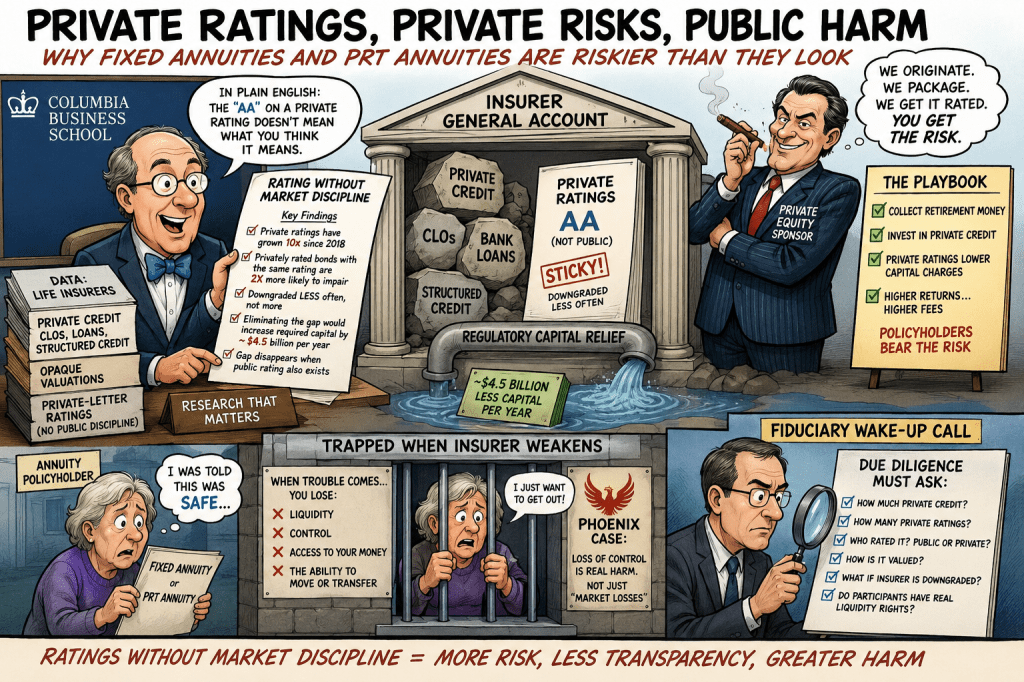

A new Columbia Business School paper, Rating Without Market Discipline, may become one of the most important academic papers in the debate over private credit, insurance company solvency, fixed annuities, and pension risk transfer annuities.

The paper’s core finding is devastatingly simple: private ratings appear to understate credit risk. That matters because life insurers increasingly hold opaque private credit, structured credit, CLOs, bank loans, and privately placed securities on their balance sheets. These assets are often treated as high-quality investment-grade assets for regulatory capital purposes. But Columbia finds that privately rated insurer bonds with the same rating as publicly rated bonds are roughly twice as likely to suffer impairments — and are downgraded less often, not more.

That is the worst possible combination.

It means the rating is not merely optimistic. It is sticky. It fails to move when the credit is deteriorating. In plain English, the insurer gets the benefit of a high rating for capital purposes while the real economic risk is higher than the rating suggests.

This finding goes directly to the heart of the private credit debate. The private credit industry has repeatedly claimed that its loans and structured assets are safe, senior, secured, carefully underwritten, and conservatively valued. But the Columbia paper shows that when private credit-type instruments move into insurance company balance sheets and are rated through private-letter channels, the ratings may not carry the same information as public ratings. The “AA” or “A” label may not mean what ordinary investors, fiduciaries, or retirees think it means.

That is a market-shaking finding.

It is especially important because the paper focuses on life insurers — the same institutions now selling fixed annuities, general account stable value products, registered index-linked annuities, group annuity contracts, and pension risk transfer annuities. These products are often marketed as safe because they are backed by insurance company balance sheets. But if the assets inside those balance sheets are increasingly private, opaque, self-priced, privately rated, and potentially overrated, then the safety claim becomes much weaker.

This also strengthens the argument made in the Phoenix/LPL litigation context. The risk in annuity products is not only whether the underlying investments “go to zero.” The risk is that policyholders and retirement plan participants become trapped inside an insurer balance sheet when the insurer weakens, enters rehabilitation, or loses liquidity. Participants may lose the ability to surrender, transfer, exchange, or reposition assets even before a traditional “principal loss” appears.

The Columbia paper makes that risk easier to prove.

For years, insurers have pointed to ratings and regulatory capital as proof that general account annuities and PRT annuities are safe. But Columbia shows that the ratings themselves may be part of the problem. If a large portion of the insurer’s supposedly high-grade portfolio depends on private ratings without market discipline, then fiduciaries cannot simply rely on the insurer’s headline rating, statutory capital ratio, or NAIC treatment.

The most important fiduciary takeaway is this:

A fixed annuity is not just a conservative bond fund. A PRT annuity is not just a pension check with an insurance wrapper. Both are concentrated credit exposures to an insurance company whose balance sheet may contain hard-to-value private credit assets that are rated through channels lacking public market discipline.

This is particularly dangerous for 401(k) and pension fiduciaries because participants do not negotiate the insurer’s investment policy, cannot inspect private ratings, cannot value opaque private credit holdings, and usually do not receive meaningful downgrade escape rights. They are told the product is safe because it is issued by an insurance company. Columbia shows why that assumption is no longer good enough.

The paper also helps explain why private equity-owned insurers deserve special scrutiny. Columbia finds private ratings are concentrated among large insurers, high-yield tilted insurers, and private equity-owned insurers. That fits the broader concern that private equity has turned insurance balance sheets into financing engines for private credit. The insurer collects retirement money. The affiliated or related asset manager originates or packages private credit. Private ratings help lower capital charges. The policyholder or retiree bears the hidden credit and liquidity risk.

That is not ordinary insurance regulation. That is regulatory arbitrage.

The paper is also important for pension risk transfers. In a PRT transaction, a plan sponsor moves pension obligations from an ERISA-protected pension plan to an insurer. The transaction is sold as “de-risking.” But if the insurer’s balance sheet is increasingly supported by privately rated credit that is less safe than its rating indicates, the transaction may simply replace transparent pension risk with opaque insurer credit risk.

This should change the fiduciary due diligence standard. Fiduciaries evaluating fixed annuities, general account stable value contracts, or PRT annuities should ask:

Are the insurer’s “AA” assets really AA?

How much of the insurer’s bond portfolio relies on private-letter ratings?

How much is private credit, CLOs, structured credit, bank loans, or affiliate-originated assets?

Who rated those assets?

Were they publicly rated or privately rated?

Are the assets priced by observable market inputs or by models, brokers, affiliates, or the insurer itself?

What happens if the insurer is downgraded?

Do participants have real liquidity rights, or are they trapped?

The Columbia paper provides academic support for a commonsense conclusion: private credit cannot be treated as safe simply because an insurer, private rating agency, or regulator assigns it a high-grade label. Ratings without market discipline are not the same as ratings tested by public markets.

That finding is enormously important for ERISA litigation, annuity fiduciary reviews, PRT due diligence, and the broader debate over private credit in retirement plans.

The insurance industry has long argued that fixed annuities and PRT annuities are safe because insurers are highly regulated and conservatively capitalized. Columbia’s paper shows the flaw in that defense. Regulation may require a rating, but it cannot create the market discipline that makes the rating reliable.

That is the bridge between private credit and annuity risk.

If the assets backing annuities are overrated, opaque, illiquid, and slow to be downgraded, then the annuity itself is riskier than advertised. The danger is not just volatility. The danger is hidden credit deterioration that remains invisible until policyholders discover they cannot get their money out.

Phoenix showed what happens when annuity owners lose control.

Columbia shows why the balance sheets backing modern annuities may be far riskier than the ratings suggest.

Li, Xuelin and Oh, Sangmin and Ricciardi, Giacomo, Rating Without Market Discipline (May 31, 2026). Columbia Business School Research Paper, Available at SSRN: https://ssrn.com/abstract=6859158

Typical well done Chris Tobe analysis!

Yahoo Mail: Search, Organize, Conquer

LikeLike