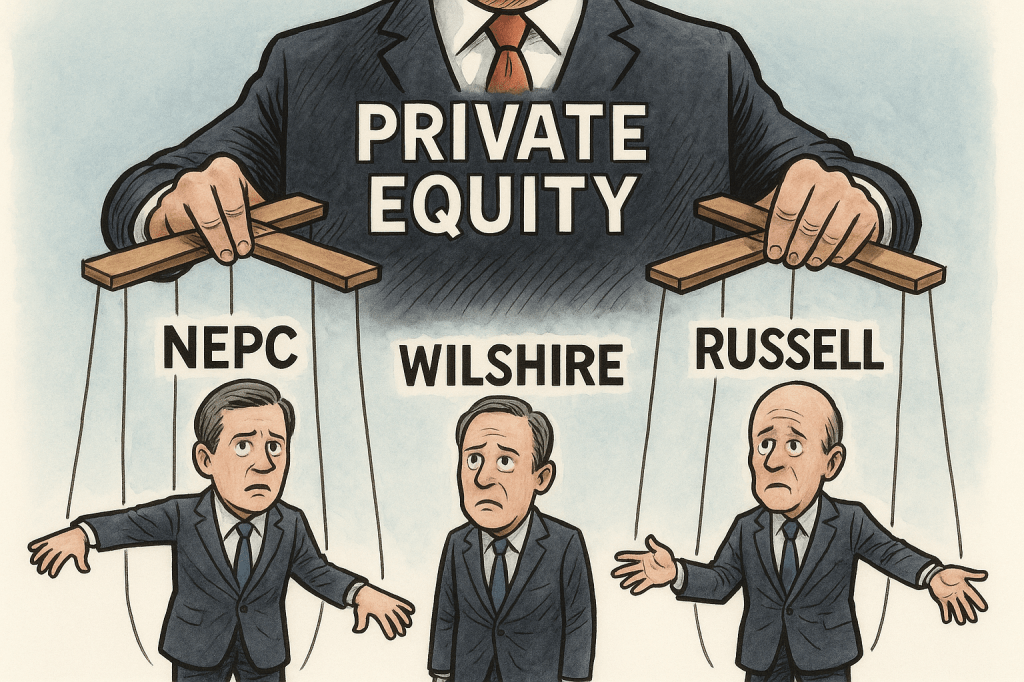

Employee-owned, publicly traded, or PE-backed—every major consultant now has financial incentives to push higher-fee private equity and private credit.

For years, institutional investment consultants have marketed themselves as independent fiduciaries guiding pension funds, 401(k) plans, endowments, and public retirement systems through the complexities of modern markets.

But the truth is far different. In 2025, the consulting industry has quietly transformed into the single most important distribution channel for private equity.

This shift cuts across every ownership model:

PE-owned consultants like NEPC (via Hightower/THL), Wilshire (CC Capital & Motive Partners), Russell Investments (TA Associates & Reverence Capital), and SageView (Aquiline).

Public-company-owned consultants like Mercer (Marsh & McLennan), Aon, and WTW—with earnings models tied to alternatives growth.

Employee-owned consultants like Callan, Meketa, RVK, Verus, and Marquette, who rely on higher-priced alternative consulting services to drive revenue and consultant compensation.

Whether PE-owned or “independent,” the economic incentives all point in the same direction: Push pensions and retirement plans into higher-fee private equity and private credit—regardless of long-term risk to beneficiaries.

PE-Owned Consultants: Conflict at the Core

NEPC – Now indirectly PE-controlled

In 2025, Hightower Holding acquired a majority stake in NEPC. Hightower is itself majority-owned by private equity firm Thomas H. Lee Partners.

This means NEPC—long positioned as a “fiduciary-only” advisor—is now part of a private-equity-backed distribution platform.

Wilshire Advisors – Apollo’s footprint via Motive & CC Capital

Wilshire was taken private by Motive Partners and CC Capital, whose leadership and capital partners maintain deep ties to Apollo and the private markets ecosystem.

Wilshire has since pivoted aggressively toward alternatives advisory and OCIO mandates.

Russell Investments

Owned by TA Associates (majority) and Reverence Capital Partners, Russell is one of the largest OCIO platforms in the world. It profits directly when clients allocate more to alternatives under its discretionary management.

SageView Advisory Group (Aquiline)

For several years, private equity firm Aquiline Capital Partners held a controlling stake in SageView. Aquiline’s strategy: consolidate RIAs and drive asset growth into high-margin private-market solutions.

In short: When the owners of a consultant profit from private equity, the advice will inevitably steer clients toward private equity. Angeles Investment Advisors owned by PE firm Levine Leichtman Capital Partners. Prime Bucholz has been in minority partnerships with PE over the years.

Even consultants not owned by private equity have public shareholders pushing them toward higher-margin advisory services—namely private equity, private credit, and OCIO.

Mercer (owned by Marsh & McLennan)

Mercer operates one of the largest:

OCIO businesses in the world

Proprietary private equity funds-of-funds

Alternative investment research and distribution groups Mercer Alternatives bought Pavillion from PE firm TriWest Capital Partners in 2018, and still influences platform.

Mercer earns much higher fees for:

Private markets due diligence

Access to Mercer-managed PE vehicles

OCIO discretionary mandates

Marsh & McLennan’s investor calls make it clear: alternatives and OCIO growth drive shareholder value.

Aon

Aon aggressively markets:

Aon Private Markets

Aon Private Credit solutions

Aon OCIO

Aon’s 10-K filings explicitly list “delegated investment management” and private markets as key revenue drivers.

WTW (Willis Towers Watson)

WTW operates its own private equity platform:

WTW Private Equity Solutions

Commingled alternative funds

Infrastructure/real asset vehicles

WTW extracts multiple layers of fees when a pension allocates to alternatives through their platform.

Conclusion: Mercer, Aon, and WTW have financial obligations to public shareholders that directly incentivize recommending higher-fee private equity allocations. Rocaton was bought by Goldman Sachs a firm deeply embedded in private equity

This is the category most trustees and regulators mistakenly assume is “independent.” But employee-owned consultants still have major conflicts of interest tied to private equity fee structures.

Callan – Pay-to-Play Through Callan College

Callan promotes itself as independent and employee-owned. Yet:

Callan College allows asset managers—including private equity firms—to pay for access to plan sponsors.

Callan charges premium fees for alternatives consulting.

This creates a baked-in incentive to recommend private equity.

Meketa – Higher Fees for Private Markets

Meketa earns:

Standard fees for public markets consulting

Much higher fees for private equity, private credit, and hedge fund oversight

Plus, Meketa markets itself as a leader in private markets advisory, turning private equity consulting into a profit engine.

Charge materially higher fees for alternatives consulting

Promote themselves as experts in private markets

Benefit through staff growth and enhanced margins when clients increase private equity allocations

Even without PE owners, the internal compensation systems reward consultants who grow alternatives business. Others with substantial conflicts around PE include CEM, Global Governance Advisors, and Funston.

The Industry-Wide Conflict: Alternatives = Higher Fees

Across all ownership structures, the economic truth is the same:

Higher consulting fees; pay-to-play structures; prestige and internal incentives

APPENDIX 1

How Consultants Use Smoothed Returns to Justify Overallocations to Private Equity and Private Credit

Summary

Pension consultants systematically overallocate to private equity and private credit not because these assets demonstrably improve risk-adjusted outcomes, but because smoothed, appraisal-based return data mechanically overstates returns and understates risk in asset-allocation models. This distortion aligns with consultants’ economic conflicts and effectively turns asset-allocation modeling into a distribution mechanism for high-fee private assets.

1. Smoothed Returns Are a Known, Documented Problem

Illiquid private assets do not trade continuously and are typically valued using appraisals, models, or manager-supplied marks. This produces stale and artificially smoothed return series.

The CFA Institute (2025) explicitly warns that analysts must test for serial correlation and states that analysts “need to unsmooth the returns to get a more accurate representation of the risk and return characteristics of the asset class.”

Failure to unsmooth causes:

Understated standard deviation (volatility)

Artificially low correlation to public markets

Inflated Sharpe ratios

Illusory diversification benefits

This is not controversial; it is widely accepted in the academic and professional literature.

2. Optimization Models Convert Smoothing into Overallocation

Consultants then feed these distorted inputs into:

mean-variance optimization,

risk-parity frameworks, or

efficient frontier analyses.

When an asset shows:

high historical returns,

low reported volatility, and

low correlation,

optimization must recommend a larger allocation. The result is mathematically predetermined.

In other words, the model is not discovering diversification—it is laundering volatility.

3. Academic Evidence Confirms the Distortion

The 2019 SSRN paper “Unsmoothing Returns of Illiquid Assets” (Couts, Gonçalves, and Rossi) demonstrates that commonly used unsmoothing techniques are often inadequate and that true risk exposures—especially market beta and downside risk—are materially higher than reported.

Once proper unsmoothing is applied:

correlations to public equities rise,

volatility increases,

and much of the apparent alpha disappears.

This finding directly undermines consultant claims that private equity and private credit offer persistent, low-risk diversification benefits.

4. Why This Serves Consultant Conflicts

As documented in How America’s Largest Pension Consultants Became the Distribution Arm for Private Equity, consultants often have:

ownership ties to private-market platforms,

revenue relationships with private managers,

internal compensation incentives linked to alternatives adoption.

Smoothed returns provide the technical justification for conflicted recommendations. They allow consultants to present sales outcomes as fiduciary analytics.

This same logic applies to private credit, where appraisal-based pricing and delayed loss recognition further suppress volatility and correlation—despite operating in highly competitive credit markets where true excess returns are measured in basis points.

5. Fiduciary Implications

Asset-allocation decisions based on smoothed private-market returns:

overstate expected returns,

understate portfolio risk,

misrepresent diversification benefits,

and systematically bias portfolios toward high-fee private assets.

From a fiduciary perspective, an allocation recommendation that collapses once returns are properly unsmoothed is not prudent—it is misleading.

6. Minimum Disclosures Fiduciaries Should Demand

Any consultant recommending private equity or private credit should be required to provide:

Serial-correlation diagnostics on private-asset returns

Full disclosure of unsmoothing methodology and parameters

Asset-allocation results before and after unsmoothing

Changes in volatility, correlation, and beta post-unsmoothing

A clear explanation of how much of the recommended allocation depends solely on smoothed data

Absent these disclosures, claims of diversification and superior risk-adjusted returns lack credibility.

Appendix 2 : Incentive Misalignment in Private Markets — Insights from CFA Institute Blog Analysis (Jan. 7, 2026)

1. Systemic Incentives Drive Supply Expansion Over Prudence

The CFA Institute piece characterizes the private markets “supply chain” as a **system driven by near-perfect incentive alignment among participants that encourages ever-greater production of private-market vehicles while de-emphasizing underwriting discipline and risk restraint.” CFA Institute Daily Browse

This dynamic applies directly to pension consultants. Once consultants expand roles from independent performance reporters into architects of portfolio design (especially alternative allocations), their professional incentives shift toward increasing portfolio complexity and assets under advisory — because:

Compensation and reputation become tied to the scale and complexity of allocations rather than outcomes.

With private market allocations embedded into policy targets, deviating toward simpler, lower-cost portfolios carries career risk.

Consultant forecasts and capital markets assumptions themselves can rise in tandem with private markets allocations — even as underlying returns lag expectations. CFA Institute Daily Browse

This precisely matches the pattern the CFA Institute warns about: incentives to expand product adoption overshadow incentives to ensure prudence or transparency.CFA Institute Daily Browse

2. Consultants Have Become Structural Amplifiers of Private-Market Narratives

According to the CFA Institute analysis, one of the most dangerous aspects of the private-market ecosystem is when various actors — from advisors to trade media and academia — reinforce a growth narrative, giving “unearned legitimacy” to private market products. CFA Institute Daily Browse

For pension consultants, this confirms two troubling dynamics previously documented in this report:

Consultants are highly influential in driving fund flows without evidence that their recommendations add value to plan sponsors. CFA Institute Daily Browse

By evolving from independent analysts into portfolio constructors and allocators, consultants become part of the amplification machinery that promotes private market adoption, not just neutrally reports it — a conflict of interest the CFA Institute explicitly identifies. CFA Institute Daily Browse

Thus, consultants do not merely advise private market allocations; they structurally reinforce the narrative that these allocations are necessary, beneficial, and inevitable — even when systemic risks and performance realities suggest caution.

3. Structural Conflicts of Interest Echo Across the Supply Chain

The CFA Institute analysis frames private markets as a complex system in which no single actor fully comprehends compounding risk, yet each participant’s incentives promote expansion rather than discipline. CFA Institute Daily Browse

In the context of pension plans, this aligns with the critical observation that:

“Consultants now evaluate outcomes generated by portfolio architectures that they themselves design, reintroducing the same conflict of interest they originally sought to eliminate.” CFA Institute Daily Browse

According to CFA Institute:

Structural incentive alignment among institutional allocators, fund managers, and distribution intermediaries has created a system in which risk segmentation and collective momentum override prudent risk analysis. CFA Institute Daily Browse

Consultants are part of this alignment; their roles have expanded from independent evaluator to essential agent of product adoption — often without accountability for long-term outcomes. CFA Institute Daily Browse

4. The Speculative Supply Chain and Retirement Plans

The CFA Institute’s “speculative supply chain” analogy applies directly to pension plans and defined contribution vehicles:

Private equity and private debt allocations have moved from niche alternatives into core portfolio components in many large plans. CFA Institute Daily Browse

Once participation becomes routinized, collective incentives can orient toward preserving allocations rather than assessing whether those allocations truly benefit participants in net risk-adjusted, cost-adjusted terms. CFA Institute Daily Browse

The narrative of illiquidity as sophistication and complexity as diversification is reinforced by administrators, advisors, consultants, and trade associations alike — exactly the type of amplifier behavior the CFA Institute warns about. CFA Institute Daily Browse

5. Evergreen and Semi-Liquid Structures — A Cautionary Parallel

Although not exclusively about consultants, the analysis highlights evergreen and semi-liquid structures as vehicles that warehouse risk, obscure valuation, and sustain the appearance of performance without transparent price discovery. CFA Institute Daily Browse

This structural design undermines the basic fiduciary principles of:

fair valuation,

periodic accountability, and

participant protection — principles central to ERISA and to the prudent management of retirement plan assets.

That these vehicles are now widely marketed — and often recommended by pension consultants — reinforces why distribution is not neutral and why incentives matter for plan governance.

Zweig is right: Target Date CITs are black boxes. Participants are flying blind. Even fiduciaries often have no idea what they’re buying.

But here’s the deeper truth Zweig could only gesture toward:

State-regulated Collective Investment Trusts (CITs) are the primary mechanism Wall Street now uses to hide high-risk, high-fee products inside 401(k) plans — including Private Equity, annuities, structured credit, and even crypto.

And the industry is now lobbying Congress to expand these opaque products even further — through the INVEST Act, which would open the door for CITs in 403(b) plans, especially for teachers and nonprofit workers.

This is not investor protection. This is a massive subsidy and legal shield for Private Equity and insurers who have already hijacked the Target Date market.

Below is how Zweig’s reporting validates — and amplifies — the very warnings I’ve been documenting for years.

1. Zweig Exposed the Key Weakness of TDF CITs: Zero Transparency

Zweig’s article highlights what most participants do not know:

CIT TDFs do not file SEC prospectuses

CITs provide no daily portfolio holdings

CITs are regulated only by weak state trust departments, not the SEC

CITs routinely change allocations without public notice

CITs often use opaque pricing, smoothing, and valuation methods

Zweig showed the symptoms. But he did not go into the deeper pathology:

The entire CIT TDF ecosystem is built to avoid ERISA and avoid SEC oversight.

It is no coincidence TDF managers moved from mutual funds to CITs. They didn’t do it to save participants fees. They did it to avoid public scrutiny and to create a regulatory gray zone where anything can be hidden.

2. Weak State CIT Oversight Enables Hidden Private Equity, Annuities, and Crypto

As my research has documented:

CITs can legally contain:

Private Equity and Venture Capital

Private Credit / Direct Lending

Insurance annuity contracts

Structured products

Commodities

Crypto ETFs or crypto derivatives

Offshore vehicles

Securitized real estate

High-fee alternative managers

Use excessive leverage

None of this would be allowed inside an SEC-registered mutual fund without substantial disclosure.

Zweig asked the right question — “Do you know what’s inside your 401(k)?” But the deeper answer is:

You don’t know. And you’re not supposed to know. CITs are built specifically so you cannot know.

Even the Department of Labor cannot easily assess CIT risks because the data is not reported to them.

Any Target Date Fund run by a party-in-interest is vulnerable to a prohibited transaction lawsuit that cannot be dismissed at the pleading stage.

This is because:

Compensation exists

The CIT is proprietary or affiliated

The 5500 filings show the affiliation

§406 violations are strict liability — no intent required

And Zweig just gave the public the roadmap.

4. 5500 Forms Make It Easy to Identify Party-in-Interest TDFs

Zweig showed investors are unaware of what is inside their 401(k)s. But what he didn’t say is that lawyers and fiduciaries and even participants can easily identify party-in-interest relationships by checking:

Schedule C (service providers)

Schedule D (CCT/CIT holdings)

Trustee and custodian identities

Indirect compensation disclosures

Affiliated service provider names

This allows plaintiffs to identify:

TDFs run by the recordkeeper

CITs operated by plan consultants

CITs relying on affiliates for valuation services

Platforms that receive crypto pay-to-play or revenue-sharing

Spread-based GICs embedded in CIT “fixed income”

Wherever a TDF manager is also:

the recordkeeper,

the broker-dealer (BrokerageLink),

the consultant/advisor,

the custodian,

or the CIT trustee,

a prohibited transaction theory is not only viable — it is almost guaranteed.

5. Wall Street Is Now Trying to Change ERISA Rather Than Comply With It

Zweig highlights how confusing and opaque CITs have become.

If Private Equity, annuities, and crypto cannot legally be placed inside Target Date CITs under ERISA today, change ERISA so they can.

Congress is being used to rubber-stamp what would otherwise be:

clear party-in-interest violations,

clear §406 prohibited transactions,

and clear breaches of loyalty and prudence.

However, Cunningham v. Cornell was a 9-0 Supreme Court decision showing that even the most Wall Street friendly judges have refused to destroy ERISA protections of DC plan.

6. Wall Street Changing laws to allow Target DATE CITs in non-ERISA plans

Zweig’s findings strengthen four major litigation arguments:

1. CIT opacity = fiduciary breach per Tibble v. Edison

Fiduciaries cannot prudently monitor an investment whose holdings are secret.

2. CITs operated by a plan’s own service provider = prohibited transaction (§406)

Zweig just provided mainstream confirmation that these relationships are common.

3. Hidden alternatives (PE, annuities, crypto) = breach of duty of loyalty

Fiduciaries who cannot see risks cannot act in participants’ best interest.

4. CITs conceal revenue-sharing and indirect compensation = §406(b)(3) violation

Zweig’s discussion of hidden fees matches precisely what I’ve shown in multiple ERISA analyses.

Conclusion: The WSJ Just Confirmed What I’ve Warned for Years — But the Real CIT Corruption Is Still Hidden

Jason Zweig’s reporting is essential. But it is only the beginning.

CIT corruption runs far deeper:

Hidden Private Equity allocations

Hidden annuity spread profits

Hidden crypto exposure through derivatives and brokerage windows

Hidden trustee wrap fees

Hidden sub-advisor platform payments

Hidden GIC spread extraction

Hidden recordkeeper revenue-sharing

The WSJ piece has now validated what fiduciary experts and whistleblowers have documented for years:

Target Date CITs are the most dangerous, opaque, conflict-ridden investment vehicles in the 401(k) and 403(b) system — and they are at the core of modern ERISA prohibited transactions.

Zweig opened the door. It’s now time for litigators, fiduciaries, regulators, and Congress to walk through it.

Appendix: Why “Fee Disclosure Parity” Claims by State-Regulated CIT Trustees Miss the Fiduciary Point

A. The Great Gray Statement: Technically Accurate, Fiduciarily Irrelevant

I wanted to test my theories on CITs. A consultant and I were discussing and he decided to see what Great Grays response would be. He recently shared the following statement from Great Gray Trust, the largest trustee and promoter of state-regulated Collective Investment Trusts (CITs): who is owned by the Private Equity firm Madison Dearborn.

“The OCC has regulations specific to CITs (Regulation 9)… and a couple of states cross-reference or incorporate those regulations… While Great Gray has generally followed those regulations… OCC regulations do not have any specific disclosure requirements regarding CIT fees and expenses. Instead, DOL Rule 404a-5 dictates what must be disclosed… Therefore, it is our view that there should be no distinction between the fees and expenses required to be disclosed for a mutual fund or a CIT… Any attempt to hide fees would be inconsistent with the DOL rule.”

This statement is not blatantly false—but it is misdirection, and from a fiduciary and prohibited-transaction perspective, it is largely irrelevant.

The issue with state-regulated CITs is not whether a standardized fee table is technically disclosed. The issue is whether the underlying assets, valuation methods, revenue flows, and conflicts are capable of being truthfully and reliably disclosed at all.

That is precisely why annuities, private equity, private credit, and crypto are prohibited from mutual funds—and why their migration into state-regulated CITs is a regulatory end-run around ERISA.

B. Why Mutual Funds Prohibit Annuities, Private Equity, and Crypto

Mutual funds are subject to the Investment Company Act of 1940, SEC valuation rules, daily NAV requirements, and independent board oversight. These regimes do not permit assets whose pricing, fees, or performance are inherently opaque or manipulable.

As a result:

Annuities are excluded because spread profits, crediting rates, and insurer balance-sheet economics cannot be independently verified.

Private equity and private credit are excluded because non-market valuations allow fee and performance manipulation.

Crypto is excluded because custody, pricing, liquidity, and auditability are unreliable.

The prohibition is structural, not disclosure-based. The SEC does not say, “You may include these assets if you disclose them better.” It says, you may not include them at all.

That distinction is fatal to Great Gray’s argument.

C. Why OCC Regulation 9 Is a Red Herring

Great Gray correctly notes that OCC Regulation 9 governs national-bank-sponsored CITs and does not impose detailed participant-level disclosure requirements.

But that observation cuts against their position.

Regulation 9 was designed decades ago for traditional bank collective trusts investing in publicly traded securities—not for modern vehicles embedding:

Insurance contracts

Private equity

Private credit

Offshore reinsurance

Derivatives

Annuity-wrapped structures

The OCC never contemplated CITs being used as containers for assets explicitly barred from mutual funds. The absence of detailed disclosure rules in Regulation 9 reflects the assumption of simple, transparent underlying assets, not a regulatory blessing for opacity.

State regulators who “cross-reference” Regulation 9 inherit the same limitations—and often lack the staff, expertise, or independence to challenge aggressive product design.

D. Why DOL Rule 404a-5 Cannot Cure Structural Opacity

Great Gray argues that DOL Rule 404a-5 ensures fee disclosure parity between mutual funds and CITs.

This argument fails for a simple reason:

404a-5 assumes that the disclosed information is accurate, reliable, and economically meaningful.

404a-5:

Does not validate valuations

Does not audit fee flows

Does not test spread profits

Does not examine affiliate compensation

Does not penetrate insurance or private-market structures

If the underlying accounting is unreliable, the disclosure is meaningless.

A fee table that reports “0.45%” is not informative if:

The underlying assets are not market-priced

Fees are embedded in spreads

Revenue flows through affiliates

Performance is smoothed or discretionary

Disclosure of fiction is not transparency.

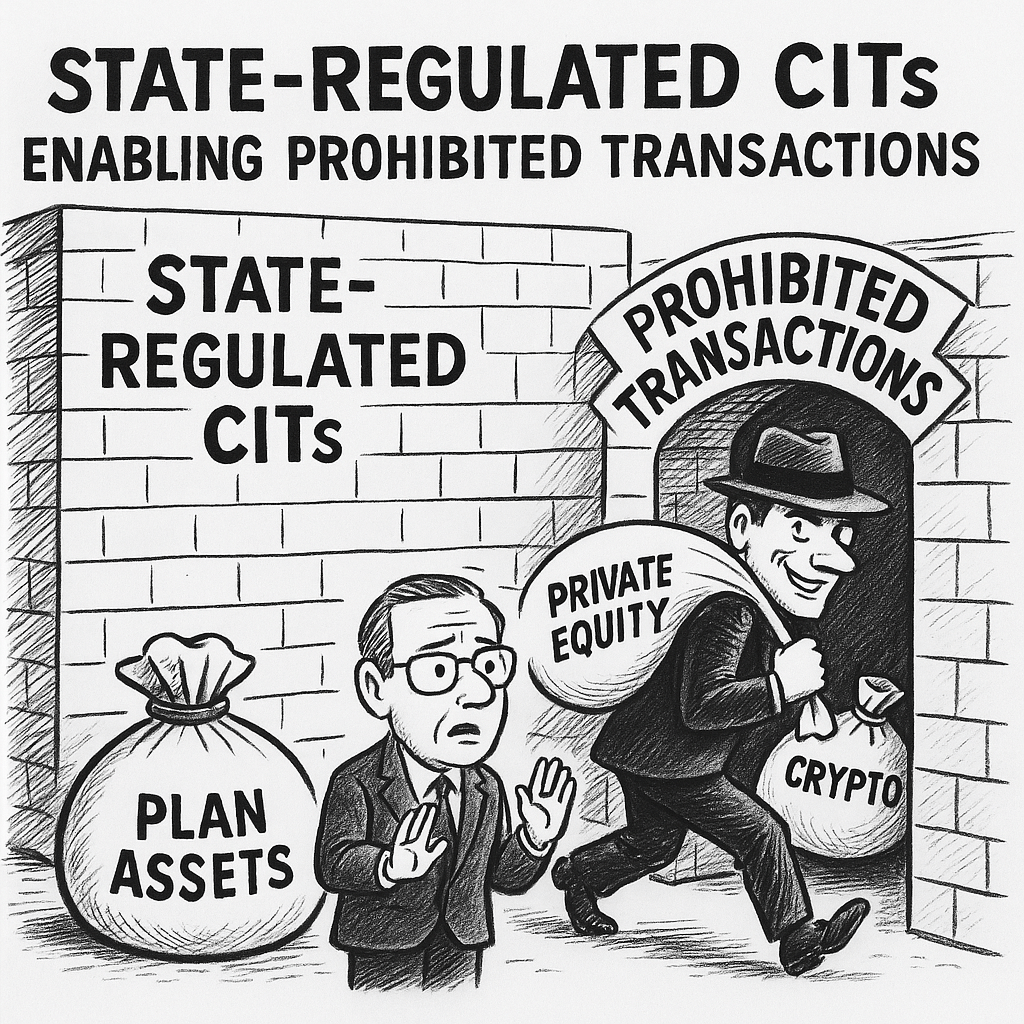

E. Why State-Regulated CITs Enable Prohibited Transactions

This is the central fiduciary issue.

State-regulated CITs allow plan fiduciaries to:

Claim compliance with disclosure rules

While holding assets that cannot exist in mutual funds

And engaging in transactions with parties-in-interest that would otherwise be plainly prohibited

In effect, state-regulated CITs function as regulatory laundering vehicles:

They launder annuities into DC plans

They launder private equity into QDIAs

They launder conflicted compensation through trust structures

That is not a disclosure problem. It is a prohibited-transaction problem.

my response to Great Gray captured the core issue succinctly:

F. Why my Response Is Exactly Right

“Annuities, private equity, and crypto are not allowed in mutual funds because their poor accounting standards make performance and fee information unreliable and subject to manipulation… while their statement is not blatantly false, it is irrelevant.”

Appendix: “NAV = Not Actual Value” — How State-Regulated CITs Allow Private-Market Accounting Fraud Inside 401(k) Plans

A. The WSJ’s Breakthrough — and Its Limits

In When Your Private Fund Turns $1 Into 60 Cents, Jason Zweig documents a phenomenon long understood by institutional fiduciaries but largely hidden from retail and 401(k) investors: private-market net asset values (NAVs) often collapse the moment they are exposed to real price discovery

.Zweig describes multiple non-traded private real estate and private credit funds that, upon listing on public exchanges, immediately traded at 25%–40% discounts to stated NAV—turning a dollar of “value” into roughly sixty cents overnight

NAV = _Not Actual Value_Zweig

. His conclusion is blunt: for many private funds, NAV does not mean net asset value but “not actual value.”

The WSJ article is correct—and devastating. But it only scratches the surface of a far more serious problem: this same fictional NAV accounting is now being imported directly into 401(k) plans through state-regulated Collective Investment Trusts (CITs).

B. Why This Is a 401(k) Problem — Not Just a Private-Fund Problem

The WSJ article focuses on:

Non-traded REITs

Private credit funds

Business development companies (BDCs)

sold primarily to high-net-worth or accredited investors.

What it does not address is that identical valuation methodologies are now being embedded in 401(k) Target-Date Funds via CIT structures, where:

Participants cannot evaluate valuations,

Fiduciaries rely on trust-level accounting,

And ERISA protections are weakened by regulatory arbitrage.

This is not accidental. It is structural.

C. The Accounting Trick: Smoothed NAVs and “Liquidity Theater”

As Zweig explains, private funds appear stable because:

Assets are not traded,

Valuations are manager-determined,

Price volatility is suppressed by appraisal models rather than markets

NAV = _Not Actual Value_Zweig

.

Once public trading begins, markets immediately apply:

Liquidity discounts,

Leverage risk adjustments,

Governance and fee haircuts,

and the NAV collapses.

Inside state-regulated CITs, that moment of truth never occurs:

There is no exchange trading,

No independent market price,

No daily redemption pressure,

No public discount mechanism.

As a result, fictional NAVs can persist indefinitely inside 401(k) plans.

D. Why Mutual Funds Cannot Do This — But State-Regulated CITs Can

The Investment Company Act of 1940 effectively prevents mutual funds from holding assets whose values:

Cannot be independently verified,

Are not market-priced,

Depend on manager discretion.

That is why:

Private equity,

Private credit,

Non-traded real estate,

Illiquid structured products,

have historically been excluded from mutual funds.

State-regulated CITs evade this regime entirely.

By operating outside the SEC’s valuation, governance, and liquidity rules, CITs allow:

Appraisal-based NAVs,

Internal valuation committees,

Manager-controlled assumptions,

to be passed directly into participant accounts—with no effective regulatory backstop.

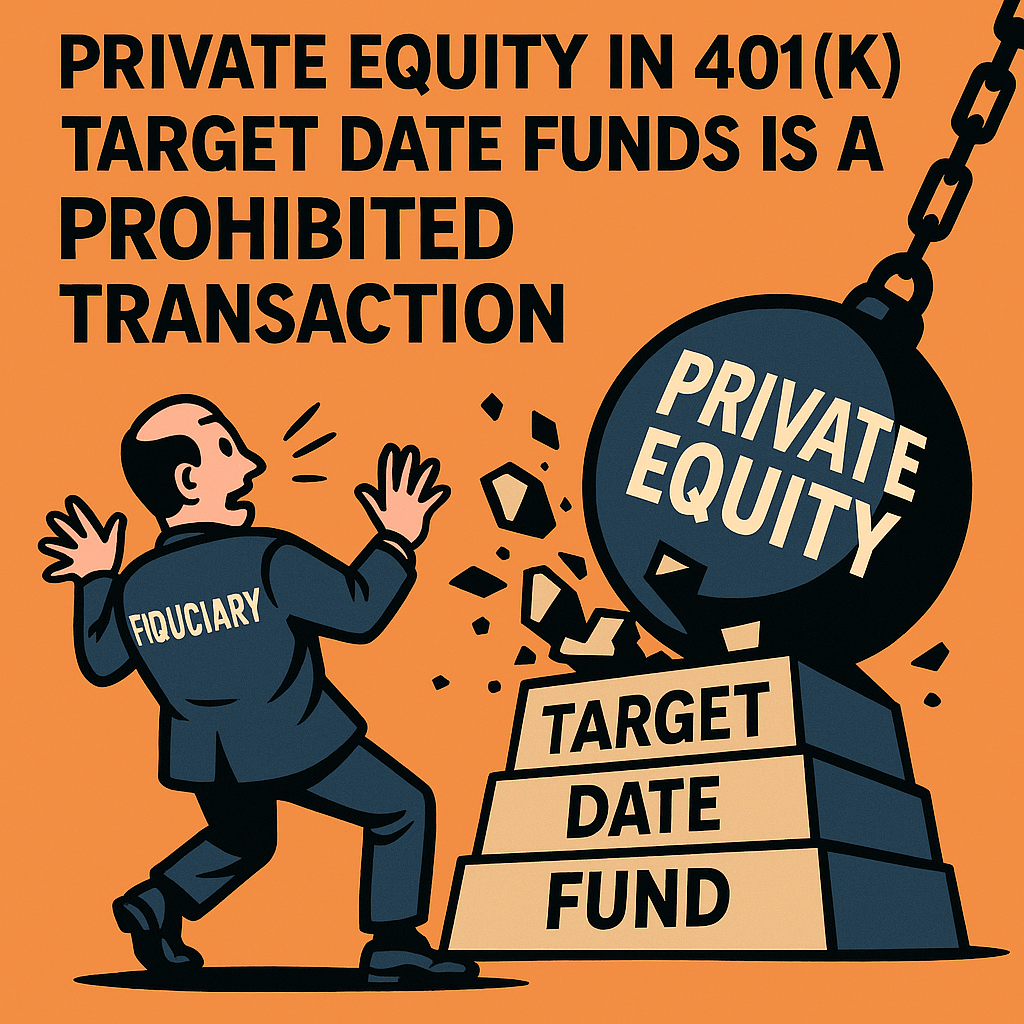

E. Why This Is Worse in Target-Date CITs

Target-Date Funds (TDFs) are uniquely dangerous vehicles for this accounting fiction because:

Participants cannot opt out TDFs are QDIAs. Most participants never choose them—they are defaulted.

Asset allocation masks valuation risk Private assets are buried inside multi-asset portfolios, making losses difficult to attribute.

Losses are discovered late As Zweig shows, losses become visible only when liquidity is forced. In TDF CITs, that may not happen for decades.

Fiduciaries rely on consultant models Consultants validate the “smoothing” as volatility reduction—confusing accounting suppression with risk reduction.

In short, Target-Date CITs are the perfect hiding place for “$1 into 60 cents” accounting.

F. ERISA Implications: Prudence, Valuation, and Prohibited Transactions

Zweig’s article bolsters multiple ERISA claims:

1. Prudence (§404)

A fiduciary cannot prudently rely on valuations that:

Are not market-tested,

Are manager-controlled,

Have repeatedly proven to be overstated when exposed to markets.

2. Disclosure Failures

Fee and performance disclosures are meaningless if the underlying NAV is fictional. Disclosure of false precision is not transparency.

3. Prohibited Transactions (§406)

Many of these private-asset CIT structures involve:

Related-party managers,

Affiliated valuation agents,

Revenue sharing,

Insurance or credit guarantees,

all of which are party-in-interest transactions masked by trust structures.

Zweig’s reporting provides real-world evidence that these structures systematically overstate value, strengthening disgorgement and rescission theories.

G. The Central Irony the WSJ Identifies — and 401(k)s Ignore

Zweig captures the irony succinctly:

Investors were told they could have the stability of private assets and liquidity—until markets proved they could not have both

NAV = _Not Actual Value_Zweig

.

401(k) CITs perpetuate this lie indefinitely:

Participants see “stability,”

But it is manufactured by accounting,

Not by economics.

The losses are merely delayed, not eliminated.

H. Why This Appendix Matters

The WSJ has documented the symptom. This Appendix identifies the disease.

State-regulated CITs allow private-market accounting failures—already exposed in public markets—to be hidden inside America’s retirement system, where:

Participants cannot see them,

Fiduciaries rely on conflicted consultants,

And regulators lack jurisdiction or expertise.

This is not innovation. It is valuation laundering.

Bottom Line

Jason Zweig has shown that in private markets, NAV often means Not Actual Value

NAV = _Not Actual Value_Zweig

. State-regulated CITs now allow that same fiction to live permanently inside 401(k) plans.

When these losses eventually surface—through plan terminations, withdrawals, or litigation—the question will not be what went wrong.

In the Schedule of Investments, the Great Gray Trust Stable Value Fund reports “Guaranteed Investment Contracts – 90.5%” and identifies the holding as “Empower Guaranteed Funding Agreement 599950-01” “exempt from registration under the Investment Company Act of 1940 … and the Securities Act of 1933,” Private Equity owned Great Gray Trust Company, LLC is the trustee and “maintains ultimate fiduciary authority

It also states the credited rate process is “discretionary and proprietary.” This is a direct admission that the plan’s return is not the transparent output of a portfolio—it’s the output of an insurer’s internal pricing decision, i.e., classic general-account spread mechanics.

Certain events could limit transacting at contract value, and “certain events allow Empower to terminate the Agreements … and settle at an amount different from contract value.”

These admissions by the trustee prove that the CIT and underlying General Account Fixed Annuities

It will be why fiduciaries allowed it in the first place.

The INVEST Act seeks to open 403(b) plans — often held by teachers, nonprofit employees, and others — to Collective Investment Trusts (CITs). On the surface, supporters call this “modernizing retirement,” “parity with 401(k),” and “lower cost institutional investing.” Sadly, rhetoric like that obscures a far darker truth: for many Americans, this law would legalize a structural conduit for hidden fees, opaque private-market gambles, and regulatory arbitrage — all at the expense of transparency, fiduciary duty, and retirement safety.

🚨 CITs Are Fundamentally Different From Mutual Funds — and Risky

CITs are not SEC-regulated; rather than SEC oversight, they operate under state banking/trust law (or OCC, IRS/DOL) when they’re “state-regulated.” That means no mandatory prospectus, no N-PORT/N-CEN holdings/flow disclosures, no regular public reports, no independent boards, and — critically — no restrictions on illiquid or alternative assets. The CommonSense 401k Project+2CLS Blue Sky Blog+2

As documented in my own recent analysis, this regulatory structure is tailor-made for ERISA §406 prohibited transactions — self-dealing, hidden revenue sharing, affiliated-manager placements, “alternative sleeves” — all far harder to spot or challenge than in a mutual-fund wrapper. The CommonSense 401k Project

The risk isn’t just theoretical: CITs now manage trillions (by some estimates ~$7 trillion) in defined-contribution assets; many major 401(k) Target-Date Funds (TDFs) have migrated from transparent mutual funds into opaque CIT wrappers. CLS Blue Sky Blog+2Yale Law Journal+2

Thus CITs are not simply a “cheaper mutual-fund alternative.” They are — structurally — a different and far riskier regime.

🧱 Private-Equity, Private Credit, Crypto — Hidden in Plain Sight

The real danger is not just opacity; it is that CITs under the new regime become the delivery vehicle for private markets, annuities, and alternative investments into retirement plans that ordinary savers trust to be safe. As I laid out previously: CIT TDFs as QDIAs are perfectly positioned to:

quietly embed private equity, private credit, crypto, real-asset private placements, or other illiquid/alternative investments under a “Target Date Fund” label; The CommonSense 401k Project+2CLS Blue Sky Blog+2

hide multiple layers of fees (sub-TA, wrap, trustee, platform, revenue-sharing), none of which are transparently disclosed; The CommonSense 401k Project+1

create “vertical stack” conflicts of interest — e.g., the same private-equity sponsor owning the trustee, the CIT issuer, the recordkeeper, and possibly advisor-platform arms — meaning that each layer profits when savers’ money is funneled into opaque investments. The CommonSense 401k Project

In effect: under the INVEST Act, retirement savings — even for teachers, nonprofit staff, lower-paid workers — could get funneled into the same private-market gambits that now benefit ultra-wealthy fund investors. And with minimal transparency, no signal, and little chance for participants to know what’s going on until it’s too late.

🏦 Regulatory Arbitrage — The “Hole” That Saves Private Markets

The shift to CITs represents classic regulatory arbitrage: by moving plan assets from SEC-regulated mutual funds into state-chartered trust vehicles, fund managers and private-equity sponsors escape public disclosure, liquidity/resale requirements, independent boards, and robust oversight. The CommonSense 401k Project+2NYU Law+2

That’s not just a compliance tweak — it’s a fundamental renaming of risk. A “Target-Date Fund” under a CIT is no longer the transparent, retail-friendly product most plan participants think they’re getting. It is a private-market trust in a cloak of respectability.

⚖️ For Retirement Savers and Fiduciaries — This Is A Regression

Fiduciaries under Employee Retirement Income Security Act (ERISA) are supposed to act with the care of a “prudent expert.” But how can that duty be meaningfully discharged when holdings, fee structures, valuation, liquidity, and conflicts are hidden? You cannot prudently evaluate what you cannot see. The CommonSense 401k Project+1

For plan participants — especially those in nonprofit, education, public service 403(b) plans — the shift under INVEST could undermine retirement security. What looks like a “safer, institutional-grade” retirement fund might in practice be a high-fee, illiquid, high-risk private-market bet.

And legal recourse is likely to be limited. By layering private-market investments inside bank-trust CITs, the accountability framework that protects mutual-fund investors becomes fragmented and attenuated.

🎯 What Should Be Done Instead

If lawmakers genuinely care about “parity” and “modernizing” retirement, that shouldn’t mean sacrificing transparency and investor protections. Instead of opening the door to CITs in 403(b)s en masse, policymakers should insist on structural reforms:

Full disclosure — all CIT holdings, underlying investments, fees, and related-party flows must be publicly available and easily accessible to plan participants.

Ban or strictly limit alternative / illiquid / private-market investments in retirement-plan CITs — particularly for non–ERISA 403(b) plans — unless underlying vehicles meet public-fund standards (liquidity, valuation, reporting).

Independent fiduciary oversight — true independent boards or third-party fiduciaries (not affiliates of providers/recordkeepers) should manage CITs for retail retirement plans.

Restore mutual-fund (or equivalent) QDIA defaults — if a default is needed, default to transparent, low-cost SEC-regulated mutual funds, not opaque CIT-TDFs.

Until such reforms are guaranteed, letting 403(b) plans invest in CITs is not “modernization.” It’s a regression — a regulatory carve-out designed to benefit private-equity, insurance, and asset-management firms at the expense of everyday workers.

📢 Conclusion: INVEST Act = Privatizing Risk Under the Guise of “Retirement Reform”

The INVEST Act’s attempt to give 403(b)s access to CITs should not be celebrated — it should be stopped, or at least substantially amended. For most Americans, retirement savings are not a speculative venture; they are a guarantee of future stability. Opening the door to opaque, alternative-heavy, private-market trusts — without meaningful transparency or fiduciary protections — undermines the very purpose of retirement plans.

Congress should reject the “privatization of risk” in favor of real retirement security: transparent, liquid, low-cost investments — not hidden private-equity funnels.

Why Rep. Randy Fine’s ERISA Bill Looks Like a Gift to Private Equity, Annuities, Crypto.

In April 2025, the U.S. Supreme Court handed down one of the most consequential ERISA decisions in decades: Cunningham v. Cornell University. This was an unanimous decision. Fine filed a bill to be more pro-Wall Street than the most pro-business justices of the current court

For the first time, the Court clarified that plaintiffs do not need to plead an exemption under ERISA §408 to survive a motion to dismiss. It is enough to plausibly allege a prohibited transaction under §406(a)(1)(C)—a fiduciary causing the plan to transact with a party in interest.

This seemingly technical point is a tectonic shift.

Cunningham dramatically lowers the barrier for bringing prohibited-transaction suits involving:

Insurance annuities

Recordkeeping and administrative arrangements

Private equity and alternative assets

Collective investment trusts (CITs)

Crypto access and custodial arrangements

Any relationship with a service provider can now face discovery unless the fiduciary proves that an exemption applies—at the defendant’s burden.

Corporate counsel, insurance lobbyists, PE firms, and employer-side ERISA lawyers panicked. Plaintiffs’ firms rejoiced. And within months, Congress saw a new bill—one designed to effectively reverse Cunningham at the pleading stage.

That bill came from a surprising place: Rep. Randy Fine, a first-term Republican from Florida’s new 6th District, best known not for retirement policy but for fiery pro-Israel rhetoric “no genocide” “no starvation” “no problem” and a deeply intertwined relationship with the Republican Jewish Coalition’s donor base. He is also a staunch Trump loyalist and Trumps DOL EBSA appointee has reflected the strong industry opposition to Cunningham https://www.levernews.com/the-corporate-crusade-of-trumps-top-retirement-cop/

This is where the story gets interesting.

H.R. 6084: The ERISA Litigation Reform Act—A Cunningham Counterstrike

On November 18, 2025, Rep. Randy Fine introduced H.R. 6084, the ERISA Litigation Reform Act. Its twin goals are simple:

Raise the pleading standard for ERISA prohibited-transaction suits.

Stay discovery until plaintiffs prove additional factual detail.

In other words: make it harder to sue annuity providers, private-equity platforms, recordkeepers, and crypto custodians—the exact entities most exposed after Cunningham.

The official statement from Fine’s office frames this as protecting employers from “abusive litigation tactics.” Committee Chairman Rep. Tim Walberg immediately endorsed the bill, calling it an essential reform for America’s retirement system.

But here’s the question:

Why is a freshman Florida congressman—whose political identity revolves around pro-Israel activism and cultural fights—leading the charge to shield private equity, annuity issuers, and crypto-adjacent financial players from ERISA suits?

The answer appears to be found in the donor network behind his campaign.

Follow the Money: RJC → Finance Billionaires → Fine

According to publicly available OpenSecrets-linked reporting:

RJC-PAC sent over $60,000 to “Randy Fine for Congress”, making Fine one of its top beneficiaries in the 2024–2025 cycle.

RJC-PAC’s funding base is heavily weighted toward high-net-worth donors from the hedge-fund, private-equity, and financial-services world.

Major RJC donors include individuals associated with Elliott Management (Paul Singer), Cerberus Capital, Apollo-adjacent networks, real-estate investment conglomerates, and other alternative-asset firms.

Historically, pro-Israel Republican super-donors like Sheldon Adelson poured tens of millions into RJC infrastructure, much of it tied to Wall Street wealth.

Put simply:

Fine is a direct financial product of a political network funded by the same financial titans who benefit most from blocking ERISA litigation against alternative assets and insurance contracts.

This doesn’t mean quid pro quo. It means alignment. It means interests line up neatly.

The RJC’s donor base includes players in those industries. And now a top RJC-funded candidate is carrying a bill that would give them precisely what they want.

The Broader Pattern: Protecting Alts in 401(k)s While Weakening Prohibited-Transaction Enforcement

H.R. 6084 doesn’t exist in a vacuum. It fits into a larger mosaic:

1. The Retirement Investment Choice Act (H.R. 5748)

A bill that would codify the Trump-era Labor Department policy allowing private equity, private credit, and non-transparent alternatives inside 401(k) plans.

2. Industry push to allow crypto in DC plans

Fidelity and other players have lobbied heavily to protect crypto access in self-directed brokerage windows—and to shield themselves from fiduciary exposure.

3. The rise of CITs holding annuities and private-credit instruments

Cunningham threatens all of these. H.R. 6084 gives them breathing room.

Why Fine? Why Now?

If you were drafting the perfect congressional messenger for this mission, you’d want someone who:

Is brand-new to Congress (not yet publicly tied to legacy retirement-policy positions).

Has a baked-in donor base from high-net-worth finance circles.

Has strong ideological credentials that shield them from intra-party criticism.

Is ambitious and eager to prove usefulness to leadership and donors.

Is aligned with a donor ecosystem where Wall Street capital and pro-Israel politics overlap heavily.

That person is Randy Fine.

He may not fully grasp the ERISA implications of his own bill. But his donors do. His committee allies do. And the financial-services industry absolutely does.

The Real Stakes: Cunningham v. Cornell Opens the Door—Fine Tries to Shut It

By shifting the pleading burden in prohibited-transaction cases back onto defendants, the Supreme Court restored the design of ERISA §406: to presume such transactions are improper unless proven otherwise.

If Congress now steps in to create a heightened pleading standard or a discovery stay, the result is predictable:

Annuity issuers avoid discovery into spread-based compensation.

Private-equity platforms avoid discovery into opaque fee structures.

Recordkeepers avoid discovery into revenue-sharing and “soft-dollar” conflicts.

Crypto custodians and fintech platforms avoid discovery into payments for distribution or platform placement.

And plan participants lose the oversight mechanism that ERISA was designed to provide.

Conclusion: Cunningham Opened a Door—Randy Fine is Trying to Close It for the Donors Who Stand to Lose

Whether or not Randy Fine personally understands the depth of ERISA fiduciary duties is almost beside the point.

What matters is this:

Cunningham v. Cornell made it easier to sue financial institutions for conflicted 401(k)/403(b) arrangements.

The industries most threatened—annuities, private equity, crypto, recordkeepers—have deep donor overlap with the Republican Jewish Coalition’s finance-heavy donor network.

RJC-PAC is one of Fine’s largest political benefactors.

Fine is now carrying a bill that would protect those donors’ industries by weakening ERISA enforcement.

This is not a coincidence. It is the normal, predictable machinery of American political economy.

And it is a reminder: Follow the money, and ERISA policy suddenly makes perfect sense.

Update 12/19/25— Fine Bill appears to be Dead on Arrival, Encore Fiduciary Conflict, and What This Means for Fiduciary Risk & Litigation

Thankfully such a blatant sellout to Private Equity, Annuities and Crypto was too much for a narrow majority to kill such legislation.

Since the original post on Rep. Randy Fine’s bill to effectively roll back the Cunningham v. Cornell University Supreme Court decision, additional context has emerged that underscores both the conflict-of-interest dynamics at play and the likely litigation response from plaintiff fiduciary lawyers.

1) Encore Fiduciary & Aronowitz: A Clear Conflict of Interest

The firm Encore Fiduciary — whose leadership until recently included Daniel Aronowitz, now Presidentially nominated to lead the Employee Benefits Security Administration (EBSA) — has publicly positioned itself as an advocate against ERISA litigation, calling for an end to what it terms “regulation by litigation.” Aronowitz’s testimony before the Senate emphasized reducing fiduciary litigation and easing plan sponsor exposure, including in areas such as private equity and crypto investment lineups for 401(k) plans. planadviser.com

This background raises an obvious conflict of interest: Encore’s business model includes focusing on fiduciary liability insurance and underwriting against litigation risk. As the head of EBSA, Aronowitz has influence over the very enforcement regime that determines how prohibited transaction claims and fiduciary breaches are litigated or regulated. Advocating publicly against litigation — especially in cases like Cunningham/Cornell — aligns with Encore’s commercial interests as much as any public-policy rationale.

Indeed, Encore has published commentary suggesting that plaintiffs’ fiduciary lawsuits such as Cornell are “frivolous” and constitute “litigation abuse” — arguing for heightened pleading standards to block access to discovery in prohibited transaction claims. Encore Fiduciary

That stance dovetails neatly with Fine’s bill (H.R. 6084, the ERISA Litigation Reform Act), which similarly seeks to raise barriers to prohibited transaction claims — effectively insulating annuities, private equity, recordkeeping arrangements, and crypto custodial arrangements from early litigation exposure. The CommonSense 401k Project The alignment between Encore’s advocacy and a sitting EBSA nominee — pushed by Fine’s caucus office — underscores that this is not a neutral policy debate but one deeply entangled with provider economic interests.

2) The Cunningham v. Cornell University Decision: Why Industry Feared It

The April 2025 Cunningham decision was unanimous (9–0) and significantly shifted the legal landscape by lowering the pleading standard for ERISA §406 prohibited transaction claims. Under Cunningham, plaintiffs no longer need to plead that a plan’s transaction lacked a statutory exemption before discovery proceeds; instead, claiming a prohibited transaction — including with a party-in-interest — is sufficient to get past initial motions. Supreme Court

This matters enormously for annuities and other insurance products. Annuities are per se transactions with parties in interest. Before Cunningham, industry defendants could often get prohibited transaction claims dismissed before discovery by arguing that a §408 exemption applied. Cunningham now means fiduciaries and insurers must plead and prove exemptions after discovery, increasing litigation risk, cost, and settlement leverage for plaintiffs.

That risk is precisely why firms like Encore have framed prohibited transaction suits as “absurd” or “frivolous,” and why Fine’s bill would reverse that dynamic by raising pleading thresholds and limiting early lawsuits. But critics argue such proposals would effectively immunize product vendors and fiduciaries from meaningful fiduciary accountability — contrary to ERISA’s protective purposes.

3) Why Fine’s Bill Is Likely Dead on Arrival (and What It Signals)

On its face, H.R. 6084 is so egregious — a legislative attempt to insulate Wall Street product vendors from fiduciary scrutiny — that it is unlikely to pass outside of a narrow party majority. Fine’s sponsorship of this bill is telling precisely because he is not a retirement policy expert; his political profile is dominated by cultural and geopolitical issues, not ERISA law. That suggests his sponsorship is not driven by substantive policy consensus, but by donor and industry networks that benefit from limiting ERISA litigation exposure. The CommonSense 401k Project

This dynamic mirrors why some industry actors openly oppose Cunningham — not because it undermines retirement plan administration, but because it makes it easier for plaintiffs to challenge products like annuities under ERISA’s prohibited transaction framework.

4) Implications for Annuity & Prohibited-Transaction Litigation

If Cunningham stands and the Fine bill falters, the litigation environment for prohibited transaction and fiduciary breach suits around annuities looks increasingly active:

Plaintiffs can now more easily survive early dismissal — gaining discovery into annuity pricing, spread profits, conflicts, and exemption defenses. Supreme Court

Increased discovery and lower pleading thresholds make it cost-effective for fiduciary lawyers to pursue cases involving annuities in 401(k) plans, especially where exemptions are routinely claimed without justification.

The industry’s public push to weaken litigation standards inadvertently signals heightened litigation risk, as plan participants and fiduciary attorneys see Cunningham as a green light to pursue cases that previously stalled at the pleadings stage. Sidley Austin

In effect, the very sector that wants to discourage prohibited transaction lawsuits — including annuity issuers and fiduciary insurers — is under pressure from participants and courts to justify their exemptions and fiduciary processes on the merits rather than avoiding discovery.

5) Broader Policy Context: Alternatives and Risk Resistance

This legislative tussle also intersects with broader regulatory movements pushing alternative assets such as private equity and cryptocurrencies into DC plans. Recent executive orders and regulatory proposals have directed agencies to consider cryptocurrency and private equity as 401(k) investment options, framing them as “competitive” and “diversification enhancing” even though most participants express little interest once risks and fees are explained. LinkedIn

Senators from both parties have sounded alarms about exposing retirement plans to these risky assets, warning they lack transparency and traditional investor protections. Senate Banking Committee

The contrast could not be starker: while industry and some political actors push to broaden product menus to include high-risk assets, courts and participant advocates are pushing back via **fiduciary litigation — particularly prohibited transactions — to ensure products genuinely benefit participants rather than vendors.

Bottom Line

The controversy around Rep. Fine’s bill and the public positioning of Encore Fiduciary’s leadership reflect an industry backlash to the Supreme Court’s Cunningham decision — a backlash driven not by participants’ interests but provider risk mitigation. Rather than weakening ERISA enforcement, this episode is likely to spur more fiduciary litigation, especially around annuities and other non-transparent products that have long escaped rigorous prohibited transaction scrutiny.

**APPENDIX

Why a Pro-Business Supreme Court Ruled Unanimously in Cunningham —

And Why the Fine Bill May Be Doomed by ERISA’s Own Architecture**

There is an apparent contradiction that has puzzled many ERISA lawyers: Why would a Supreme Court that is widely described as “pro-business” issue a unanimous opinion in Cunningham v. Cornell that makes it easier for plaintiffs to sue plan fiduciaries and service providers?

A deeper look at the Court’s ERISA jurisprudence reveals the answer

Thole v. U.S. Bank (2020) shut down DB plan standing so aggressively that the Court had to preserve standing and enforcement power in defined-contribution (DC) plans.

And once you understand that logic, the Randy Fine bill looks not only dangerous — but possibly unconstitutional or structurally impossible under ERISA.

1. Thole v. U.S. Bank: The Court Closed the Door in DB Plans

In Thole v. U.S. Bank (2020), the Supreme Court held 5–4 that defined-benefit (DB) participants lack Article III standing to sue for fiduciary breaches unless they can show an immediate financial loss.

Because DB benefits are fixed and guaranteed (unless the plan collapses), the Court reasoned that mismanagement doesn’t necessarily injure individual participants.

It was a massive win for employers, private-equity-heavy pension portfolios, and corporate de-risking strategies.

But it created a structural problem.

Thole wiped out ERISA fiduciary enforcement in DB plans.

plan fiduciaries suing themselves (never happens), or

criminal cases (extremely rare).

The Court knew what it had done.

2. Cunningham v. Cornell: The Court Had to Leave the DC Door Open

Fast-forward to 2025.

Cunningham v. Cornell arrives — focusing on §406(a)(1)(C) prohibited-transaction claims in 403(b)/DC plans.

The question: Must plaintiffs plead and disprove an exemption (408) at the motion-to-dismiss stage?

The Second Circuit said yes. The Supreme Court unanimously said no.

Why?

Because if the Court had closed off §406 claims in DC plans the same way it closed DB standing in Thole, ERISA enforcement would be nearly dead.

Cunningham is the “counterweight” to Thole.

Once Thole gutted DB enforcement, the Court had to preserve DC standing and DC prohibited-transaction claims to keep ERISA’s structure constitutional and functional.

Some key doctrinal reasons:

ERISA §406 is designed to be strict-liability unless an exemption is proven. The burden is on fiduciaries — not participants.

Congress intended broad enforcement in DC plans because participant accounts rise or fall based on fiduciary conduct.

If both DB and DC plan enforcement vanished, ERISA’s protective purpose would be nullified, contradicting 29 U.S.C. §1001 and decades of precedent.

Thus, the Court ruled 9–0 to preserve basic DC enforcement.

This is the only position that keeps ERISA’s statutory scheme coherent.

3. Cunningham Wasn’t “Anti-Business” — It Was Doctrinal Maintenance

The Justices weren’t siding with plaintiffs. They were preserving:

statutory interpretation integrity,

the §406/§408 burden structure,

constitutional standing doctrine, and

the basic idea that DC participants must have a remedy.

Even the Court’s staunchest “pro-business” members (Alito, Gorsuch, Roberts) signed on because ERISA’s architecture left no other legal option.

To rule the other way would have:

broken ERISA’s strict-liability structure,

inverted burdens of proof contrary to the text,

expanded Thole into DC plans (unthinkable), and

left ERISA practically unenforceable.

Which brings us to the new bill.

4. Why the Randy Fine Bill May Be Impossible to Implement Under ERISA

Some ERISA attorneys are already saying quietly what you’re saying loudly:

H.R. 6084 may be unworkable or even unconstitutional because it would violate ERISA’s core structural principles — the very principles the Supreme Court just reaffirmed in Cunningham.

Problems with the Fine bill:

(1) It tries to reverse the burden of proof Congress placed on fiduciaries.

ERISA §406 presumes transactions with parties in interest are prohibited. The defendant must prove reasonableness under §408.

H.R. 6084 tries to force plaintiffs to disprove a §408 exemption before discovery — exactly what the Supreme Court rejected.

(2) It would undermine basic trust-law foundations.

ERISA’s fiduciary scheme is explicitly built on trust law, where fiduciaries carry the burden to justify conflicted transactions.

Congress cannot legislate away the trust-law core without rewriting ERISA from scratch.

(3) It could violate Article III by stripping remedies.

If both DB (Thole) and DC (under H.R. 6084) claims lack meaningful enforcement, courts could find the statute constitutionally deficient.

(4) It directly contradicts the unanimous statutory interpretation in Cunningham.

The Supreme Court’s reasoning is built on the text — not on policy:

Exemptions are affirmative defenses.

Plaintiffs do not need to plead them.

Burden is on fiduciaries.

H.R. 6084 would flip all of that, setting itself up for immediate judicial invalidation.

(5) It conflicts with ERISA’s remedial purpose in §1001.

Congress explicitly declared the purpose of ERISA is to provide “ready access to the Federal courts” and “adequate remedies.”

A law closing off both DB and DC enforcement could violate Congress’s own statutory preamble unless rewritten wholesale.

5. The Bottom Line: The Supreme Court Already Told Congress What It Can’t Do

Thole closed DB standing.

Cunningham kept DC standing alive because otherwise ERISA enforcement collapses.

The Fine bill aims to do indirectly what the Court explicitly said plaintiffs don’t need to do.

For that reason, the bill is likely dead on arrival in the courts, even if it passed legislatively.

Put bluntly:

If Congress passed H.R. 6084, it would almost certainly be struck down as violating ERISA’s structure, statutory text, and basic trust-law principles reaffirmed unanimously in Cunningham.

Some employer-side attorneys already know this. Some are quietly admitting it. Others are hoping no one notices.

Appendix: The Two-Step ERISA Rollback Strategy Behind “Democratizing Alternatives”

How the Wagner White Paper and Encore’s “Higher Pleading Standard” Campaign Work Together to Protect Private Equity, Annuities, and Crypto

Your main post explains why Rep. Randy Fine’s bill (H.R. 6084) is best understood as a Cunningham counterstrike—a legislative attempt to re-raise the barrier to prohibited-transaction cases by requiring more detail up front and restricting discovery. The CommonSense 401k Project This Appendix adds an important framing: the policy ecosystem is not just legislative. It is also being built through “thought leadership” legal memos that normalize alternatives in DC plans and describe ERISA’s prohibited-transaction design as a litigation “problem” to be fixed.

Two recent examples show the full architecture:

Wagner Law Group White Paper: normalize private equity/alternatives as prudent “portfolio modernization” and promise future “safe harbors” and reduced litigation uncertainty.

Read together, they are a two-step strategy to strip ERISA’s effective bite without openly repealing ERISA.

Step One: Wagner’s “Permission Structure” for Private Equity and Alternatives in 401(k)s

The Wagner white paper is framed as neutral “fiduciary considerations,” but its practical effect is to legitimize and operationalize the expansion of private equity, private debt, crypto-related vehicles, real estate, infrastructure, and annuity/lifetime-income structures inside DC plans.

A. It leans heavily on Executive Order policy signals—without grappling with ERISA’s statutory prohibitions

Wagner’s opening premise is that a White House action “signals” a more favorable environment and directs agencies to create safe harbors and reduce legal uncertainty.

WagnerWhitePaperAlternativeInve…

But executive orders and agency tone shifts don’t change ERISA §406. They can repackage the narrative, but they can’t repeal the statute.

B. It treats DOL “neutrality” as a green light

Wagner highlights the DOL’s rescission of the 2021 supplemental statement as a return to a “neutral, principled-based approach.”

WagnerWhitePaperAlternativeInve…

That’s exactly the rhetorical move product manufacturers need: “We’re not endorsing—just being neutral.” In practice, “neutrality” becomes a distribution strategy for opaque, high-fee structures.

C. It moves the debate into §404 “prudence process” and away from §406 “prohibited transaction”

Wagner repeatedly emphasizes that the “duty of prudence is assessed based on processes, not outcomes,” using Intel/Natixis to steer fiduciaries toward documenting committee steps.

WagnerWhitePaperAlternativeInve…

But process formalism is the wrong center of gravity for many alternative structures, because the core issue is often structural conflicts and compensation—i.e., §406 prohibited transactions—where “good process” does not legalize an inherently conflicted arrangement.

D. It acknowledges liquidity and valuation problems—then downplays them into “manageable considerations”

Wagner concedes the obvious: liquidity mismatch and valuation are central risks (stale marks, true-ups, lagged valuations, “hard to value” assets).

WagnerWhitePaperAlternativeInve…

It even explains that plan-level funds may rely on valuation reports with lags (e.g., quarterly with a 30-day lag) and face “true-up” risk later.

WagnerWhitePaperAlternativeInve…

But it frames these as technical process issues (“hire valuation agents”) rather than the core enforcement problem: once you embed products that cannot be independently priced daily, you are effectively asking participants to accept manager-controlled mark-to-model NAVs—the same mechanism that makes benchmarking and accountability collapse.

Bottom line of Step One: Wagner supplies a legal-professional narrative that tells plan fiduciaries: you can do this, just document it, hire experts, and watch for safe harbors.

WagnerWhitePaperAlternativeInve…

Step Two: Encore’s Campaign to Make ERISA Prohibited-Transaction Claims Harder to Bring (and Much Harder to Discover)

Encore’s December 18, 2025 post is explicit: it argues that Congress must “fix” the Cunningham pleading framework by raising the pleading standard and limiting access to discovery. Encore Fiduciary

A. Encore defines the problem correctly—then frames the solution as “litigation reform,” not ERISA compliance

Encore complains that after Cunningham, “the mere allegation that a plan hired a service provider…is enough to survive a motion to dismiss” if the complaint also says fees were too high. Encore Fiduciary But that is not a bug in ERISA. It is ERISA’s design:

§406 treats conflicted transactions as presumptively improper

§408 exemptions are affirmative defenses

discovery is often the only way participants can prove hidden compensation and conflicts

B. Encore ties its argument directly to Fine’s bill and the goal of overriding Cunningham

Encore explicitly says Fine’s bill would “override” Cornell/Cunningham and describes it as addressing a “must-fix” problem. Encore Fiduciary That aligns precisely with the mechanism you describe in the Fine post: raise barriers, stay discovery, and blunt §406 suits targeting annuities, PE platforms, recordkeepers, and crypto custody. The CommonSense 401k Project

C. Encore’s “unworkable law” claim is really a defense of hidden economics

Encore argues the law becomes “unworkable” if hiring a service provider triggers discovery pressure. Encore Fiduciary But the reason defendants fear discovery is not because ERISA is irrational. It’s because discovery is where you find:

spread-based compensation in annuities / stable value

revenue-sharing and platform payments

affiliate deals, cross-subsidies, and “free” services funded elsewhere

opaque valuation practices and fee layering

conflicts buried in non-core options, managed accounts, custom TDF unitization, and CIT wrappers

In short: Encore is attacking the enforcement pathway precisely because the enforcement pathway reveals the economics.

Why the Two Pieces Fit Together: “Expand First, Disarm Enforcement Second”

Seen as a system, Wagner + Encore map onto a predictable playbook:

1) Normalize and distribute opaque products into DC plans

That is how you “strip ERISA” without formally repealing it: keep the statute on paper, but remove the functional ability to enforce it.

The Key Contradiction You Should Highlight

Wagner admits alternatives bring:

fee opacity

liquidity mismatch

valuation subjectivity and stale marks

WagnerWhitePaperAlternativeInve…

Encore simultaneously argues courts should make it harder for plaintiffs to get discovery unless they plead more specific facts up front. Encore Fiduciary

But plaintiffs often cannot plead “specific facts” about valuation manipulation, revenue sharing, spread profits, and affiliate payments until they get discovery, because those facts are controlled by the defendants and hidden behind:

proprietary fee schedules and revenue-sharing arrangements

So the combined message becomes:

“We want to move more complex, harder-to-value, harder-to-disclose products into 401(k)s… and also make it harder for participants to use litigation to learn what those products really cost and how they really work.”

That is not “democratizing access.” It is democratizing exposure while privatizing information.

Appendix: The Two-Pronged Campaign to Mainstream Alternatives and Disable ERISA Enforcement

(Wagner “Alternatives in 401(k)s” white paper + Encore’s HR 6084 / pleading-standard push)

This appendix is designed to bolt onto your November 29, 2025 post on Rep. Randy Fine’s bill and Cunningham. It shows how two seemingly separate “thought leadership” streams are actually complementary parts of the same policy machine:

Wagner Law Group provides the “how-to” legal memo for injecting private equity / private credit / crypto / real estate / annuities into participant-directed plans—by reframing everything as a §404 “prudence/process” discussion and leaning heavily on Trump’s Executive Order 14330 and prospective “safe harbors.”

Encore Fiduciary provides the “litigation shield” narrative—arguing that Cunningham made ERISA “unworkable” and demanding Congress raise pleading standards and stay discovery so prohibited-transaction cases die before plaintiffs can obtain the very evidence (fees, side payments, spreads, valuation inputs, affiliate deals) that proves conflicts.

Put plainly: first normalize alternatives in 401(k)s, then neuter the enforcement mechanism that would expose how those alternatives actually pay.

A. Wagner’s Paper: “Process” as a Substitute for Legality

1) The core framing problem: “prudence theater” instead of §406 analysis

Wagner sets the stage by celebrating a “more favorable regulatory environment” for “Investment Solutions that incorporate alternative investments.”

WagnerWhitePaperAlternativeInve…

But notice what disappears in the paper’s architecture: ERISA §406’s per se prohibitions and the real-world implication of Cunningham (burden shifts; exemptions are affirmative defenses; discovery becomes the battleground). Instead, Wagner repeatedly presents alternatives as a matter of:

prudent selection

monitoring

documentation

“key considerations” (fees, valuation, liquidity)

…as if a “good process” can cure a structurally conflicted transaction.

That is the same conceptual error you’ve flagged repeatedly in your prohibited-transaction writing: §404 process cannot legalize a prohibited transaction under §406.

2) Executive Order 14330 as a rhetorical lever (not a legal change)

Wagner leans hard on Trump’s Executive Order 14330 and, critically, highlights the EO’s directive to develop “appropriately calibrated safe harbors” and to “curb ERISA litigation.”

WagnerWhitePaperAlternativeInve…

That’s not neutral fiduciary education—it is policy advocacy language that presumes litigation is the problem, not conflicted compensation.

And Wagner’s “watch for pending safe harbor guidance” framing nudges fiduciaries to behave as if future administrative safe harbors will sanitize what is, in many settings, a current statutory problem.

Wagner explicitly pitches alternatives via target-date suites, managed accounts, and custom TDFs, including the use of “Non-Core Options” that participants don’t directly select.

WagnerWhitePaperAlternativeInve…

This is the practical playbook for what you’ve been calling laundering:

bury fee layers

obscure benchmarks

disconnect participants from line-of-sight holdings

reduce accountability through “unitization” and valuation smoothing

Wagner treats this as operational sophistication. Your framework treats it as transparency regression by design—especially dangerous after Cunningham, because the entire point of §406 pleading is to open discovery into exactly these hidden arrangements.

B. Encore’s Argument: Rewrite Pleading Rules So §406 Can’t Function

That’s not an “ERISA crisis.” That is ERISA functioning as written: §406 presumes certain transactions are suspect; §408 exemptions are defenses to be proven by defendants.

1) Encore’s thesis (in their words): discovery is the enemy

Encore complains that Cunningham gives plaintiffs “a free pass to discovery every time that a plan hires a service provider,” creating pressure to settle. Encore Fiduciary

But for alternatives/annuities/crypto/CITs, discovery is not a nuisance—it is the only tool participants have to uncover:

indirect compensation

spread profits

revenue sharing / platform payments

affiliate self-dealing

valuation inputs and “true-up” practices

gate/redemption discretion and side letters

In other words, Encore is openly describing a world where plans can transact in opaque, conflicted markets without the risk of having to produce documents early.

2) The HR 6084 mechanism: shift the burden back to plaintiffs

Encore praises HR 6084 (Fine’s ELRA) because it would require plaintiffs to plead and prove that a transaction does not qualify for the §408(b)(2) “reasonable compensation” exemption—at the motion-to-dismiss stage.

Encore also notes the bill would “generally stay discovery until after a motion to dismiss is ruled on.”

That combination is the whole trick:

Plaintiffs must allege non-exemption facts

But plaintiffs can’t access the facts because discovery is stayed

Result: de facto immunity for opaque compensation models

This is especially potent for private equity, private credit, annuities, and crypto custody, because the most important economic evidence is not public and often not meaningfully disclosed to participants.

3) “Frivolous” is a marketing label, not a legal analysis

Encore repeatedly characterizes these cases as “baseless” or “frivolous,” including Cornell itself. Encore Fiduciary+1

But the Supreme Court was explicit that the statute’s structure compels the burden allocation—and Encore admits that, too, while blaming Congress for writing ERISA that way. Encore Fiduciary

So what Encore is really saying is: ERISA’s design is inconvenient for the plan sponsor / service provider market, therefore Congress should redesign it.

That is precisely why this belongs in your Randy Fine narrative.

C. How the Two Pieces Fit Together: “Open the Door to Alternatives, Close the Courthouse Door”

Here’s the combined logic chain you can state plainly in your post:

Wagner tells fiduciaries: the White House wants alternatives in 401(k)s; DOL is moving back to “neutrality”; safe harbors are coming; proceed with a prudent process.

WagnerWhitePaperAlternativeInve…

WagnerWhitePaperAlternativeInve…

Encore tells Congress: Cunningham makes it too easy to sue; discovery is the problem; raise pleading standards; stay discovery; force plaintiffs to plead away exemptions. Encore Fiduciary+1

Randy Fine’s HR 6084 operationalizes Encore’s wish list while the Trump EO provides the policy “wind at the back” for the Wagner “how-to memo” ecosystem. The CommonSense 401k Project+1

Net effect: alternatives get distributed more widely, while ERISA enforcement becomes harder precisely where opacity is greatest.

That is not “democratizing access.” It is democratizing fee extraction.

D. Closing

Wagner’s white paper is the polite, professionalized version of the sales pitch: “Don’t worry—just document the process, and the regulatory winds are shifting.”

WagnerWhitePaperAlternativeInve…

Encore’s blog is the hard-edged political version: “Don’t allow discovery—raise pleading standards—make plaintiffs plead away exemptions up front.” Encore Fiduciary+1 Together they reveal the real strategy behind the Fine bill: expand distribution channels for private equity, annuities, and crypto wrappers inside 401(k)s and then strip participants of the only practical enforcement tool that can expose hidden compensation and conflicts after Cunningham.

The Wagner paper functions less as neutral fiduciary analysis and more as a legal normalization memo for private equity and alternatives in DC plans. Its core flaws are:

Treating ERISA §404 prudence as the controlling standard while largely ignoring ERISA §406 prohibited transactions

Framing private equity risk as a disclosure and process problem rather than a structural illegality

Relying on executive orders and agency tone shifts as if they could override statute