I have expressed concern over Morningstar’s promotion of annuity products. https://commonsense401kproject.com/2026/01/27/morningstar-the-referee-who-designs-the-insurance-playbook/

Recently, Morningstar published an insurance industry-friendly report, “Evaluating Target-Date Strategies With Annuities” https://www.morningstar.com/content/cs-assets/v3/assets/blt9415ea4cc4157833/bltd9e4637261d27afb/6a07705cbf17f75ee4e5f1c6/Evaluating_Target_Dates_with_Annuities.pdf

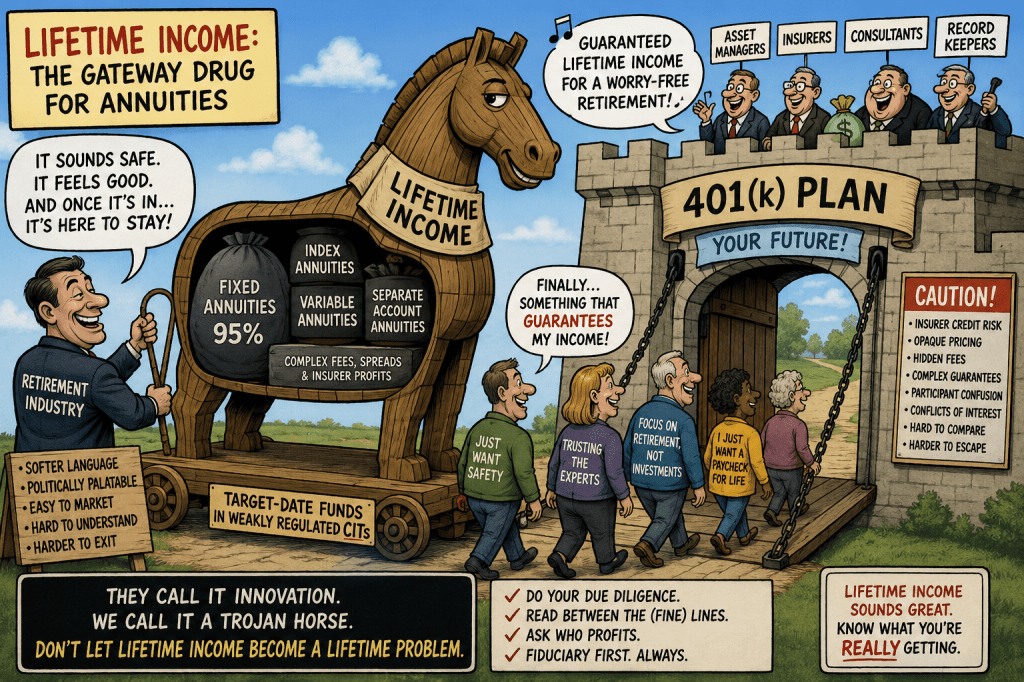

For years, the retirement industry struggled to push annuities into 401(k) plans. Participants distrusted them. Fiduciaries worried about liability. Regulators remained cautious. Traditional mutual fund structures and SEC accounting rules created barriers around valuation, liquidity, leverage, and fee transparency.

So the industry changed the marketing.

Instead of selling “fixed annuities” or “index annuities,” it began selling “lifetime income.”

That phrase is politically brilliant. Nobody wants to argue against retirees having dependable income. But behind the softer language sits the same insurance-driven business model that has long dominated retail annuity sales: opaque pricing, embedded spreads, insurer credit risk, weak benchmarking, and conflicts of interest between insurers, consultants, recordkeepers, and product manufacturers.

The Morningstar report “Evaluating Target-Date Strategies With Annuities” unintentionally exposes how rapidly this transformation is occurring.

Morningstar reports that assets in target-date strategies with annuities reached $44 billion by March 2026, while broader multi-asset portfolios with embedded annuities surpassed $115 billion. The report presents this as innovation. In reality, it represents the institutionalization of insurance products inside default retirement structures where most participants will never understand the underlying risks.

The retirement industry understands something very important: once insurance products get into the Qualified Default Investment Alternative (QDIA), they become extraordinarily sticky. Participants rarely move money out of default target-date funds. That makes target-date funds the perfect Trojan horse for embedding annuity structures into retirement plans.

The insurance industry could never successfully convince millions of participants to voluntarily buy retail fixed annuities one by one inside their 401(k). But it may not need to. If insurers can get annuity components embedded inside target-date funds, particularly inside weakly state regulated Collective Investment Trusts (CITs), the battle is largely won.

The industry’s public narrative focuses heavily on “lifetime income” target-date products. But when you examine actual plan assets over $100 million, a very different picture emerges. The overwhelming majority of annuity balances inside plans are still traditional fixed annuities and general account products. In my review of large plans, roughly 95% of annuity-related assets remain concentrated in fixed annuities, with variable annuities, index annuities, separate account annuities, and newer lifetime income structures making up only a small fraction of balances.

That distinction matters.

The industry uses lifetime income products as the politically acceptable entry point because they sound safer, more participant-friendly, and more fiduciary-oriented. But once fiduciaries and regulators normalize insurance structures inside target-date funds, the door opens for broader use of insurance products across the entire defined contribution system.

Morningstar itself acknowledges many of the underlying problems, even while promoting the category.

The report concedes that evaluating these products requires analyzing insurer financial strength, liquidity constraints, opaque payout structures, valuation complications, and participant confusion. It openly admits that participants may not understand the products and that complexity creates a major fiduciary challenge.

The report also admits that many products have no transparent fee disclosure because costs are embedded inside payout structures rather than explicit expense ratios. This is one of the oldest tricks in the annuity industry: hide compensation and spreads inside insurance pricing rather than clear investment management fees.

Even more troubling is the paper’s discussion of valuation.

Morningstar states that these products generally avoid the valuation concerns associated with private markets because they still provide daily NAV pricing. But this completely misses the real issue. Daily NAV pricing does not eliminate valuation risk when the underlying guarantees, insurer obligations, private credit exposures, and embedded spreads are themselves difficult to independently value.

This is precisely why SEC mutual fund structures historically limited these kinds of insurance and alternative structures. Traditional SEC frameworks evolved over decades to address problems involving liquidity, leverage, valuation, affiliated transactions, and hidden compensation.

Weakly state regulated CIT structures increasingly bypass those protections.

That is why the target-date fund wrapper matters so much. Once annuity structures move into CITs rather than SEC mutual funds, insurers and asset managers gain significantly more flexibility around valuation methods, disclosure standards, and underlying holdings. The result is a retirement system moving away from transparent publicly traded securities and toward opaque insurance-based structures that participants cannot realistically monitor.

Morningstar’s paper also highlights another critical issue: conflicts of interest.

The report repeatedly suggests that plan sponsors may need to rely on the same asset managers selling these products to evaluate whether the pricing and guarantees are reasonable. That is not independent fiduciary analysis. That is product manufacturers grading their own homework.

This is especially dangerous because many of the largest firms promoting these structures simultaneously operate across multiple layers of the ecosystem: asset management, insurance manufacturing, consulting relationships, recordkeeping partnerships, CIT administration, managed accounts, and annuity distribution.

The industry calls this “innovation.” In practice, it increasingly resembles vertical integration around opaque retirement products.

The deeper issue is philosophical.

For decades, the retirement system largely operated through transparent securities markets governed by SEC rules emphasizing disclosure, comparability, liquidity, and independent valuation. The new retirement model increasingly shifts toward insurance-based promises backed by insurer balance sheets, private credit portfolios, structured products, and actuarial assumptions that ordinary participants cannot evaluate.

The retirement industry is not merely adding “income solutions.” It is changing the architecture of the 401(k) system itself.

And the public should understand where this road leads.

History shows that whenever financial firms are permitted to combine opaque accounting, hidden spreads, illiquid assets, and weak oversight, abuse eventually follows. We saw it in Executive Life. We saw it in AIG. We saw it in structured products before 2008. We are now watching similar structures migrate into retirement plans under the more politically acceptable language of “lifetime income.”

Lifetime income may sound comforting.

But fiduciaries should ask a more important question:

What exactly is sitting underneath the guarantee?

Addendum: Prohibited Transaction Risk, Litigation Exposure, and the Dangerous Mixing of Accounting Standards

The greatest risk in the current “lifetime income” movement may not be the annuity itself. The greater danger is the gradual collapse of consistent accounting and fiduciary standards inside the 401(k) system.

For decades, SEC mutual fund rules imposed relatively consistent standards around valuation, liquidity, diversification, leverage, affiliated transactions, fee disclosure, and performance reporting. These rules were not accidental. They evolved through repeated financial scandals involving opaque insurance products, hidden leverage, structured products, and conflicts of interest.

Today, the retirement industry increasingly seeks to bypass those standards through Collective Investment Trusts (CITs), insurance separate accounts, general account products, private credit structures, and embedded annuity arrangements. The result is a growing mismatch between the appearance of a traditional diversified retirement investment and the underlying economic reality.

This creates profound prohibited transaction and fiduciary concerns.

ERISA prohibited transaction rules exist because Congress recognized that financial firms operating inside retirement plans possess enormous incentives to steer participants into proprietary or affiliated products generating hidden compensation streams. When insurers, consultants, recordkeepers, target-date managers, and affiliated asset managers all participate economically from the same structure, the distinction between independent fiduciary advice and product distribution begins to disappear.

The Morningstar report repeatedly frames these products as ordinary target-date investments with an added insurance feature. But economically, many of these arrangements operate far closer to vertically integrated insurance distribution systems than traditional investment funds.

That distinction matters legally.

Once a retirement plan embeds insurer-backed guarantees inside a target-date structure, fiduciaries may inherit a wide range of risks not present in traditional public-market target-date funds:

• insurer insolvency risk

• general account credit risk

• liquidity restrictions

• valuation uncertainty

• opaque embedded spreads

• affiliated compensation structures

• private credit exposure

• actuarial pricing assumptions

• conflicts between participant interests and insurer profitability

These risks become even more serious when plans mix accounting regimes and regulatory standards inside a single retirement product.

A traditional SEC mutual fund historically could not easily hold many of the opaque insurance or alternative structures now appearing inside CIT-based target-date products. That was not regulatory oversight—it was often intentional regulatory restraint. SEC accounting frameworks generally demand clearer pricing, liquidity, diversification, and disclosure standards than weakly regulated state insurance structures or bank-trust CIT frameworks.

The modern retirement industry increasingly engages in what can fairly be called “accounting arbitrage.”

Private equity, private credit, insurance guarantees, stable-value contracts, and annuity structures are inserted into retirement vehicles operating under weaker disclosure and valuation standards while still being marketed to participants as if they were ordinary diversified investments comparable to SEC mutual funds.

This creates enormous litigation risk.

Plaintiffs’ firms increasingly understand that many of these structures may expose fiduciaries to prohibited transaction claims under ERISA Sections 406(a) and 406(b), particularly after Cunningham v. Cornell clarified that prohibited transaction claims should not be prematurely dismissed merely because a transaction appears common within the industry.

The legal problem for fiduciaries is straightforward:

If a plan fiduciary selects a product where insurers, consultants, recordkeepers, or affiliated managers receive indirect compensation streams, embedded spreads, proprietary distribution advantages, or affiliated revenue arrangements, courts may increasingly ask whether the fiduciary truly acted solely in participants’ interests or instead facilitated a conflicted transaction benefiting parties in interest.

The litigation danger is amplified because many of these products are extremely difficult to benchmark independently.

Morningstar itself acknowledges that meaningful benchmarking becomes difficult after annuitization and that sponsors may need to rely heavily on provider-generated assumptions and scenario analysis. That is precisely where fiduciary danger increases. When a product cannot be independently benchmarked using transparent market comparisons, proving prudence becomes substantially harder.

This is especially true for products with:

• implicit rather than explicit fees

• insurer-controlled payout assumptions

• embedded private credit exposure

• self-rated or weakly rated assets

• actuarial assumptions participants cannot evaluate

• illiquid structures lacking transparent market pricing

The retirement industry presents these developments as “innovation.” But many resemble the same structural problems that repeatedly appeared before prior financial crises: opaque valuation, hidden compensation, regulatory fragmentation, and products that become impossible for ordinary investors to understand.

The danger is not merely theoretical.

History shows that insurance-based structures can fail slowly and quietly before collapsing suddenly. Executive Life, AIG, structured products before 2008, and multiple failed annuity issuers all demonstrated how quickly supposedly stable guarantees can deteriorate when opaque assets, leverage, and accounting flexibility combine.

The irony is that many of these risks are now entering retirement plans under the most trusted label in modern investing: the target-date fund.

Fiduciaries should remember a simple principle:

If an investment structure could not comfortably survive traditional SEC mutual fund accounting and disclosure standards, there should be an extremely strong presumption against placing it inside a participant-directed retirement plan through weaker regulatory wrappers.

From a legal standpoint, income alone is not enough if there is an alternative strategy or product that better serves the plan participant’s best interest. As I have previously posted, a simple strategy of rolling Treasuries or CDs is better under a terminal wealth approach, as it provides income while preserving capital, something most annuities cannot match when annuitization is required. Terminal wealth approach is accepted as legitimate concept by the courts.

Yahoo Mail: Search, Organize, Conquer

LikeLike