and Non-Verifiable Valuation

A. NAV as a Practical Expedient Undermines Independent Verification

Private equity funds commonly report values using NAV, which is:

- Calculated by the fund manager

- Not independently market-tested

- Often accepted by auditors without full verification

Under ASC 820, NAV may be used as a “practical expedient,” but this creates a circular valuation problem:

Managers determine value → fiduciaries rely on that value → no independent price discovery occurs.

Accounting and regulatory commentary has noted that investors may rely on NAV even where it does not reflect realizable value, raising serious concerns about transparency and accuracy.⁵

B. Immediate Mark-Ups and Internal Pricing

NAV-based accounting also permits:

- Immediate valuation increases upon acquisition

- Use of comparable multiples chosen by the manager

- Internal revaluation without market transactions

These practices further detach reported values from objective economic reality, particularly in stressed markets.

IV. Private Credit Accounting Lacks Market Discipline

Private credit presents even greater accounting concerns:

- Loans are not traded in active markets

- Credit ratings are often internal or privately assigned

- Valuations rely on discounted cash flow models using subjective inputs

Academic work on private credit markets highlights:

- Opaque borrower quality

- Lack of price transparency

- Persistent spreads that are not clearly tied to observable risk metrics⁶

This results in valuations that are:

- Non-comparable to public fixed income

- Highly sensitive to assumptions

- Potentially disconnected from actual default risk

V. Mixing Accounting Regimes Produces Non-Comparable and Misleading Results

A. Multiple Valuation Systems Within a Single Fund

When these assets are combined—particularly in target date CITs—participants are exposed to simultaneous use of incompatible accounting systems:

| Asset Type | Accounting Method |

| Public equities | Daily market pricing (Level 1) |

| Private equity | Model-based fair value (Level 3) |

| Private credit | Internal valuation / discounted cash flow |

| Annuities | Book value with discretionary crediting |

Academic literature emphasizes that fair value itself is controversial for private assets; combining it with non-fair-value accounting (e.g., book value) creates even greater distortion.¹

B. Lack of Comparability and Benchmark Integrity

Because these valuation systems operate differently:

- Returns are not measured on a consistent basis

- Volatility is artificially dampened for illiquid assets

- Benchmarks become meaningless or misleading

This directly undermines the ability of fiduciaries to:

- Compare investment alternatives

- Assess risk-adjusted performance

- Monitor ongoing prudence

VI. Conflict with ERISA Fiduciary Duties

A. Duty of Prudence

Under Employee Retirement Income Security Act of 1974 §404(a)(1)(B), fiduciaries must act with:

“care, skill, prudence, and diligence under the circumstances then prevailing.”

This requires evaluation based on:

- Reliable data

- Objective valuation

- Comparable metrics

Where valuations are:

- subjective

- internally generated

- non-verifiable

a fiduciary cannot reasonably determine whether an investment is prudent.

B. Duty of Loyalty and Prohibited Transactions

Under ERISA §406(a) and (b), fiduciaries must avoid:

- transactions with parties in interest

- conflicts of interest

- undisclosed compensation

Accounting opacity exacerbates these risks by:

- obscuring embedded fees (e.g., annuity spreads)

- masking transfer of value to affiliated entities

- preventing participants from understanding true costs

C. Process Cannot Cure Unreliable Inputs

Courts have emphasized that fiduciary review must be based on a reasoned and informed process. However:

- A process relying on unreliable or non-comparable data

- cannot produce a prudent outcome

Thus, a checklist-based approach—such as that proposed by the DOL—does not cure:

- flawed valuation methodologies

- lack of transparency

- structural accounting inconsistencies

VII. Implications of the DOL Proposed Rule

The DOL’s proposed rule on fiduciary duties in selecting investment alternatives emphasizes:

- process-based compliance

- consideration of multiple factors

- fiduciary discretion

However, it does not require:

- standardized valuation methods

- reconciliation of accounting regimes

- independent verification of private asset values

As a result, the rule effectively permits fiduciaries to:

- rely on inconsistent accounting frameworks

- document compliance without resolving valuation conflicts

- include opaque investments in participant-directed plans

VIII. Conclusion

Accounting and academic literature consistently demonstrate that:

- Private market valuations are subjective and model-driven

- Reported values are often smoothed and lagged

- NAV-based accounting is circular and non-verifiable

- Private credit lacks objective pricing discipline

When these assets are combined with publicly traded securities and insurance products, the result is a multi-layered accounting structure that obscures true economic value.

Such a structure is fundamentally incompatible with ERISA’s requirements of:

- prudence

- transparency

- loyalty

and creates a substantial risk of:

- mispricing

- hidden compensation

- prohibited transactions

📚 Footnotes

- Renato Maino & Vera Palea, Private Equity Fair Value Measurement: A Critical Perspective on IFRS 13 (Bocconi Univ.) (noting reliability and comparability concerns in fair value accounting for private equity).

- Institute of Chartered Accountants in England and Wales (ICAEW), Fair Value Measurement by Listed Private Equity Funds (highlighting subjectivity and controversy in Level 3 valuations).

- João Gomes et al., Valuation of Private Equity Investments (Univ. of Manchester) (finding significant reliance on preparer judgment and assumptions).

- Accounting research (2026) (documenting “stickiness” and opportunistic valuation in Level 3 assets).

- See, e.g., commentary on NAV reliance in private equity valuation practices (noting limited independent verification and potential divergence from realizable value).

- Y. Zou (2026), Private Credit Markets (describing opacity, internal pricing, and lack of observable market benchmarks).

Comment on DOL Proposed Rule (EBSA-2026-0166):

A Checklist No One Will Follow—and No One Will Enforce

The Department of Labor’s proposed rule creates the illusion of fiduciary rigor through an elaborate, process-based checklist. In reality, most investment products—especially those involving alternative assets, annuities, and state-regulated CITs—cannot meaningfully satisfy these standards.

The rule requires fiduciaries to evaluate performance, fees, liquidity, valuation, complexity, and benchmarks in an “objective, thorough, and analytical” manner.

But this is theater, not enforcement.

1. Most Products Fail the Test—So the Test Won’t Be Applied

If the checklist were applied honestly:

- Private equity and private credit would fail on valuation transparency

- Annuities would fail on fee disclosure and conflicts (spread pricing)

- CITs would fail on comparability and benchmark integrity

So what happens?

Fiduciaries will “paper the file” and proceed anyway.

And the DOL has effectively invited that outcome by:

- Emphasizing process over results

- Providing a safe harbor for documentation, not outcomes

- Avoiding any requirement for objective, market-based validation

2. The Enforcement Reality: DOL Rarely Polices Investment Choices

The premise of the rule is that it reduces litigation risk and improves fiduciary compliance.

That ignores reality.

Even the DOL’s own enforcement posture shows:

- Focus on egregious misconduct (fraud, embezzlement, operational failures)

- Limited resources directed toward investment-level prudence analysis

- Shifting priorities away from complex fiduciary investigations

In practice, the DOL has never systematically enforced investment selection standards at the level this rule pretends to require.

This rule does not change that.

It simply gives regulators—and fiduciaries—cover to say the process was followed.

3. This Rule Is Not About Litigation Risk—It Barely Applies to Plans That Get Sued

The DOL frames this as addressing litigation risk.

That is fundamentally misleading.

- ERISA litigation is overwhelmingly concentrated in large plans

- Roughly 9,000 plans over $100 million face meaningful litigation exposure

- The remaining 700,000+ small plans are effectively outside the plaintiff bar’s economic reach

This rule primarily affects:

- Small and mid-sized plans

- Plans without sophisticated oversight

- Plans heavily dependent on bundled providers

These are precisely the plans where:

Prepare an analysis of the DOL’s proposed rule re alternative investments in terms of compliance with the Administrative Procedures Act, especially re misleading statements that could harm plan sponsors and plan partucipants, and inconsistencies re ERISA and other applicable laws that could frustrate ERISA’s intended goals and purposes

Below is a structured, litigation-oriented analysis of the Department of Labor’s (DOL) proposed rule on alternative investments in defined contribution (DC) plans, focusing on Administrative Procedure Act (APA) vulnerabilities, misleading framing, and conflicts with ERISA and trust law principles.

I. Regulatory Context and Framing

The proposed rule—“Fiduciary Duties in Selecting Designated Investment Alternatives”—implements a policy shift driven by a 2025 Executive Order to expand access to private equity, private credit, real estate, and digital assets in 401(k) plans.

It introduces:

- A procedural due diligence framework for fiduciaries

- A safe harbor concept tied to compliance with that framework

- An explicit policy goal of reducing perceived litigation barriers to offering alternatives

At the same time, the rule acknowledges heightened risks:

- Illiquidity

- Valuation uncertainty

- Complexity and fees

This dual structure—encouragement + procedural shielding—creates the core APA and ERISA tensions.

II. APA Compliance Analysis

A. Arbitrary and Capricious Standard (5 U.S.C. § 706(2)(A))

1. Selective Framing of Risk (Material Omission Problem)

The DOL emphasizes process (due diligence factors) but downplays or structurally neutralizes substantive risk considerations, despite acknowledging:

- Liquidity mismatch concerns

- Retail investor suitability issues

APA vulnerability:

- An agency acts arbitrarily when it fails to consider an important aspect of the problem (Motor Vehicle Mfrs. Ass’n v. State Farm).

- Here, the “important aspect” is whether certain asset classes are inherently imprudent for participant-directed plans, not merely whether procedures were followed.

Argument:

The rule substitutes process compliance for substantive prudence, effectively ignoring:

- Structural unsuitability of illiquid assets in daily-valued plans

- Asymmetric information between fiduciaries and participants

This is not just a policy choice—it is a category error under trust law, which the APA requires the agency to rationally address.

2. Internal Inconsistency (Safe Harbor vs. Fiduciary Duty)

The rule:

- Requires fiduciaries to consider risk factors

- Simultaneously offers liability protection (“safe harbor”) if procedures are followed

APA issue:

- The agency cannot reconcile how procedural compliance immunizes outcomes that may be substantively imprudent.

This creates a logical inconsistency:

If an investment is imprudent in substance, no amount of process cures the breach under trust law.

Failure to reconcile this contradiction is classic arbitrary-and-capricious reasoning.

3. Predetermined Outcome / Policy-Driven Rulemaking

The rule is explicitly tied to an Executive Order directing expansion of alternatives.

APA concern:

- Evidence suggests policy-driven reversal of prior cautionary guidance (e.g., prior DOL skepticism toward private equity in 401(k)s) without a fully reasoned explanation.

Courts require:

- A reasoned explanation for changing position, especially where reliance interests exist (FCC v. Fox Television Stations).

Argument:

The DOL appears to:

- Recharacterize prior concerns as merely “chilling effects”

- Without adequately addressing whether those concerns were substantively correct

This exposes the rule to challenge as pretextual or insufficiently reasoned.

B. Misleading Statements / Regulatory Mischaracterization

1. Procedural Prudence as a Proxy for Compliance

The rule implies:

Following a checklist of factors = fiduciary compliance

This is misleading as a matter of law.

Under ERISA (incorporating trust law):

- Prudence is substantive, not merely procedural

- Courts evaluate outcomes and decision quality, not just process

APA issue:

- Agencies cannot misstate governing law or create misleading compliance expectations

2. Understatement of Litigation Exposure

By suggesting safe harbor protection, the rule risks misleading plan sponsors into believing:

- Litigation risk is materially reduced

However:

- ERISA fiduciary liability is statutory and judicially enforced

- Safe harbor constructs cannot override:

- Duty of loyalty

- Duty of prudence

Result:

Potential regulated-party harm, a recognized APA concern:

- Sponsors may rely on the rule and later face liability

- Participants may be exposed to imprudent investments

C. Failure to Adequately Assess Costs and Risks

The rule acknowledges risks but does not appear to:

- Quantify participant-level harm scenarios

- Address systemic risks (e.g., liquidity runs, valuation lag)

APA deficiency:

- Inadequate cost-benefit or risk analysis

- Failure to evaluate downside asymmetry for retail investors

III. ERISA and Trust Law Conflicts

A. Substantive Prudence vs. Procedural Formalism

ERISA fiduciary duty derives from trust law, which requires:

- Objective prudence under the circumstances

- Independent evaluation of investment suitability

The rule’s emphasis on:

- Documentation

- Analytical consideration

…implicitly reframes prudence as process-driven, which is inconsistent with:

- Tibble v. Edison International (ongoing duty to monitor)

- Fifth Third Bancorp v. Dudenhoeffer (context-sensitive prudence)

Key conflict:

The rule attempts to decouple process from outcome, which courts have repeatedly rejected.

B. Duty of Loyalty Concerns

The rule’s practical effect:

- Opens large pools of retirement capital to private asset managers

Industry response (positive market reaction) underscores:

- Strong economic incentives for asset managers

ERISA issue:

- Fiduciaries must act solely in participants’ interests, not to:

- Expand market access

- Satisfy policy goals

If the rule facilitates:

- Revenue generation for asset managers

over - Participant protection

…it risks being inconsistent with the exclusive benefit rule.

C. Structural Incompatibility with DC Plan Design

Alternative assets exhibit:

- Illiquidity

- Opaque pricing

- Long lock-up periods

These conflict with:

- Daily valuation

- Participant-directed liquidity expectations

Legal implication:

Even if procedurally vetted, such assets may be:

- Categorically imprudent in participant-directed plans

Failure to address this structural incompatibility undermines:

- ERISA’s protective purpose

IV. Frustration of ERISA’s Statutory Purpose

ERISA’s core objectives:

- Protect plan participants

- Ensure prudent management

- Provide effective judicial enforcement

The proposed rule may frustrate these by:

1. Shifting Risk to Participants

- Increased exposure to complex, high-fee, illiquid investments

2. Diluting Fiduciary Accountability

- Procedural safe harbors weaken enforcement signals

3. Creating False Compliance Signals

- Sponsors may believe checklist compliance satisfies fiduciary duty

4. Undermining Judicial Oversight

- Attempts to preemptively shape liability standards via regulation

VI. Bottom-Line Assessment

From an APA and ERISA perspective, the rule is vulnerable because it:

- Elevates procedural compliance over substantive fiduciary duty

- Creates misleading impressions of legal protection

- Fails to reconcile inherent incompatibilities between alternative assets and DC plan structures

- Advances policy objectives that may conflict with ERISA’s participant-protective purpose

In litigation terms, the strongest theme is:

The DOL is attempting to reframe fiduciary law from a substantive standard grounded in trust law into a procedural checklist regime, without statutory authority and in a manner that misleads regulated parties and endangers plan participants.

—————————————————————————

🔧 If you want next:

I can convert this into:

- Complaint-ready section with case law (Cunningham, Brotherston, etc.)

- Expert report format with exhibits

- Visual “Accounting Stack” diagram to pair with this appendix

This appendix is very strong for judges because it reframes your argument from opinion → accounting system failure.

Top of Form

Bottom of Form

- Fiduciary processes are weakest

- Conflicts of interest are highest

- Documentation is most likely to be boilerplate

In other words, the rule expands theoretical fiduciary duties where enforcement is weakest and litigation is nonexistent.

4. The Real Outcome: Regulatory Safe Harbor for Box-Checking

The practical effect of this rule is simple:

- Investment providers design products that cannot pass the checklist substantively

- Advisors and recordkeepers create templated “fiduciary files”

- Committees sign off based on process documentation

- The DOL does not second-guess outcomes

Result:

👉 A “check-the-box fiduciary system”

👉 Where compliance = paperwork

👉 And prudence = narrative justification

5. Why This Matters

This is not a neutral modernization.

It is a structural shift that:

- Decouples fiduciary duty from measurable reality

- Expands high-risk, opaque investments into weakly governed plans

- Provides regulatory cover for decisions that would not withstand true scrutiny

Combined with:

- State-regulated CIT opacity

- Spread-based annuity economics

- Multi-layered valuation inconsistencies

This rule creates the perfect environment for:

👉 Undetectable underperformance

👉 Hidden compensation

👉 Systematic fiduciary failure without accountability

Bottom Line

This rule is not about improving fiduciary behavior.

It is about standardizing defensibility.

Most products cannot pass the checklist.

Most fiduciaries will pretend they did.

And the DOL will look the other way—just as it always has.