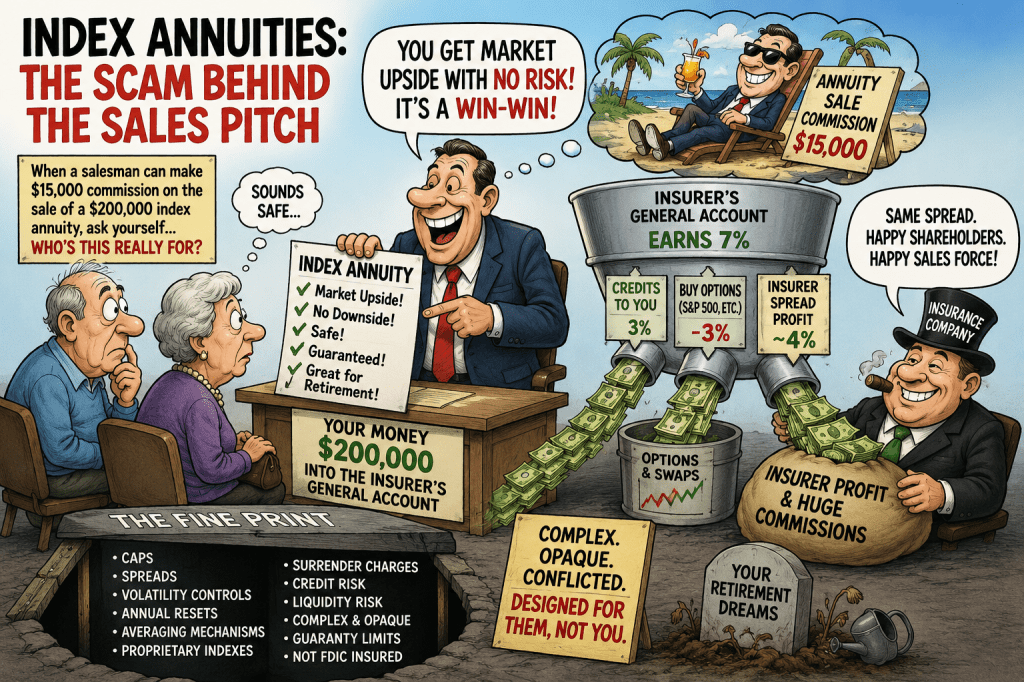

When a salesman can make a $15,000 commission selling a $200,000 indexed annuity, common sense tells you something is wrong.

That money does not magically appear.

It comes from hidden spreads, opaque options pricing, surrender charges, insurance company profits, and risks that most retirees never understand.

I know because I helped build these products at Transamerica.

Indexed annuities are not sophisticated market miracles. They are essentially traditional fixed annuities wrapped with derivatives and marketing gimmicks.

The core structure is remarkably simple. And they offered inside and outside ERISA plans

The insurer places your money into its General Account (“GA”), the same insurance company balance sheet used for ordinary fixed annuities. The insurer then invests that money in bonds, private credit, mortgages, structured products, and other assets designed to generate a spread.

Suppose the insurer’s General Account earns 7%.

With a traditional fixed annuity, the insurer may credit the retiree only 3%, while keeping roughly 4% as spread profit.

With an indexed annuity, the insurer instead uses part of that 7% return to purchase options or swaps tied to the S&P 500 or another index. Often these options cost around 3%.

That leaves the insurer with the same approximate 4% spread.

Part of that spread funds massive commissions to salespeople. The rest becomes insurance company profit.

The retiree sees advertisements promising “market upside with no downside risk,” but the economics are designed primarily to enrich insurers and distributors.

The entire product is engineered backward from the commission structure.

The problem becomes even worse when retirees believe they are receiving stock market exposure.

They are not.

The insurance company is usually purchasing short-term call options, option spreads, or swaps with severe limitations:

- Participation caps

- Spread deductions

- Volatility controls

- Complex crediting formulas

- Annual resets

- Averaging mechanisms

- Index substitutions

- Proprietary indexes

These restrictions dramatically reduce the actual market participation received by investors.

Many in the retail versions discover years later that when the stock market rises 20%, their indexed annuity may credit only 4% or 5%.

Meanwhile the insurer still collects its spread.

The insurance industry markets indexed annuities as “safe,” but the underlying risk remains tied to the solvency and liquidity of the insurer’s General Account.

That means retirees are exposed to:

- Credit risk

- Liquidity risk

- State insurance guaranty limits

- Complex surrender charges

- Opaque accounting

- Illiquid private credit portfolios

- Commercial real estate exposure

- Structured finance exposure

The same concerns I have raised regarding fixed annuities inside ERISA plans apply equally — and often more severely — to indexed annuities.

The industry itself effectively admits this in its own lobbying documents.

In comments submitted to the U.S. Department of Labor, the Indexed Annuity Leadership Council argued aggressively that indexed annuity sales should not be treated as fiduciary investment advice under ERISA.

Why?

Because once fiduciary standards apply, the conflicts become impossible to defend.

The industry specifically complained that:

- commissions create conflicts,

- rollover recommendations could become prohibited transactions,

- insurers cannot adequately supervise independent agents,

- and fiduciary standards would interfere with sales practices.

That is an extraordinary admission.

The indexed annuity industry is essentially arguing:

“We cannot operate profitably under true fiduciary standards.”

The Department of Labor should recognize that indexed annuities present the same fundamental prohibited transaction and conflict concerns as fixed annuities:

- insurers acting as parties in interest,

- hidden spreads,

- conflicted compensation,

- opaque valuation,

- illiquidity,

- and products too complex for ordinary retirees to understand.

The reality is simple.

If a product requires:

- giant commissions,

- 100-page disclosures,

- derivative overlays,

- surrender penalties,

- proprietary indexes,

- and armies of lobbyists arguing they should not be fiduciaries,

it is probably not designed for the benefit of retirees.

It is designed for the benefit of the insurance industry.

Appendix: The Chicago Fed Shows How Private Equity Turned Indexed Annuities into a Private-Credit Funding Machine

An April 27, 2026 Federal Reserve Bank of Chicago working paper provides unusually direct evidence about the business model behind the rapid growth of indexed annuities sold by private-equity-owned insurers.

The paper does not call indexed annuities a scam. Its authors examine insurer balance sheets and market share rather than consumer suitability, commissions, or sales abuses. But their findings reinforce the central argument of this article: the indexed annuity is not primarily a stock-market investment for the consumer. It is an opaque insurance liability designed to provide insurers and their private-equity owners with profitable, long-duration funding for private credit.

Private equity doubled its share of the indexed annuity market

The Fed researchers found that private-equity-owned insurers increased their share of the overall annuity market from 8.5% to 18% between 2017 and 2024.

The concentration was much greater in indexed annuities. Their share of indexed annuity premiums more than doubled from 16% to 33%.

The authors estimate that increased investment in financial-sector and privately placed asset-backed debt accounted for:

- approximately 61% of the increase in PE-owned insurers’ overall annuity market share; and

- potentially all of their increase in indexed annuity market share.

This is not a minor correlation. The paper’s central finding is that the transformation of insurer assets into private credit helped PE-owned insurers capture the indexed annuity market.

The customer hears “stock-market upside.” Private equity sees permanent capital.

Indexed annuities are sold with references to the S&P 500, proprietary indexes, participation rates, bonuses and protection from market losses.

That sales presentation can leave consumers believing their money is meaningfully invested in the stock market. It generally is not.

The purchaser gives money to an insurance company. The insurer places the premium in its general account, invests most of it in debt instruments and uses a relatively small portion of the economics to obtain index-linked exposure. The purchaser receives only the return calculated under the insurer’s contract formula, subject to caps, spreads, participation rates, volatility controls and other restrictions.

The Chicago Fed paper explains what increasingly happens to the larger pool of money behind that promise.

Life-insurer private placements grew from $386 billion in 2014 to $849 billion in 2024, reaching approximately 14% of general-account assets. Private-equity-owned insurers were the main force behind that expansion. After PE takeovers, their private-placement allocation increased far more than that of traditional insurers.

The PE firms did not simply buy insurers to sell insurance. They valued annuity liabilities as a form of long-duration, relatively illiquid capital that could fund their investment operations.

The economic chain increasingly looks like this:

Retiree’s savings → indexed annuity → insurer general account → private placements and structured credit → income and fees for the private-equity complex

The index is the marketing wrapper. Private credit is a major part of the economic engine.

Indexed annuities are especially useful for this model

The Fed paper finds that the results are concentrated in indexed annuities because they generally have shorter terms than many traditional annuity liabilities—often approximately five to ten years—and their credited returns vary with market conditions.

PE-owned insurers increased their holdings of:

- floating-rate private placements;

- private debt issued by financial companies and private-credit funds;

- privately placed asset-backed securities; and

- shorter-maturity private credit that better matches indexed annuity liabilities.

Insurers with the largest indexed annuity businesses held substantially more private placements and floating-rate debt. Their private placements generally had maturities about two years shorter than those held by insurers without indexed annuity businesses; the difference for floating-rate investments was approximately two and a half years.

The insurers in the highest indexed-annuity market-share group allocated an additional 7.1 percentage points of general-account assets to private placements and more than 8 percentage points more to floating-rate investments than insurers without indexed annuity business.

The product and the asset strategy were built for each other. The indexed annuity gave PE-owned insurers a liability whose duration and cash flows could be matched with higher-yielding private credit.

The takeover comes first. The private credit follows. The indexed annuity sales follow later.

The timing is particularly important.

The researchers found no evidence that private-equity firms merely purchased insurers that were already expanding aggressively into private placements. Instead, the asset allocation changed after the takeover.

Private-placement investment increased almost immediately following PE ownership. The increase in annuity market share generally appeared about three years later. After five years, the average acquired insurer had increased its indexed-annuity usage by approximately 15 percentage points.

That sequence supports a straightforward interpretation:

- Private equity acquires or controls the insurer.

- The insurer shifts assets into private placements, structured credit and floating-rate debt.

- The insurer uses the higher yields and better liability matching to offer more competitive indexed annuity terms.

- Indexed annuity sales increase.

- More consumer money becomes available to fund the private-credit strategy.

The Fed paper therefore documents more than simultaneous growth. It presents evidence that the private-credit transformation helped drive the later expansion of indexed annuity sales.

Many of the investments are tied to affiliates

The conflict becomes more serious because PE-owned insurers do not always purchase private credit from unrelated borrowers in an open market.

The paper finds that they hold significantly more debt issued by affiliated entities—companies or financing vehicles controlled by the same parent organization as the insurer.

Of the $82 billion increase in privately placed asset-backed securities from 2017 through 2024, approximately $50 billion was issued by financing vehicles affiliated with PE-owned insurers.

The paper identifies approximately:

- $21 billion associated with Athene and Apollo-related entities;

- $18 billion associated with KKR’s Global Atlantic; and

- approximately $10 billion associated with Blackstone’s Everlake and Resolution Life operations.

PE-owned insurers had an affiliated-investment allocation approximately 2.5 percentage points of general-account assets higher than other insurers. Their affiliated private-placement allocation was approximately 1.8 percentage points higher.

This means that the private-equity parent can potentially operate on several sides of the transaction:

- control the insurer collecting annuity premiums;

- control or advise the entities originating the private assets;

- place those assets into the insurer;

- earn asset-management or structuring fees;

- earn the spread between the investment return and what is credited to the annuity holder; and

- benefit from the increased value and market share of the insurer.

Even where each transaction is technically permitted, the conflicts are structural. The consumer buying the annuity may receive little meaningful disclosure about the affiliated entities, embedded fees or financial interests flowing through this chain.

The extra yield is compensation for risks the sales pitch hides

Why are these private investments valuable to an indexed annuity provider?

They pay more.

The Fed researchers found that private placements produced yields as much as 80 basis points above comparable public corporate bonds. Privately placed asset-backed securities had spreads approximately 156 basis points higher, compared with about 82 basis points for public ABS.

That additional yield can support:

- more attractive initial participation rates;

- larger promotional bonuses;

- higher agent commissions;

- greater insurer spreads;

- affiliated asset-management fees; and

- greater profitability for the PE owner.

But the yield does not appear from nowhere. It reflects risks and costs.

Private placements were only about half as likely to trade in a quarter as comparable public bonds. Privately placed ABS were sold at approximately half the rate of CLOs. Transactions frequently occurred over the counter, sometimes through small brokers with limited balance-sheet capacity.

The paper also finds that private placements were more likely to become distressed, although less likely to reach a formal default. One possible explanation is that private debts are renegotiated rather than immediately declared in default. That may delay loss recognition while imposing restructuring and workout costs.

The insurer earns an illiquidity and complexity premium. The annuity holder supplies the locked-up money that makes it possible.

The surrender charge is part of the funding structure

Indexed annuity surrender periods are commonly described as consumer-behavior controls or compensation for the insurer’s acquisition costs.

The Fed findings suggest another economic purpose.

A long surrender schedule helps stabilize the insurer’s liabilities while the company invests the premiums in assets that may be difficult to sell. The consumer’s inability to freely withdraw money is what permits the insurer to hold less-liquid private placements and capture the higher spread.

The consumer therefore bears two related constraints:

- the investment assets behind the annuity may be illiquid; and

- the consumer’s contract is made illiquid through surrender charges and withdrawal restrictions.

The insurer receives the illiquidity premium. The consumer receives a complicated index-crediting promise that the insurer can modify within the contract’s permitted limits.

The marketing promise and the economic reality are almost opposites

The typical sales pitch emphasizes simplicity:

You cannot lose when the market falls, and you participate when the market rises.

The Fed paper reveals a much more complicated economic reality:

Your retirement savings become an illiquid general-account liability used by a PE-controlled insurer to fund private debt, structured vehicles and sometimes affiliated borrowers. The insurer keeps the investment spread and gives you a contractually restricted portion of an index calculation.

The customer is shown an index.

The insurer owns private credit.

The agent receives a commission.

The private-equity organization may earn fees and profits at several levels.

The consumer receives whatever remains after the insurer applies the cap, participation rate, spread, volatility control, option budget and contract limitations.

The real question is not whether the index went up

The usual indexed annuity comparison asks whether the contract credited more than a bank certificate of deposit or avoided a stock-market decline.

That is too narrow.

The proper comparison should ask:

- What did the insurer earn on the assets supporting the contract?

- How much of that return was retained as spread?

- How much was paid to the selling agent?

- How much was paid to affiliated asset managers, originators and structuring entities?

- How much of the portfolio consisted of illiquid private placements?

- How much was invested in affiliated debt?

- What portion of the higher yield represented credit, valuation or liquidity risk?

- Could the purchaser have earned a better transparent return using Treasury securities, low-cost bond funds and low-cost equity index funds?

- Was the index designed to illustrate attractive back-tested results that are unlikely to be reproduced after fees and option costs?

- Can the insurer reduce future participation rates or otherwise make the contract less favorable after the purchaser is locked into the surrender period?

Without answers to those questions, an indexed annuity illustration reveals little about the actual economics of the transaction.

What the Fed paper proves—and what it does not

The study does not prove that every private placement will default. It does not conclude that every PE-owned insurer is insolvent, nor does it analyze whether every indexed annuity sale is unsuitable.

What it does demonstrate is highly significant:

- PE ownership caused major changes in insurer investment behavior.

- Those insurers moved aggressively into less-liquid private credit.

- They had greater access to debt issued by affiliates.

- The investments paid higher yields.

- The higher-yielding private assets helped PE-owned insurers capture annuity market share.

- The effect was overwhelmingly concentrated in indexed annuities.

- Private-credit growth may explain all of the increase in PE-owned insurers’ indexed annuity market share.

That makes indexed annuities much easier to understand. Their extraordinary growth is not simply evidence that retirees demanded better protection from stock-market losses.

It is also evidence that private equity found a product capable of converting household retirement savings into stable funding for private credit.

Minimum disclosure that should be required

Before an indexed annuity is sold, the purchaser should receive a plain-language disclosure showing:

- The insurer’s controlling owners and affiliated asset managers.

- The percentage of general-account assets invested in private placements, private ABS, private credit and affiliated securities.

- All compensation paid to the agent and distributor.

- All investment-management, origination, servicing and structuring fees paid to affiliates.

- The insurer’s actual general-account investment return compared with the amount credited to policyholders.

- The guaranteed minimum participation rate, cap and spread after the initial promotional period.

- The insurer’s authority to change those terms.

- The surrender value for every contract year.

- The proportion of the supporting portfolio that lacks observable market prices.

- The protections available if the insurer fails—and the material differences between state guaranty associations and federal PBGC insurance.

Consumers are currently asked to evaluate pages of index formulas while the more important information—the insurer’s assets, affiliates, conflicts, spreads and liquidity risks—remains largely hidden.

Bottom Line

The Chicago Fed paper supplies the missing institutional explanation for the indexed annuity boom.

Private equity did not merely acquire insurance companies and continue the traditional insurance model. It changed insurer portfolios, expanded lending to private financial intermediaries and affiliated vehicles, and used indexed annuities to capture a larger stream of consumer savings.

The index is what sells the product.

The surrender charge stabilizes the funding.

Private credit generates the spread.

Private equity captures much of the value.

And the retiree is left holding an opaque promise from an insurer whose real investment strategy may bear little resemblance to the stock-market story used to make the sale.

From “Life Insurers’ Private Credit Investments and Annuity Market Share Capture,” Ralf R. Meisenzahl, Jackson Overpeck, and Andy Polacek. WP 2025-09 REVISED April 27, 2026 https://doi.org/10.21033/wp-2025-09