Today, the retirement industry insists that if a product is somehow legal under lax state insurance rules or state banking laws and has a vague, weak ERISA exemption, then it somehow belongs inside a 401(k) plan. That logic is backwards.

A much better test is this: Could the product survive inside a fully transparent, federally regulated, SEC-registered mutual fund subject to daily fair-value accounting? If the answer is no, fiduciaries should immediately ask why.

That question is becoming increasingly important as Wall Street attempts to push private equity, private credit, insurance annuities, and other opaque contract-based products into retirement plans through CITs, insurance wrappers, and other structures exempt from the accounting standards applied to SEC mutual funds.

Ironically, the best historical example may be stable value itself.

The Forgotten Stable Value Mutual Funds

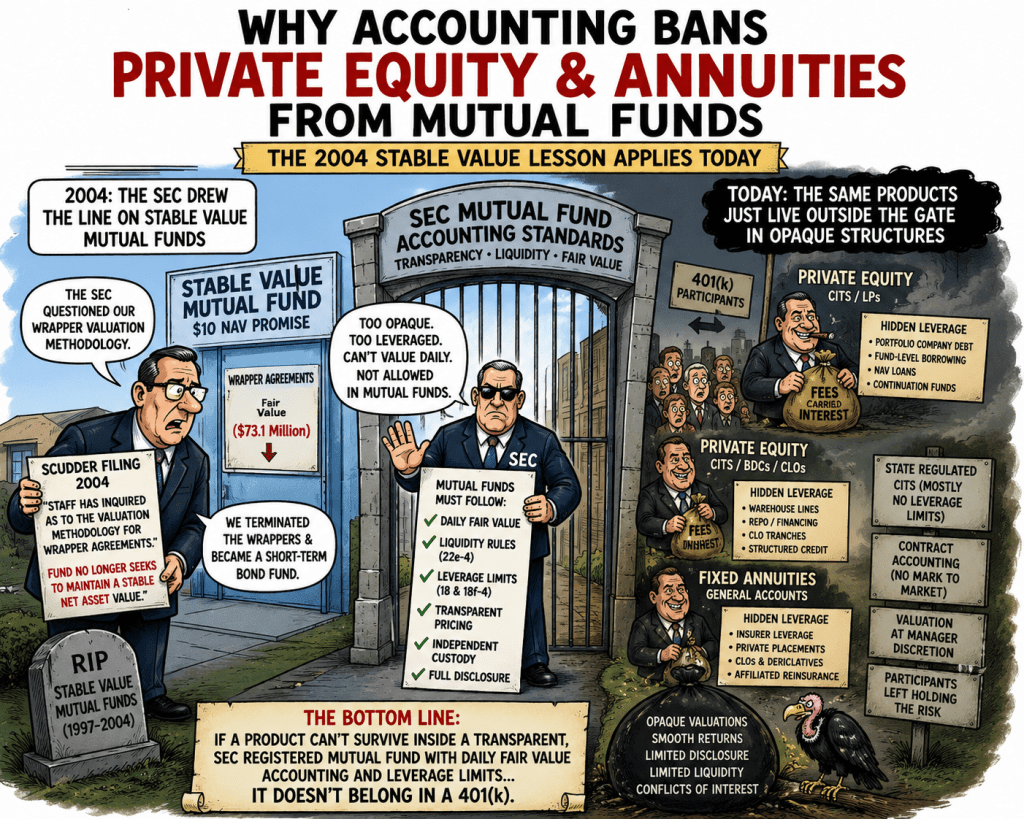

Most younger fiduciaries do not realize that from roughly 1997 to 2004, several firms attempted to operate synthetic stable value products inside SEC-registered mutual funds. They never even tried with fixed annuities. Deutsche/Scudder, Morley, PBHG, Pilgrim Baxter, Dwight and others experimented with structures that used wrap contracts and book-value accounting techniques inside registered investment companies. It was basically 95% SEC short bond fund and 5% insurance wrapper. I remember because I was the wrapper.

The experiment quietly failed. Not because participants lost money. Not because the underlying bond portfolios collapsed.

But because the SEC accounting framework could not comfortably accommodate book-value insurance accounting inside a daily NAV mutual fund structure.

One of the most important historical documents is a 2004 SEC filing from Scudder/Deutsche involving the Scudder PreservationPlus Income Fund.

The filing states:

“The staff of the Securities and Exchange Commission has inquired as to the valuation methodology for Wrapper Agreements utilized by ‘stable value’ mutual funds, including this Fund.”

That sentence is extraordinary.

The SEC staff was directly questioning the accounting treatment of wrapper agreements used by stable value mutual funds. The filing further explained that if the SEC required the wrappers to be valued differently, the fund would no longer be able to maintain a stable NAV.

Then came the real admission. Effective November 17, 2004:

“the fund no longer seeks to maintain a stable net asset value per share”

And “terminated all of its wrapper agreements … and effectively became a short-term bond fund.” The stable value mutual fund structure effectively disappeared shortly thereafter.

The Real Problem Was Accounting

This is one of the most misunderstood episodes in retirement-plan history.

The issue was not necessarily that the underlying bonds were impaired. In many cases, market-to-book values were manageable or even positive. Providers could quietly unwind the wraps and transition the products into short-duration bond funds without creating participant panic.

The problem was structural.

Stable value depended on:

- book-value accounting,

- contract-value reporting,

- insurance-style smoothing,

- and wrapper agreements whose economics did not fit naturally inside a mutual fund built around daily fair-value NAV accounting.

That distinction matters enormously.

The Investment Company Act of 1940 is fundamentally a transparency regime. Mutual funds generally operate under:

- daily liquidity,

- observable valuation,

- mark-to-market discipline,

- independent custody,

- and fair-value accounting.

Stable value strained those rules.

And if a synthetic stable value had trouble surviving inside a registered mutual fund structure, then general account fixed annuities are dramatically worse.

Synthetic Stable Value Was the Furthest the SEC Would Go

The industry now portrays synthetic stable value as conservative and traditional.

Historically, however, synthetic stable value represented the outer boundary of what regulators were willing to tolerate inside transparent investment structures.

Synthetic stable value at least had:

- externally plan owned bond portfolios,

- independent trusts,

- observable fixed-income assets,

- and some degree of market transparency.

General account annuities eliminate even those protections.

Under a traditional general account GIC:

- the insurer owns the assets,

- the insurer controls valuation,

- the insurer controls liquidity,

- participants become exposed to insurer solvency,

- spreads are opaque,

- private assets may be self-rated,

- and fiduciaries cannot independently observe underlying economics.

From an accounting perspective, general account annuities are far further removed from SEC mutual fund standards than synthetic stable value ever was.

The Same Accounting Arbitrage Is Happening Again

The stable value mutual fund story is not ancient history.

It is the blueprint for what is happening today with:

- private equity,

- private credit,

- insurance annuities,

- interval funds,

- target-date CITs,

- and insurance-based retirement products.

Products that struggle under SEC accounting standards increasingly migrate into structures like State Regulated Insurance and State Banking-regulated CITs where:

- fair-value discipline weakens,

- disclosures decline,

- liquidity assumptions soften,

- Benchmarking becomes manipulable,

- and fiduciary oversight becomes more difficult.

The common denominator is not diversification.

It is accounting arbitrage.

Wall Street increasingly seeks products that cannot survive under ordinary mutual fund transparency rules because opaque accounting produces:

- higher fees,

- smoother reported returns,

- hidden leverage,

- spread extraction,

- and greater control over valuation.

That is not modernization.

It is a regression.

A Useful Fiduciary Test

The retirement industry spends enormous energy debating whether products technically qualify for ERISA exemptions.

Fiduciaries should ask a more important question:

Would this product survive inside a fully transparent SEC mutual fund subject to daily fair-value accounting and independent valuation standards?

If the answer is no, that is not automatically proof of a prohibited transaction.

But it is a major warning sign.

The stable value mutual fund collapse of 2004 suggests regulators themselves became uncomfortable with stretching SEC accounting rules even for synthetic stable value products that were far more transparent than modern general account annuities, private credit vehicles, and private equity structures now being pushed into 401(k) plans.

The further a product must migrate away from SEC accounting standards and toward opaque contractual accounting systems, the more likely it is that the product’s economics depend on conflicts of interest, hidden spreads, valuation discretion, or fiduciary opacity.

That is exactly the environment ERISA’s prohibited transaction rules were designed to prevent.

SEC 2004 filing on Scudder/Deutsche https://www.sec.gov/Archives/edgar/data/906619/000008805304001111/

https://commonsense401kproject.com/2026/04/03/dol-401k-fiduciary-rule-enables-accounting-fraud/

https://commonsense401kproject.com/2025/08/12/4-sets-of-books-how-trumps-401k-push-opens-the-door-to-accounting-chaos/ and my newest

New Phoenix/LPL Litigation Strengthens the Case Against Fixed Annuities in 401(k) Plans

ERISA Private Equity Fiduciary Due Diligence Checklist

Target Date Fund Fiduciary Due Diligence Guardrail Checklist

ERISA Fixed Annuity Due Diligence Checklist